LRCX - Lam Research: Waiting For A Better Entry

2023-03-09 13:37:02 ET

Summary

- Lam Research Corporation has a high level of exposure to the memory sector among large-cap semiconductor companies.

- Lam Research still has edge in memory chip technology with its advanced chipmaking equipment, such as etching and deposition.

- I expect a cyclical upturn in the back half of CY24 and maintain a Hold rating on Lam Research Corporation for now.

Thesis

Lam Research Corporation (LRCX) is a dominant player in various areas of the semiconductor industry, such as plasma etch, thin-film deposition (including metal and dielectric), photoresist strip systems, and single-wafer wet/plasma-based cleaning products. The company's existing customer base consistently performs well regardless of market fluctuations. The demand in 2023 is expected to be weak, especially from memory-chip customers and also Chinese clients due to a U.S. ban on tool exports.

Lam Research Corporation's etching and deposition equipment is indispensable for making advanced NAND-memory chips, such as those with 176 layers, could keep a dominant market share for 3D NAND-making tools in the long term, boosted by a portfolio of high-margin products in a concentrated market. However, LRCX is up 19% YTD, and with reducing WFE spending and slowing demand, I currently do not see much upside in the near-term, which is why I keep a Hold rating on Lam Research Corporation stock.

{kind=link}

Post-2Q Earnings Outlook

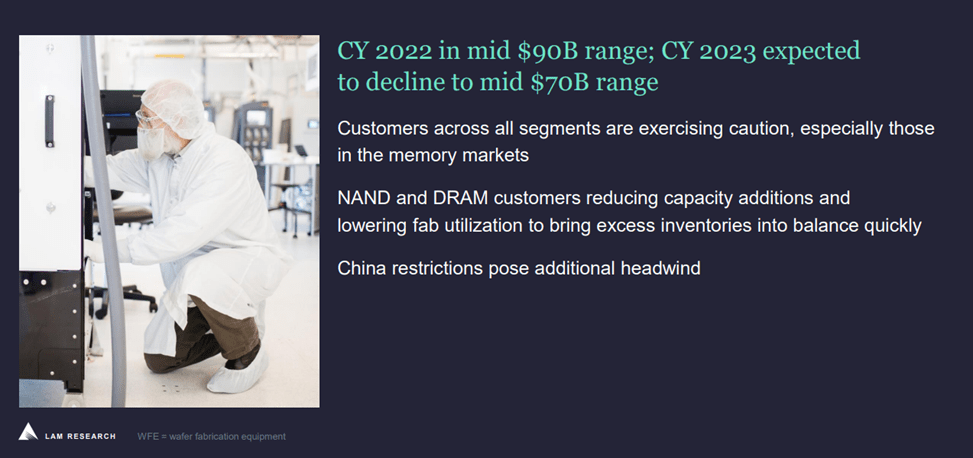

LRCX posted strong earnings and revenue growth in its fiscal Q2 2023 , beating market estimates. However, the company's revenue in fiscal 3Q ending in March could drop from a year earlier and sequentially after growth of 25% year-over-year in 2Q. Demand from memory-chip customers, which is 50% of its revenue, may decline due to oversupply , particularly NAND flash-memory chips. A U.S. ban on tool exports to China could also be an impediment. Lam is reducing about 7% of staff, which may lead to a 1% of improvement in gross-profit margin.

Considering the current economic uncertainty and decreased spending by memory makers to balance supply and demand, the management's conservative approach towards 2023 seems justified in my view. Although the company reported strong results for the December quarter, its forecast for the future is cautious as it faces the impact of U.S. export restrictions to China and a significant decline in memory demand. Although there may be a slight decline in the services sector due to lower utilizations and restrictions in China, Lam Research is expected to maintain its strong earnings power through its operational leverage.

Anticipating Significant Reductions in Memory Spending

With the supply improvements, the equipment suppliers will overcome their issues of the past and ship against their large backlogs while rightsizing inventory. Due LRCX's deferred revenue, I believe that the previous quarter largely remain insulated, but I believe we would see the effect in the next few quarters.

The management guided WFE spending to decrease by 21% in CY23, primarily due to cuts in capex and delays in nodal transition by memory manufacturers, as well as weak demand for foundry and logic customers. However, Lam's services business is expected to hold up well in the long run due to strong ratable services agreements and increasing dollar per chamber. The company has seen a significant increase in installed base over the past few years and has strong tailwinds in memory and foundry/logic transitions. The company has also gained share at Intel on every new technology generation, which is a positive factor for its logic segment. Despite weaker fundamentals, Lam Research Corporation is expected to maintain strong earnings power due to operational leverage and strong execution by the team.

