LIFZF - Labrador Iron Ore: Low Downside Risk With Production And Pricing Upside On High Grade Iron Ore Royalty

2023-05-18 09:48:54 ET

Summary

- Labrador Iron Ore Royalty Corporation (LIORC) currently trades at around a 10% trailing free cashflow yield, making it undervalued.

- Its stock price has upside from both possible higher prices and increased production.

- This upside is underlined by the important role its high-grade iron ore products will play in decarbonizing the steel industry.

- The downside risks are low as it is primarily a royalty company and is therefore well insulated from higher mining costs.

Thesis

LIORC (LIFZF) owns a royalty and equity stake in the Carol Lake high grade iron ore mine in Newfound and Labrador, Canada. It has no debt, low overhead and trades at around a 10% trailing free cashflow yield. It has high potential upside from price increases on the premium iron ore pellets it produces, which are essential for decarbonizing the steel industry. The mine has ample resources and there were previously plans by the mining operator, Rio Tinto (RIO), to increase iron ore production to 50 million tons annually, which is triple current production. Therefore, I think the stock could trade at multiples of its current stock price and rate it as a strong buy.

Company Overview

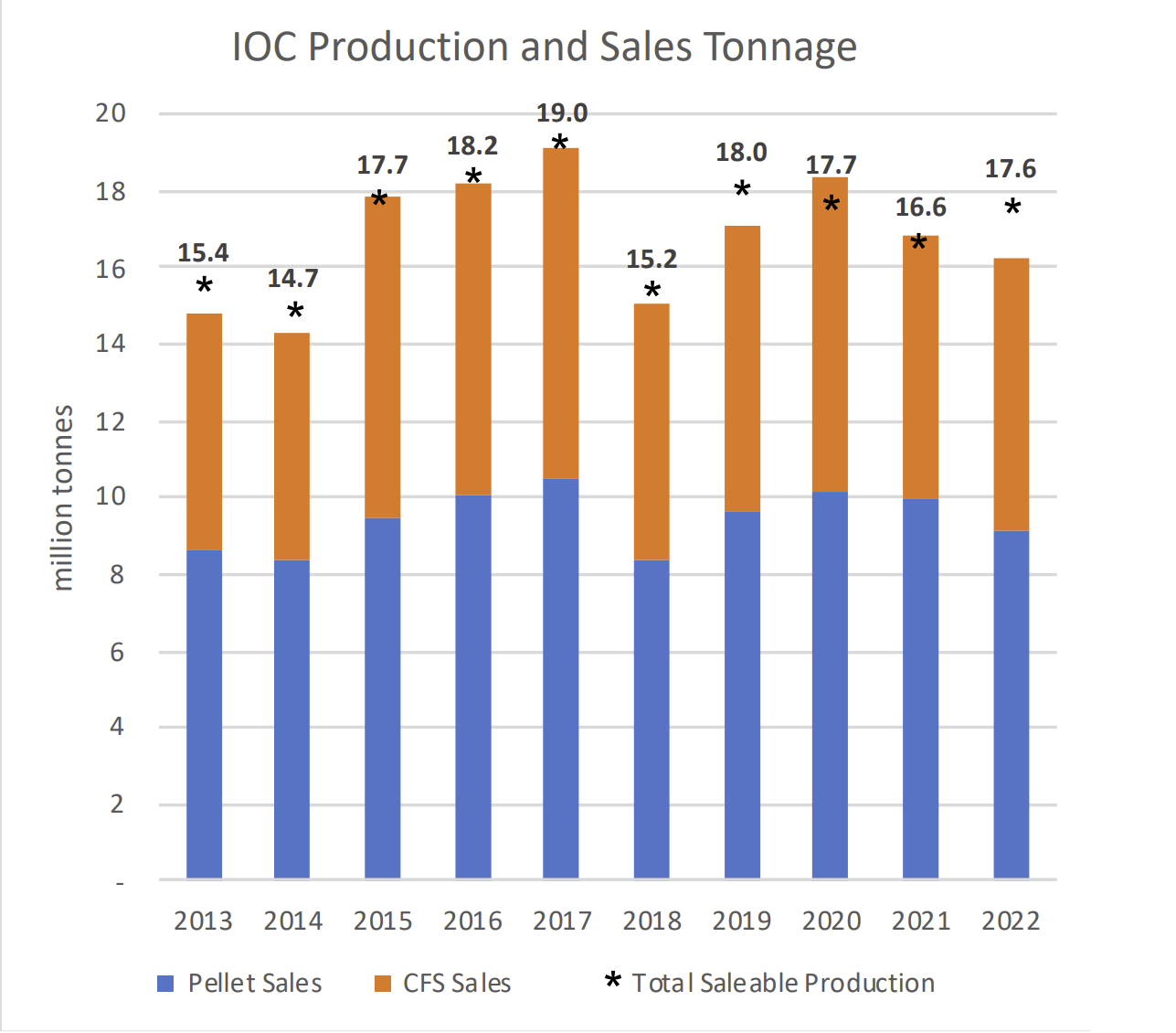

Labrador Iron Ore Royalty Company ((LIORC)) is a Canadian royalty company which owns a 15.1% equity stake in Iron Ore Company of Canada ((IOC)), a 7% top line royalty in IOC and C$0.10 per ton commission on all IOC iron ore sales. The proceeds from the royalty are relatively stable as they are based on company revenues, while the proceeds from the equity stakes are based on profits