LAKE - Lakeland Industries: M&A Unlikely To Provide Consistently High Returns

2023-09-14 09:39:34 ET

Summary

- Lakeland Industries has historically only generated high ROIC in years with global health crises such as the Covid-19 pandemic, and the Ebola and Avian Flu epidemics.

- The company has the chance to change this moving forward with its commitment to drive growth via M&A.

- While the Eagle Technical acquisition has been successful, I don't think the company's compensation plan aligns well with making value accretive M&A over the long term.

- I am assigning a sell rating due to these incentives, and due to my estimate of Lakeland's intrinsic value based on management's guidance and Lakeland's past financials.

Lakeland Industries ( LAKE ) has historically been an average business at best, producing below average returns on invested capital outside of the outlier pandemic and epidemic years. While this is the case, there have been a few changes in the business over the last year that create the need for investors to take a second look. First, Lakeland acquired Eagle Technical Products in FY2023 for $10.8 million. Eagle Technical is a designer and provider of protective apparel to the fire and industrial sectors. This acquisition fits in quite well with the rest of Lakeland’s business. Second, the company’s management team was shaken up drastically in early FY2024 with the departure of the executive chairman of the board , Christopher Ryan, and the CFO, Allen Dillard .

The main questions stemming from these changes are whether the Eagle Technical acquisition will provide high returns, and whether management will be able to generate high returns on acquisitions going forward. I will discuss these questions in more detail in this report as I believe they will dictate the long-term value of the business.

Most recently, Q2 results were solid and investors reacted favorably as the company beat both top and bottom line expectations. Lakeland's stock rose 10% the day these results were released. Notably, the Eagle Technical acquisition seems to be providing solid returns as it generated $900 thousand in adjusted EBITDA for the quarter.

If management can continue to drive high margin growth via intelligent acquisitions over the long-term, the stock should do well from here. The Eagle Technical acquisition seems to indicate that Lakeland is capable of this, but I don't think that management’s incentives align with long-term value creation as equity awards and bonuses don’t take invested capital or assets into account. Additionally, the history of the business shows that topline growth and margin expansion is hard to come by. Nothing has drastically changed with the business over the past decade so it’s difficult to bet that those trends will change.

The positives are good to see for shareholders, but I estimate that Lakeland is at best fairly valued based on both my estimates of its future cash flows, and based on my estimate of FY2026 cash earnings per share of $1.37 and a 12x multiple.

