LRCX - Lam Research: An Opportune Moment To Add The Stock

2023-10-10 10:36:21 ET

Summary

- The memory chip market is in a devastating cyclical downturn, hurting the company's sales.

- The company has multiple long-term secular growth drivers behind it.

- Semiconductor experts predict the memory chip market to rebound in 2024, providing a tailwind for wafer fabrication equipment manufacturers like Lam Research.

The last time I wrote about Lam Research (LRCX) was on September 3, 2021, when the aftereffects of the pandemic created a global chip shortage . The situation was dire, and chip manufacturers' executives like STMicro's Chief Executive Officer Jean-Marc Chery forecast that the chip shortage would end by the first half of 2023. At the time, the global chip shortage provided tailwinds for a multi-year wafer fabrication equipment (WFE) spending spree by chip manufacturers, boosting Lam and other WFE companies' business. I recommended a buy when I authored that article based on the belief that the chip shortage would last at least a year, driving robust revenue growth throughout 2022. I also believed that even when the chip shortage did end, long-term secular growth drivers would dampen or eliminate the cyclical nature of the chip industry. Unfortunately, in the short term, I was wrong, and those who feared peak memory and the subsequent crash of the memory market were correct.

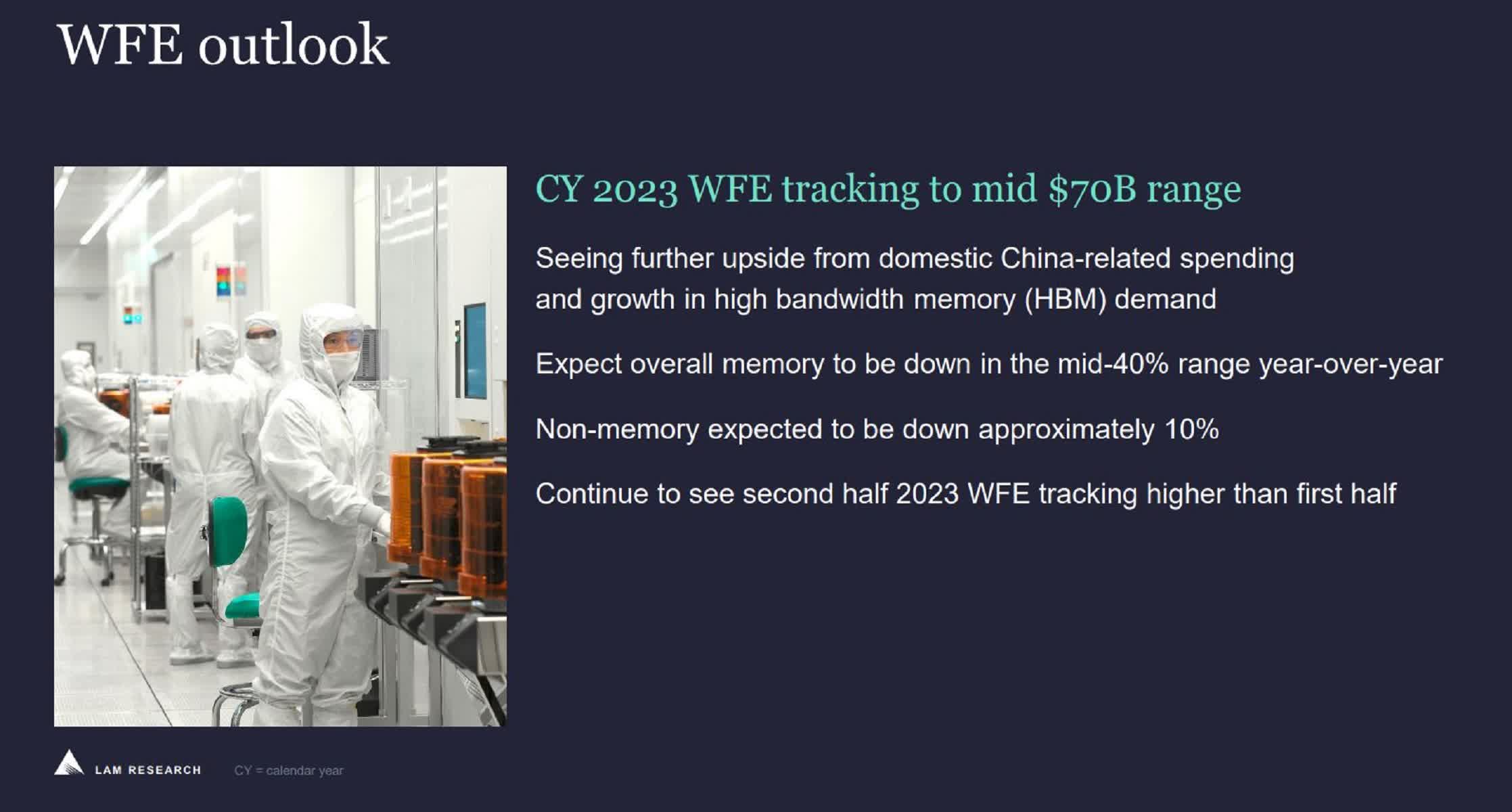

The market for NAND and DRAM memory chips began imploding in the second half of 2022 and has lasted into 2023. WFE spending ended 2022 at $94 billion. Earlier in the year, Chief Executive Officer Tim Archer said during the June quarter 2023 earnings call that he believed overall WFE spending would end 2023 in "the mid-$70 billion range," down around 20%.

Lam Research June quarter 2023 financial results

{kind=link}

At the Evercore ISI 2023 Semiconductor & Semiconductor Equipment Conference, Lam's Executive Vice President and Chief Financial Officer Douglas Bettinger said:

I have never seen a downturn this significant in memory in my entire career. I've been in the industry for a while. Memory, in total, down north of 40% kind of sequentially year-on-year from an investment standpoint. NAND is down 75%. It is substantial. And when you look at what my customers are doing, utilization is dialed back more than I've ever seen.

Source: Evercore ISI 2023 Semiconductor & Semiconductor Equipment Conference

