LRCX - Lam Research: Strong Execution Attractive Valuation

Summary

- Lam Research is well positioned to benefit from the increase in semiconductor manufacturing capacity and has executed well in a tough environment.

- Despite their operational success and growth prospects, the stock has sold off over the past year.

- Due to an attractive valuation, we believe now is a good time for long-term investors to buy Lam Research.

Thesis

Lam Research ( LRCX ) has done surprisingly well in an environment that has been difficult for many companies in the semiconductor industry. We believe that Lam Research is a buy at these levels because of their continued execution and attractive valuation.

Strong Execution

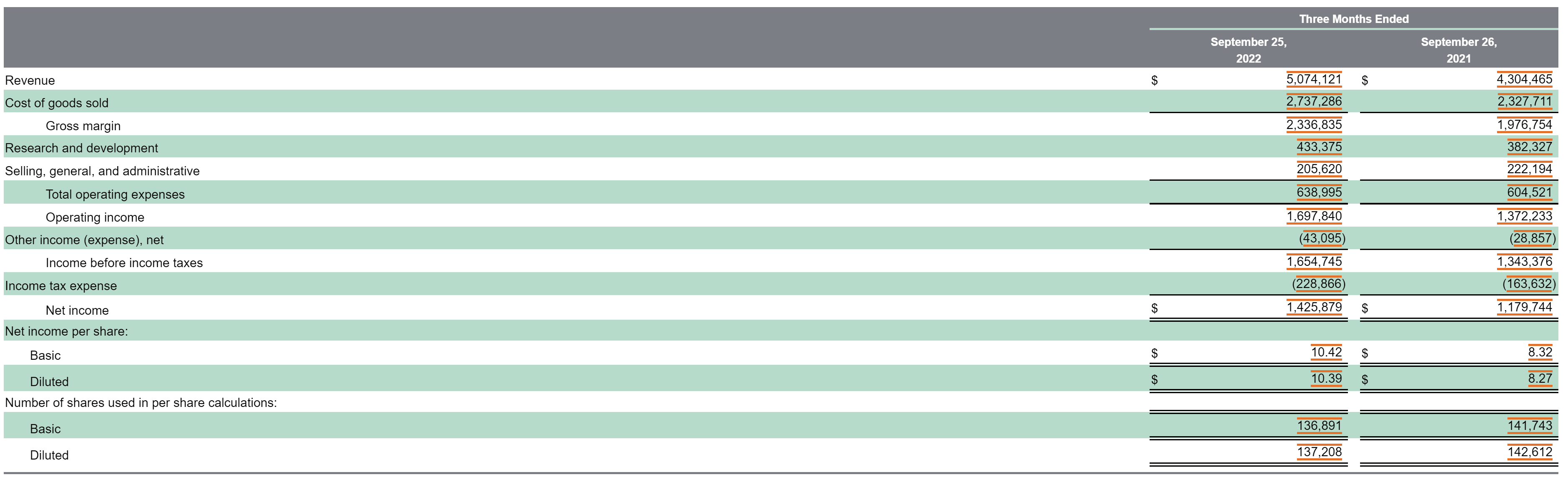

In their most recent quarter Lam Research posted revenue growth of 17.88% and operating income growth of 23.72%.

Q3 Income Statement (Lam Research Q3 Earnings Report)

{kind=link}

This is especially impressive when we consider that this macro environment has been difficult for many companies in the semiconductor industry. Lam Research has been executing well in a tough environment and this reflects well on their industry positioning and competitive advantages. The increasing demand for WFE should fuel the growth of Lam for many years to come.