Business Overview

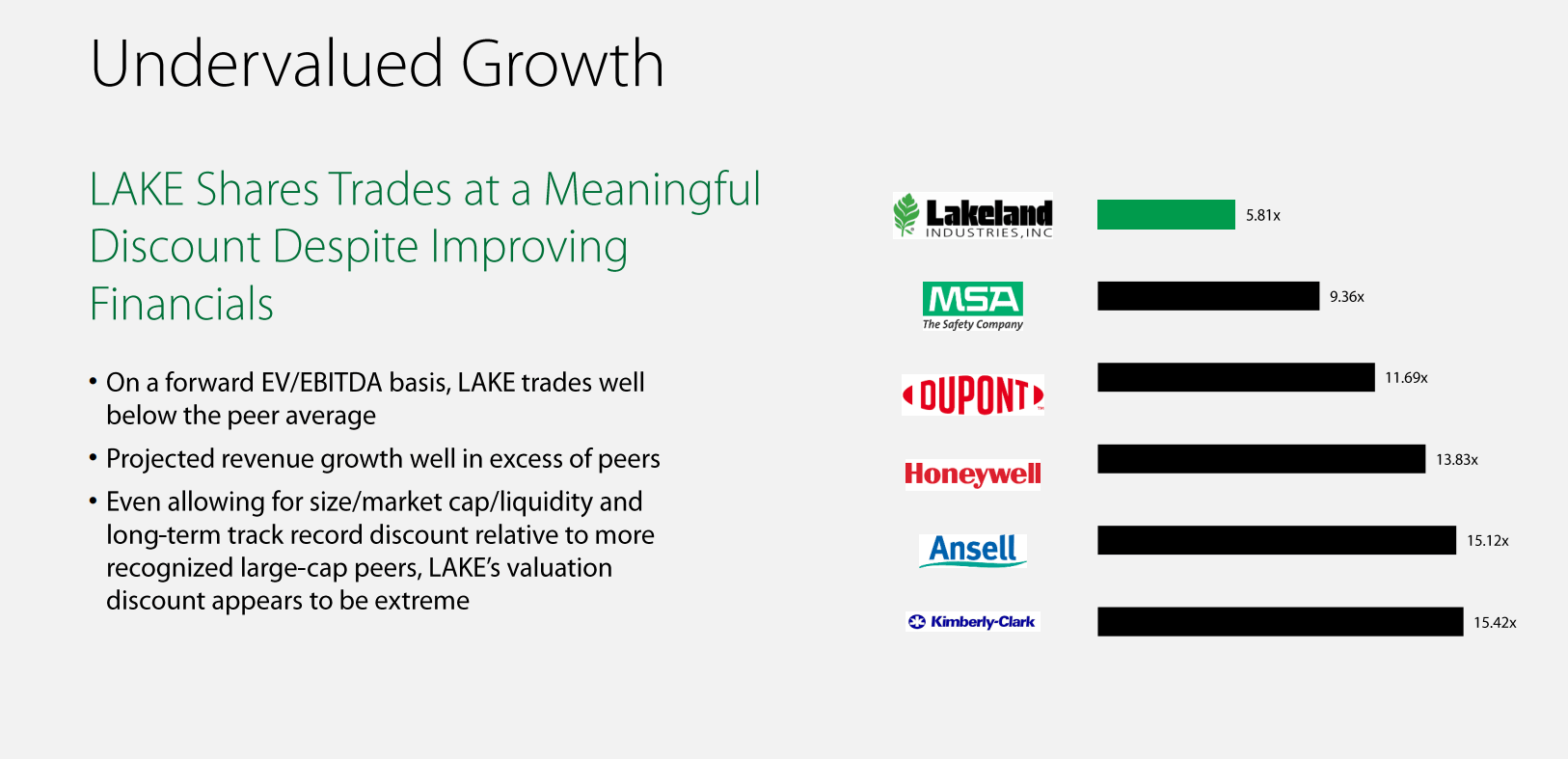

Lakeland manufactures and sells a comprehensive line of industrial protective clothing and accessories for the industrial and protective clothing market. There are many public companies that have business segments that operate in this industry, but Lakeland is the only pureplay company in this space that I am aware of.

The company has mentioned some of these competitors in past investor presentations, but those companies should not be thought of as direct comps because most of them have very diversified operations outside of their PPE segments. In fact, PPE is a very small portion of most of these businesses.

