LRCX - Lam Research Earnings: All Eyes On Memory Chip Recovery

2023-07-24 16:31:03 ET

Summary

- Lam Research’s percentage of systems revenue in memory was 32% in the past quarter, a decline from the prior quarter level of 50%.

- Lam Research will report a further decline in both NAND and DRAM revenue in the June quarter.

- Lam Research will report an increase in revenue from foundries, an increase in revenues in mature nodes, and a slowdown in revenue for sub-7nm nodes.

- Memory equipment sales will again dominate Lam Research's revenues in CY2024.

Lam Research ( LRCX ) is expected to report June 2023 quarter earnings on Wednesday, July 26, after market close.

The consensus revenue estimate of $3.12 billion for the current quarter represents a YoY change of -32.7% and -19.4% QoQ.

Revenue of $3.87 billion in the previous quarter represented a YoY change of -4.7% and QoQ change of -26.7% from $5.28 billion in F2Q.

For the current quarter, Lam is expected to post earnings of $5.03 per share, a change of -43% YoY and -28.0% from an EPS of $6.99 for the previous quarter.

Analysis

Based on revenue consensus, revenues are estimated to change -40.9% from $5.28 billion to $3.12 billion. In order to strategize forward earnings of LRCX, it's necessary to understand what got the company into this situation.

First of all, I forewarned this problem in June 2021, so Lam et al had plenty of warning.

I presented my thesis in mid 2021 that the extraordinary amount of capex spend for equipment will lead to a severe downturn in 2023 for equipment companies because of an oversupply of capacity and chips, in my July 11, 2022, Seeking Alpha article entitled " Assessing My 2021 Call For A Likely Semiconductor Equipment Meltdown In 2023 Impacting Applied Materials ."

The current macro factors have clouded the issue - less demand for consumer products resulting in capex cuts by Micron and SK hynix, and the China sanctions. What would have been a severe hit in 2023 has been moved forward into 2022, lessening the shock in 2023. But my thesis calls for a continued slowdown in 2024.

Lam reported in the previous earnings call that within Memory, the NAND segment represented 23% of our systems revenue, down from the December quarter level of 39%. And DRAM decreased sequentially, coming in at only 9% of systems revenue compared with 11% in the December quarter.

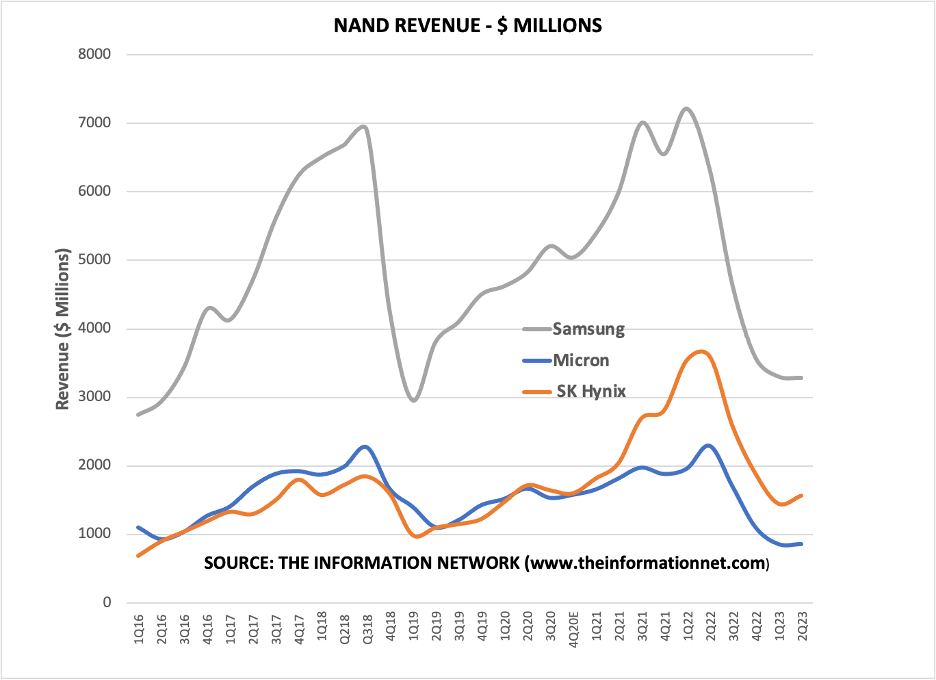

The downturn in the memory sector is illustrated in Chart 1 NAND. I present data from Q1 2016 through Q1 2023 and including my estimates for Q2 2023, according to The Information Network's report entitled Hot ICs: A Market Analysis of Artificial Intelligence ((AI)) 5G, Automotive, and Memory Chips.