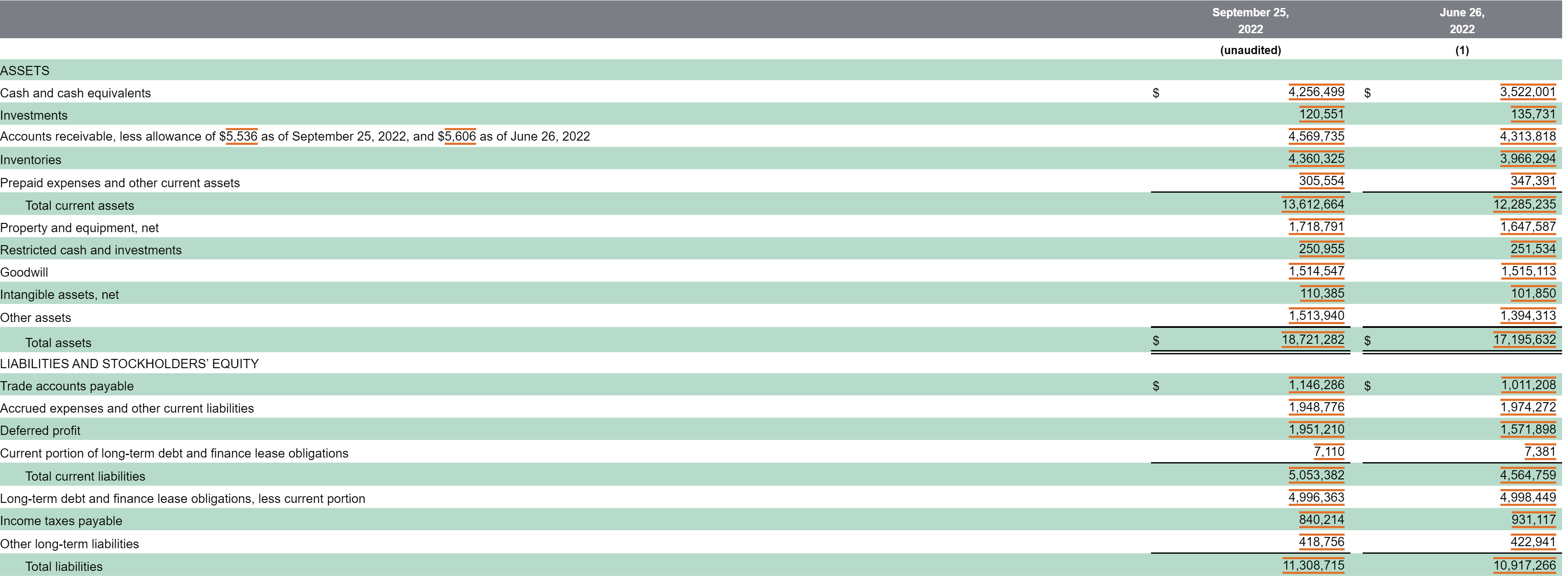

Lam Research has a high quality balance sheet with almost as much cash on hand as debt. They could pay off their debt with a little more than a year's worth of earnings. This is always a good sign as it shows that Lam is not overleveraged and that they have good financial management. Good financial management leads to operational flexibility over the long-run which is especially important for companies that are expected to constantly innovate.

Q3 Balance Sheet (Lam Research Q3 Earnings Report)

