LRCX - Lam Research: A Better Entry Point Is Coming

2023-06-01 03:24:12 ET

Summary

- The semiconductor sector, particularly the memory segment, has experienced a downturn, but a rebound in demand is expected in the second half of 2023 and into 2024.

- Lam Research, a supplier of wafer fabrication equipment and services, has strong financials and is well-positioned to weather the downturn and benefit from the rebound.

- The stock price may experience volatility in the short term, but the company is expected to reward shareholders in the long run as the sector recovers.

Investment Thesis

With the memory sector at the lowest it's been in years and the negative sentiment over the last while for the whole semiconductor sector, I believe that we are nearing the bottom and companies like Lam Research ( LRCX ) will see a sustainable revenue rebound in the long run, coupled with great financials, the company is about fairly priced but further economic headwinds may present a better entry point.

Briefly on the Company

The company is a supplier of wafer fabrication equipment and services to the semiconductor sector. Their primary focus is on semiconductor memory products. Products in deposition, etching, and cleaning.

Sector Outlook

So, we all have seen the deterioration of the semiconductor industry in the last while, where oversupply has grounded all of the demand for new chips and integrated circuits, with high-interest rates and a weakened global economy playing a huge role too.

I’ve covered a few semiconductor companies in the past and most, if not all, have said that they see a rebound in demand in the second half of ’23 and return to growth sometime in ’24. The thing is though, macroeconomic headwinds are yet to meaningfully show themselves. Inflation is coming down, which is a good sign, however, it is still very sticky and well above where the Fed Chair wants it to be.

The overall semiconductor market is predicted to decline by 4.1% in ‘23 , which will be mainly driven by the memory segment and that is the main segment LRCX operates in. According to Gartner , the semiconductor sector is projected to decline around 11%, while the memory segment is to decline 35.5%, so we see projections are a bit all over the place, but I would trust Gartner a little more since the article was published just a month ago, however, both sources cite memory segment to be the main culprit. On a positive note from the same source, Gartner sees a massive rebound in the memory segment in ’24, which seems to be coinciding with how the management of Lam Research feels also. The management said that the memory revenues have been at the “lowest levels in a decade.”

That doesn't necessarily mean that the bottom is in, however. It is more probable that the rebound is going to happen given that many companies in the semiconductor sector have decreased their inventory levels to a more stable level and the demand for these products is going to pick back up sometime in the second half of ’23 and certainly in ’24. I'm just not sure if we will see such a rebound as Gartner suggests, however, seeing that NVIDIA ( NVDA ) has massively increased its guidance for the next quarter due to a significant increase in interest surrounding their data center business, which is mostly fueled by the hype of artificial intelligence. I know that Lam Research isn’t specializing in components for data centers, however, they do have some skin in the game with their photonic integrated circuit.

Overall, I can see further volatility in the upcoming 6 months or so when the stock price may vary wildly, which may present a decent entry point, but now let’s look at the company’s financial health.

Financials

Just to note one thing, the below graphs will be as of the company’s fiscal year ’22, which ended in June of last year. I will include numbers from the latest quarter if I believe they are relevant for extra color.