and are therefore highly leveraged to the price of iron ore. Over the last 10 years IOC has produced between 14 and 19 million tons of iron ore. This means that the LIORC per ton commission is fairly minor at around C$2 million per year. Production is roughly divided evenly between 65% iron ore grade concentrate for sale ((CFS)) and premium iron ore pellets. IOC produces both direct reduction and blast furnace pellets, which involve an extra processing step and therefore sell at a higher price compared to concentrate.

Rio Tinto, one of the world's largest mining companies, is the operator of IOC and it has been continuously operating for over 50 years without a shut down due to market conditions. IOC operates the Carol Lake mine close to Labrador City in Newfoundland and Labrador, Canada. It has a long mine life of 23 years based on reserves only, although it has resources available to continue operating for over 50 years. Furthermore, its nameplate capacity is 23 million tons of concentrate and 12.5 million tons of pellets, which means it has further immediate production upside. Rio Tinto has been making significant investments over the past couple of years to bring production up to nameplate capacity. The quality of the company is underlined by it being held by three other royalty companies. Franco-Nevada ( FNV ) and Ecora Resources ( ECRAF ) own 9.9% and 1.6% of LIORC respectively. Altius Minerals (ATUSF) purchased an additional 550,000 shares of LIORC in quarter 3 of 2022, bringing its ownership percentage up to 5.8%. Ecora Resources and Altius Minerals are the two main non-precious metals diversified royalty companies, and Altius' stake in LIORC is fairly significant, accounting for around 16% of its asset value.