When chipmakers have lower utilization, they use less chip manufacturing capacity, which has terrible consequences for WFE companies like Lam. When "utilization is dialed back," manufacturers use existing WFE equipment less, resulting in lower sales of new equipment, spare parts, service calls, and upgrades. You can see the impact on Lam's revenue in the chart below.

The excellent news for Lam investors is that Bettinger thinks the chip industry is "bouncing along a bottom." Although he doesn't know when things will turn up again, he doesn't see things worsening. Despite some investors thinking that because the memory chip industry won't immediately turn up in the fourth quarter of 2023 is a reason to avoid the stock, today may be an ideal time to buy. The microelectronics industry association SEMI.org recently issued a report forecasting a significant rebound in WFE memory spending in 2024. Another factor for investors to consider is that one of the world's largest memory manufacturers, Micron's ( MU ) third-quarter earnings report indicated that it plans to increase spending for WFE in 2024. Since investors usually get the best results investing in cyclical stocks by buying at a low point in the cycle and the memory WFE cycle is near or at its low point, today is a beautiful time to start dollar cost averaging into the stock. Those investors waiting to see the first signs of increased orders or hearing that analysts have upgraded the stock could miss a considerable portion of the initial rally before deciding to pull the trigger on a buy.

If you decide to buy today, you should do much better in the long-term buying at the bottom of a WFE spending cycle than my previous 2021 buy recommendation that encouraged investors to buy near the top in the WFE spending cycle. Once the spending cycle turns up, quarterly year-over-year revenue growth should reaccelerate, and investor demand for Lam's shares should drive the stock price higher -- potentially providing market-beating returns.

Long-term secular growth drivers

Advanced technologies such as cloud, 5G, AI, high-performance computing, wearables, and IoT have increased demand for semiconductors that have more efficiency, power, and performance. One of the industry's most significant innovations for keeping up with this need for better chips is using three-dimensional (3D) architectures and advanced packaging -- a trend favoring sales of Lam Research's etch and deposition tools.

