LRCX - Lam Research Is Still A Long-Term Buy

2023-07-11 23:35:07 ET

Summary

- Lam Research, a company that designs, manufactures, and services semiconductor processing equipment, has seen its revenues increase by 409% over the last decade.

- The company's EPS has grown by 3000% over the same period, with analysts predicting continued growth in sales and EPS in the medium term.

- Despite short-term risks, including potential tensions between the US and China, LRCX's long-term prospects look bright due to increasing demand for semiconductors and strategic partnerships.

Introduction

As a dividend growth investor, I always seek new investment opportunities in income-producing assets. I often add to my existing positions when I find them to be attractively valued, and I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital.

The semiconductors sector is interesting today as AI (artificial intelligence) is taking the front row in the tech sector. The demand for semiconductors is growing immensely as more smart devices require them. Finding an attractive company in the sector can benefit long-term returns, and Lam Research ( LRCX ) is interesting as it supplies the equipment needed to create these chips.

I will analyze Lam Research using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company's fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it's a good investment.

Seeking Alpha's company overview shows that:

Lam Research Corporation designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used to fabricate integrated circuits. The company offers ALTUS systems to deposit conformal films for tungsten metallization applications, SABRE electrochemical deposition products for copper interconnect transition that offers copper damascene manufacturing, SOLA ultraviolet thermal processing products for film treatments, and VECTOR plasma-enhanced CVD ALD products. The company sells its products and services to the semiconductors industry in the United States, China, Europe, Japan, Korea, Southeast Asia, Taiwan, and internationally. Lam Research Corporation was incorporated in 1980 and is headquartered in Fremont, California.

Fundamentals

The revenues of Lam Research have quintupled over the past decade as they increased by 409%. The company increases its sales as it sells more equipment due to the increased demand and increase in the price of the equipment. Moreover, the company is also engaged in M&A activity, which are mostly tactical acquisitions to improve the value proposition. In the future, as seen on Seeking Alpha, the analyst consensus expects Lam Research to keep growing sales at an annual rate of ~2% in the medium term.

The EPS (earnings per share) of Lam Research has shown a much more impressive growth rate over the last decade. The EPS is up by 3000% during that time. The EPS increased much faster as technological improvement allowed the company to become more efficient and increase its margins. Significant buyback activity also supported superb EPS growth. In the future, as seen on Seeking Alpha, the analyst consensus expects Lam Research to keep growing EPS at an annual rate of ~4% in the medium term.

The dividend increased by 15% last August, and investors should expect another double digits dividend increase in the coming weeks. The dividend seems extremely safe as the company grows its EPS, and the payout ratio stands at 18%, leaving the management with a lot of flexibility. The dividend yield is 1.1%, and while it is a low initial yield, there is plenty of room for growth with EPS growth and payout expansion.

In addition to dividends, the company returns capital to shareholders via buybacks. Buybacks support EPS growth as they lower the number of shares outstanding. The company has bought back nearly 20% of its shares over the last five years. Buybacks are effective when the share price is attractive, and the management will be wise to take advantage of any weakness in the share price to increase buybacks.