Source: LIORC January 2023 Investor Presentation

{kind=link}

Company Financials

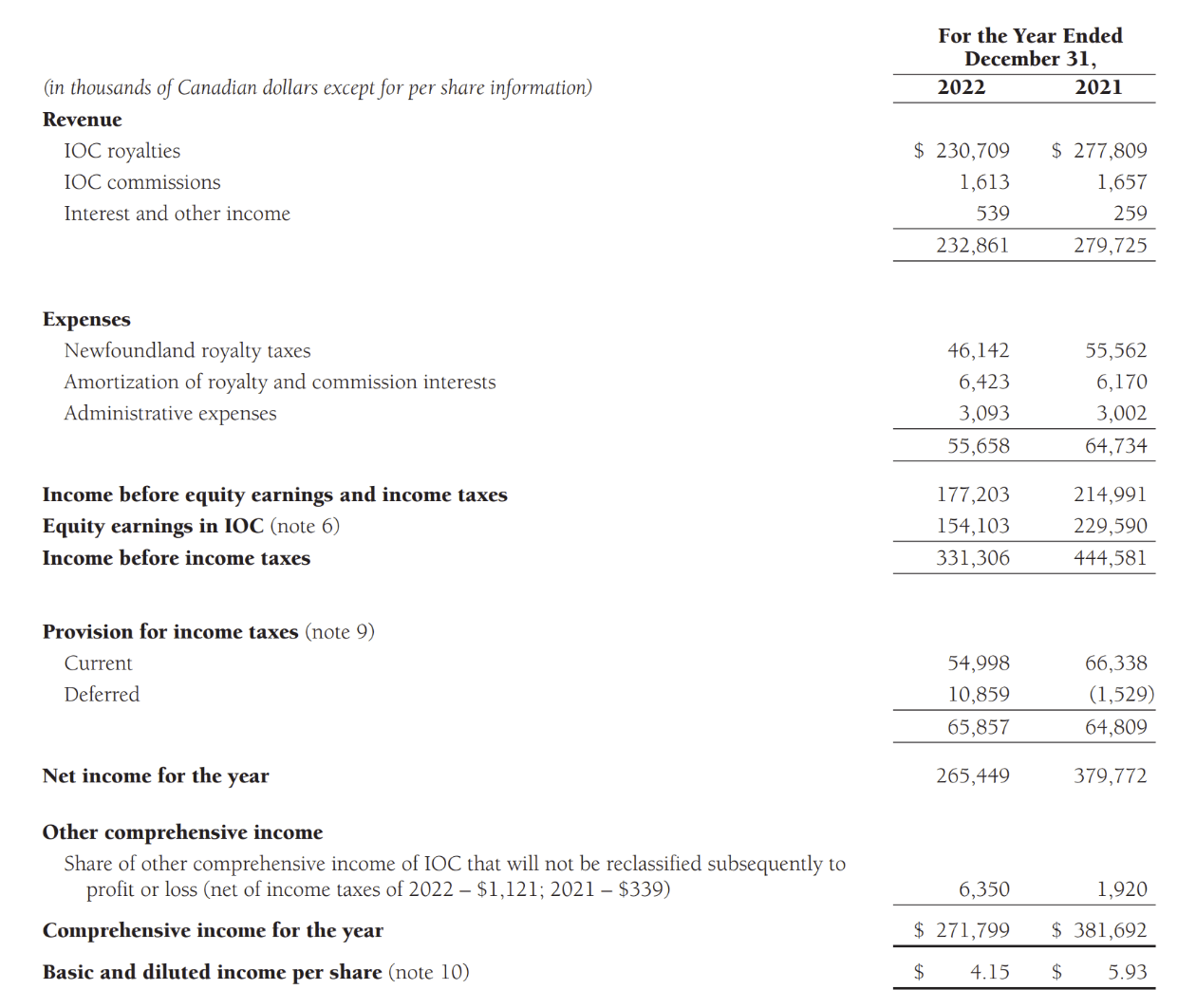

The financial statements of LIORC reflect its split royalty and equity ownership of IOC as well as its relationship to iron ore prices which have been falling since peaking in 2021. It receives revenues from its royalty (and per ton commission) and earnings from its equity stake in IOC. As the Q1 2023 financial statements are very high level, I will go over the 2022 Annual Report financial statements. For reference the Q1 2023 revenues were C$47.2 million and the Q1 2023 equity earnings from IOC were C$21.8 million. Its revenues fell from C$278 million in 2021 to C$231 million in 2022 due to lower iron ore prices. Due to higher leverage to the price of iron ore, its equity earnings fell more sharply from C$223 million to C$154 million. For reference, LIORC has 64 million shares, so revenues per share were C$3.6 in 2022 and equity earnings per share were C$2.4 in 2022. Its main expense category was Newfoundland royalty taxes, while G&A was relatively low at around C$3 million. Net income per share fell from C$5.93 in 2021 to C$4.15 in 2022. Net income does not include corporate taxes, so this has to be netted out to get free cash flow. As LIORC traditionally pays out all its free cash flow in dividends, this closely corresponds to the dividend amount. Dividends were C$3.10 per share in 2022 and 6.00 per share in 2021. Using a share price of C$30 (around US$22.5), gives a dividend yield of around 10% based on 2022 dividend, and around 20% based on 2021 dividends. For Q1 2023, LIORC paid out C$0.50 per share.

