LRCX - Lam Research: Growth Rooted In Innovation

2023-04-20 16:22:16 ET

Summary

- Product strength in core leading-edge segment propelled strong growth in FY Q3.

- Recent ground-breaking research could be a game-changer for the company and the industry.

- Setback from China export ban looks more manageable than previously expected.

- Recession headwind remains, but management has active measures in addressing it.

Investment Thesis

Company Overview

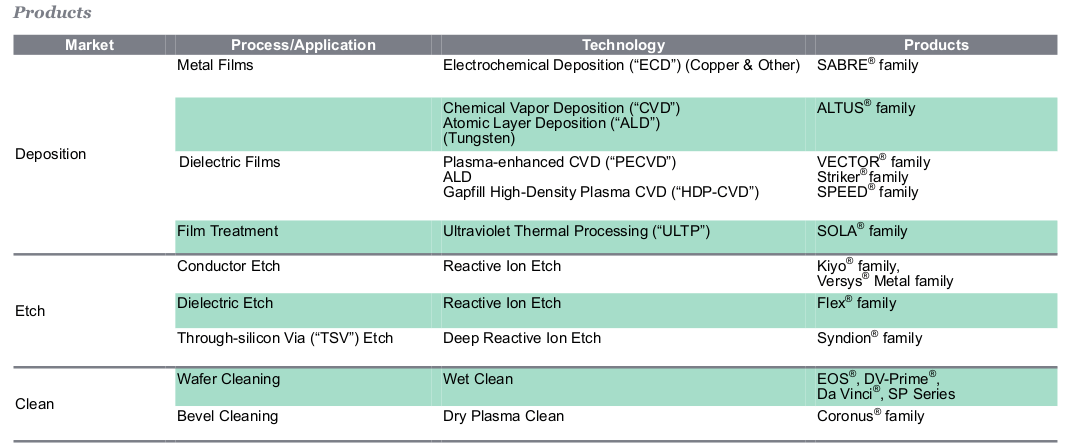

Lam Research ( LRCX ), founded in 1980 and headquartered in Freemont, California, "is a global supplier of innovative wafer fabrication equipment and services to the semiconductor industry". The company's core competence includes nanoscale applications enablement, chemistry, plasma and fluidics, advanced systems engineering, and other operational disciplines. Its products can be applied to Deposition, Etch and Clean in the semiconductor production process.

FY Q3 2023 Earnings Review

Q3 Non-GAAP EPS of $6.99 beats by $0.46, which is the fourth consecutive quarterly beat on the consensus. Revenue of $3.87B (-4.7% Y/Y) beats by $20M. We will dive into the respective aspect of its financials in the analysis below.

Strength

A review of Lam's current product offering shows that it is highly specialized in the three essential steps of every chip or transistor designing and producing process - depositing, etching, and cleaning of the films and wafers.

{kind=link}

While innovation gave birth to Lam Research by its namesake founder, it seems the company's latest research drive has yet to bring about another round of opportunities. The company recently used AI to identify a "Game-Changing Development Approach for Speeding Up, Slashing Cost of Chip Innovation". In the chip-making process, building those nanometer-sized devices on a silicon wafer is an essential phase that is currently done by human engineers. In this study, Lam's researchers used a Bayesian optimization algorithm applied to a "human first-computer last strategy" in the depositing and etching process. The study has yielded some promising results. It showed that when the algorithm is partnered with an experienced human engineer, it could slash the cost by more than half compared to less experienced engineers.