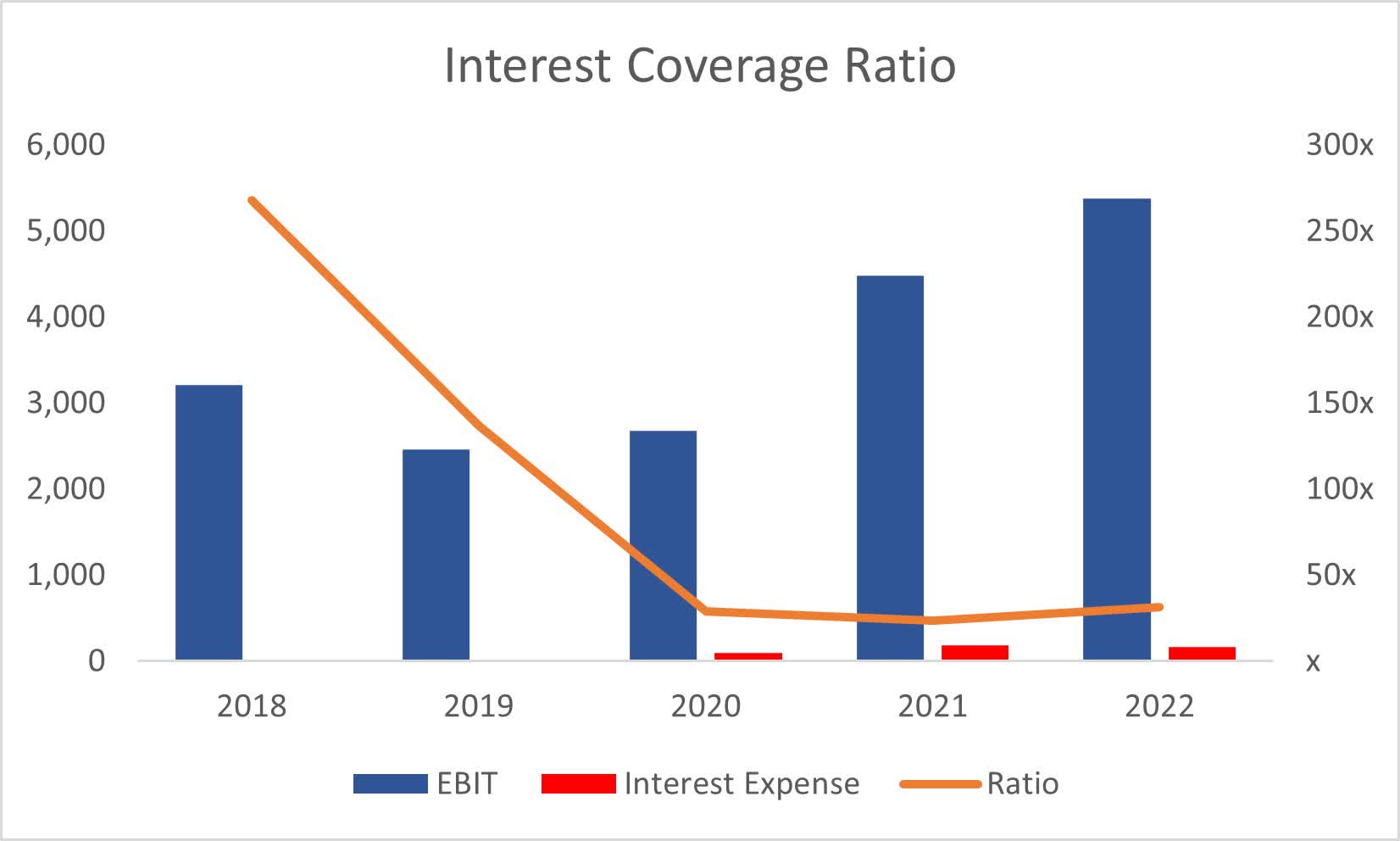

At the end of Q3 ’23, the company had $5.3B in cash on around $5B of long-term debt. That's a decent position to be in, in my opinion. Annual interest expense was around $170m for FY22 and seeing that the debt figure hasn't changed that much in the last 3 quarters, I will assume similar expenses will be booked in the full year of FY23. EBIT easily covers the company’s interest expense, and I don’t see an issue with having this much leverage on the books.