Source: Income Statement, LIORC 2022 Annual Report

{kind=link}

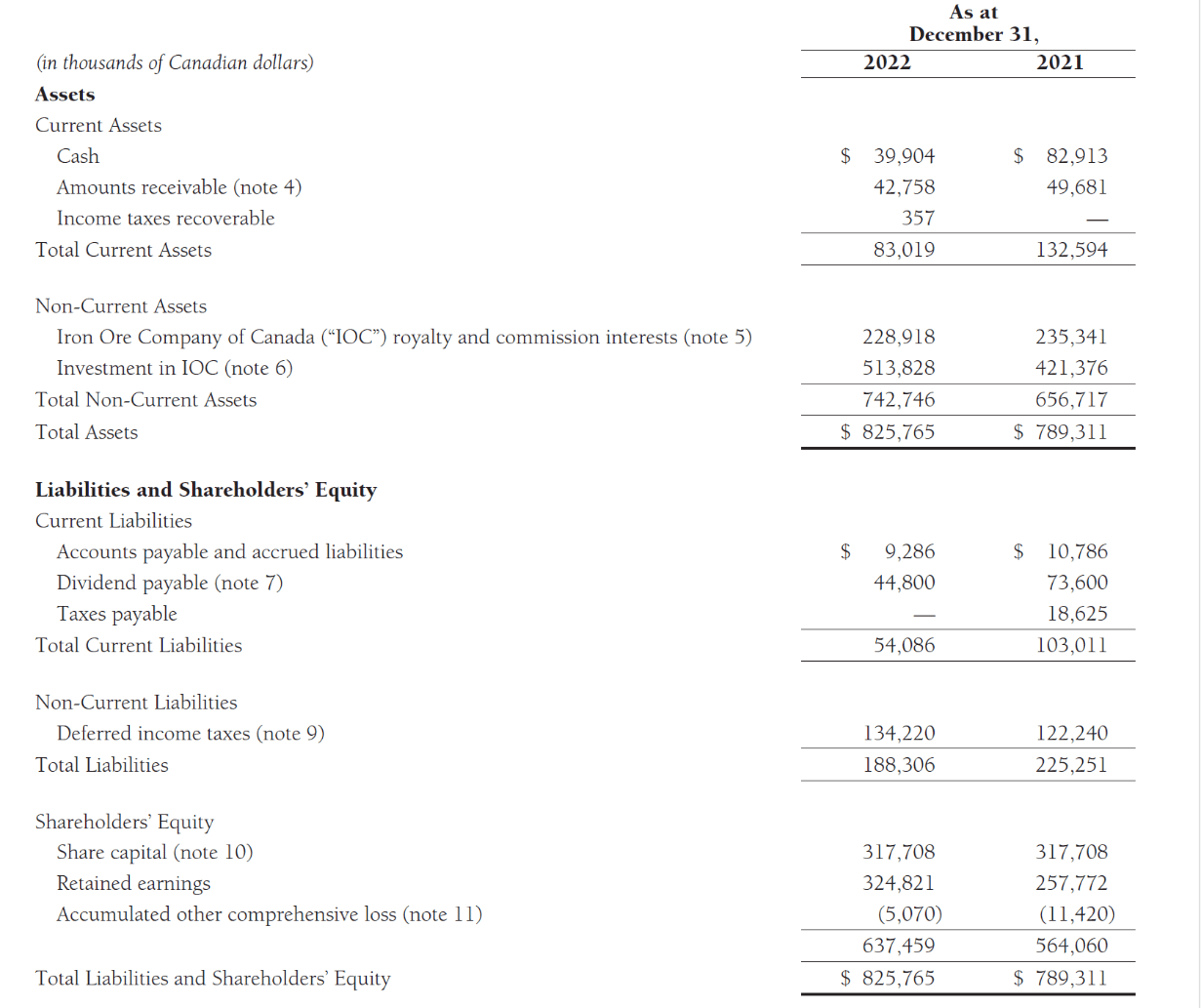

LIORC has no debt and had C$40 million in cash at the end of 2022 (see balance sheet statement below). It had assets worth around C$826 million of which the majority derived from its investment in IOC. Assuming stock price of C$30 (or US$22.5), this compares to a market capitalization of C$1,920 (or US$1,485), giving a P/NAV of 2.33 (1,920/826). This P/NAV ratio seems high, however, and is due to a very conservative valuation of the royalty and commission interest. This royalty interest generated around C$233 million last year which exceeds its stated value. Generally, royalty assets, particularly long-life royalty assets in safe jurisdictions such as Carol Lake, tend to trade at a minimum of 10 times revenues. Therefore, I would argue a more appropriate valuation for this asset is C$2,330 million. Using this updated asset valuation would give LIORC total assets of C$2,927 million. The resulting P/NAV of 0.66 (1,920/2,927) is below one, highlighting that LIORC is undervalued at its current share price.

