LRCX - Lam Research Q3 2023 Results: Important Takeaways

2023-04-21 05:50:56 ET

Summary

- Lam Research's revenue and earnings are down due to challenging market conditions in memory, with spending at a historic low.

- Lam Research is making the right moves to outperform when growth resumes, including heavy R&D spending and becoming a more efficient company.

- We believe shares are somewhat undervalued, although investors will likely have to be patient for the current down cycle to turn.

If one thing was made clear by Lam Research's ( LRCX ) recent quarterly results it is that the near-term demand environment remains extremely challenging, especially for memory. Things are a little bit better for foundry and logic, but unfortunately memory spending in 2023 is at a historic low as a percentage of total wafer fabrication equipment (WFE). To give an idea of just how bad things are with respect to the memory business, memory spending is down approximately 50% from 2022, led by NAND. Read our previous coverage here.

Much of this was expected, and the headwinds should eventually dissipate. In fact, as we write this article, Lam Research shares are actually up ~8% following their Q3 results, reflecting investors optimism that results were not as bad as feared and that things might start improving relatively soon. It's also helped that the company has made a huge effort to control expenses and improve operations, which has meant profitability has been less impacted than it would otherwise have been. Other positives include the company continuing to invest heavily in R&D, with a lot of promising new products expected to be launched soon which should further the company's technology moat. Finally, the installed base continues to grow, now 40% bigger compared to the last downturn, which should result in excellent growth in the parts and services business. In other words, the company is going through a very difficult period right now, but is making the right moves to outperform once growth in its markets resumes.

Q3 Results

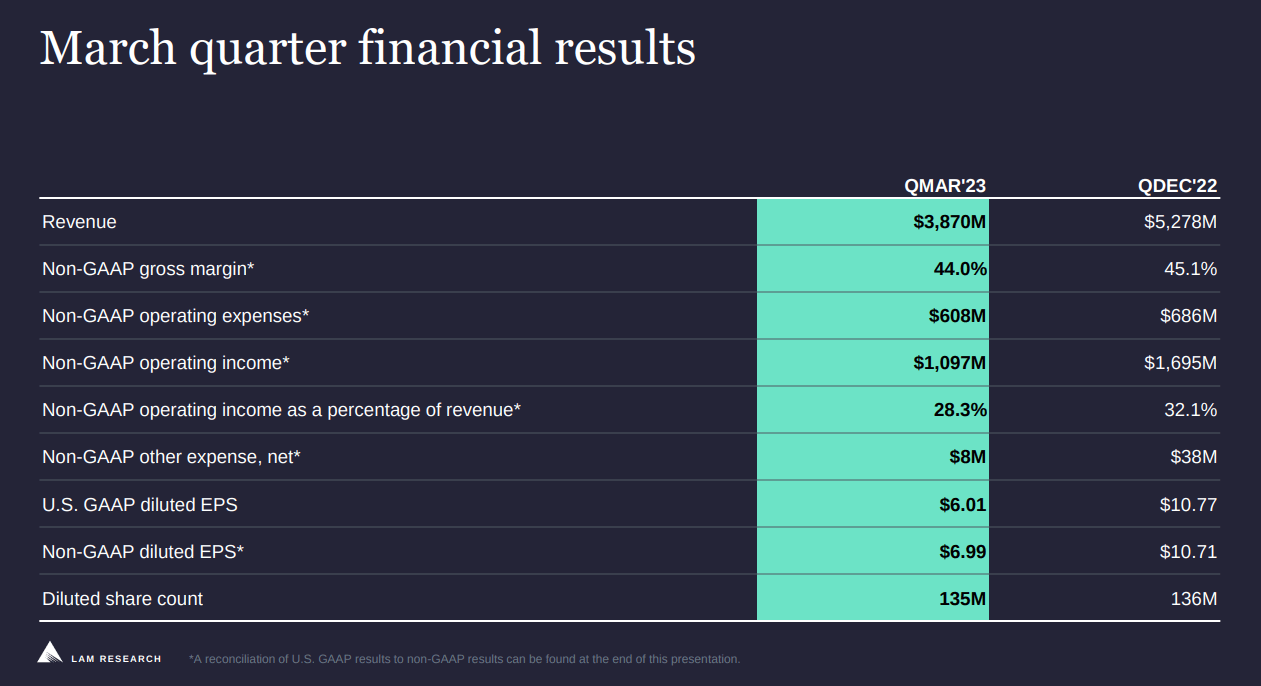

Revenue for the third fiscal quarter was $3.87 billion and EPS was $6.99. As can be seen in the slide below, that is a drastic reduction in revenue and earnings compared to the previous quarter. Still, despite the difficult environment the company manged to generate over $1.6 billion of free cash flow.

Lam Research Investor Presentation

{kind=link}

Services

The spares and services businesses performed relatively well, in large part because upgrade revenues increased. Customer's lower equipment utilization resulted in lower revenue from spare parts and services. This business continues to be one of the most resilient, reporting only a revenue decrease of 7% from the December quarter. It was up 14% compared to the March quarter in calendar 2022. In total the business brought in $1.61 billion, and Lam Research believes this is a business that can grow most years, even if it might not happen this year because of customer utilization cuts. In any case, its resiliency showed, as this segment represented over 40% of revenue in the quarter.