Valuation

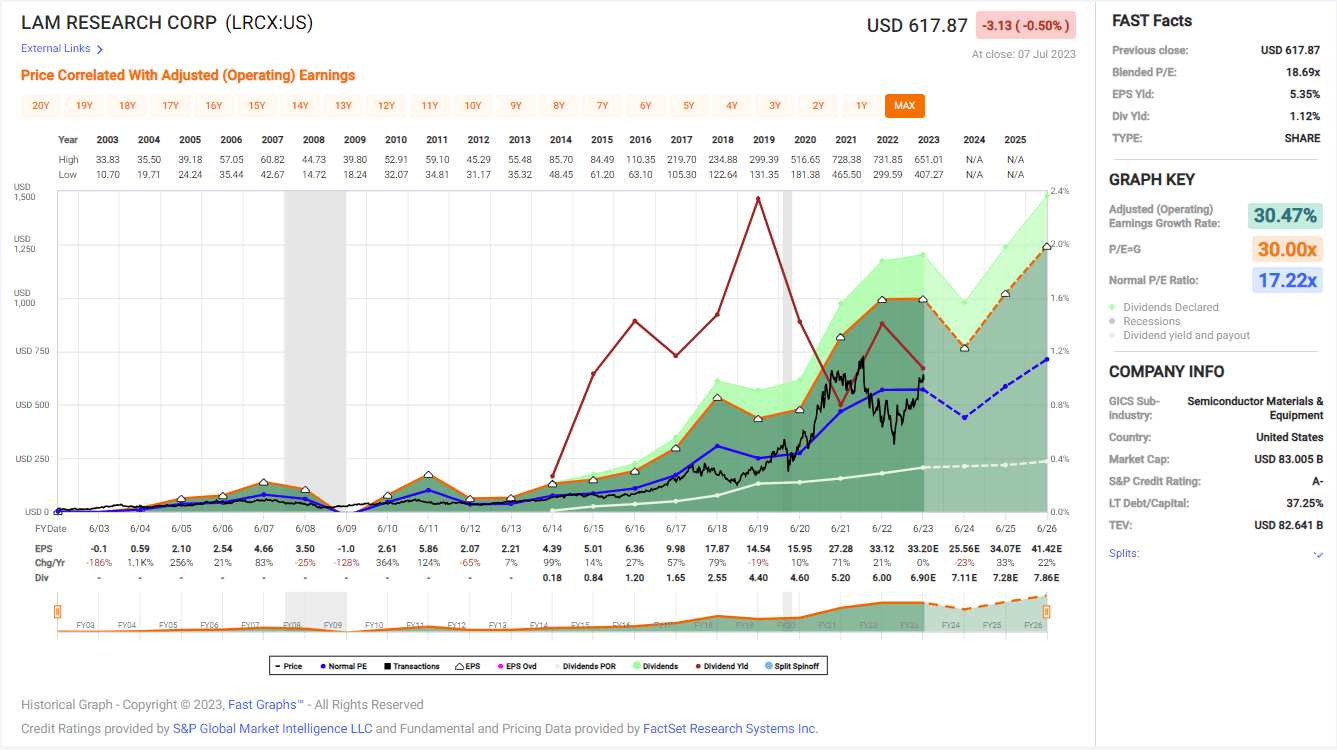

The P/E (price to earnings) ratio of Lam Research stands at 24.3 when using the EPS estimates for next year. The high P/E ratio is because analysts expect a temporary lower demand for semiconductors. The EPS expectations are for a recovery in the year after. While that is a short-term hiccup, the long-term growth trajectory should justify the current valuation. Therefore, I believe shares are fairly valued.

The graph below from Fast Graphs emphasizes that the shares are fairly valued in terms of valuation. The average P/E ratio of the company over the last two decades was 17.22, and the current forward P/E ratio stands at 24. Once the company recovers from that hiccup next year, its valuation again will be in line with the historical average. Investors should expect the company to keep growing at a double digits rate after the coming weaker twelve months.

{kind=link}

Opportunities

In the long run, demand for semiconductors is expected to grow significantly. In the past, we have seen the smartphone revolution. Then we had smart devices at home. Following that, our cars have become smart, and the use of IoT (Internet of Things) is growing at home, in our cities, and in different industries. The current catalyst is AI which requires sophisticated chips and will continue together with other trends to increase the demand for semiconductors.

