LH - Laboratory Corporation: Predictability Of Cash Flows Less Visible

2023-06-20 22:33:26 ET

Summary

- Laboratory Corporation has visible headwinds to growth ahead.

- The company's return on capital employed has lagged behind the required rate of return in the last two periods.

- Net-net, reiterate that LH stock is a hold, valuation of $221.

Investment Summary

After paring back the position on Laboratory Corporation of America Holdings (LH) to buy from hold, it was time to revisit the investment thesis given it had been: 1) 3 months of trading activity, and 2) there have been several updates in the critical facts.

In the last LH publication , I revised the thesis down on a number of fundamental and economic factors, namely:

- Potential headwinds to growth coupled with a lack of viable investment opportunities to grow intrinsic value.

- Breakdown in post-tax margin coupled with substantial reduction in asset utilization and capital intensity.

- Unsupportive valuations, just 13% margin at the time of safety on a 9% projected earnings yield.

- Significant haircut to profitability in recent periods despite substantial increases in turnover from Covid-19-related sales. I would expect LH to be deploying the extra income at tremendously high rates of return.

There were a few more points as well, but the point is my sentiment, along with the market's has been revised lower on the company. Net-net, my latest findings corroborate a hold thesis within my own investment criteria, that will be discussed at lengths here today. Net-net, I am reiterating LH as a hold at a $221 valuation.

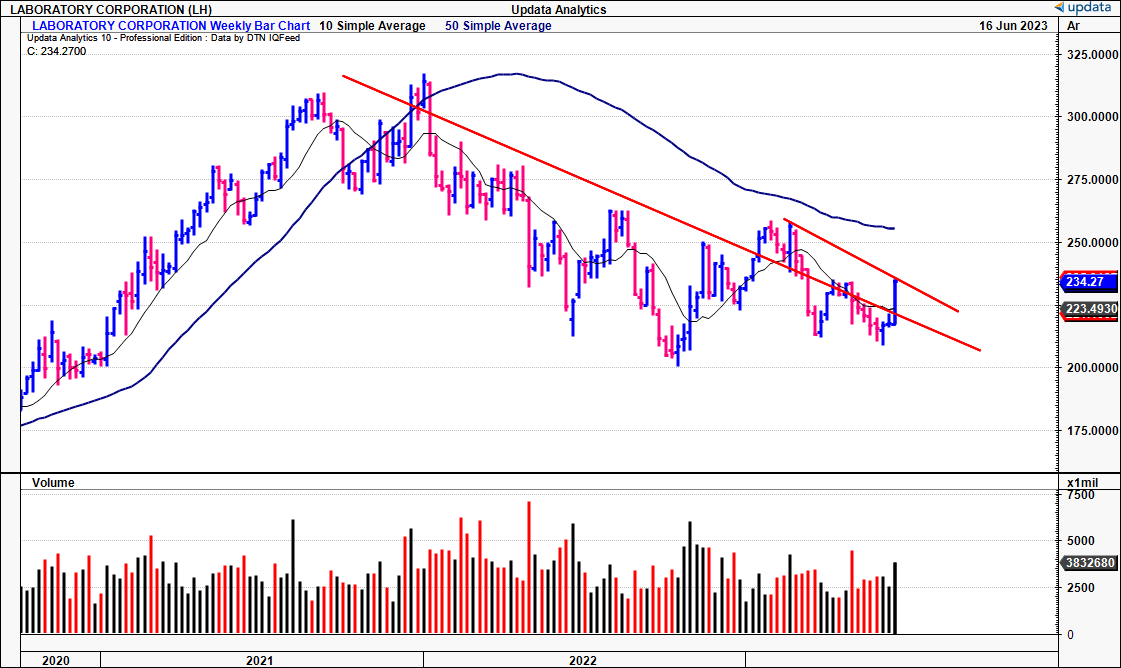

Figure 1. LH long-term price evolution, downtrend with recent breakout

{kind=link}

Data: Updata

Analysis of LH value drivers

The company is best looked at in terms of its prospects at compounding its intrinsic valuation (and therefore market valuation) over time. In that vein, there are fundamental, economic, sentimental and valuation factors to consider in this investment debate. Chiefly, my estimates point to challenges in LH increasing its net worth over time.

(1). Fundamental value drivers

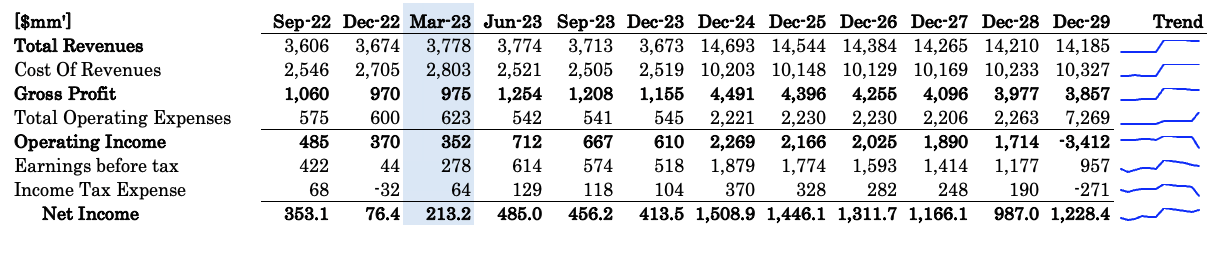

There are notable trends observed in LH's operating numbers. Most notably, the diminishing benefit of Covid-related turnover is felt quite extensively. Looking to its latest numbers, posted back in May , Q1 r evenue was $3.8Bn, a 3.1% decrease compared to Q1 FY'22. Management confirmed the decline was due to COVID testing demand. Notably, COVID testing sales were down 84% YoY, while the base business grew by 9.8%, showing the dichotomy.