The Tailwind From Rising Complexity

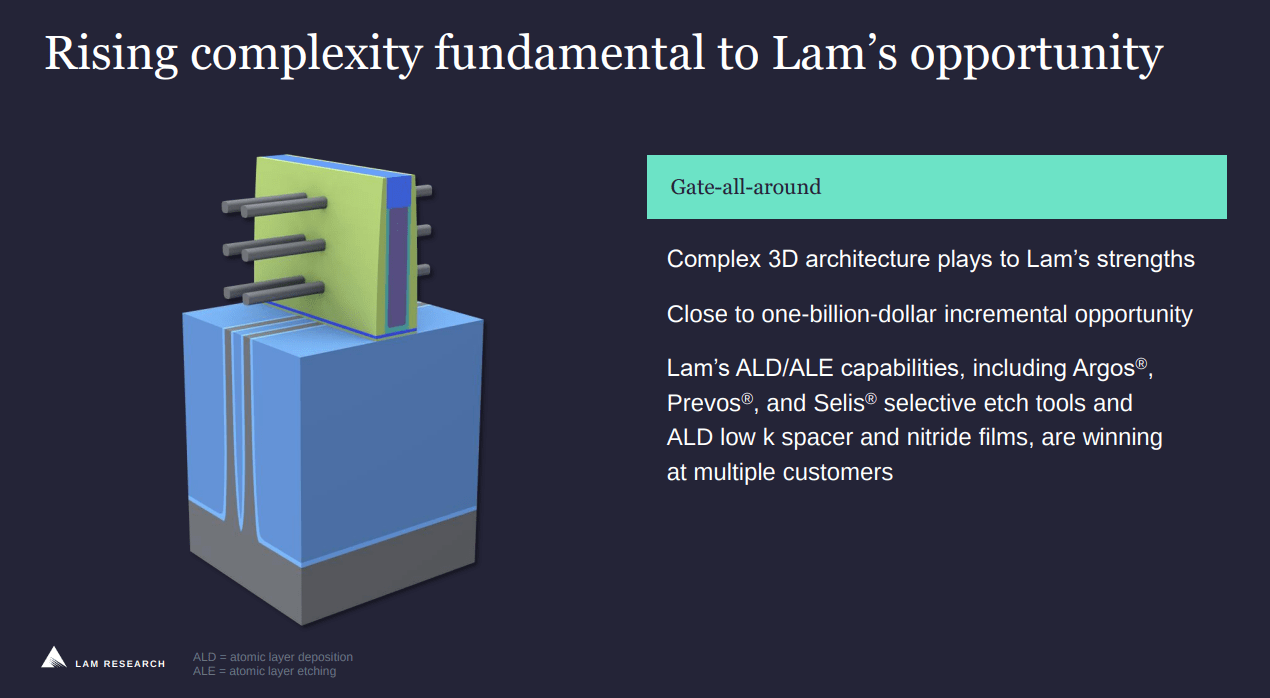

The current headwinds from lower demand should not prevent investors from seeing the long-term benefits of rising manufacturing complexity for Lam Research. As the technology gets more complex, only those are investing in the cutting-edge will be able to continue to compete and be able to charge higher prices. For example, EUV patterning and gate all-around devices are two important technology inflections where Lam Research has made significant investments in new products, for processing at the atomic scale.

Many of these new products are in the early stages of ramp-up and are expected to contribute meaningfully to growth in the future. For example, Gate-all-around could results in close to a one billion dollar incremental revenue opportunity for the company. The reason the company is likely to succeed with this new technology opportunities is because it has spent the money to stay at the cutting-edge. Recently its R&D expenses reached nearly 70% of its operating expenses, which goes to show that innovation is not an area where the company is cutting back.

Lam Research Investor Presentation

{kind=link}

Guidance

Next quarter things are expected to remain challenging, with forecasted revenue of $3.1 billion, plus or minus $300 million. The sequential decline reflects continued weakness in the memory environment. Logically, that is also likely to result in lower EPS, with the company guiding to earnings per share of $5, plus or minus $0.75. During the earnings call there was some optimism that things might start improving in the second half of 2023.

Valuation

We believe shares are currently slightly undervalued, even if they are trading with an EV/Revenues a little over the ten year average. The reason is that Lam Research has become a much more efficient and profitable company in the last few years.

Based on the net present value of our estimates for future earnings per share, and using a 10% discount rate, we believe the fair value for the shares is around ~$651.

| EPS |

| Discounted @ 10% |

| FY 23E |

| 33.37 |

| 30.34 |

| FY 24E |

| 25.77 |

| 21.30 |

| FY 25E |

| 34.22 |

| 25.71 |

| FY 26E |

| 41.93 |

| 28.64 |

| FY 27E |

| 54.15 |

| 33.62 |

| FY 28E |

| 57.94 |

| 32.71 |

| FY 29E |

| 60.84 |

| 31.22 |

| FY 30E |

| 63.88 |

| 29.80 |

| FY 31E |

| 67.07 |

| 28.45 |

| FY 32E |

| 70.43 |

| 27.15 |

| FY 33E |

| 73.95 |

| 25.92 |

| Terminal Value @ 3% terminal growth |

| 1056.41 |

| 336.60 |

| NPV |

| $651.45 |

Risks

We believe the main risk at this moment with Lam Research is that the downturn in the semiconductor fabrication equipment industry could be more severe and last longer than currently expected. Especially for memory equipment which is showing particular weakness. Longer-term there is technology risk and price competition risk, especially from potential new rivals that could emerge in low cost countries.

Conclusion

Lam Research is currently experiencing severe headwinds from a deep downturn in its industry. Still, the company has managed to cut costs and improve its efficiency, protecting its profitability to a certain degree. Importantly, it continues making significant R&D investments and the rising technology complexity should prove a tailwind for the company. The company has also benefited from the parts and services business, which has proven very resilient and is benefiting from a growing tools installed base. We view shares as slightly undervalued, and patient investors willing to wait out the downturn could be compensated once the industry returns to more normal dynamics. As such we are maintaining our 'Buy' rating and believe shares offer value at current prices.

For further details see:

Lam Research Q3 2023 Results: Important Takeaways