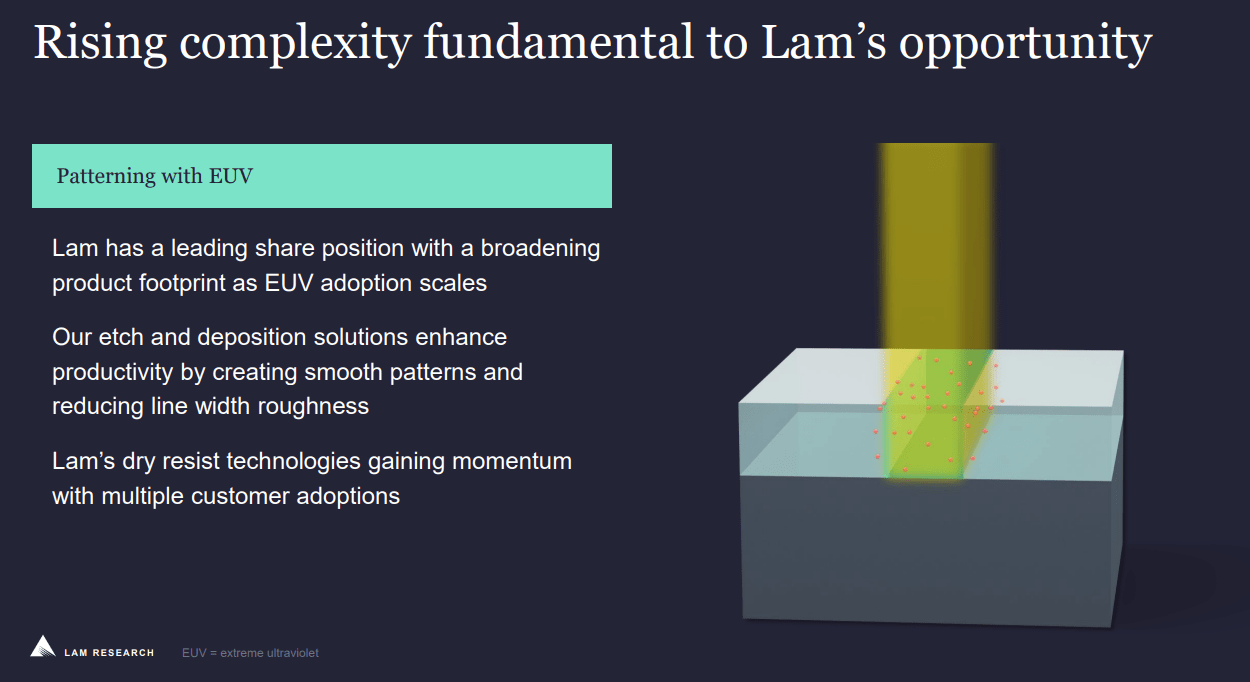

Cooperation with ASML ( ASML ) is also beneficial for both companies. ASML is practically a monopoly when it comes to EUV (extreme ultraviolet lithography) machines. The cooperation combines Lam's capabilities in etch process and ASML's capabilities in EUV machines to offer the dry resist technology that is now gaining momentum and should cement the leading position of both companies.