Source: Final Position, LIORC 2022 Annual Report

{kind=link}

Company Valuation

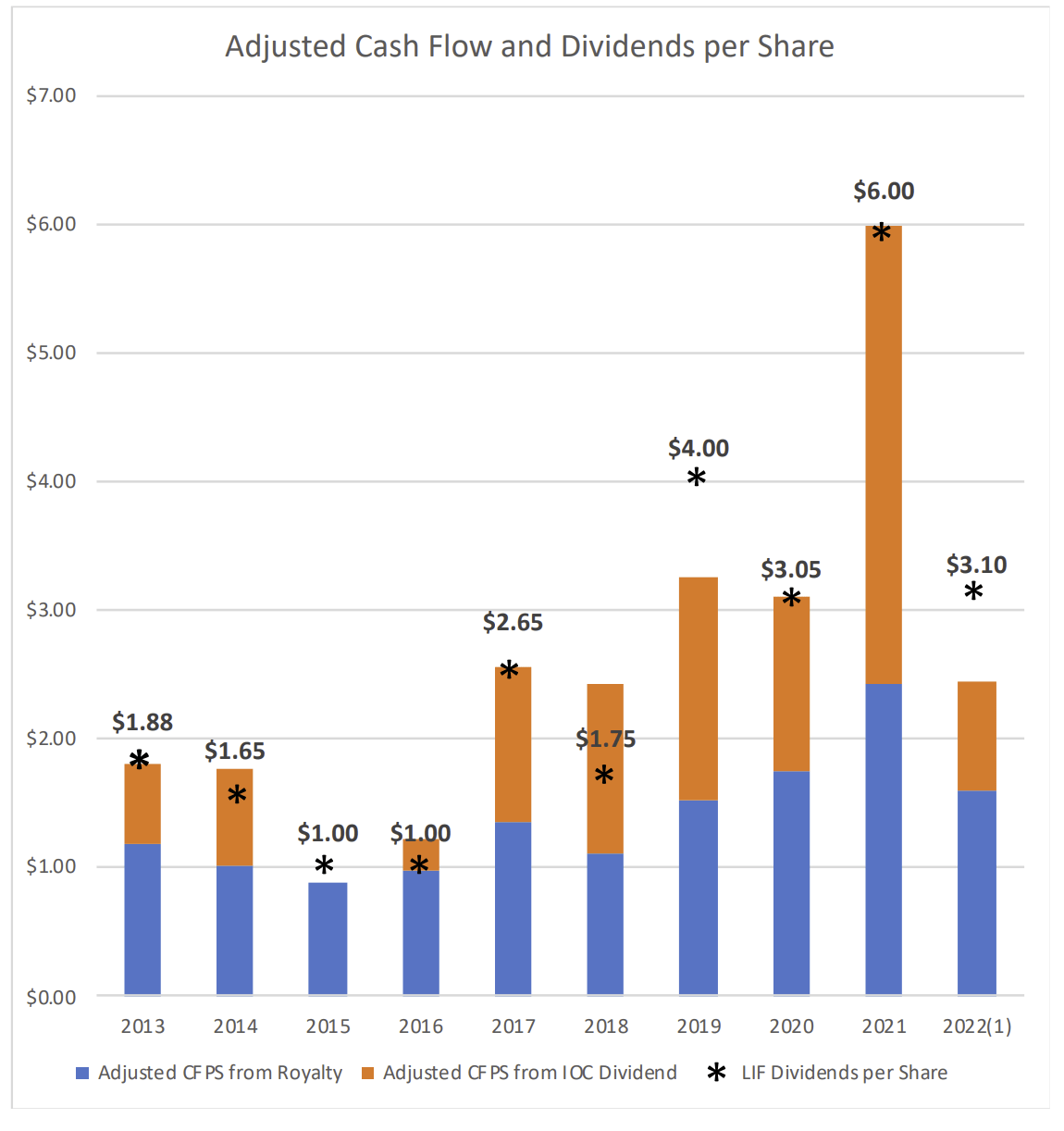

Given the fact that all cash generated by LIORC has historically been returned as dividends, this is a good way to value the company. The chart below shows dividends return over the past 10 years. From 2019-2022, annual per share dividends have exceeded C$3 or 10% based on as share price of C$30. Given the high rates of inflation that have occurred in the last few years, this is likely the floor in LIORC's valuation. LIORC's royalty is particularly valuable, as unlike mining companies, royalty companies benefit from inflation, as they benefit from the rises prices while not being exposed to rising costs. However, unlike other royalty companies, LIORC does have an equity stake in IOC, which is impacted by rising costs. Interestingly, though, there was only one year, 2015, out of the last 10, where LIORC did not receive a dividend from IOC, due to low iron ore prices. Even in that year though LIORC paid a dividend of C$1.