{kind=link}

Chart 1

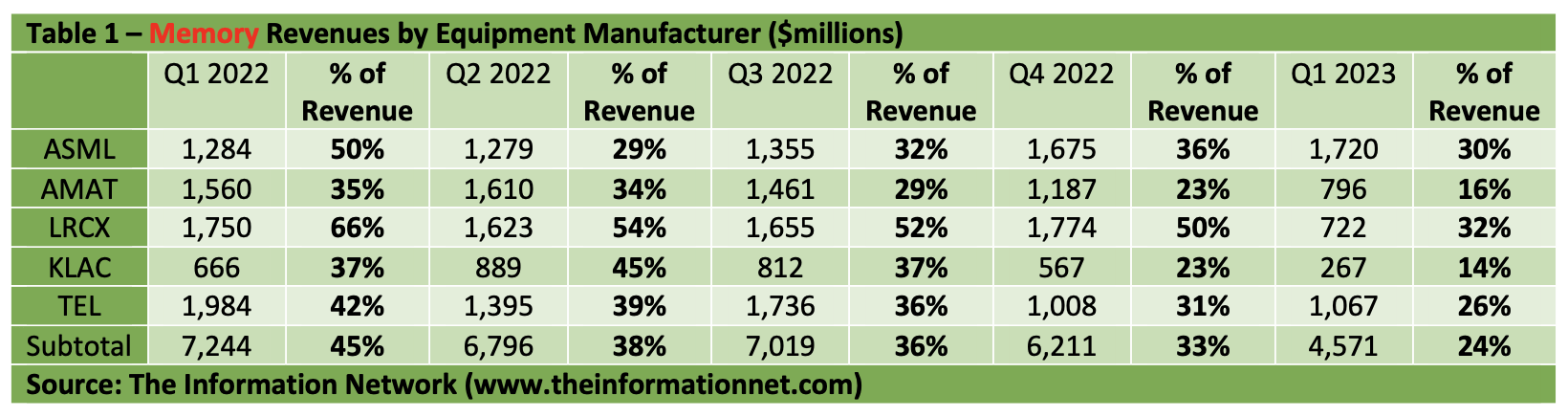

According to Table 1, in which I show revenue from the top 5 equipment companies generated from sales of equipment to memory companies. There are two takeaways:

- Lam generated the greatest percentage of its revenues in 2022 from Memory companies.

- Lam's share of memory revenues decreased QoQ successively throughout 2022, and in Q1 2023, dropped significantly to 32% as memory revenues decreased from $1,774 million in Q4 2022 to just $722 million in Q1 2023.