{kind=link}

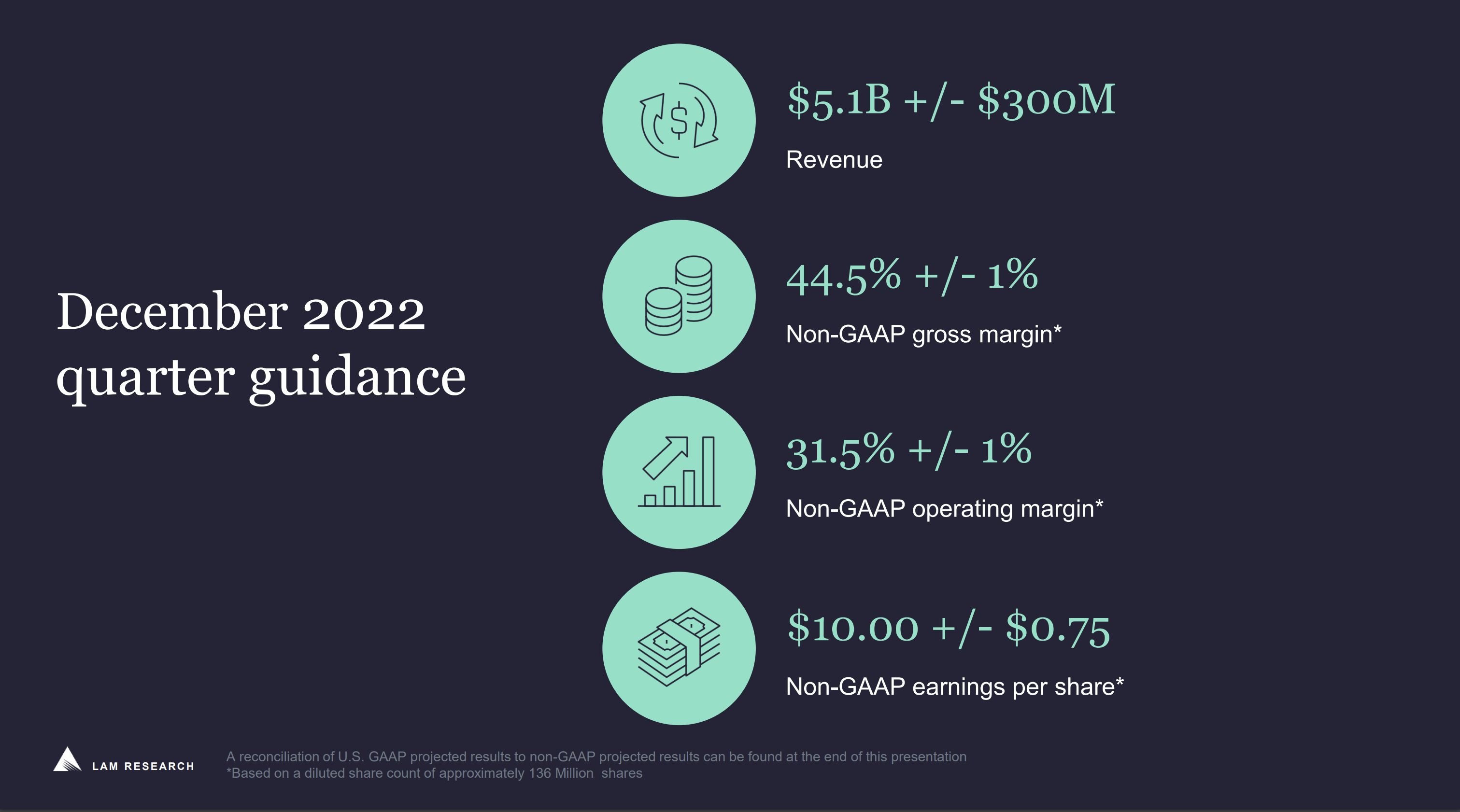

The guidance for Q4 was a little bit light and it wouldn't take much for Lam Research to surpass it. This could be a case of management wanting to be conservative given the difficult operating environment and it wouldn't surprise us to see them beat on both the top and bottom lines in Q4.

Q4 Guidance (Lam Research Q3 Earnings Presentation)