According to CFO Douglas Bettinger:

[To] foreshadow a little bit of the Lam story, when I look at a very kind of macro level, you have these changes in architectures that are inflecting in the third dimension, right? NAND [chips] did it years ago. The industry is looking forward, still pretty far away, but DRAM [chips] is eventually going to adopt a 3D structure. You're beginning to see it in foundry and logic with gate-all-around [chips]. When things go 3D, Lam does well. We are an etch and deposition company. We've put film down on the wafer, and we remove it with our etch bills. That is the definition of 3D. Everybody is super excited about advanced packaging today. Well, guess what, to make advanced packaging happen, you need to deposit conductive material and you need to create space to deposit that. That's etch and deposition.

Source: Evercore ISI 2023 Semiconductor & Semiconductor Equipment Conference

The 3D structure opportunity is massive. For instance, the gate-all-around chip opportunity in foundry and logic alone is nearly an incremental $1 billion for every 100,000 wafer starts that chip manufacturers generate. Lam's management believes the company can win a sizable chunk of that business. As for advanced packaging, Chief Executive Officer Tim Archer said during Lam Research's June quarter earnings call , "Overall, we have greater than 50% market share in deposition and edge solutions required for advanced 3D stacking of high bandwidth memory."

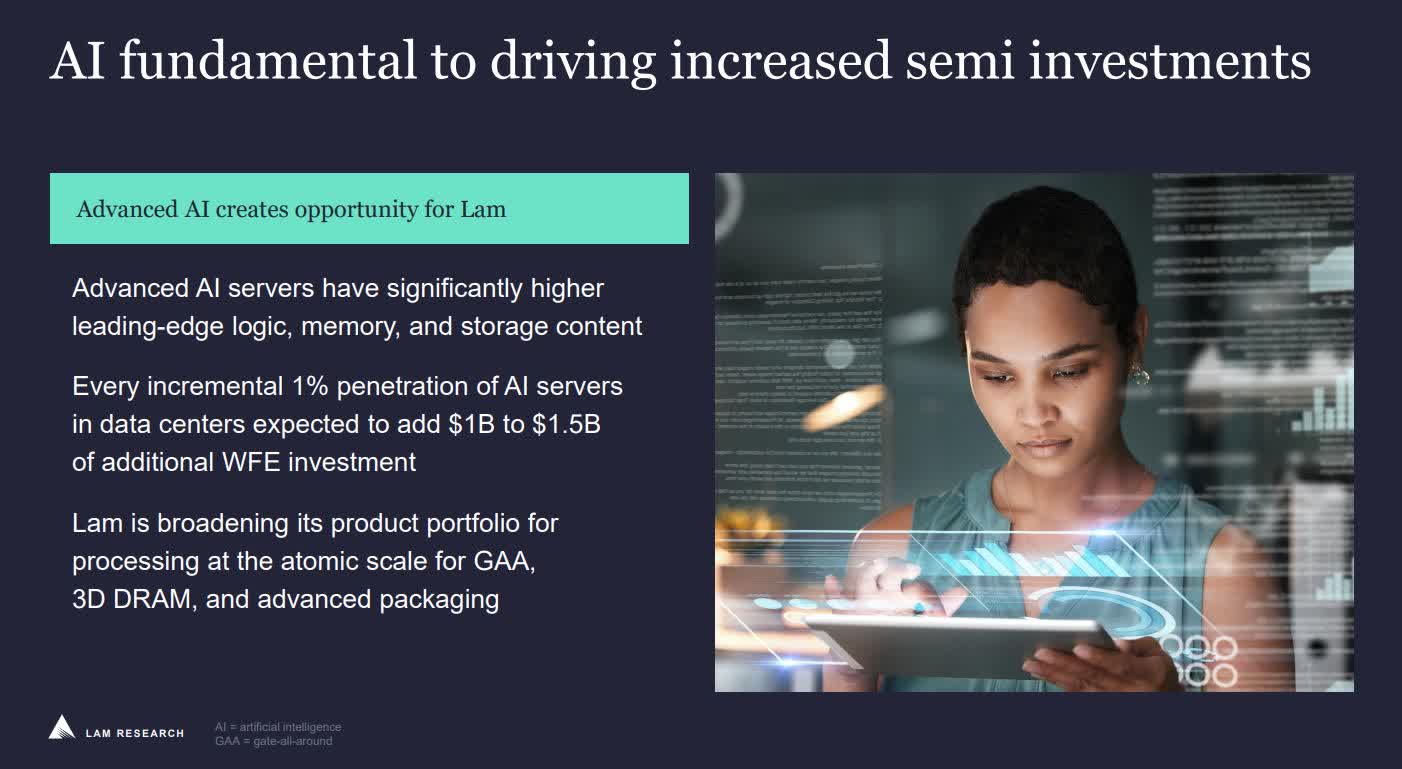

In addition to the shift to 3D architectures, the company should benefit from the quantum leap in Artificial Intelligence adoption sparked by OpenAI introducing generative AI to the world through ChatGPT. Lam management believes that every 1% of data center volume that shifts to an AI server versus a traditional server configuration will drive an additional $1 billion to $1.5 billion of WFE investment.

Lam Research June Quarter 2023 Investor Presentation

{kind=link}

Lastly, Lam investors should pay close attention to the company's installed base, which, as of the December 2022 Earnings Conference Call , numbers 84,000 process chambers, up 27% from an installed base of close to 66,000 chambers from the pandemic's December 2020 Earnings Conference Call -- solid growth throughout the worst of the pandemic period. The company typically reports its installed base numbers in the December quarter's earnings report. As its installed base grows, it increases its annuity-like revenue from Lam's Customer Support Business Group ("CSBG"), which consists of spare parts, service, equipment upgrades, and legacy equipment sales. During the company's latest quarter, CSBG generated approximately $1.5 billion, 47% of its revenue, providing a stable source of income during this industry's down period.

Is the stock overvalued?