{kind=link}

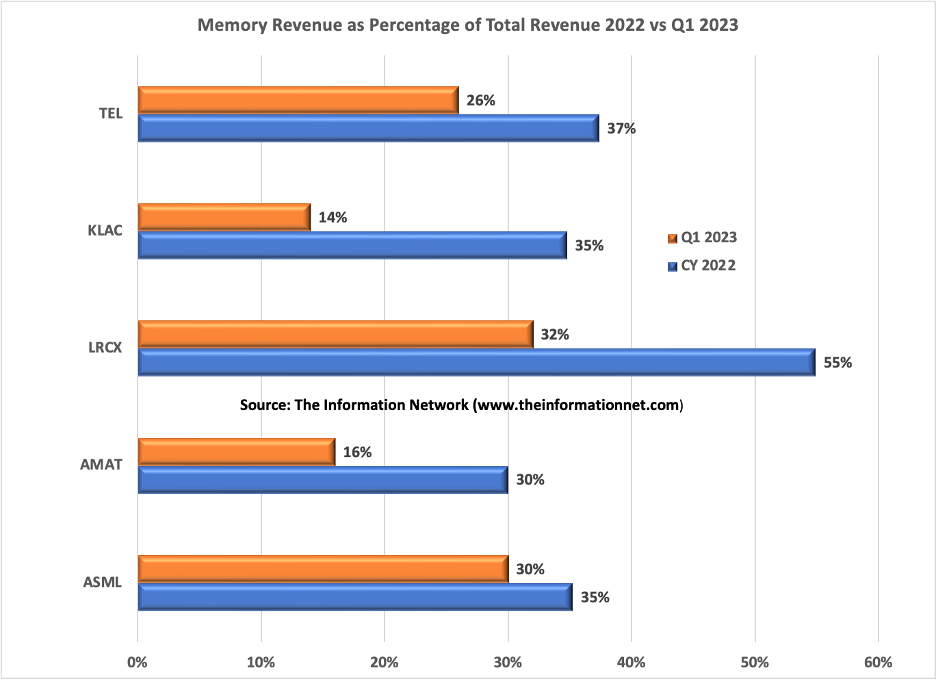

Chart 2 illustrates the data in Table 1, where I show CY 2022 memory revenue percentage (blue bar) and the drop in Q1 2023 revenue as the downturn in equipment, which I initially foretold in June 2021, takes effect.

{kind=link}

Chart 2

Competitive Position in Q1 2023

Recognizing that LRCX is impacted by its high exposure, it's imperative to determine the extent of that impact, or whether there are other factors responsible for its 40.9% drop in revenues over the past two quarters.

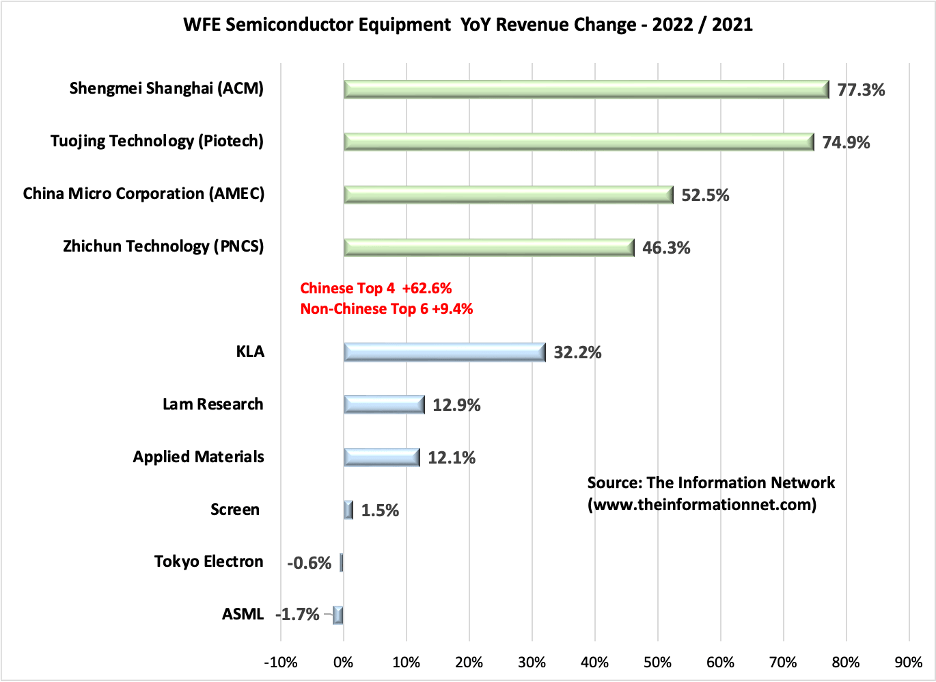

In 2022, LRCX fared well compared to competitors. Chart 3 shows that Lam's revenues grew 12.9% YoY, above the mean growth for the Top 6 companies of 9.4%.

But because of U.S. sanctions against China, which have been a catalyst for growing China's nascent equipment industry, year-over-year revenues were small compared to Chinese competitors, which had a mean growth of 62.6%.