{kind=link}

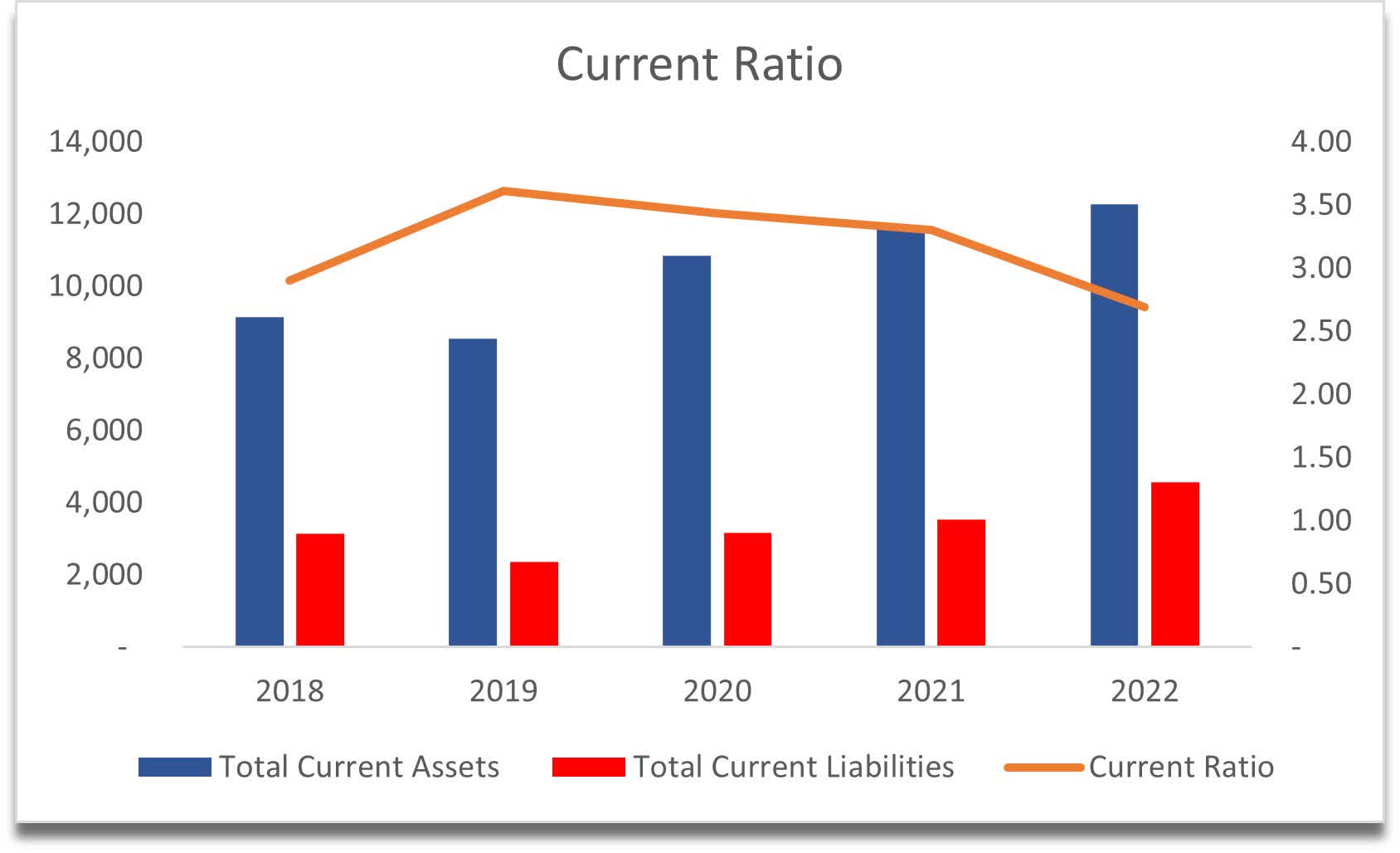

The company’s current ratio is also very healthy, standing at 2.69 by the end of FY22, and around 3 in Q3 ’23, so it slightly improved. LRCX has no liquidity issues as it can cover its short-term obligations 3 times over. It will have no problem weathering a macroeconomic downturn in the near future.