{kind=link}

Lam Research Still has Edge in Memory Chip Technology Revolution

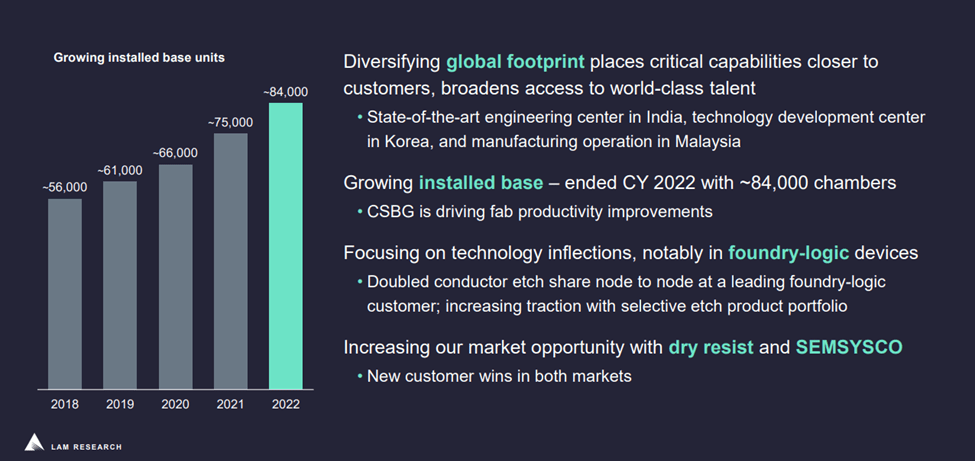

Lam Research can draw long-term benefits from memory chip technology's evolution with its advanced chipmaking equipment, such as etching and deposition. Despite its vulnerability to choppy sales in 2023 due to high exposure to memory chips, increasing hyperscale data centers, and artificial intelligence applications, big data and the metaverse are likely to drive solid DRAM production. Device sales may also gain on 3D-NAND transitions from 200 or more layers to 500 in five to six years. Sales from logic and foundry customers could also rise on new transistor structures such as gate-all-around .

Positioning to capitalize on long-term demand trends (Company Presentation)

{kind=link}

Valuation

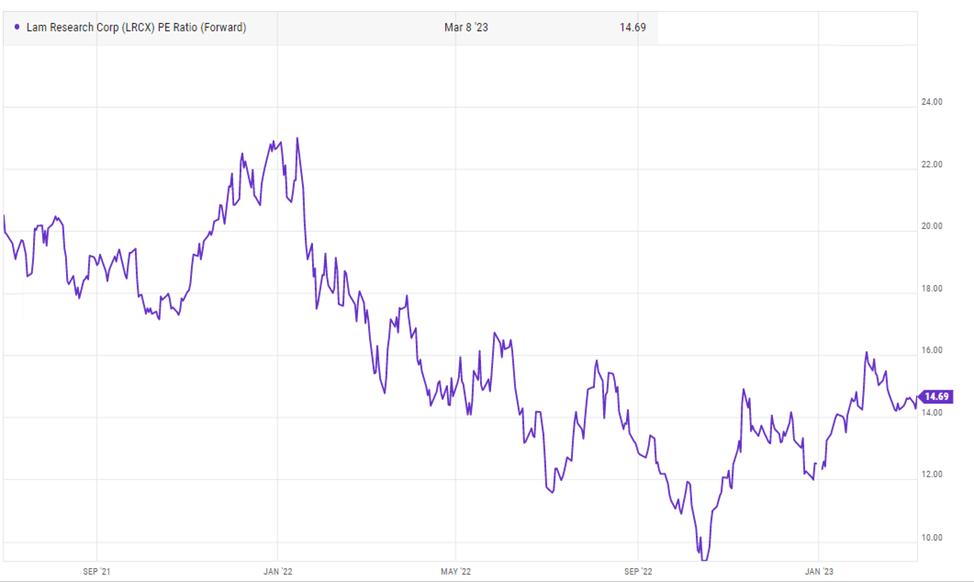

Lam Research Corporation stock is currently trading at 14x forward P/E, significantly below the sector median of 24.2x and at a discount to its own historical multiple. Lam Research has a high level of exposure to the memory sector among large-cap semiconductor companies. This has resulted in a decline in its stock value, as many memory suppliers are indicating significant capital expenditure cuts and new export restrictions for China's memory companies, which are expected to negatively impact the industry. However, I expect the semicap equipment industry to enter a cyclical upturn in the back half of CY24, particularly for memory capex, which would trigger the re-rating of LRCX's stock. Therefore, I keep a Hold rating on Lam Research Corporation and currently do not have a price target on the stock.

{kind=link}

Final Thoughts

Lam Research Corporation is the market share leader in etch and chemical vapor deposition ((CVD)). These two areas have experienced significant growth in the past, making Lam Research a strong contender in the industry. The company has several advantages, including wide competitive moats and a focus on technological advancements such as high-performance computing ((HPC)), artificial intelligence ((AI)), and machine learning ((ML)). Additionally, Lam Research is well-positioned due to the increasing capital intensity of the leading edge and the construction of approximately 50 new fabs.

However, there are some short-term challenges for Lam Research Corporation, including macroeconomic conditions, fluctuations in memory demand, and restrictions on exports to China. I expect a cyclical upturn in the back half of CY24, and maintain a Hold rating for Lam Research Corporation for now.

For further details see:

Lam Research: Waiting For A Better Entry