LAKE - Lakeland Industries: Strong Balance Sheet Should Help Navigate Current And Potential Headwinds

2023-06-10 02:07:39 ET

Summary

- Lakeland Industries' sales are stabilizing after a coronavirus-related boost.

- The share price has dropped 73% from all-time highs due to inflationary pressures, weakening demand, and recession fears.

- The company has a strong balance sheet, is modernizing manufacturing processes, and has recently made a major acquisition, making it an attractive investment opportunity.

- Risks include persistent inflationary pressures, a potential global recession, and difficulty in depleting inventories if demand continues to fall.

- This represents a good opportunity to acquire shares at reasonable prices as the P/S ratio is below the average of the past 10 years.

Investment thesis

Operations of Lakeland Industries ( LAKE ) are returning to normal after a boost derived from the high demand for their products as a result of measures used to contain the spread of the coronavirus throughout the world in 2020 and 2021. To this, we must also add ongoing headwinds related to inflationary pressures, weakening demand, and also growing fears of a potential recession as a consequence of recent interest rate hikes.

These headwinds and a potential recession have caused a significant share price decline of 73% from all-time highs reached in February 2021 and a sharp decline in the P/S ratio as investors are placing less value on the company's sales. Still, although profit margins are being currently impacted by increased production costs and weaker demand, they are starting to stabilize and the company finds itself with a very robust balance sheet thanks to huge cash reserves, and this is allowing it to invest heavily in production capacity expansion and manufacturing process modernization, which should help improve profit margins in the long run. In addition, high cash reserves have also allowed the company to grow through a major acquisition carried out in December 2022. These three factors (a strong balance sheet, modernization of manufacturing processes, and growth) make me believe that the recent decline in the LAKE stock price represents a good opportunity for investors who want to take advantage of the current pessimism among investors as current headwinds are likely temporary due to their direct link to the current macroeconomic landscape.

A brief overview of the company

Lakeland Industries is a global manufacturer of protective clothing and accessories for the industrial and public protective clothing market, including firefighting and heat protective apparel, high-end chemical protective suits, disposable protective clothing, durable woven garments, high visibility clothing, gloves, and sleeves. The company's products are sold in over 50 countries, which means it has very strong geographical diversification, and around half of its sales come from disposable products. It was founded in 1982 and its market cap currently stands at $96 million, employing around 1,500 workers worldwide.

Lakeland Industries logo (Lakeland.com)

The company's shares have been subject to periods of high volatility throughout history as it operates in a fairly cyclical industry, so it is important to take advantage of economic cycles in which there is more pessimism among investors to acquire shares at reasonable prices. Until now, the only way to get a return on the investment was through capital gains, but the company began paying a dividend in 2023, albeit with a very low dividend yield as it also has recently started buying back its own shares and is increasing capital expenditures in order to expand and optimize its operations.

Currently, shares are trading at $13.16, which represents a 72.55% decline from all-time highs of $47.95 on February 9, 2021. This shows growing pessimism among investors as net sales are stabilizing after abnormally high demand for personal protective equipment during the coronavirus pandemic in 2020. Furthermore, profit margins have recently been negatively affected by increased production costs due to inflationary pressures and slowing demand as growing fears of a potential recession are causing not only weaker demand from consumers but also lower expectations among investors.

The company is expanding in Europe through a major acquisition

In November 2022, the company acquired Eagle Technical Products Limited, a UK-based manufacturer of firefighting turnout gear that exports its products through European, Middle East, and Asian markets, for $10.8 million. Lakeland used part of the cash and equivalents available on the balance sheet to make the acquisition as it enjoys a very strong balance sheet with zero debt, and intends to expand the operations of Eagle through its existing sales channels.

The acquisition should help cushion a small part of the impact on sales that the end of the coronavirus pandemic is currently having and drive sales in the long term, which is necessary for the company as growth has been somewhat disappointing in the past 10 years.