The stock sells at a price-to-earnings (P/E) ratio of 18.95 compared to its median P/E ratio of 18.83 over the past ten years. Based on those metrics, some might consider the stock fairly valued.

However, its valuation based on its price-to-sales (P/S) ratio is 4.89, well above its ten-year median P/S ratio of 3.37. Additionally, Seeking Alpha Quant's overall valuation ratio is a D+ . So, there are reasons to consider Lam overvalued, especially considering that the near-term prospects over the next several quarters look bleak.

If you are a value investor and worry about conditions in the WFE market, you may be uncomfortable with investing in the stock at the current valuation. However, considering that Lam has positioned itself to outperform in an industry experts expect to grow to more than $1 trillion in 2030 , I believe its valuation is more than justified.

Profitable and positioning itself to grow more profitable

Lam's gross margin was at 45.7% in the June quarter, up from 44% in the March quarter and exceeding company guidance. The company is on a cost and efficiency improvement campaign with a long-term goal to achieve a 47% to 48% gross margin that it committed to in March 2020.

The company plans to increase its gross margin over time through restructuring, increased digital transformation efforts, and using AI to increase efficiency and lower costs. During Lam's presentation at a recent investor conference, Douglas Bettinger said regarding improved gross margin in the June quarter:

A key component of that is this program is ahead of schedule. And by the way, a portion of what we're doing in this restructuring is related to kind of figuring out how to make AI work at the company, right? We're undertaking a digital transformation project that's delivering some of this.

Source: Evercore ISI 2023 Semiconductor & Semiconductor Equipment Conference

Bettinger also mentioned that most of the June quarter's margin improvement came from its decision several years ago to build a factory closer to its Asian customers. By building a massive factory in Malaysia , the company saves on labor costs and achieves lower shipping costs to Asian chip manufacturing facilities. However, the best part is that even though the company must invest significantly in Research and Development (R&D) to stay ahead of the competition, Lam has remained profitable on a trailing 12-month ("TTM") basis over the last ten years. Additionally, the company has increased free cash flow ("FCF") to $4.7 billion TTM over the past ten years.

The company plans to return 75% to 100% of that growing free cash flow to investors for the foreseeable future. On August 24, the company raised its dividend by 16% to reach $2.00 per share, adding to its record of consistently raising its dividends over the past ten years, as seen in the chart below.

So, if you are looking for a stock capable of consistently growing its dividends, Lam could be a wise choice.