{kind=link}

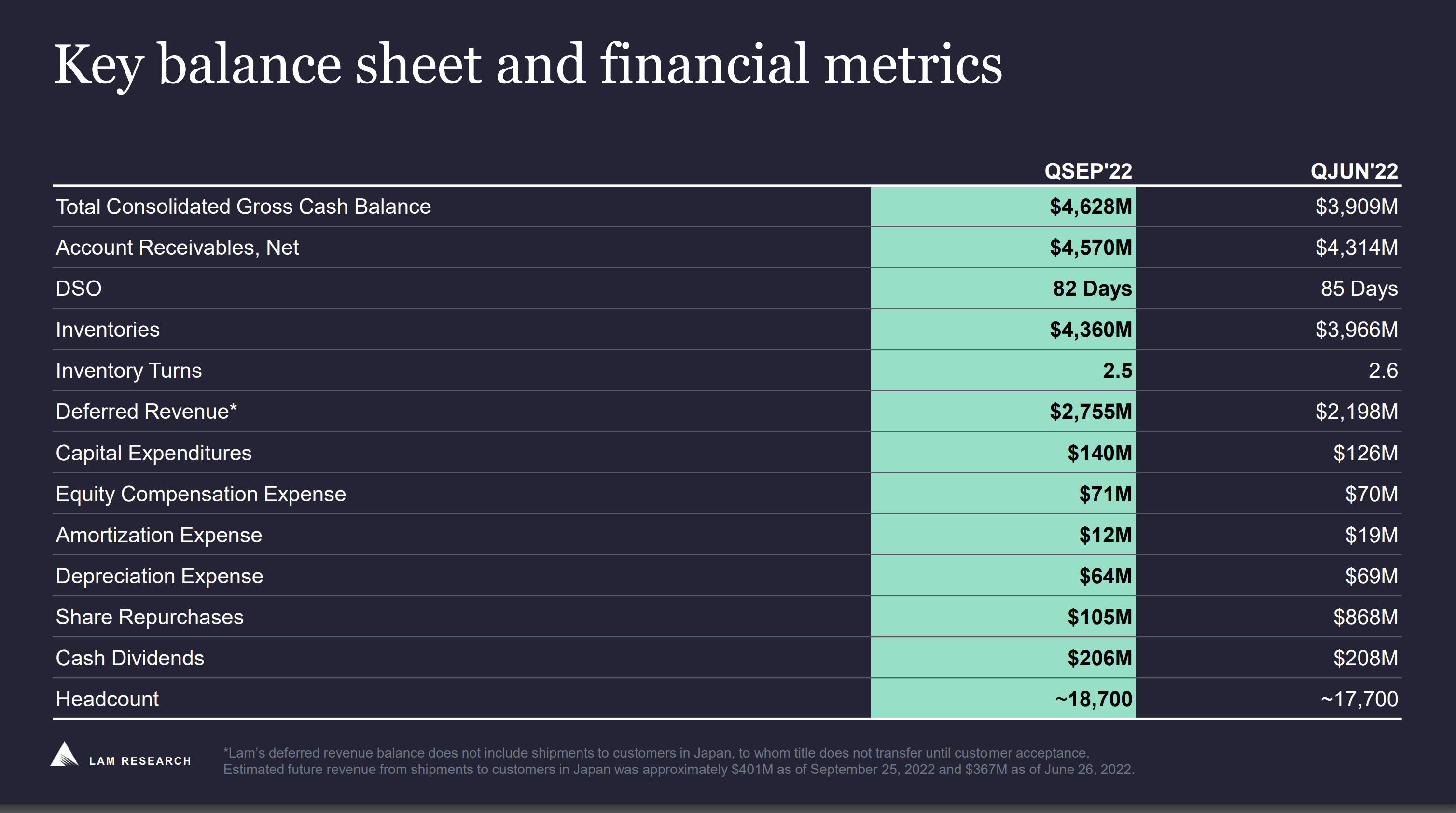

When we take a closer look at their financial metrics we can see a clear operational trend by management. Management has decided to increase their cash on hand and drastically decrease their amount of share repurchases. This is a prudent decision and shows that management is willing to be financially disciplined and prepare for a worst case scenario. If the operating environment improves it can be reasonably expected that management will resume their former pace of share buybacks.

Key Financial Metrics (Lam Research Q3 Earnings Presentation)

{kind=link}

Lam Research has been executing well and is positioned nicely to capitalize on the buildout of semiconductor manufacturing capacity around the globe. Despite their execution and strong financial position the stock has been heavily punished over the past year. We view these depressed prices as a buying opportunity.

Price Action

Lam Research has not fared well over the past year, with their stock declining by over 30% compared to the 12.82% drop in the S&P 500. This underperformance is more a reflection of investor fear than it is a reflection of Lam's operating results. The company has done remarkably well given the circumstances, yet the stock has been punished anyways.

We believe that the stock is oversold and trades at an attractive valuation.

Valuation

Lam Research trades at a PE of 13.58, which is lower than their historical average. The semiconductor industry has matured a lot over the past decade, and there is a case to be made that Lam should trade at a premium to their historical PE multiple, but they are instead trading at a discount.

Lam has shown choppy revenue growth numbers but this is more a product of their industry than it is their own decisions or execution. Their long-term growth is well above that of the S&P 500 yet the stock trades at a discount.

We believe that Lam Research is undervalued based on their current valuation and growth prospects. We believe that Lam should trade at a multiple of 20x trailing earnings to more accurately reflect their growth potential and get more in line with their historical averages. This would equate to a stock price of $559.40, which is an increase of 18.09% from these levels. It's important to note that analysts expect a sharp earnings contraction over the next 12 months, and should that earnings decline fail to materialize shares could go much higher than our estimate.

Risks

There are some major risks to the bull thesis that investors need to consider.

