LRCX - Lam Research: Reaching The Upper Range Of Its Valuation (Rating Downgrade)

2023-07-13 11:07:36 ET

Summary

- Lam Research Corporation's stock has risen by over $80 or about 19% in the past two months, prompting a review of our investment thesis.

- The company's strength lies in its innovation and research, which underpins its growth, although weaknesses we specified previously became inadequately accounted for with such a fast rally.

- Despite the increase in stock price, the valuation remains the same as previous estimates, with the current price nearing the top of our bullish case.

Investment Thesis

Since our first coverage of Lam Research Corporation (LRCX) where we recommended a buy, the market has quickly caught up to our valuation. The stock has jumped by $83 or about 19% in about two months. We review our investment thesis and update our rating now to hold.

Review

In our previous article , we concluded that Lam Research Corporation has strength in innovation and research that gives deep roots to its growth, including gaining edge over its competitors and driving down its own production costs. The stock's rise by 19% is not only riding on the back of the AI frenzy, but also a vote of confidence that the investors are willing to accelerate the upside expectation for the stock. Its weakness, however, lies in higher inventory, higher debt load coupled with slower sales induced by US-China tension. Our analysis shows the last one is manageable by the company, while the first two are still risks for medium-term growth.

Analysis Update

In the past two months, significant news from the company was its achievement in introducing " Coronus DX, the industry's first bevel deposition solution optimized to address key manufacturing challenges in next-generation logic, 3D NAND, and advanced packaging applications ". This technology is part of its Coronus Family, applied in Bevel cleaning to expand its share in the application of the Clean market. It gives Lam's products another edge in leading its competitors, but the Clean market application in itself has a much smaller revenue generation than Deposition and Etch.

Lam Research: Product Application (Company 2022 Proxy Report)

Currently, the stock is at the top of our estimates. In order for it to go even higher, I think it needs higher growth prospects. Lam Research faces several hurdles in this regard.

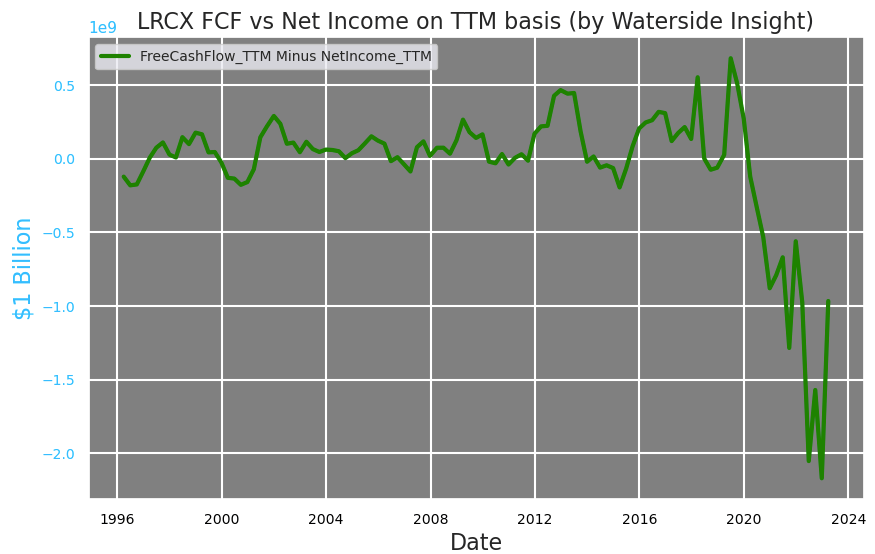

Lam's free cash flow has reached one of its highest levels in the last quarter historically, but will it be able to top this and continue a steep ascend? And will it continue to have high volatility? A simple comparison shows that the free cash flow is insufficient to keep up with the net income growth. In a simple comparison, one can see its free cash flow growth is trailing behind the net income growth on a TTM basis. The company had always been able to keep some extra free cash flow while growing its net income. That is no longer the case since 2020. It has been going on large CapEx spending. Although, in the last quarter, it has finally been able to pull free cash flow above net income, the trend on a TTM basis is still subdued.

Lam Research: Free Cash Flow vs Net Income (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

And this pulling ahead was mostly due to a large drop in the net income for the last quarter, and with its top-line growth weakened, net income could stay lower for a few more quarters. With lower net income, free cash flow is unlikely to grind higher. This scenario is priced in our bullish case in the last publication and is the main reason for our fair valuation to not be revised higher. In the end, for the company to top its highest level of free cash generation historically will be hard, while the volatility of it remains a risk.