{kind=link}

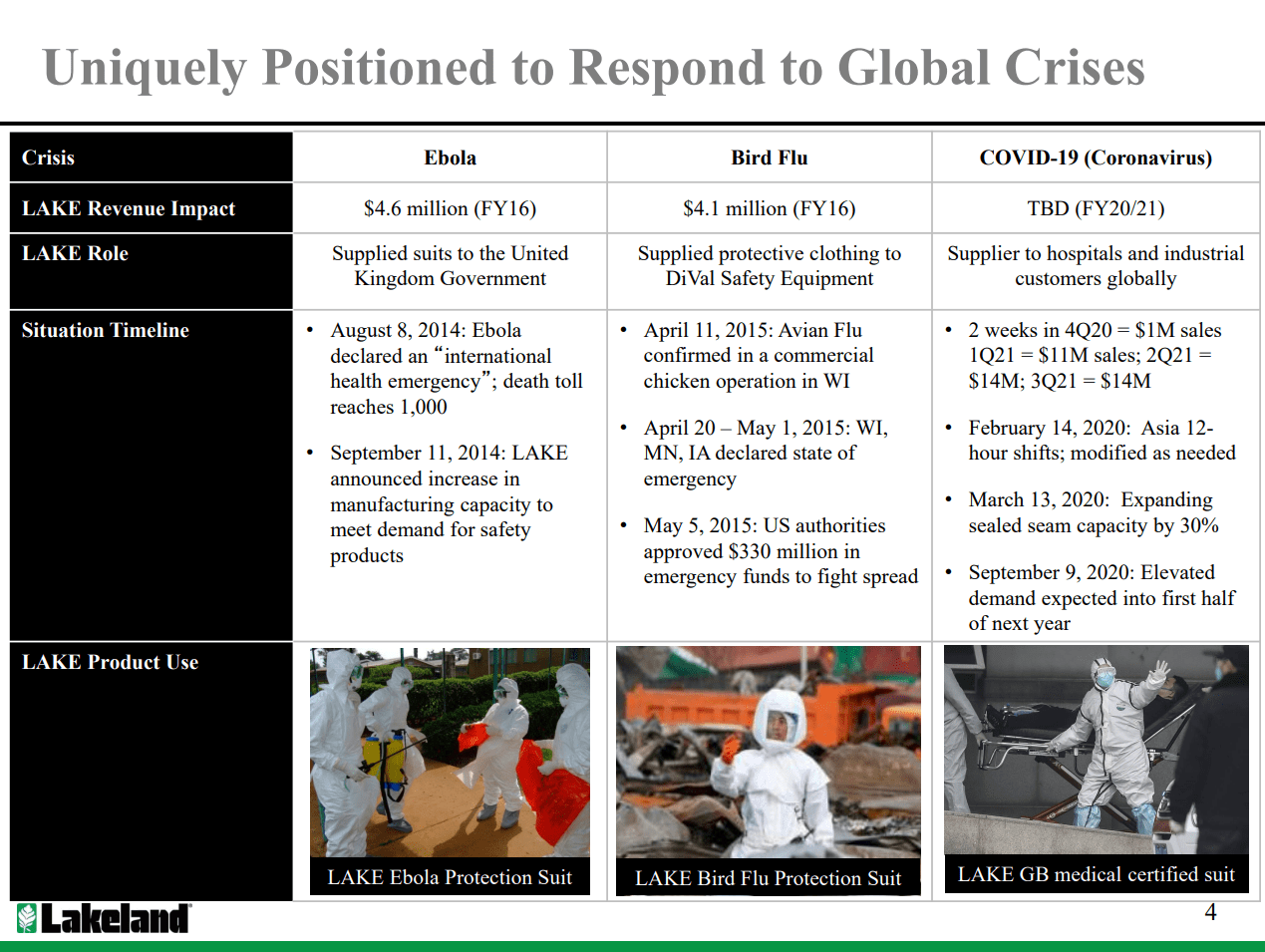

Lakeland benefitted from both the recent Covid-19 pandemic and prior health crises like the Ebola and Bird Flu epidemics in 2016, although the benefit from the Covid-19 pandemic was much greater. In fact, Lakeland’s stock never dropped during the March 2020 Covid market crash and actually rose into it. Investors realized that the benefit from the pandemic would be massive for the business and bid the stock up just on the news that the Covid-19 virus was spreading.

{kind=link}

How Health Crises Effect Lakeland (Lakeland Investor Presentation)

The PPE and industrial protective clothing market is not a big one and historically has not grown much. Lakeland’s sales have not grown much over the past decade because of this and outside of the recent pandemic and epidemics, its stock has not done very well.

Past Financial Results

As I mentioned above, the past decade has been underwhelming for Lakeland. Prior to the pandemic the company’s sales and earnings had been relatively stagnant with small periods of growth from the Ebola and Bird Flu epidemics, and returns on invested capital were poor in all years also excluding those health crisis years.

{kind=link}

Lakeland's ROIC (Created by Author)

These returns make sense when thinking about the industry from a supply perspective. The high demand and high returns for these products lead to new capacity coming online as capitalists enter the industry in order to capture those excess returns. When demand drops as the health crisis dies down, the industry has too much capacity and returns on invested capital for the companies that sell PPE products drops. This means that the best time to invest in the business is directly before a global health crises occurs. However, I have no ability to predict when this type of event will happen and I imagine most other investors don’t have insight into this either.

While organic growth will be difficult to come by if history is an indicator, Lakeland has now made a commitment to make more acquisitions. Lakeland's management made this quite clear on the most recent earnings call :

Moving forward, our leadership team is committed to identifying and maintaining a robust acquisition pipeline with opportunities that enhance Lakeland's strategic product portfolio and expand our geographic reach. Our M&A efforts are focused on finding opportunities like Eagle that meet our SSQ, small, strategic and quick acquisition strategy by identifying targets that are similar in size, highly strategic, and accretive to our bottom line in a short period of time.

If the company is able to consistently make acquisitions with high rates of returns, there is a good chance the stock will re-rate to a higher multiple. The most recent acquisition was Eagle Technical, which Lakeland acquired for $10.8 million. In the most recent quarter, Eagle Technical generated $900 thousand of adjusted EBITDA which indicates that the acquisition is providing solid returns, according to my math.

Annualized, Eagle Technical is generating $3.6 million of adjusted EBITDA. Assuming D&A is 10% of EBITDA and Eagle Technical has a 28% tax rate, I estimate that Eagle Technical's annualized operating income after tax is $2.3 million. With the $10.8 million price tag, I estimate the acquisition is providing a 21% return. If Lakeland’s management team is able to continually make acquisitions with 20%+ returns, Lakeland’s future financial results should be much improved over those from the last decade.