{kind=link}

Chart 3

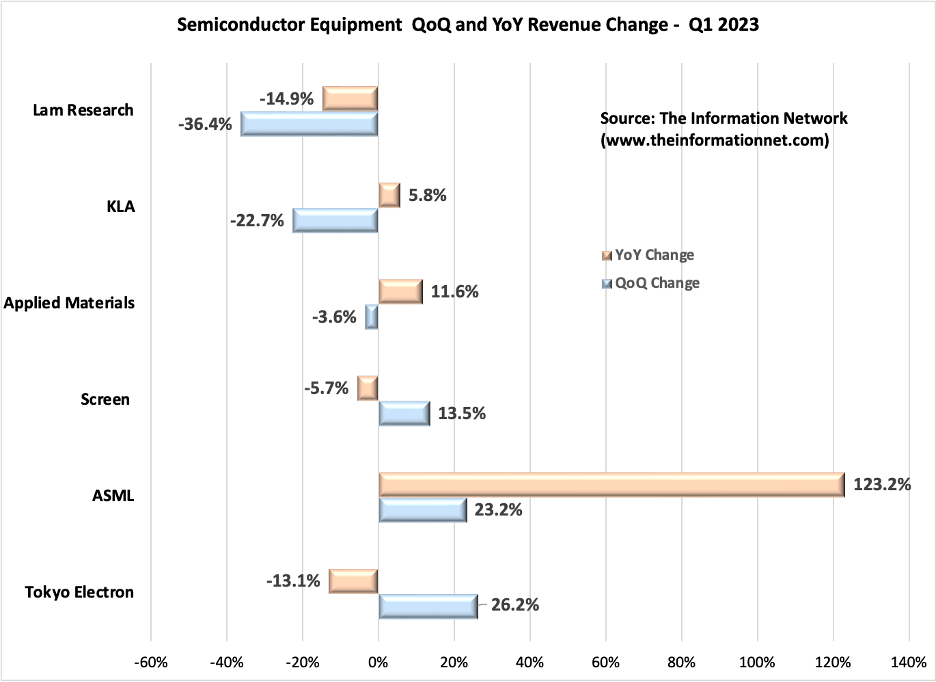

Lam's -26.7% QoQ change in total revenue in the previous quarter and consensus for another 28.9% in the current quarter is a disaster. Chart 4 shows Q1 2023 Total Semiconductor revenue change on a QoQ and YoY basis for Semiconductor equipment. On this basis, Lam's Q1 semiconductor fared significantly worse QoQ and YoY than Top 6 competitors.

If we review Memory exposure for Q1 2023 in Chart 2 above (orange bars), ASML's ( ASML ) Q1 2023 Memory revenues were 30% of Total revenue, nearly the same as Lam's 32%, yet ASML's revenue was significantly greater and different from LM'S.

Conversely, KLA's ( KLAC ) QoQ semiconductor revenue (Chart 4) change of -22.7% was similar to Lam's, yet its Memory revenues were just 14% of total revenue.

{kind=link}

Chart 4

Investor Takeaway

The downturn in Lam's revenue for the previous quarter and consensus revenues for the current quarter equate to a change -40.9% from $5.28 billion to $3.12 billion. With its high exposure to memory, which was impacted by a combination of excessive WFE spend and a poor economy, which I detailed in my Dec. 15, 2022, Seeking Alpha article entitled " Micron: Excessive Capex Spend Responsible For Plummeting Memory Market ."

Thus, the return to normalcy for memory companies will be contingent on a recovery in the consumer electronic product sales, which will reduce inventory overhand and adjust supply-demand dynamics. But this recovery also depends on strengthening macroeconomic conditions, which will improve end market demand. But currently:

- Global smartphone shipments fell to 287 million units in Q2 2022 , the lowest quarterly figure since Q2 2020, when the pandemic first hit.

- The worldwide PC market decline slowed in Q2 2023, with total shipments of desktops and notebooks down 11.5% year on year to 62.1 million units. This follows two consecutive quarters where shipments declined by over 30%. The second quarter volume represents a sequential increase in shipments by 11.9%.

The decline in both smartphones and PCs is moderating, but through first half 2023, it's still slowing. For LRCX, the turnaround in memory revenues will come once consumers start making discretionary purchases of electronic gadgets, and that has to do with the economy.