{kind=link}

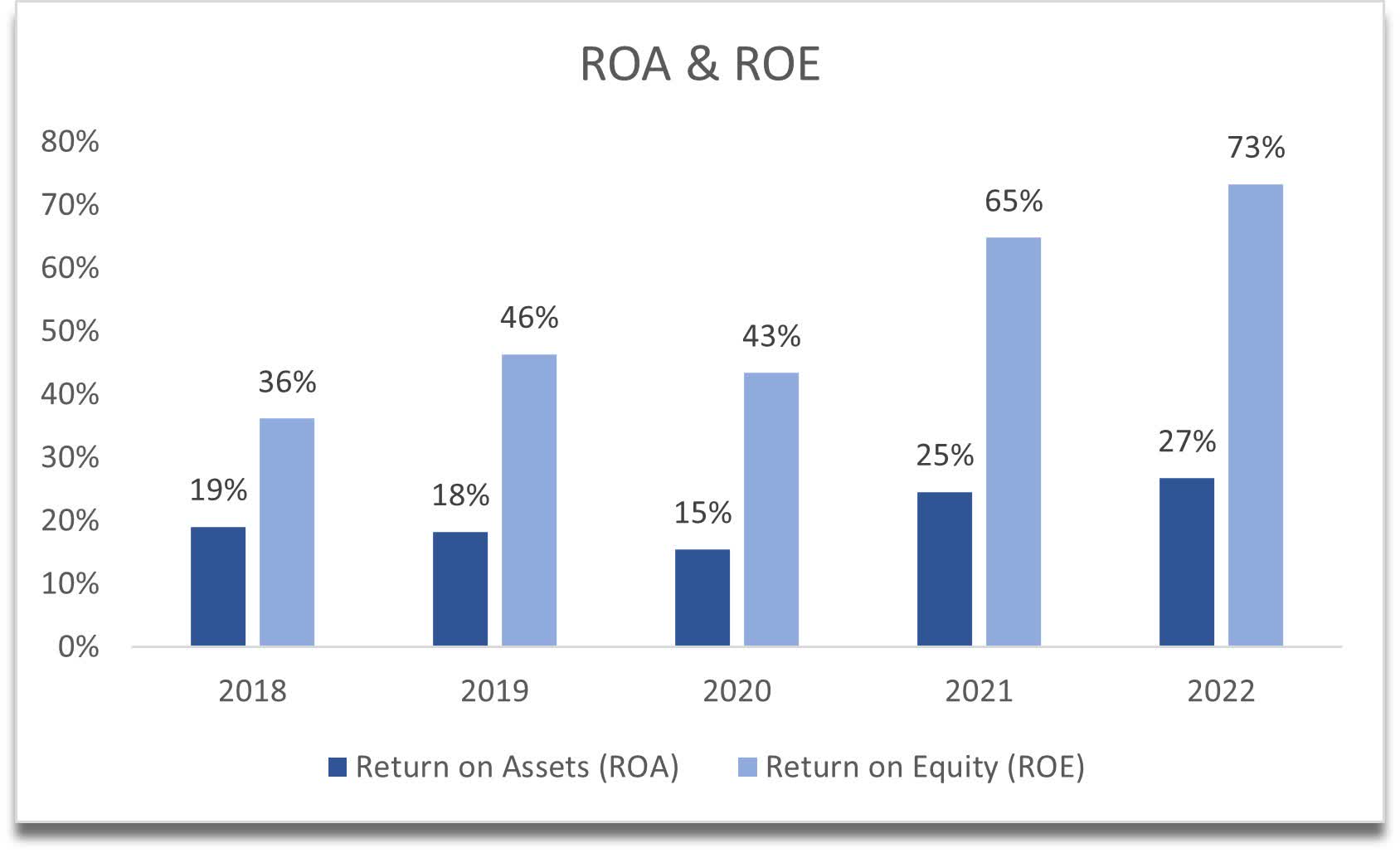

The company’s efficiency and profitability ratios are quite outstanding also. ROA and ROE have been steadily increasing over the last 5 years and are well above my minimum threshold of 5% on ROA and 10% on ROE. The management is utilizing the company’s assets and shareholders’ capital very efficiently and is creating value.