Lakeland has also invested in Bodytrak, a provider of “wearable monitoring solutions for customers in industrial health, safety, defense and first responder markets wanting to achieve better employee health and performance”. The company has invested a total of $5.8 million in the company for a minority interest, but has only recognized losses for the investment. In contrast to the successful Eagle Technical acquisition, this investment creates questions in management’s ability to drive growth efficiently with M&A.

It's impossible to know what the future will hold for Lakeland’s M&A prospects, but the executive incentive compensation plan does not create the proper incentives for long-term value creation. From the most recent proxy statement , executive bonuses are tied to “revenues (weighted at 40%), EBITDA margin (weighted at 40%) and free cash flow (weighted at 20%)”, while equity awards are tied to the amount of time the executive is with the company and “revenue growth and EBITDA margin.”

Concerningly, there is no mention of invested capital, the company’s asset based, or working capital in the compensation plan. Lakeland’s executives can hit the goals for their bonus and equity awards simply by making acquisitions without concern for the price paid.

The Eagle acquisition is a good start but over the long-term I believe that incentives generally dictate how a management team operates and the current incentives don’t give me confidence that the company will be able to sustainably make intelligent acquisitions.

Valuation and Price Target

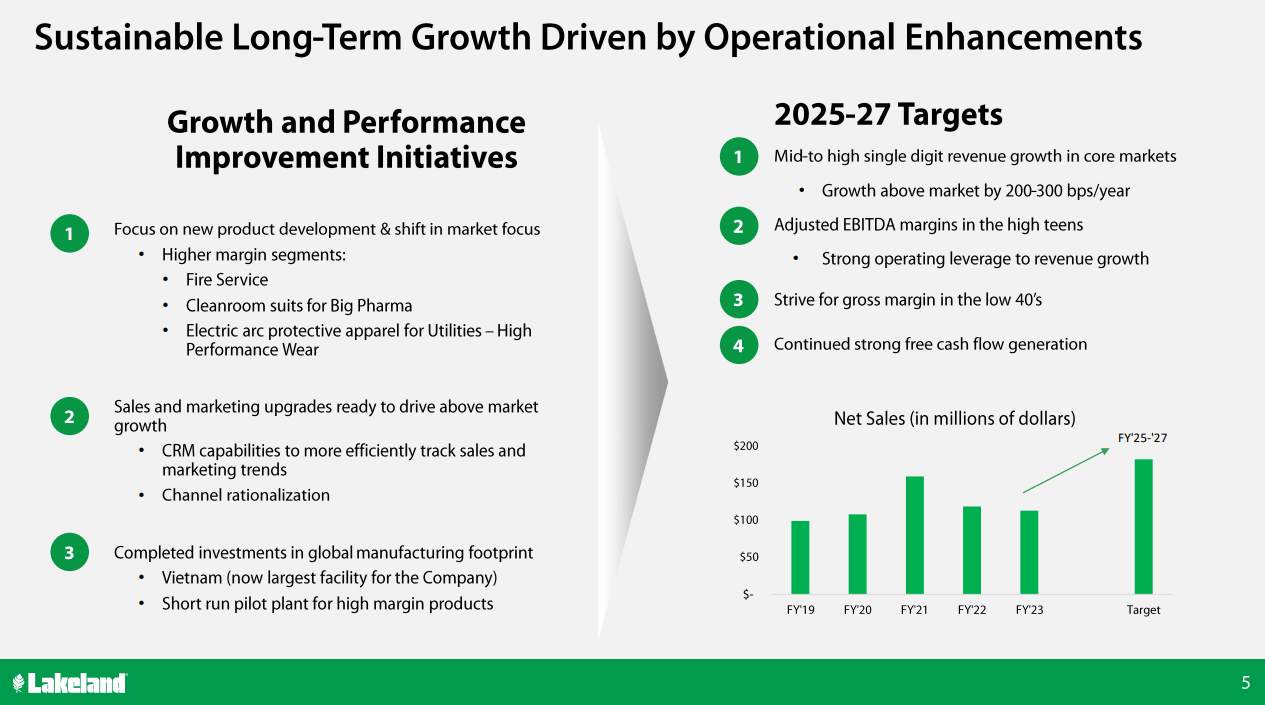

I am using management’s longer-term guidance as a base for my price target.