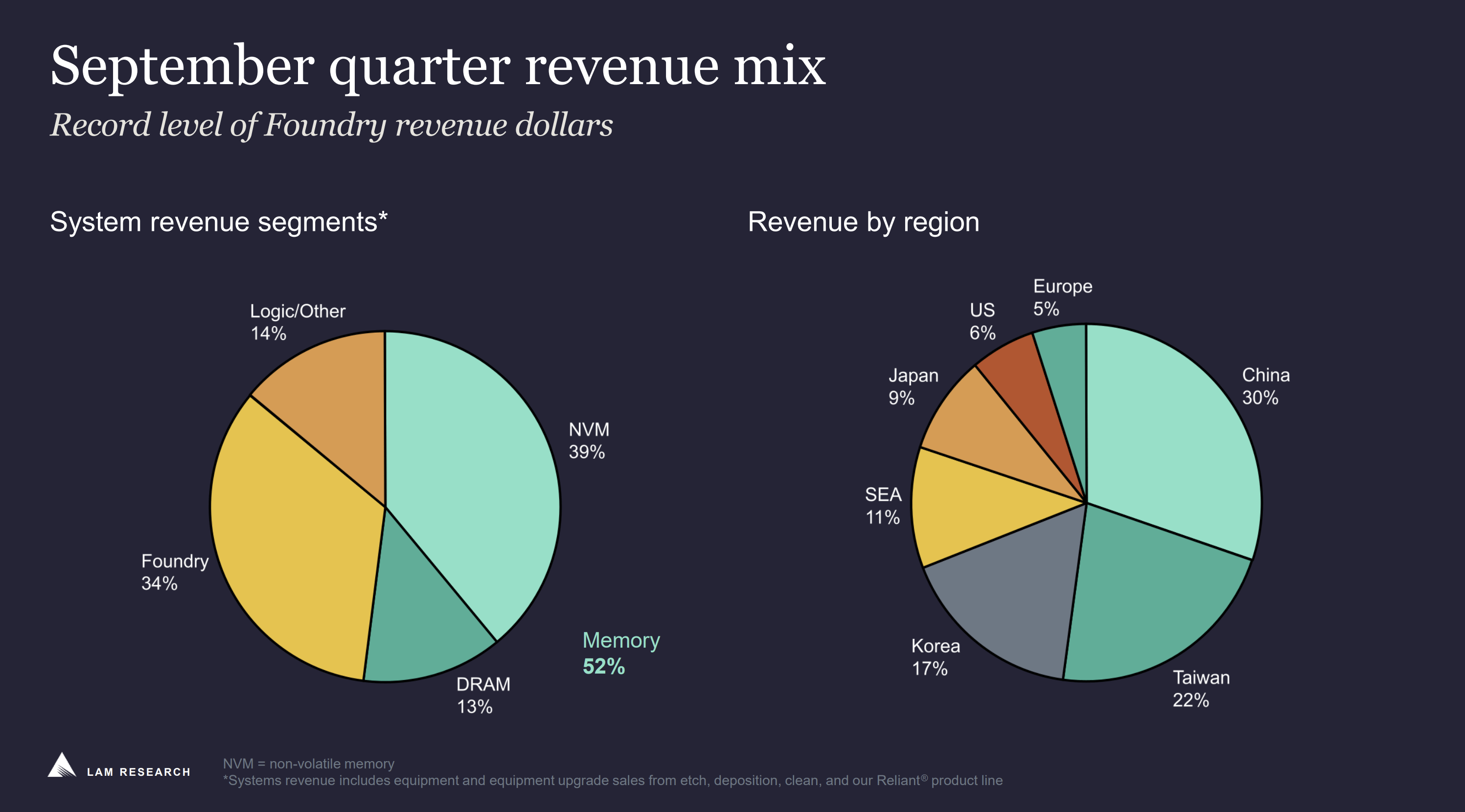

Lam Research earns 30% of their revenue from customers in China and 22% from customers in Taiwan. If geopolitical tensions were to escalate further it could severely impact their revenue.

Revenue Mix (Lam Research Q3 Earnings Presentation)

{kind=link}

A prolonged slowdown in the semiconductor industry would negatively impact WFE equipment orders and slow the revenue growth of Lam Research.

If the semi industry doesn't need as much capacity as expected, foundries will lower their total WFE budget leading to lower revenues for Lam.

New WFE technologies could be developed that would disadvantage Lam and lead to their customers choosing to purchase from a competitor.

All of these risks are significant and must be considered. That being said we like the overall risk/reward at this price and will continue to monitor these risks, especially when it comes to geopolitical risk.

Key Takeaway

Lam Research has done well to continue to grow revenue and earnings in a tough environment. Their balance sheet is rock solid and they are well positioned to take advantage of secular trends in the semiconductor industry. We believe the stock is a buy at this depressed valuation multiple, however investors should familiarize themselves with the industry and associated risks before making a purchase.

For further details see:

Lam Research: Strong Execution, Attractive Valuation