{kind=link}

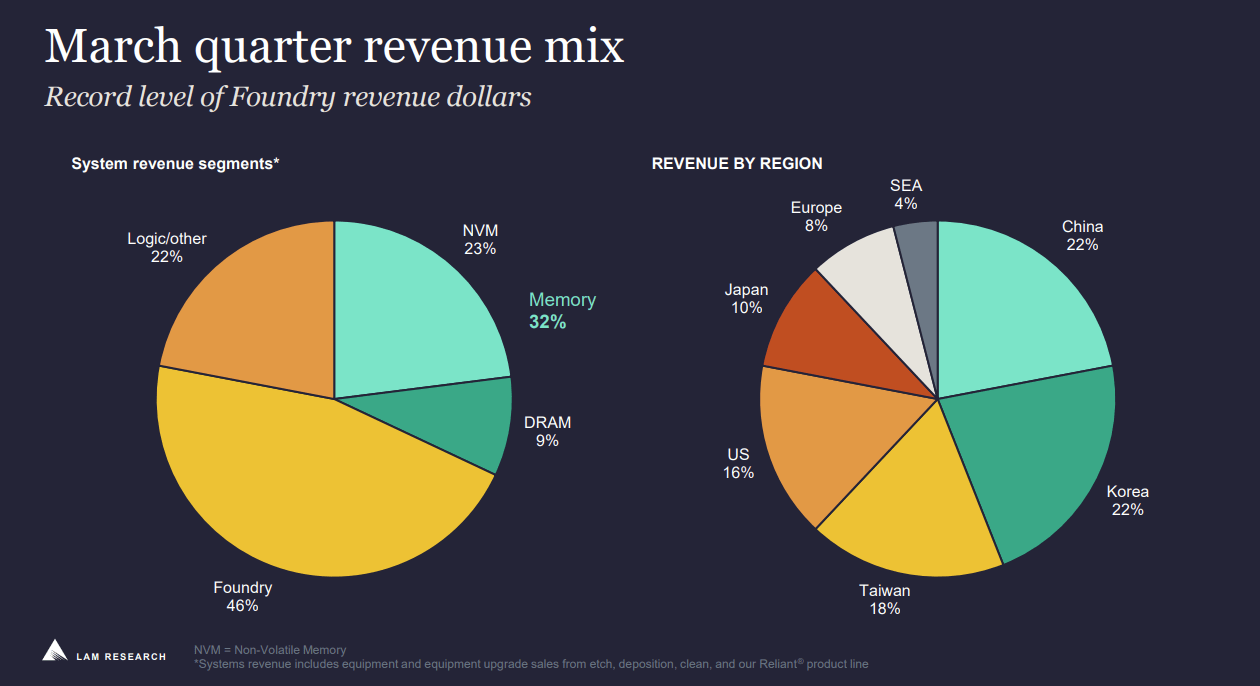

Diversification is another key opportunity for Lam Research. The company can manufacture equipment for producing different types of semiconductors and for different clients. If memory slows down, it can grow through logic and foundry. Moreover, it also enjoys geographical diversification with sales dividends between China, Korea, Taiwan, the U.S., and several more markets. Therefore, Lam Research can grow through different geographic and product lines depending on where the growing demand is.

{kind=link}

Risks

Short-term weakness might get prolonged. The first risk is the short-term risk. The company is trading for 24 times earnings, which is a reasonable valuation since investors believe it is a short-term hiccup. If we get into a recession or a slowdown, and this weakness is prolonged, additional share price declines will be declined as the current valuation may become harder to justify in the short term.

However, 22% of the company's revenues over the last quarter came from China. If the tensions between the United States and China become harsher, there may be increasing limitations on Lam's ability to sell in China. Currently, the company can still ship some of its equipment, but the procedure is complicated, and it has to constantly get clarification from regulators so it doesn't break the law.

We got some clarification on the rule -- the regulations relative to what we could ship into China provided a little bit of an upside that we believe we will ship in the second half. I describe that for Lam as a few hundred million dollars that will show up in the second half.

(Doug Bettinger - Chief Financial Officer, America Global Technology Conference, June 2023)

Another long-term risk is the competition in the semiconductors equipment sector. The long-term outlook and everyone in a rapidly expanding market looks great. However, when the growth slows down, we will see more competition for market share. Companies like KLA ( KLAC ) and ASML might compete fiercely with Lam Research. The company must invest heavily to stay up-to-date regarding its products and technology.

Conclusion

To conclude, Lam Research is a great company. It shows amazing growth of the top and bottom lines that leads to dividend growth and buybacks. The company has several fantastic growth opportunities as the demand for its product is poised to grow, and it has a strategic partnership with its peer ASML, where each company contributes its expertise.

While there are risks, they are mostly in the short term as the long-term trajectory of this industry looks bright. Its bright trajectory makes me rate the shares a BUY despite the fact that the short-term valuation may look a bit high. However, for long-term investors, it is still a decent entry point to capitalize on the long-term growth in the semiconductor demand.

For further details see:

Lam Research Is Still A Long-Term Buy