CCO - Lamar Advertising: Shares Look Appropriately Valued Heading Into Earnings

2023-04-30 05:02:52 ET

Summary

- The management team at Lamar Advertising will be announcing financial results for the first quarter of the company's 2023 fiscal year in a few days.

- Performance for the company has been really solid lately, especially relative to the market, thanks to robust financial performance.

- Absent a major industry downturn, the picture for the company looks fine, but there are likely better opportunities on the market at this time.

I've always found myself drawn to the companies that have the most unique business models. I think it's the novelty concept that really appeals to me. One firm that fits this description is Lamar Advertising ( LAMR ), an owner and operator of billboards, digital displays, and other forms of signage. Recently, attractive financial performance achieved by the company has been instrumental in pushing shares higher. But given broader economic uncertainty, I can understand why some investors might be cautious about the enterprise. The good news is that, in the next few days, we will have a fresh look at how operations are from a fundamental perspective. This is because, before the market opens on May 4th, the management team at the firm will report financial results covering the first quarter of the company's 2023 fiscal year. Leading up to that time, I do think that there is reason to believe that the picture for the company will continue to improve. But with all that's going on in the economy and how shares are currently priced, I have decided to downgrade the business from a 'buy' to a 'hold'.

A look at expectations

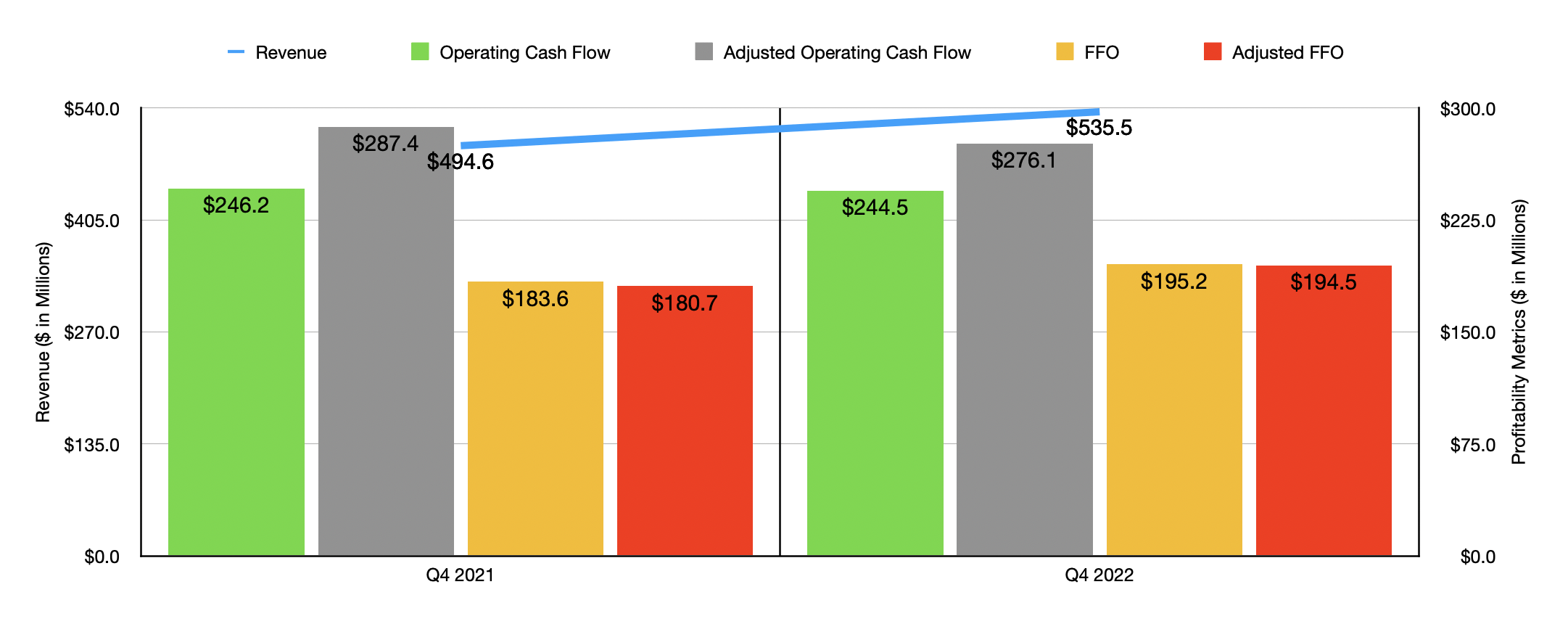

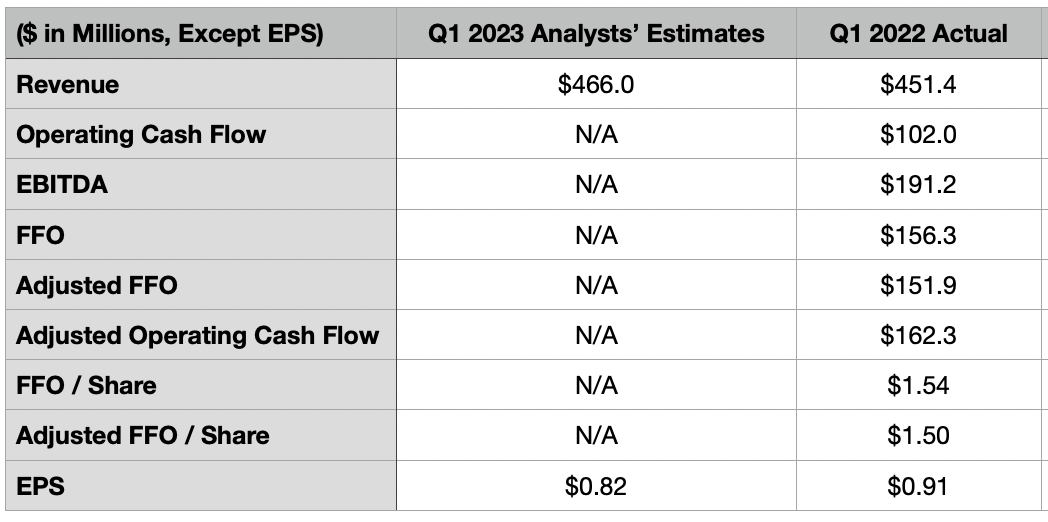

As I mentioned already, before the market opens on May 4th, the management team at Lamar Advertising will announce financial results covering the first quarter of the company's 2023 fiscal year. The current expectation is for the business to report revenue of $466 million. If this comes to fruition, it would translate to a 3.2% increase over the $451.4 million the company reported one year earlier. There would be some precedent for this sales increase. For instance, in the final quarter of the company's 2022 fiscal year, revenue came in at $535.5 million. That was 8.3% above the $494.6 million the company reported one year earlier. Although higher pricing and a change in utilization rate could affect the company's top line, the most likely driver behind this increase will be acquisitions that the company made. During the final quarter of 2022, the company completed 19 acquisitions for a total of $192 million. That brought acquisitions for 2022 as a whole up to 73, for a total purchase price of $480 million that added over 8,200 advertising displays to the company's portfolio.