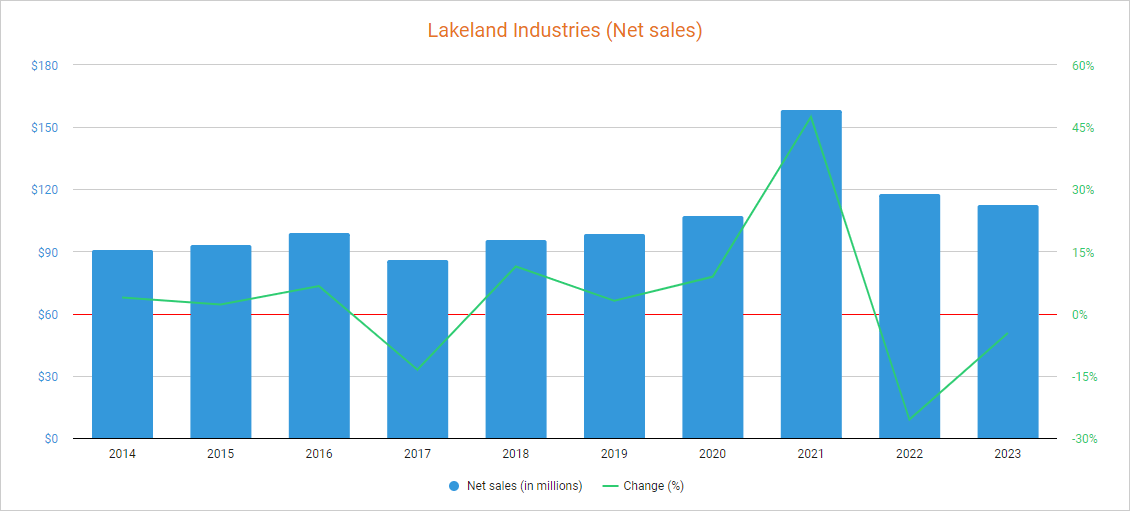

Net sales are stabilizing after high demand related to the coronavirus

Although sales had been quite stagnant for a while before the coronavirus pandemic, the company has historically managed to grow its sales, albeit at a slow pace. Using fiscal 2023 as a reference, 34% of the company's net sales are provided by operations within the United States, whereas 40% are produced in Asia, 7% in Latin America, 5% in Europe, and the rest in the rest of the world. Boosted by globally increased demand for protective suits during the coronavirus pandemic, net sales increased by 47.48% in fiscal 2021 and then stabilized in fiscal 2022 and 2023 as net sales declined by 25.54% and 4.68%, respectively.

{kind=link}

Lakeland Industries net sales (Seeking Alpha)

But more specifically for fiscal 2023, net sales declined by 19.99% year over year during the first quarter, increased by 2.61% year over year during the second quarter, declined again by 5.48% year over year during the third quarter, but increased by 8.21% year over year during the fourth quarter (and by 2.11% quarter over quarter), which means that sales started to stabilize at the end of fiscal 2023 at higher levels than before the coronavirus pandemic, partly boosted by the recent acquisition of Eagle Technical Products Limited as the fourth quarter of fiscal 2023 already included $1.3 of net sales coming from the Eagle acquisition, which was closed in December 2022. Sales continued somewhat stable during the first quarter of fiscal 2024 as net sales increased by 5.21% year over year (but declined by 1.03% quarter over quarter), boosted by $2 million provided by Eagle during the quarter, which makes investors think that the fall in sales after the coronavirus pandemic is drawing to a close.

But the recent collapse in the share price despite stabilizing sales has caused a significant decline in the P/S ratio to 0.877, which means the company currently generates net sales of $1.14 for each dollar held in shares by investors, annually.

This ratio is 6.60% lower than the average of the past 10 years and represents a 60.83% decline from decade-highs of 2.269 reached in 2021, which reflects the current investors' pessimism despite recent improvement as demand is weakening after the coronavirus pandemic boost. Nevertheless, sales are expected to increase by 7.18% in fiscal 2024 and by a further 5.46% in fiscal 2025. Still, it is not only the lower demand that is causing pessimism among investors but also the risk of a potential recession due to recent interest rate hikes and the currently limited margins due to inflationary pressures.