A wonderful time to buy

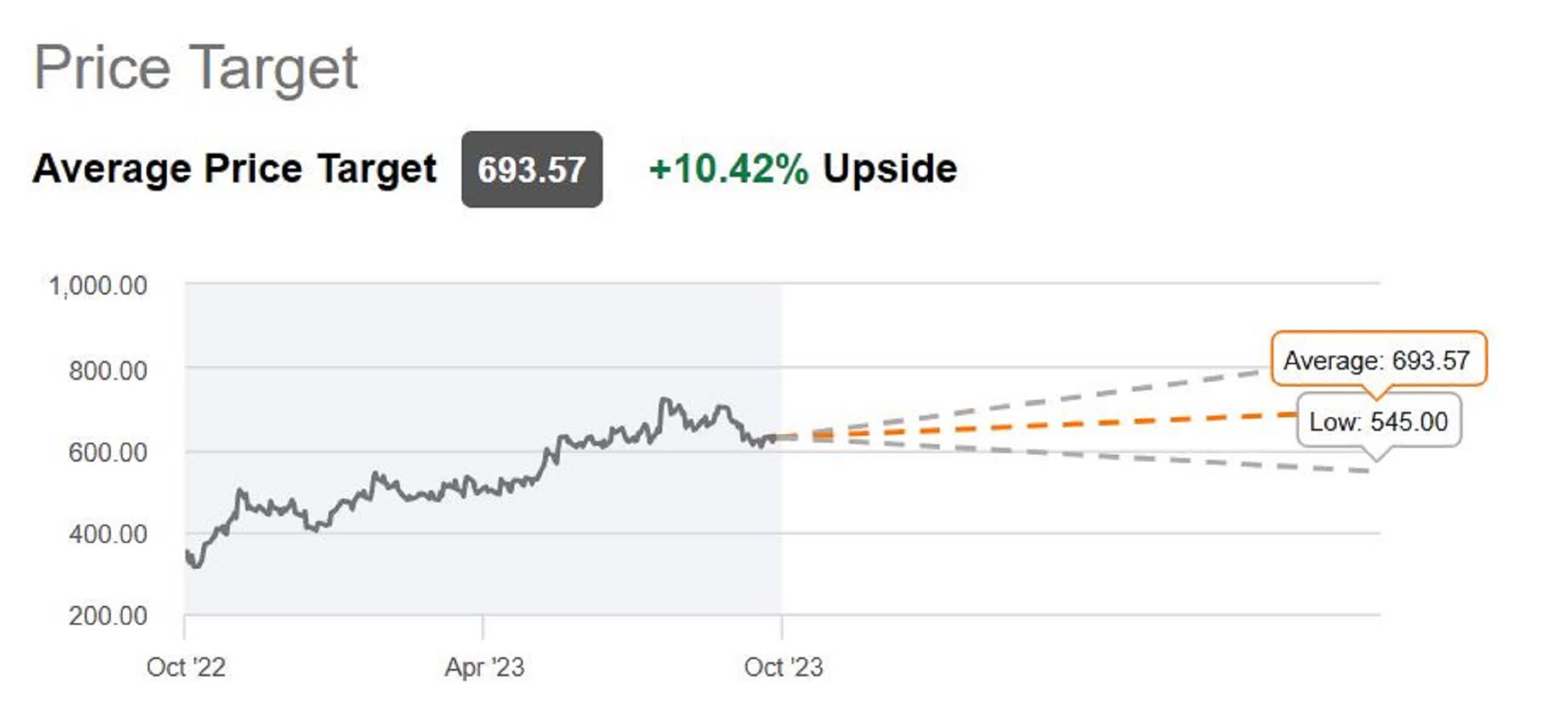

Although Seeking Alpha analysts and quant rate the stock a "Hold," the wizards on Wall Street rate the stock a "Buy," with an average price target of $693.57. That price target translates into a 10.42% return from its October 6, 2023, closing price over the next year.

{kind=link}

I believe Lam Research's long-term growth drivers should provide market-beating returns over the next three to five years. If you are a growth investor looking to capitalize on secular trends like the increasing number of more powerful chips used for AI, 5G, autos, consumer electronics, and more, consider dollar cost averaging into the stock over the next year.

For further details see:

Lam Research: An Opportune Moment To Add The Stock