{kind=link}

Lakeland Long-Term Guidance (Lakeland Investor Presentation)

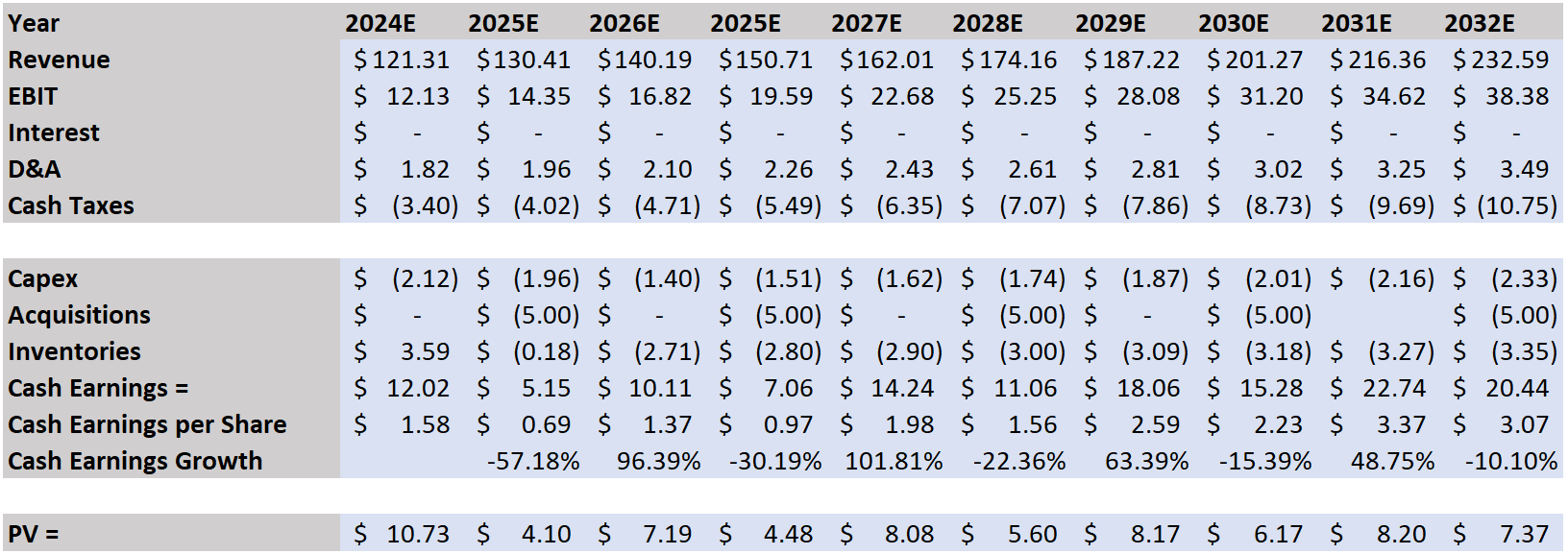

In my estimate of the company’s intrinsic value I am assuming revenue growth of 7.5% through 2032, gradually rising operating margins, a 28% tax rate, D&A equal to 1.5% of revenue, capital expenditures equal to 1% of revenue, inventories declining over time to equal 34% of revenue in 2032, and that the company will make a $5 million acquisition every other year starting in FY2025. Finally, I am applying a 12% WACC and a 2% terminal growth rate. With $24.5 million of net cash and 7.6 million shares outstanding, I estimate that Lakeland’s intrinsic value is about $15 per share.

{kind=link}

Lakeland DCF (Created by Author)

Lakeland DCF Continued (Created by Author)

Using an earnings multiple approach, I am estimating that Lakeland’s stock will trade at around $16 per share based on FY2026 cash earnings of $1.37 per share and a 12x multiple. The stock has historically traded at around 10x free cash flow but I am applying a premium based on the successful Eagle Technical acquisition. Taking the midpoint of these two price targets, I am assigning the stock with a $15.50 price target.

While this indicates that the stock is currently trading at about fair value, I am assigning a sell rating because I believe the company’s long-term executive compensation structure is creating incentives that don’t lead to long-term value creation and because my estimates are based on optimistic assumptions from the company’s most recent investor presentation. I believe there is a higher probability for underperformance relative to my price target than there is for outperformance, barring another global health crises.

Final Thoughts

Lakeland has historically generated high returns on invested capital only during years with global health crises. This was the case with the Covid-19 pandemic and with the Ebola and Avian Flu epidemics. Outside of these years, the company has generated poor returns on invested capital and has not been able to grow consistently. This may change with management’s recent focus on making acquisitions, but I believe the company's executive compensation structure does not create the proper incentives for long-term value creation.

My $15.50 price target is based on my estimate of Lakeland’s future cash flows which is based on the company’s past results and management’s longer-term guidance. While this price target is about where the stock is currently trading I see a higher probability for underperformance given the general difficulty of sustainably driving growth efficiently with M&A and due to the company’s history of low growth and poor ROIC.

For further details see:

Lakeland Industries: M&A Unlikely To Provide Consistently High Returns