Margins are currently limited due to rising production costs and weaker demand

In general, the company has managed to maintain positive gross profit and EBITDA margins over the years despite going through some headwinds that have temporarily affected its profit margins. Still, temporary margin contractions haven't significantly affected its balance sheet as it is very strong thanks to a very conservative use of cash by the management. In this regard, the trailing twelve months' gross profit margin currently stands at 41.34%, and the EBITDA margin is at 6.62%.

Still, the gross profit margin increased to 43.36% during the first quarter of fiscal 2024, and the EBITDA margin to 8.37% as margins are stabilizing, which means current headwinds are starting to soften. These headwinds are directly related to increasing production costs caused by inflationary pressures at a time when declining volumes due to weaker demand are causing unabsorbed labor, which is directly linked to the current macroeconomic landscape, so their nature is, in my opinion, temporary. Nevertheless, temporary price concessions due to an inventory alignment strategy are still negatively impacting margins. And also, the acquisition of Eagle is causing some concerns about their potential contribution to the company's margins as historically its operations had lower gross profit margins than the overall operations of Lakeland.

Still, EBITDA margins in Eagle's operations are significantly higher than the EBITDA margins of Lakeland Industries, so there should be no problem in operating the newly acquired business in a profitable way. Furthermore, the new facility located in Monterrey, Mexico, which should be operational during this fiscal 2024, has modern manufacturing processes and automation systems that the company's existing factories do not have, which means that profit margins should improve in the foreseeable future. The problem is that the company reported a trailing twelve months' cash from operations of -$3.69 million, which means that it is using its cash and equivalents to continue operating as it keeps raising inventories, and trailing twelve months' capital expenditures of $2.21 million are higher than usual due to strong investments in the Monterrey facility.

As for the first quarter of fiscal 2024, cash from operations was positive at $3.7 million thanks to higher margins, inventories decreased by $0.2 million and accounts receivable by $0.4 million while accounts payable increased by $1.7 million, and the company reported a positive net income of $1.3 million. In this regard, the company is returning to profitability, although cash from operations is still very limited due to lower demand and the recent squeeze in margins. For this reason, the company will likely keep using its cash reserves in order to cover capital expenditures and dividend expenses and perform further share buybacks. Still, as I mentioned, the recent contraction in margins is directly linked to the current macroeconomic landscape marked by weak demand and strong inflationary pressures, so headwinds should fade as soon as the macroeconomic picture improves.

Returning to capital investments, the trailing twelve months' capital expenditures have recently increased as the company is currently expanding production capacity in Mexico, and the management expects CAPEX to reach around $3 million in fiscal 2024. Fortunately, Lakeland's balance sheet is very robust, so the company has enough resources to finish its plans for expansion and modernization, both of which should help improve profit margins in the long run.

A rock-solid balance sheet will allow the company to navigate current headwinds and even a potential recession

The company fully deleveraged its balance sheet in 2020, coinciding with the beginning of the coronavirus pandemic crisis, and significantly strengthened its balance sheet by accumulating $60 million in cash and equivalents, more than half of which has been already used for the acquisition of Eagle Technical Products Limited, strong capital investments, and aggressive share buybacks.

The management is currently trying to gradually empty inventories in order to generate stronger cash from operations in the coming quarters, but weaker-than-expected demand is making it difficult due to the current macroeconomic landscape marked by weakening consumer purchasing power as a consequence of inflationary pressures and growing fears about a potential recession as a consequence of recent interest rate hikes. In this regard, inventories are starting to decline, but they will likely do so very slowly due to weaker demand.

In this regard, inventories are currently as high as $58 million, and the management will likely not be able to empty them at a fast pace due to the fact that it is actually expanding operations, so the capacity of these inventories to provide cash from operations in the coming quarters should be slow unless it is decided to close a factory to transfer production to the new factory in Monterrey. Still, facility modernization and slow emptying of inventories should allow Lakeland to keep a robust balance sheet for many years to come, and the company will likely be able to keep investing in further growth and modernization initiatives, as well as covering its dividend and keep performing share buybacks.