Lam

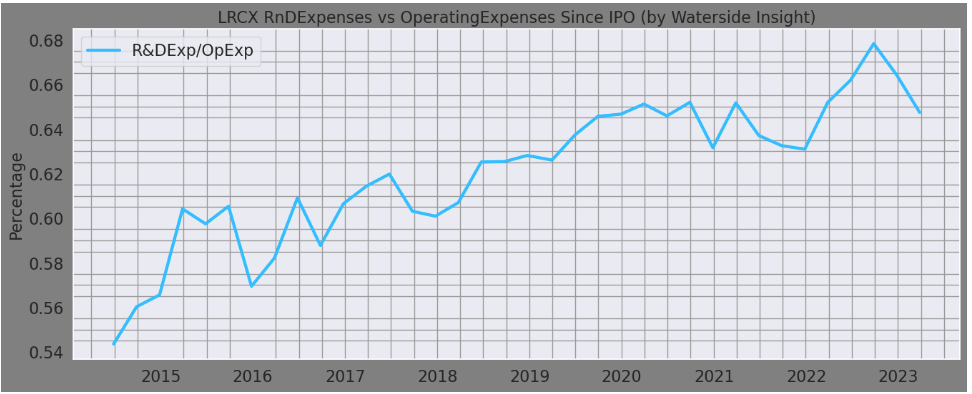

Although it is a fresh-out-of-the-oven research that could take some time to make its way into production, it indicates where Lam Research wants to go in the near-term future with its production and improvement. Behind this effort, the company's research and development expenses as a percentage of operating expenses have been climbing to higher levels historically, highlighting its research-oriented propensity.

{kind=link}

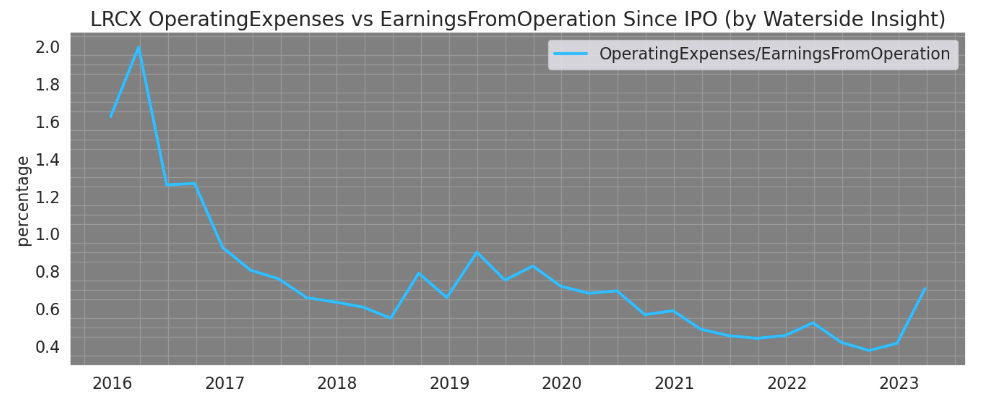

Yet in the meantime, its operating expenses have been shrinking as a percentage of earnings from operation, down by 20% compared to about five years ago. Although it had an upward spike in the most recent quarter, it is still at a similar level as in 2020. It shows that the company has been growing more efficient and focused. If the company can implement its recent research results, this ratio could continue to go down in the medium term.