Source: LIORC January 2023 Investor Presentation

{kind=link}

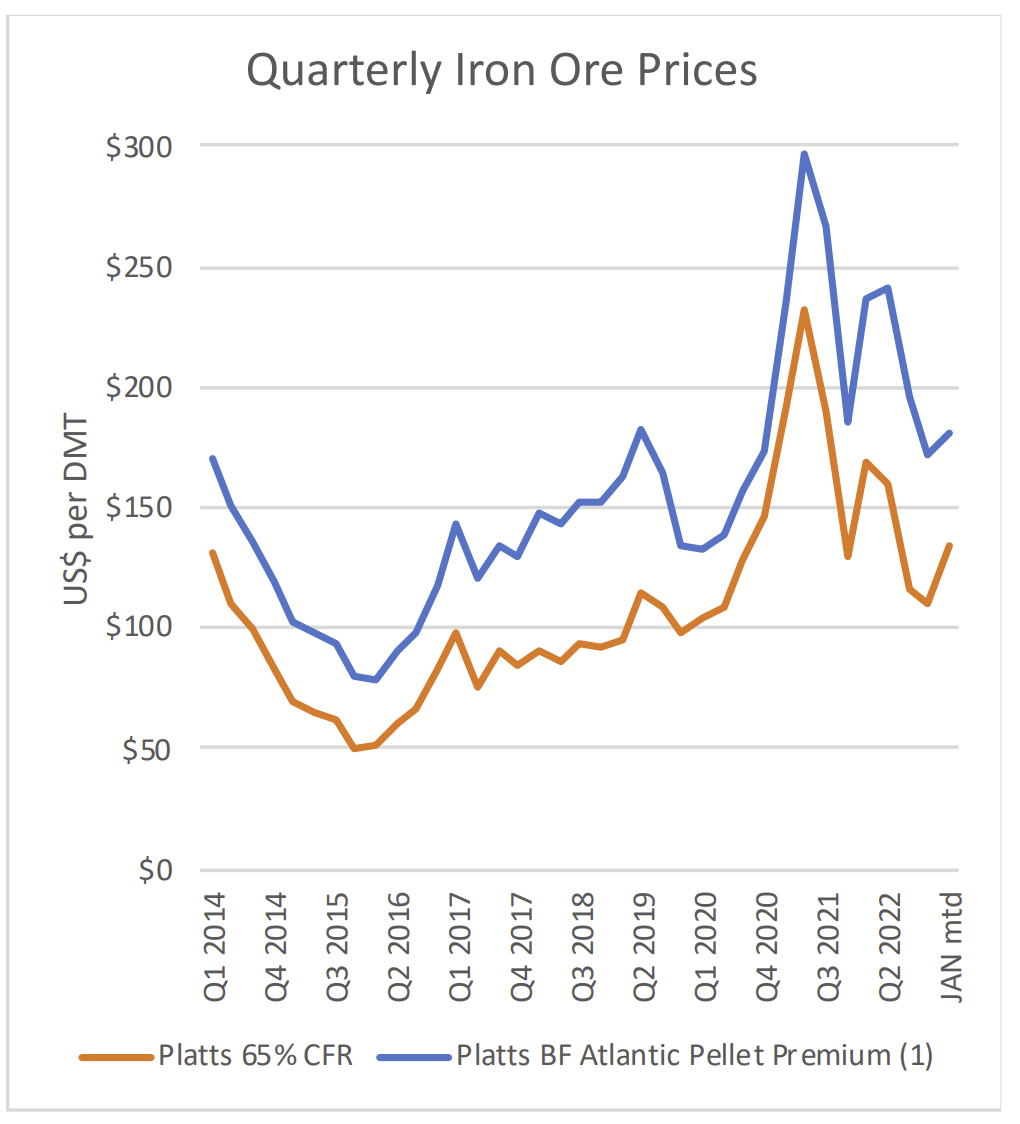

Looking at prices of the iron ore products LIORC sells, we can see the dip that occurred in 2015 and the spike that occurred in 2021. Moving forward, the valuation of LIORC depends on what the future prices of its products are. If the prices are at 2021 levels, LIORC would generate around a 20% dividend yield, while if prices are at 2015 levels, LIORC would generate around a 3% dividend yield. One potential argument that 2021 prices are more likely moving forward is the role high grade iron ore will play in decarbonizing the steel industry.