The recently initiated dividend has strong upside potential, but dividend volatility will always be a risk

In February 2023, the company announced the initiation of a quarterly dividend of $0.03 per share, and it paid another dividend of the same amount during the second quarter of fiscal 2024. Considering the current share price of $13.16, the dividend yield stands at just 0.91%. Still, considering the current number of shares outstanding, the company will spend just around $0.88 million in dividend payments per year, so the potential dividend upside is high. In this regard, the dividend potential upside is not only because of a relatively low cash payout ratio (once current headwinds ease) but also due to relatively high excess cash that can be used not only to keep growing and expanding but also to keep buying back the company's shares.

Still, it is very important to bear in mind that the volatility of operations derived from the cyclical nature of the company's operations makes the dividend susceptible to being frozen, cut, and even canceled in times marked by strong headwinds, so I think Lakeland is a good opportunity to get potentially high capital returns once current and potential headwinds ease, but should not be seen as a long-term dividend investment.

The company just began buying back its own shares

The company has been recently buying back its own shares as it announced a share repurchase program of up to $5 million in July 2021 in order to reduce the total number of shares outstanding, and announced another share buyback program of up to $5 million in April 2022. Thanks to these share buybacks, the number of shares outstanding declined by 7.88% in the past 3 years.

This means that each share represents a growing size of the company. Furthermore, there is still a share buyback authorization of $5.1 million as the management didn't buy back any shares in the fourth quarter of fiscal 2023 due to the expectations of a higher CAPEX and bought back only $0.3 million worth of shares during the first quarter of fiscal 2024. In this sense, I believe that there is a good chance that the company will continue to buy back shares in the foreseeable future due to its very strong balance sheet, although the management could limit such buybacks in order to preserve cash while headwinds continue to be so intense and the risk of a recession continues to be a concern.

Risks worth mentioning

Overall, I view Lakeland's risk profile, despite the high cyclicality of its operations, to be relatively low thanks to its robust balance sheet with high cash and equivalents and inventories and a below-average P/S ratio. Still, there are certain risks that I would like to highlight.

- If inflationary pressures persist for longer than expected or intensify again, the company could continue with contracted margins for longer, which could force it to use its cash reserves to continue operating.

- Recent interest rate hikes carried out to mitigate high inflation rates could cause a global recession, which could have a significant impact on demand for the company's products. This would affect not only the company's sales but also the profit margins as a consequence of a less-absorbed workforce.

- The company could have difficulty depleting its inventories if demand continues to fall, thereby losing pricing power.

- The quarterly dividend of $0.03 that the company has begun issuing in 2023 could remain frozen until macroeconomic conditions allow for raises. In addition, the high volatility in the company's operations could lead to an eventual cut or cancellation of the dividend in times marked by strong headwinds.

- The current share buyback program could be canceled if profit margins do not improve and the company fails to empty its inventories in a profitable way as the management has historically been very conservative regarding the use of cash.

Conclusion

The situation of Lakeland Industries has weakened in recent quarters due to the end of anti-covid measures carried out in the countries in which the company operates. Still, sales appear to be stabilizing at levels above those prior to the coronavirus pandemic and are expected to increase at an acceptable rate in the coming years, boosted by the Eagle acquisition.

Profit margins are currently tight as a result of inflationary pressures and weakening demand, and a potential recession could hit margins even further. Still, they are starting to stabilize at relatively healthy levels and the headwinds that are causing this contraction in margins are likely temporary due to their direct link to the current macroeconomic context, and furthermore, the company is prepared to face them for a very long time, and even to go through a potential recession, thanks to a debt-free balance sheet with high cash and equivalents and inventories. Still, emptying inventories will likely be difficult in the short to medium term due to weaker demand, but heavy investments to build a new modern factory in Mexico, as well as the acquisition of Eagle, which has higher EBITDA margins than Lakeland, should drive margins in the future. For these reasons, I believe that the recent fall in the share price represents a good opportunity for investors with enough patience to wait for current headwinds (and a potential recession) to ease.

For further details see:

Lakeland Industries: Strong Balance Sheet Should Help Navigate Current And Potential Headwinds