{kind=link}

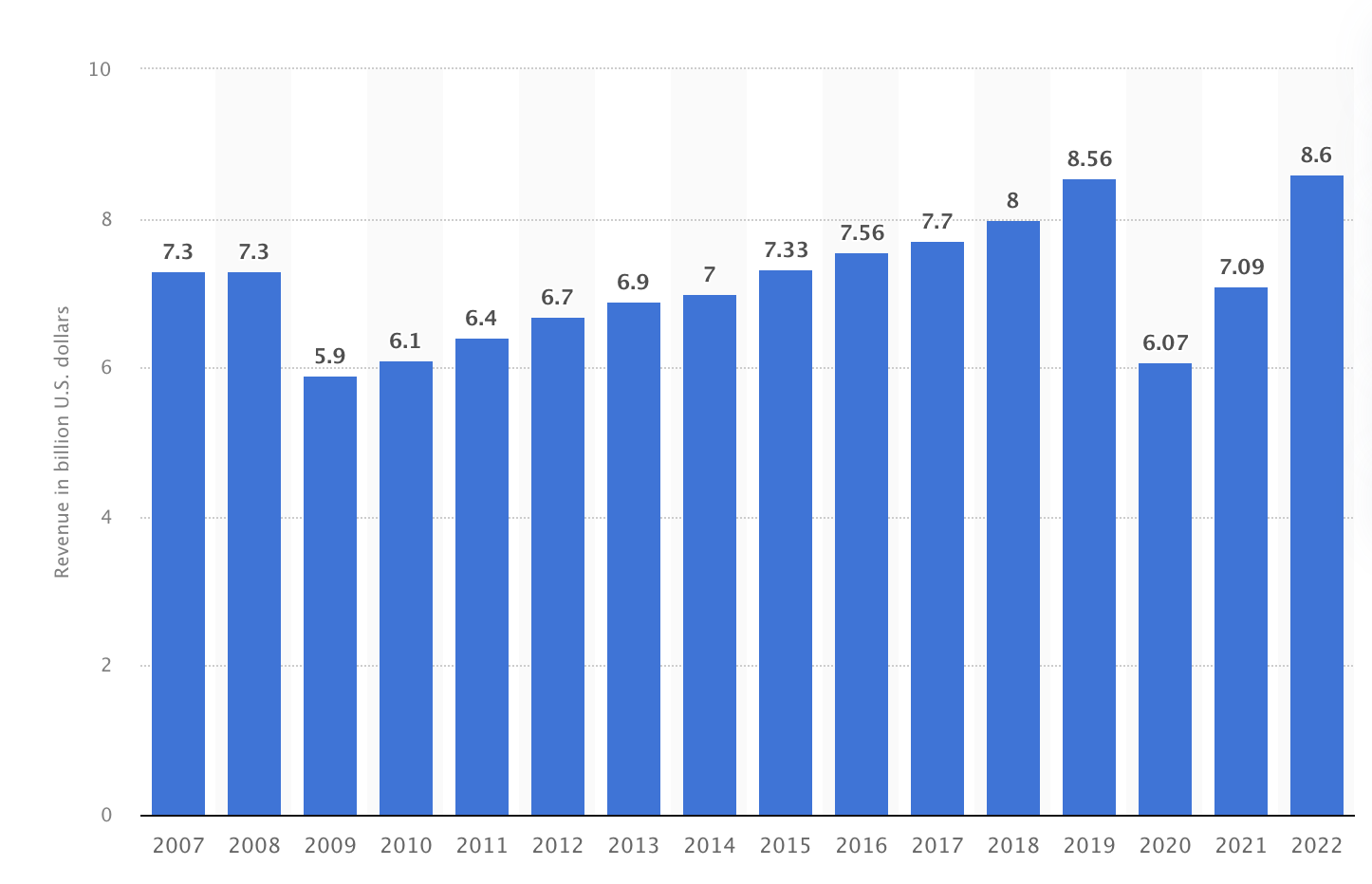

It is very likely that the company will report continued revenue growth. Having said that, it wouldn't be unprecedented for there to be a decline in the event that market conditions worsen. From 2019 to 2020, for instance, total out of home advertising revenue in the US fell from $8.56 billion to $6.07 billion. It was only by 2022 that the industry had fully recovered and then some. Obviously, this would be contingent on a significant economic downturn. Any sort of weakness in the economy would probably be a slower decline than what was seen in 2020 and what was seen during the last financial collapse.

{kind=link}

On the bottom line, the picture is slated to be a bit worse. At present, analysts expect the company to report profits per share of $0.82. That would be down from the $0.91 per share reported for the first quarter of 2022. As a REIT, net income is not all that significant. But analysts have not really provided much in the way of guidance when it comes to other profitability metrics. If net profits do decline, it's likely that other profitability metrics will drop as well. For context, operating cash flow in the first quarter of 2022 was $102 million. If we adjust for changes in working capital, it would have been slightly higher at $162.3 million. FFO, or funds from operations, totaled $156.3 million, while adjusted FFO was $151.9 million. And finally, EBITDA for the company came in at $191.2 million.