{kind=link}

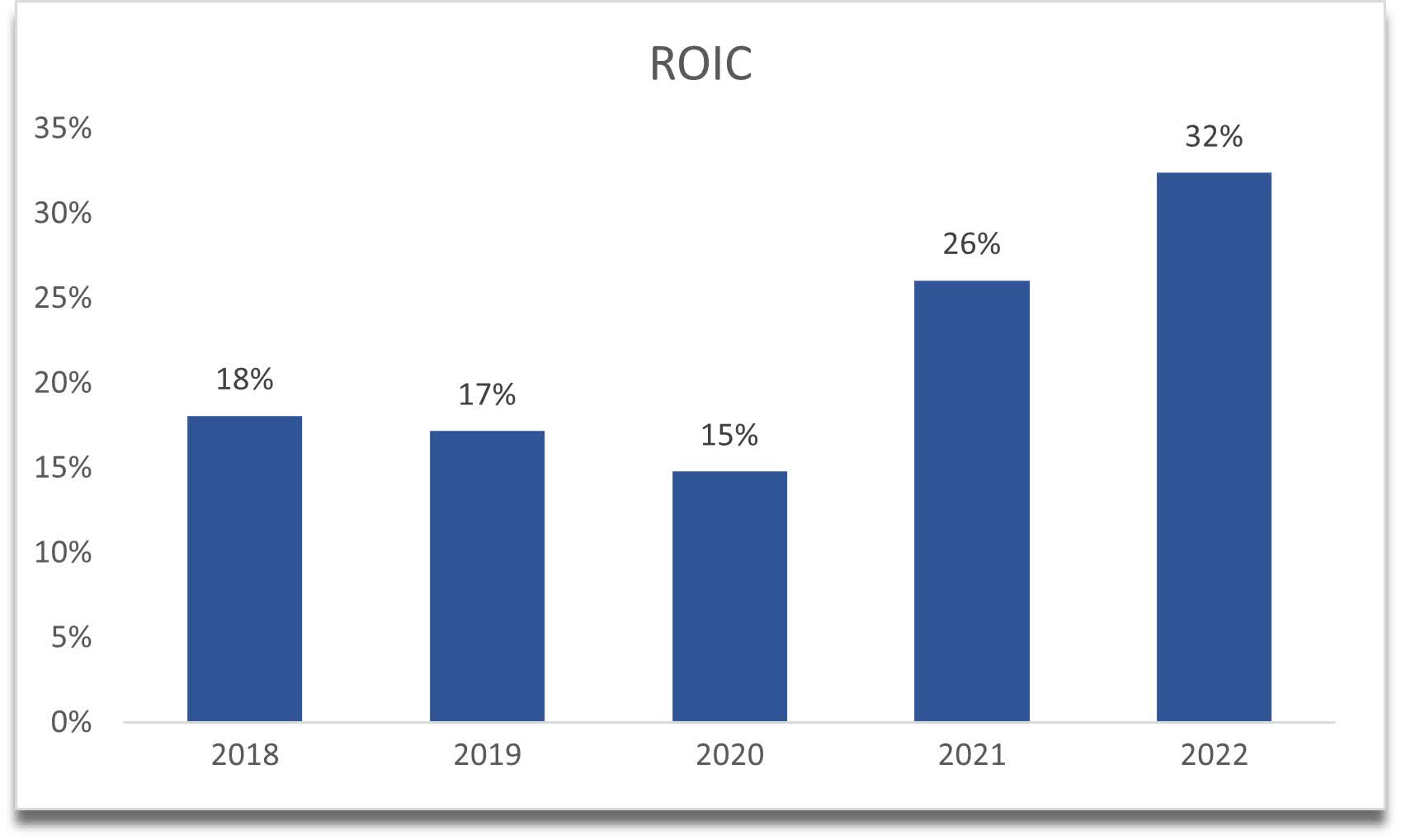

I am not surprised to see a similar story on a company’s return on invested capital. It’s been on an uptrend since the bottom during the pandemic. This tells me that the company is enjoying a decent competitive advantage and has a strong moat.

{kind=link}

Margins have slightly decreased from the FY22 figures, but with cost-cutting initiatives that the management mentioned in the latest transcript and a return to better profitability in '24, I can easily see the company coming back to its higher margins.

Overall, the company is in a very strong financial position, just like the other semiconductor companies I’ve covered in the past (most of them). It will easily weather the downturn, but the stock price could be very volatile.

Valuation

I was very surprised to see that analysts have baked in around a 17% decrease in revenues for FY24, and then all of a sudden back to 18%-21% growth the next year. I’ll go with that negative estimate for ’24, which I’m guessing might change in the next quarter, however, I’ll keep it conservative.

The company averaged around 20% revenue growth in the last decade, so for my base case scenario I went with a slightly more conservative estimate of around 11% for the next decade, with 1% growth in '23 and -17% growth in '24.

For the optimistic case, I went with 15% CAGR over the next decade, while for the conservative case, I went with 9%. These estimates are all reasonable in my opinion and the company could easily outperform even the optimistic scenario.

In terms of margins on the base case, I improved gross and operating margins by 200bps, or 2% in the next decade, which I believe is quite conservative still. For the optimistic case, I improved them by 75bps from the base case, and I left them as they have been at the end of FY22 for the conservative case.

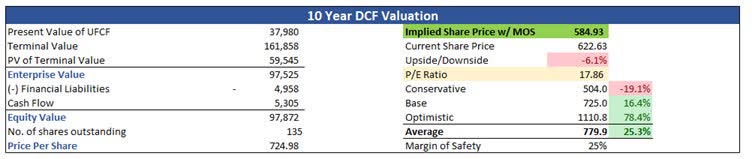

I also added a 25% margin of safety just to be even more conservative. With that said, the company's intrinsic value is $584.93, suggesting a 6% downside from the current valuation.

{kind=link}

Closing Comments

I don't think I'm being too optimistic with my assumptions here, the 18x PE ratio doesn't seem to be too expensive in my opinion. I can easily see the company coming back below the intrinsic valuation, with all the macroeconomic downturns still ahead, which will bring further volatility to the stock market. The sentiment of the semiconductor industry is starting to change a little and the love for it is coming back. I would expect the cyclicality to end sometime later in '23 and early '24 as the mentioned sources predict. The company has a really strong balance sheet and can generate good cash flows. Its profitability and efficiency metrics are outstanding. The company is going to reward its shareholders in the long run.

I will wait for the next quarterly report, which will be the FY23 report to see how the management will feel about the future demand for the products and what kind of tone they're going to be using, but I think that going forward, it is going to get much better. It might get worse before it gets better, so I will wait patiently for more assurance that the tide has turned and the love for the sector is back strong.

For further details see:

Lam Research: A Better Entry Point Is Coming