{kind=link}

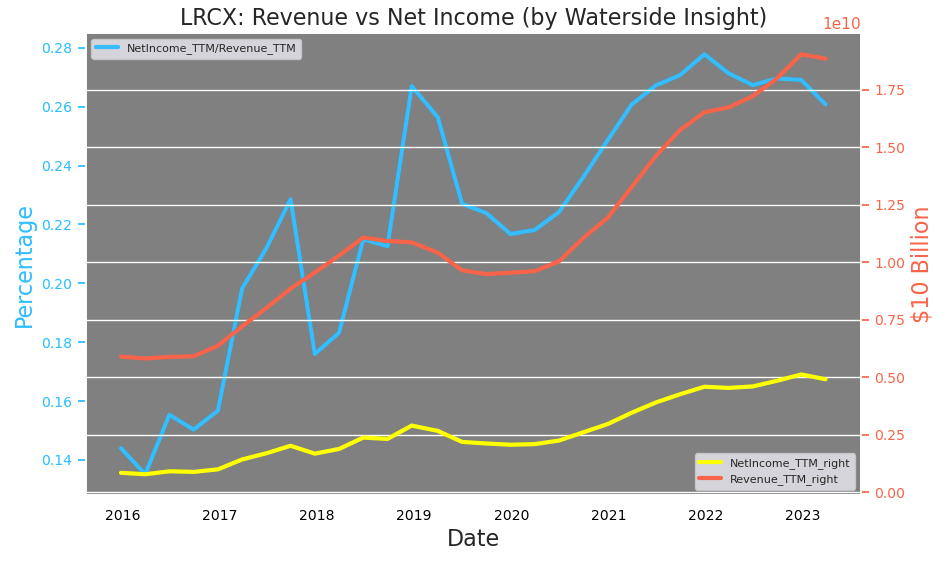

The company's revenue, reflecting continued strong customer demand for semiconductor equipment, has taken off since the recession in '08, along with its net income. The latest quarterly results have a 26.67% QoQ decline in revenue due to both scale back of demand and some seasonality. But on a TTM basis, they are still at one of their high levels. The demand from both increased investments in semiconductor capex as well as support spending, such as spares, services and upgrades, and mature node equipment, have contributed to the growth. In the last quarter, 58% of its revenue was from systems, while 42% was from customer support-related sales.

{kind=link}

By Q2 of FY 2023, Over 80% of its primary markets are in leading-edge technology, while 19% are in non-leading. Among the leading-edge technological application, Memory chips have declined from 61% to 50%, while Foundry has increased from 28% to 33% from 2021 to 2022 for the same six months ending in December. From the earnings call , its President and CEO Tim Archer stated that Lam Research achieved record foundry-related revenue in the March quarter, and its installed base for memory has increased close to 40% compared to the last down cycle. The EUV, "extreme ultraviolet" lithography's patterning and gate all-around devices are its investment focuses on processing at the atomic scale, and they are expected to gain more traction. Patterning alone is expected to be a multibillion-dollar opportunity ahead for the company. He believed the rising complexity in product manufacturing would continue to benefit Lam from the capital intensity and product strength.

Lam

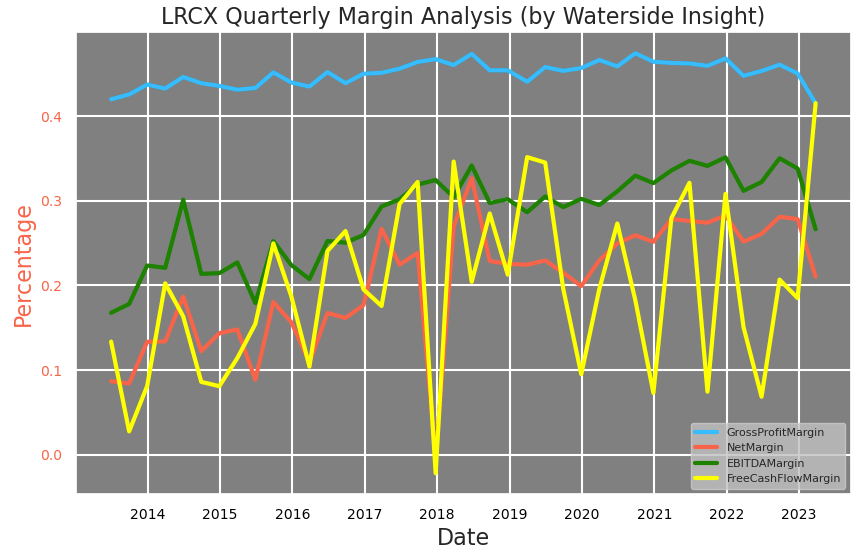

A broader examination also shows all of its margins are still in a healthy range. Although net margin and EBITDA margin have dipped, its free cash flow margin posted improvement, continuing a trend set in the last quarter.