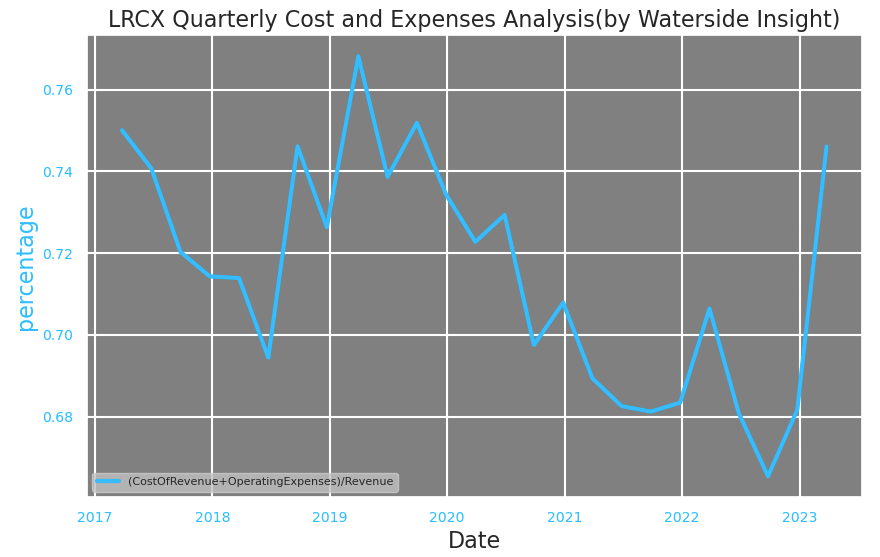

Lam's volatile free cash flow may have impacted its decision-making process. The company's CapEx has lowered by $44 million or 27% YoY in Q1. With the topline growth weakening, it will need to continue curbing its CapEx for the next few quarters to backstop this trend. This coincides with its costs and expenses ramping up in the last two quarters. In the long term, the company's competitive production edge can still drive down the expenses, but that will take time to play out. At the same time, the company's higher inventory level and the reasons that caused it we mentioned last time are still in place.

Lam Research: Quarterly Cost and Expenses Analysis (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

All these are the hurdles Lam Research is facing to attain a higher valuation from its current levels in the next six to twelve months when the recession alert is still on the horizon. Looking ahead, the next quarterly earnings results could still be dealing with these hurdles.

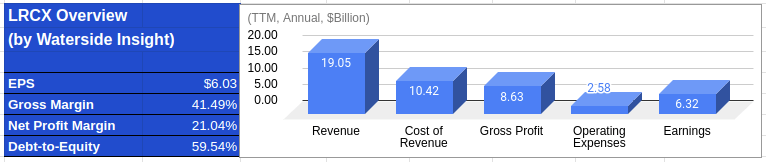

Financial Overview

Lam Research: Financial Overview (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

Valuation

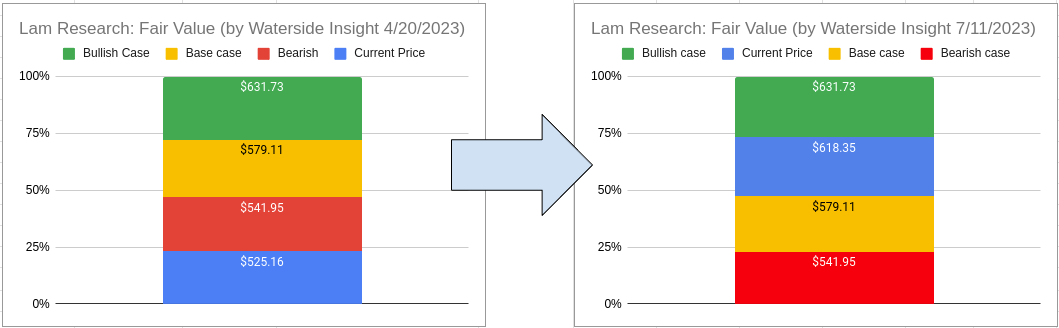

We maintain the same valuation as our previous estimates. Compared to our previous results, the only difference is the current price has moved up to almost the top of our bullish case. After reviewing the updates, we have decided against updating our valuation. The bullish case will not be extended much further from here in the near term as we still expect a slowdown in the next six months into '24. For the bullish case to be upgraded, we must first remove the near-term macro headwind hovering above the economy, on top of the several hurdles we outline above. Moreover, since the AI frenzy has helped accelerate the market's bullish expectation for Lam Research, its price is more vulnerable to downside risks. We still believed in our general bullish case for the stock in the long term, which is based on its deep-rooted innovation that thrives in complex production processes. The competitive edge of Lam Research will continue to bring in strong growth in the long term. But the current valuation has reached its near-term upside potential.

Lam Research: Fair Valuation (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

Conclusion

The past two months' rally of Lam Research came faster than we expected, bringing the stock almost doubling from its November lows of last year. The bullish case for the stock hasn't changed, but the bearish side became inadequately accounted for. The upper range of our valuation has been reached with its current prices; we suggest a hold at this point.

For further details see:

Lam Research: Reaching The Upper Range Of Its Valuation (Rating Downgrade)