- Additional quarterly takeouts:

- One point that is essential to bring to the forefront in my view, is that the acquisition of Ascension was expected to add ~$550mm–$600mm in revenue once fully integrated. Based on LH's current run rate, the clip could even be in-line or slightly ahead of this range this year. You'd be looking at a contribution of ~5% to the company's top-line growth this year by estimate.

- On the call , management said it had contributed ~7.5% YoY growth to the quarter, something to consider.

- Core business revenue pulled to 9.2% in "constant currency terms", excluding all FX headwinds, that is. Growth benefitted directly from the Ascension lab management agreement. This contributed ~4% of the Q1 upside. There is an important distinction to make when it comes to the deal's structuring as well. The outreach business [that was acquired from Ascension] is treated as an acquisition. However, the lab management agreement is considered organic growth on the income statement. Hence why I've separated the numbers here.

- It pulled this down to adj. operating income of $341mm or 9% of revenue. If you back out amortization and restructuring charges as one-off items, the adjusted income was $494mm, or 13.1% of turnover. Hence it is likely going to be a year of difficult comps for LH on the back of its Covid-19 tidal wave. You can note the pullback in operating margin, back to c.9% from 30% in December 2020.

Figure 2.

Data: Author, LH SEC Filings

(2). LH economic characteristics

There is no question of LH's profitability – $2.3Bn in TTM EBITDA, $11.13 in trailing earnings per share. The company, therefore, feeds big piles of cash down the income statement. Free cash to the firm was ~$1Bn in the TTM by the end of Q1, down from $1.2Bn two years ago, and off highs of $2.5Bn during the pandemic's height.

Question is, where has this cash been deployed? For one, it hasn't been any growth in dividends, implying the company foresees more profitable ways to add value for shareholders. Hopefully, anyway. Execution is the next question. Looking back to 2020, I've tabulated the capital employed by LH, and the corresponding post-tax earnings in Table 1. Trailing figures are used. You'll note there are fairly good results over this period– up to 20–22% return on existing capital over this time, averaging $2–$3Bn in earnings.

The more recent trends a slightly more concerning in my eyes, Q4 FY'22, and Q1 FY'23. For a couple of reasons, actually:

- One, without the Covid-19 "stimulus", the company hasn't beaten a 12% hurdle in the last 2 quarters (12.6% in December, not statistically meaningful).

- Two, the company's high free cash flows have been redeployed into more operating assets to grow operations. This hasn't materialized as of midway through Q2 2023. Forecasts don't imply a change from this either.

- Should these trends prevail, I don't see the company compounding its intrinsic value above the market's return on capital (I use 12% here as it is a fair representation of the long-term market averages. You might call it the required rate of return in this instance).

- Further, there's been just 6.6% incremental return on capital produced over this time, another $118mm in post-tax income from a $1.8Bn investment. That is a large factorial.

Table 1. LH return on capital employed to tangible assets has lagged the required rate of return in this instance

Data: Author, LH SEC Filings

Of course, these historical results – whilst valuable – do nothing in the way of future outcomes. What happens going forward matters to us most from here. On my estimates [shown in Appendix 1], it wouldn't be unreasonable to see LH pushing 12-15% ROIC over the coming 3–5 years. I would expect these on two reasons, one quantitatively, and one intuitively:

- As to the intuition, LH has been around since 1994, growing the business on aggregate each decade. There is no reason to see it "going away" at all. In that vein, it is likely the company will adapt to survive and start to put its balance sheet to work to pick up the pace. The question is how well, and how quickly.

- Forward estimates point to 12-15% compounding ROIC as mentioned, and would align with a longer-term growth rate, ex-Covid that is. Hence, you're not getting a company that's inefficiently allocating capital by any means. Au contraire, the company is profitable and defensive, as mentioned. However, in terms of what's in front of LH, its best days may either be behind itself or at another time in the future (just not now, in my view).

Table 2. Forward estimates on additional capital employed and return on capital employed.