{kind=link}

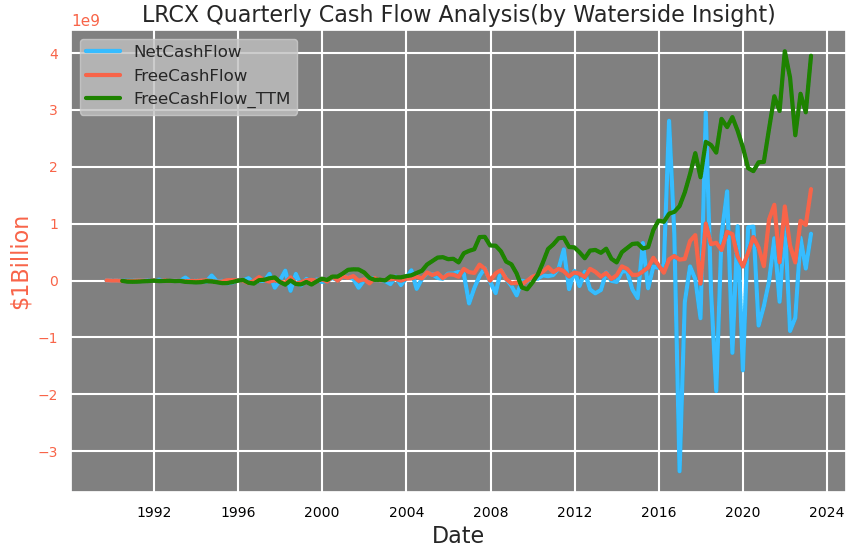

In particular, its free cash flow and net cash flow have staged rising trends. Its free cash flow is the highest on a quarterly basis, while net cash flow continued its recovery in recent quarters. Strong cash flow will allow the company to implement its growth strategy with flexibility and control overall.

{kind=link}

Weakness/Risks

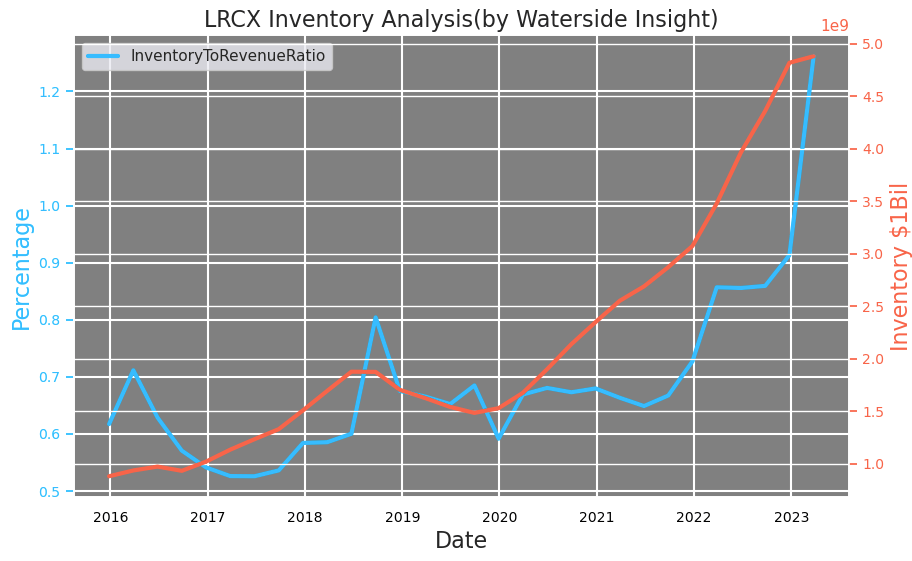

Some of the contributing factors of lower Q3 revenue were due to its Memory customers lowering fab utilization, slowing technology conversions, and reducing investments in capacity additions to limit bit output and normalize their own inventory. Therefore, Lam has a bit of a near-term problem at hand with respect to its own record-high inventory, both in absolute value and as a percentage of revenue. Its inventory turnover declined to 1.9x from the previous quarter. As its CEO addressed this issue, they will "continue to manage the inventory balance during the calendar year". Higher inventory can be good or bad depending on the logistics and inflationary challenges the company faces. Active assessment and management are indeed required, although we think it's less of a concern in the longer term.

