LRCX - Lam Research's Strategic Dance In The Semiconductor Landscape

2023-10-20 11:34:54 ET

Summary

- Lam Research's performance metrics exceeded expectations for the second consecutive quarter.

- The wafer fabrication equipment environment is projected to reach $80 billion in spending in 2023.

- Lam Research is well-positioned to benefit from semiconductor manufacturing complexity and anticipates future growth.

- Despite some stronger than expected performances, the semiconductor industry looks to be in a cooldown period.

Following its recent earnings call, Lam Research ( LRCX ) experienced a significant selloff, a testament to the ever-evolving nature of the semiconductor industry. This sector, which surged amid the tumultuous backdrop of the mid-2019 pandemic, now appears to be entering a more tempered phase, leading to a recalibration of previously soaring stocks. The semiconductor landscape has often been likened to a roller-coaster, with its cyclical ups and downs. As we witness this industry-wide cool-down, the age-old narrative of semiconductor cyclicality re-emerges, causing investors to brace for potential market downturns, even as the landscape continually transforms. In this piece, we'll delve deep into Lam's current position and offer insights on what investors might anticipate in the days to come.

(I have covered this company in the past. For a more detailed company profile, follow this link )

Earnings Download

Before diving deep, let's discuss the recent report. Lam reported revenue figures that exceeded many of their own forecasts. Achieving a revenue of $3.48 billion in the September quarter, up 9% from the prior one, is no trivial feat, but it will be overshadowed when seen in the context of the over 30% YoY decrease.

Management drew attention to the deferred revenue balance, which stood at $1.69 billion. While this marked a decline from the June quarter, it's vital to note that this relates predominantly to the recognition of revenue tied to customer advance payments. With the expectation of recognizing a portion of these deposits in the upcoming December quarter, the projections for the deferred revenue balance in 2024 are noteworthy but not redeeming. The main takeaway here is that the semiconductor companies are working through an inventory glut created by an overreaction to the supply chain constraints that we saw in the pandemic, along with cooling demand.

Margin Performance – Stubbornly Strong

Operating at a gross margin of 47.9%, the company surpassed its own guided range. Compared to the June quarter's 45.7%, this growth is largely due to favorable customer mix dynamics.

The main concern was always margin compression, which hasn't really happened yet. We have seen some serious compression in past slowdowns, and with signs of cooling demand, it remains a major item to focus on.

Semiconductors are undeniably one of the most cyclical industries globally. Historically, during global downturns, they have experienced significant declines, paving the way for prime buying opportunities as a new business cycle commences. While it's a trope often heard, there are compelling reasons to believe the current scenario might be an exception. The convergence of artificial intelligence, escalating device intricacy, and the expansion of the Internet of Things ((IOT)) have generated unprecedented momentum for the sector. For budding investors, this implies that even if there's a downturn, the rock-bottom prices witnessed in yesteryears might remain elusive. The crux of the matter is, the longer the investment horizon for semiconductor stocks, the more compelling the rationale to invest. If, a decade from now, semiconductors become redundant, it's probable that the world would be grappling with concerns far graver than a mere investment portfolio. Moreover, recent reports hint at a diverse performance trajectory across different business sectors, lending a more optimistic perspective to the latest results.

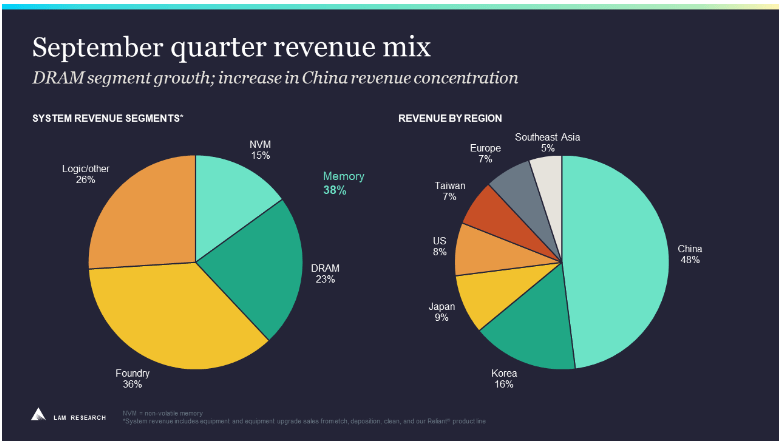

Memory : This segment saw a growth spurt. System revenues from memory reached 38%, up from the previous quarter's 27%. This growth is attributed mainly to DRAM's sequential increase.

Foundry : Representing 36% of systems revenue, the foundry segment did see a dip from the previous quarter. However, the decline is seemingly due to the timing of leading-edge investments in 2023.