Source: LIORC January 2023 Investor Presentation

{kind=link}

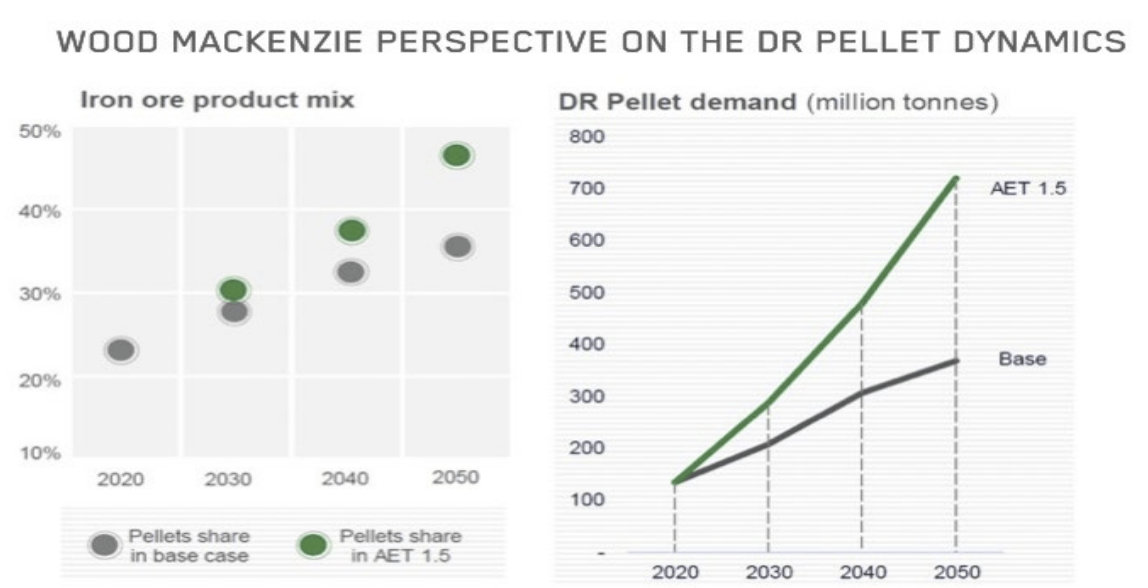

Due to a high use of steelmaking coal for making steel, the steel industry accounts for around 8% of all global carbon emissions . This contrasts with the much more widely discussed carbon emissions of the aviation industry, which current accounts for 3% of all global carbon emissions. There is an obvious solution to decarbonizing the steel industry, but it can currently only be implemented using high grade iron ore. The most common way to produce steel is by using a blast furnace, which requires steelmaking coal. However, steel can also be produced using an electric arc furnace which uses electricity rather than coal, and therefore can be decarbonized using electricity from carbon free sources. The electric arc furnace, though, requires direct reduced ((DR)) iron pellets, which can only be produced using high grade iron ore. Therefore, decarbonization of the steel industry would require a substantial increase in the DR pellet production. The chart below shows projected DR pellet demand under various carbon reduction scenarios. The high forecasted demand would be very bullish for the DR pellets IOC produces. In addition, IOC could upgrade all of its 65% iron ore grade concentrate for sale and blast furnace pellets to DR pellets, which would further increase IOC revenues and consequently LIORC royalties.