{kind=link}

Lam has always been able to utilize its debt leverage to drive profitability effectively. This almost synchronized growth pattern of its total liability and EBITDA reflects the capital intensity in the industry's nature for the company to gain growth. The recent quarter's EBITDA drop has broken this pattern in the short term. Such a severe drop in comparison to the leverage of the capital only happened before post '08. The company actually ramped up borrowing last time to spur earnings growth, but it was from a much lower base. Its total liability has jumped almost 10-fold since then. It will need to use other ways in combination to stimulate its earnings. Its workforce reduction of about 1,400 employees and 700 temporary workers in March was a way for the company to cut costs. It even affected positions in a "somewhat higher seniority level". Hence the severance-related payments contributed to $99 million from workforce actions. It also prioritized its investment in the technology unit in a transformational change, mostly also related to its personnel, to incur a total of $250 million in FY 2023 with $144 million reflected in Q3. It shows the company's determination to restore higher profitability.

{kind=link}

The China export ban will impact Lam Research's revenue by $2 to $2.5 billion annually, according to its CEO during the earnings call in FY Q1 2023. That will be about a 13.2% cut from its topline. That means about half of its export to China is in the sensitive technological area designated in the latest restriction. Since it's been three quarters of FY 2023, reviewing its revenue by region shows that the company's sales to China indeed have dropped from 31% to 22% of the total revenue, while all other regions have seen some increases. In total, its nine months revenue ending in March has increased from $12.39 to $14.22 billion YoY, showing the company's expansion elsewhere has made up for the loss and more. For the rest of FY 2023, its export to China could go down to 18%, another 4% drop from Q3. It is likely to have been factored in the Q4 outlook given by the company of $5 a share on sales of $3.1 billion, lower than the consensus of $5.61 per share. The US-China tension is an ongoing concern, but since the company has started effectively addressing it, it looks more manageable with lesser impact than initially expected. Going forward, without being able to capture the full demand from China, it might curb its speed of growth. But Lam could more than make up by building tighter relationships with other regions. There could be another round of growth in the US which only accounted for 10% of its overall revenue. With $39 billion from the CHIPS Act for manufacturing and $11 billion for R&D, that growth in the US could accelerate in 12-18 months' time.

Lam

Financial Overview

{kind=link}

Valuation

Using all our analysis above, we assess Lam Research's fair price with a ten-year projection forward with our proprietary models. We use a cost of equity of 7.87% and WACC of 7.88%. In our bullish case, Lam still has a positive growth in FY '23 but has some setbacks in FY'24, which starts in Q3 of 2023, as the broader economy slides into a recession. But its long-term growth trajectory is strong, with double-digit growth further out in the next eight years, subject to the volatility within the semiconductor industry; it was valued at $631.73. In our bearish case, the recession slide deepened in FY '24, and the company was valued at $525.16. In our base case, we price in more volatility due to the cyclicality of the semiconductor industry while accelerating the product cycles as the manufacturing process becomes more efficient and scalable. Compared with the bullish case, it was valued at $579.11. Even after the post-earnings rally, the current price is still below our bearish estimate.

Lam

Conclusion

Lam Research has propelled its growth with constant innovation and development, as it is shown in its latest research with a promising algorithm-assisted process to accelerate the critical and complex manufacturing process. It has two main headwinds in the near term: China export ban and the macroeconomic slowdown. The company has actively addressed them with export expansion and cost-cutting measures. In the meantime, its core leading-edge products in Memory and Foundry have faster growth in Q3, which indicates its product strength even as its customer base cuts back in some of production and spending. It is likely that some of its innovation-spurred growth could overcome the recession pullback. With the growth slowdown priced in, we still reached a valuation range that is above the current market price. We recommend a buy for the stock.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Lam Research: Growth Rooted In Innovation