Logic and Other : Staying steady at 26%, the investments in this segment showed a noticeable inclination towards specialty devices.

{kind=link}

China on the Rise

Shifting our gaze to the geographical landscape, China has not just left a mark but set a benchmark. The nation now accounts for an astonishing 48% of Lam Research's revenue, a significant leap from its previous 26%. But here's the twist - a vast portion of this financial injection emanated from China's domestic clientele. This suggests not just a fleeting trend but a rooted growth and consolidation within the Chinese market.

However, it's not all smooth sailing. Despite the stellar China performance, looming clouds of uncertainty cast shadows over the future. With the mounting inclination of major global powers to regionalize semiconductor production, the stability of this revenue stream may face turbulence in FY24. Let's put this into perspective: we're talking about nearly half of Lam's revenue. So, while the company maintains an optimistic stance on sustaining this segment, the path forward might be strewn with challenges.

Capital Return & Shareholders – The Mutual Love Affair

Lam's dedication to its shareholders shone brightly. The company earmarked approximately $830 million for open market share repurchases and splurged on $230 million in dividends in the September quarter. This caps the company's proud history of raising the dividend amount nine times since its inception in 2014.

The Road Ahead

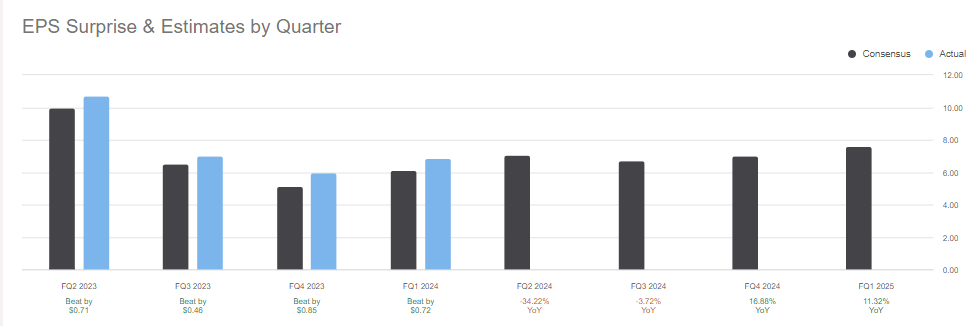

Lam Research's forward-thinking strategy is evident in its non-GAAP projections for December 2023, suggesting a promising revenue outlook of $3.7 billion. This isn't just a mere statistic—it's an assertion. Lam isn't merely adapting to the times; it's paving its path forward. Anticipating and acting on future technical challenges, Lam stands at the forefront of innovative breakthroughs. Its engagement in pioneering projects, such as backside power delivery, transcends strategic choices—it embodies a visionary spirit in my view. This cutting-edge initiative has the potential to catapult the SAM by an impressive $1 billion, contingent on every 100,000 monthly wafer starts. However, a note of caution is essential. Emerging from one of the most vibrant semiconductor markets in recent memory, the current EPS trends indicate a transition into a more moderate phase.

But even amidst projected EPS dips, Lam consistently outperforms market predictions. Setting aside the China quandary, I believe Lam's current trajectory shows minimal threats, positioning the company to hit its $7 EPS target by December comfortably.

{kind=link}

Despite the expected EPS reductions, the company still does a good job beating estimates. The problem for shareholders is that the market seems to know this. A look at historical PE and PS ratios shows that this stock is priced at long-term averages despite clear downside risks on the horizon.

In terms of the upside potential, it is hard to see large catalysts to the upside in the short term. We are seeing cooling demand for ample inventory with a possible economic slowdown as the Fed's rate hikes will likely begin to bite over the coming quarters.

The Takeaway

Lam Research continues to establish itself as a trailblazer in the semiconductor domain, highlighting its prowess with consistent outperformance against market estimates. The company's current trajectory, underscored by its robust revenue outlook and forward-thinking initiatives like the backside power delivery, denotes more than just mere numbers—it signals a transformative vision. That said, while the semiconductor arena is notoriously cyclical, the current landscape, enriched by technological advancements and global digital shifts, might hint at an atypical cycle. As investors gaze into the crystal ball, discerning between transient market jitters and genuine long-term concerns will be pivotal. And for those with a longer investment horizon, Lam Research seems poised to continue its dance on the cutting edge, even if it occasionally misses a beat or two. I love the company, but broader macroeconomic headwinds lead me to believe cheaper prices are on the horizon. The investment thesis here depends on the timeframe. I look forward to rebuilding my position at lower prices over the coming quarters, but for now, Lam Research is a hold.

For further details see:

Lam Research's Strategic Dance In The Semiconductor Landscape