Source: Altius Minerals February 2023 BMO presentation

{kind=link}

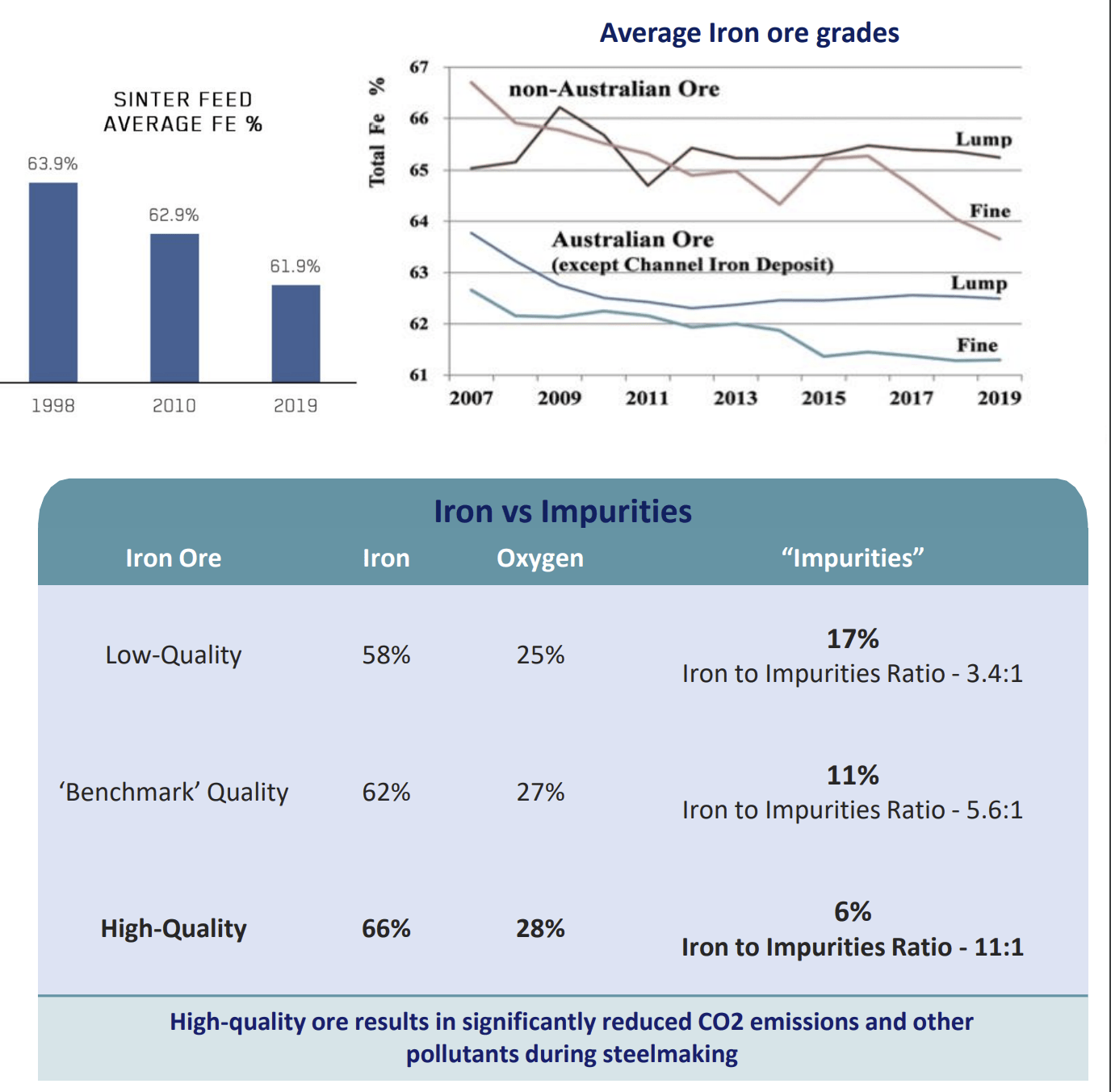

Lastly, there is an upside to LIORC from increases in IOC's nameplate capacity. Although, Rio Tinto has not announced any plans to expand IOC's nameplate capacity, it has become more reliant on IOC's high grade iron ore, as it blends it with its lower grade iron ore mined in Australia to increase its iron ore content. As can be seen on the graph below, all Australian producers, including Rio Tinto are vulnerable to declining grades in the iron ore mined in Australia. This low-grade iron ore is only suited for blast furnaces and requires more steelmaking coal as the iron ore grade declines, resulting in higher carbon emissions. Furthermore, IOC's Carol Lake mine is the only mine Rio Tinto operates that can produce feedstock for DR pellets. Therefore, there is an incentive for Rio Tinto to increase nameplate capacity and production at IOC.

Source: Altius Minerals 2022 Investor Day presentation

{kind=link}

Rio Tinto has previously contemplated increasing the nameplate capacity of IOC, most recently in 2011, during the last iron ore bull, when Alan Davies, Rio Tinto's president of international operations in iron ore, said the company was planning to more than double production, from 23 million tons to 50 million tons . Combining potential 2 times upside from higher prices and potential 3 times upside from higher production (as current production is around 17 million tons), and the general inflationary environment which LIORC benefits from, this stock could trade at multiples of its current price. Furthermore, there is plenty of iron ore at Carol Lake , which has mineral reserves and resources of 1.1 billion tons and 1.7 billion tons, respectively, with an average grade of approximately 38% iron.

Investment Risks

Regarding potential downside risks, the main risk would be a fall in the price of iron ore. This would not bankrupt the company, but would reduce dividends paid out, which would likely cause the stock price to fall. It would be more likely for IOC to go bankrupt, but this is still unlikely as it has been continuously operating for over 50 years. Rio Tinto could attempt to sell its stake in IOC, which it has mulled doing in the past, which would create an operator risk for IOC. However, Rio Tinto has not recently made any announcements to this effect and is instead increasing its investments in IOC. Finally, the government could shut down the mine, as happened to the coal mines in Alberta. However, this is highly improbable as, unlike coal, high grade iron ore reduces rather than increases carbon emissions. and the mining of iron ore is much cleaner than the mining of other metals such as copper.

Final Thoughts

Despite being the main cash cow for major miners such as BHP ( BHP ), Rio Tinto and Vale ( VALE ), iron ore is often overshadowed by other commodities such as copper. Both commodities will play an essential role in the drive for decarbonization, but the copper shortage narrative is much more prevalent than the high-grade iron ore shortage narrative. This is advantageous in a way as it means that high grade iron ore stocks trade at lower valuations than copper stocks, and therefore will likely deliver higher returns.

For further details see:

Labrador Iron Ore: Low Downside Risk With Production And Pricing Upside On High Grade Iron Ore Royalty