Note: Numbers show estimated additional investment (CapEx + Intangibles + Acquisitions + NWC) LH will employ into FY'28. Estimated TTM figures are shown to December 2023, where annual estimates are shown thereafter. (Data: Author Estimates)

(3). Market-generated data

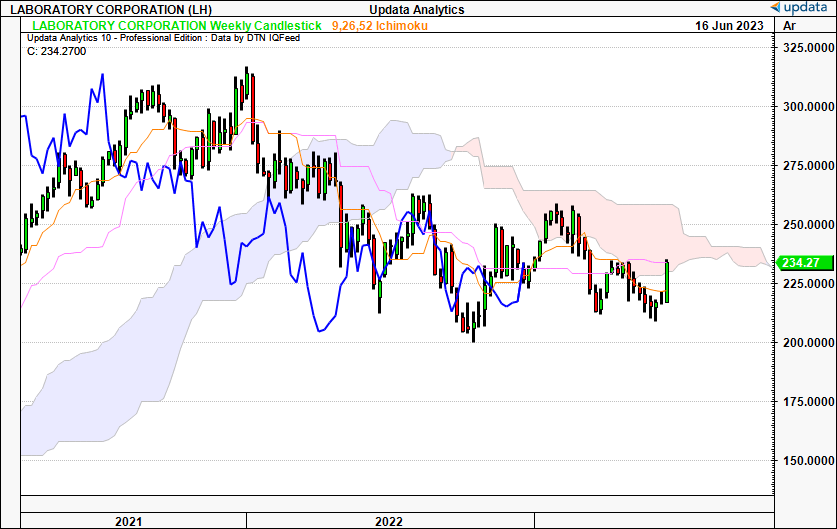

The persistent downtrend calls for an analysis to see where we are within the trend. Looking at Figure 2, you'll note the weekly cloud chart from 2021. The stock has been trading below the cloud for the good part of 18-months, and has just broken through the base.

You would need a break above $242 by August in my view, based on the chart below. Another thing to consider is the lagging line hasn't broken into the cloud yet, so there's no way to call it bullish yet, nor have either of the turning lines shown any major bullish action. Alas, this chart is neutral in my view, supportive of the fundamental thesis.

Figure 2.

{kind=link}

Data: Updata

It would be unsurprising to see that we have both downside and upside targets on LH on the daily point and figure chart studies. The stock has met the $226 target, adding to the fact a new upside objective may be generated. This would require another thrust of $20.7Bn, the current market value. There is a downside target to $172, but given the recent price action and short-term uptrend, I believe we can disregard this figure for the time being. It does show where the market got to in terms of its expectations of the company, however. Again, this is supportive of neutral.

Figure 3.

Data: Updata

Valuation and conclusion

On merit, there is some attractive value on offer in LH trading at 13x forward earnings and 10x forward EBITDA. These are 31% and 20% discount to the sector, respectively. Why has the market discounted LH below industry peers? One explanation we went through in this report is returns on capital invested and economic earnings.

However, it appears the market still hasn't fully discounted the fact there will be zero Covid-19 sales at some point in time (nil meaningful). Each down-step in YoY earnings of the FY'22 base has been priced lower in companies who are enduring this phenomenon– and in healthcare, medtech, medical devices et al., there are many, as you can imagine.

I've got LH at $14.6Bn in turnover at FY'24 to pull this down to $1.5Bn in earnings, but I believe this will roll off going forward. This is due to the factors discussed here on Covid-19 sales, returns on capital, but also the general economy. It is unpredictable at the moment, and it is wise to consider the potential for a broad slowdown.

At 13x forward this gets me to $221 at my FY'24 assumptions, well below the current market price (13x1,508/88.6 = $221.26). Is there reason to expect differently on LH, and prescribe a higher multiple? Not in my opinion. I've discussed ad nauseum the reasons why. And these all pertain to an investment cortex, one that is biased towards capital appreciation.

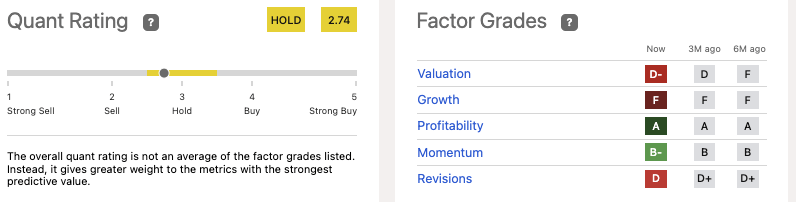

I would finally note that these findings are robustly supported in the objective data outlaid by the quant system. You can note the major downgrades in valuation and growth, consistent with my own findings. Further, there have been 11 downgrades to earnings in the last 3-months from analysts, supporting the flat sentiment. This supports a neutral viewpoint.

Figure 4. LH Quant grading system

{kind=link}

Data: Seeking Alpha

Net-net, after extensive review of the critical facts, there doesn't appear to be a major reason to change the rating from hold in my view. Investors have the option to allocate to numerous, highly profitable, highly valuable companies that are putting capital to work and recycling it back at 15-30% return each period. They are the benchmark, so I'd be looking to LH getting towards this range before becoming interested. That, and more evidence can overcome the intermediate "adjustment" over to a land of no Covid-19 revenue and keep up the value-add. Reiterate hold.

Appendix 1.

{kind=link}

Data: Author estimates

For further details see:

Laboratory Corporation: Predictability Of Cash Flows Less Visible