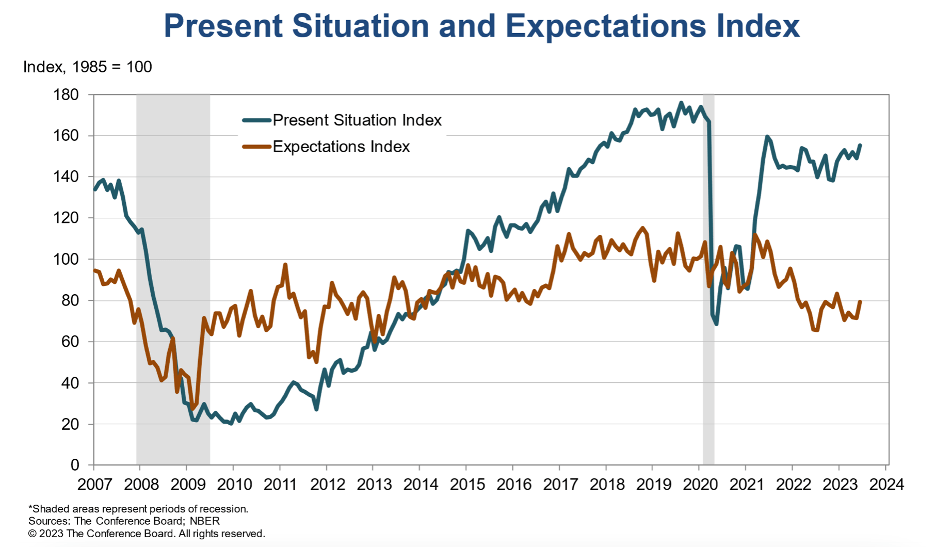

Consumer confidence is important, because if consumers feel the economy is poor or getting worse, they stop buying discretionary electronics products like PCs and smartphones.

In Chart 5, I show data from the Conference Board , showing Present Situation and Expectations Index.

{kind=link}

Chart 5

From Chart 5:

Consumers' assessment of current business conditions was more positive in June.

- 23.7% of consumers said business conditions were "good," up from 19.7% last month.

- 16.3% said business conditions were "bad," down from 16.7%.

Consumers were marginally more optimistic about the short-term business (six months) conditions outlook in June.

- 14.2% of consumers expect business conditions to improve, up from 13.2%.

- Meanwhile, 17.7% expect business conditions to worsen, down from 21.4%.

Bottom line is that even with improvements in June, only 23.7% felt they were currently good, and only 14.2% felt short-term conditions would improve.

I expect another quarter of strong negative revenue growth to be reported in the upcoming earnings call. Since the traditional segmentation of semiconductor equipment companies is either memory or foundry, Lam's dropping share of revenues from sales to memory companies means its share of foundry companies increases. But Lam's total revenues are dropping significantly.

For Q1 2023, there's no direct correlation between revenue exposure to Memory and overall revenue. And thus, the poor performance for Lam in the previous quarter and equally poor performance from guidance/consensus suggest other issues impacting the company. So there are several issues:

For most of CY2021 and CY2022, Lam has been complaining about supply chain issues. I wrote numerous articles on this such as my April 20, 2022, article entitled Lam Research: Expect More Supply Chain Woes In Upcoming Earnings Call . Lam reported in its previous earnings call that since improvement in supply chain constraints, Lam exited the March quarter having completed shipments for nearly all of its outstanding back order systems.

The impact of a ransomware attack on key supplier MKS ( MKSI ), which I discussed here: MKSI's Ransomware Attack Could Have Significant Implications For Applied Materials .

The impact of China sanctions, which I discussed here: Lam Research: Understanding FQ2 2023 Guidance Amid Memory Meltdown And China Sanctions

While these headwinds may have been transient, they nevertheless contributed to poor earnings in the past few quarters. Combine that with poor fiscal and Fed policy and the poor monitoring of capex/WFE spend by memory companies, LRCX revenue has been impacted.

I maintain my Hold rating on LRCX.

For further details see:

Lam Research Earnings: All Eyes On Memory Chip Recovery