{kind=link}

Truth be told, it would be peculiar for the company to report a decline in profitability year over year. Consider how the business performed during the final quarter of its 2022 fiscal year. Although operating cash flow dropped from $246.2 million to $244.5 million, while the adjusted figure for this dropped from $287.4 million to $276.1 million, other profitability metrics performed well compared to the same time one year earlier. EBITDA, for instance, expanded from $230.7 million to $252.3 million. FFO grew from $183.6 million to $195.2 million. And adjusted FFO increased from $180.7 million to $194.5 million.

Shares look decent but not great

{kind=link}

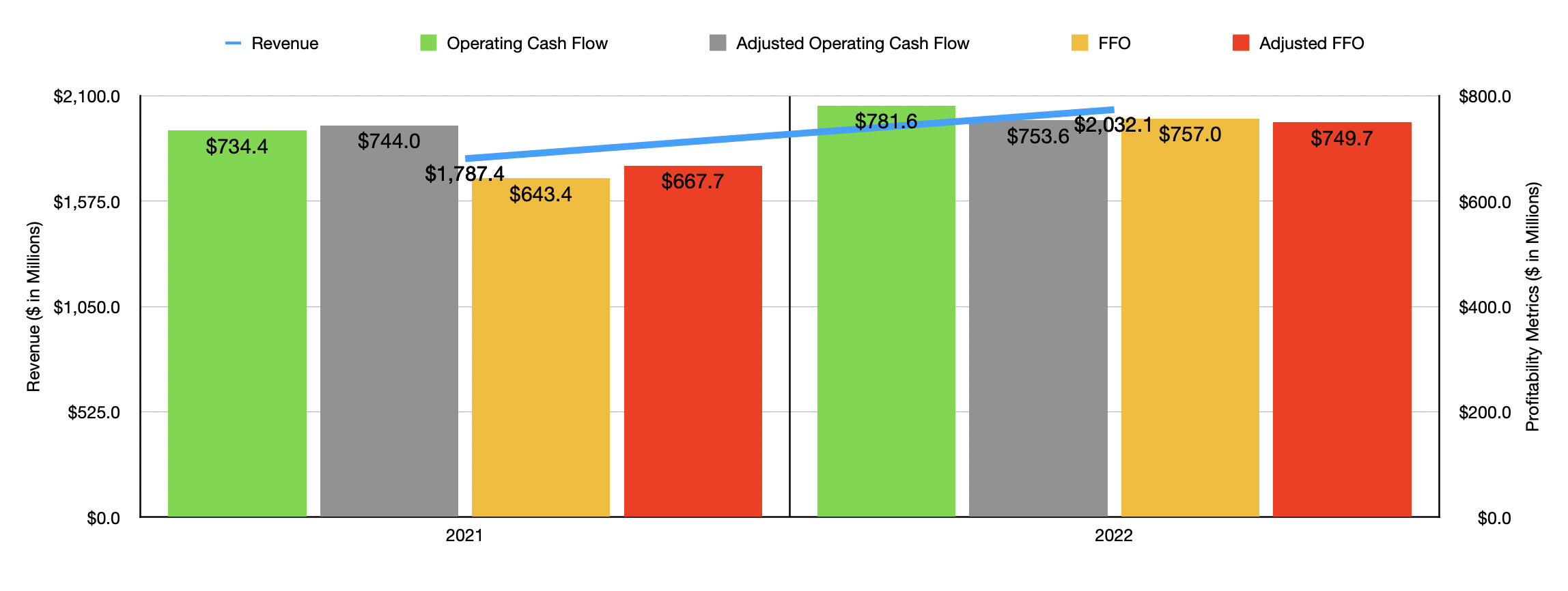

When it comes to the 2023 fiscal year, management expects adjusted FFO per share to be between $7.40 and $7.55. This would imply a reading of between $755.7 million and $771.2 million. By comparison, FFO should be between $770 million and $777.5 million. You can see how these numbers stack up against what the company generated in 2021 and 2022 in the chart above. If we assume that other profitability metrics should rise at a rate that is similar to what adjusted FFO should climb at, then we would anticipate adjusted operating cash flow of $767.5 million and EBITDA of $955.4 million.

{kind=link}

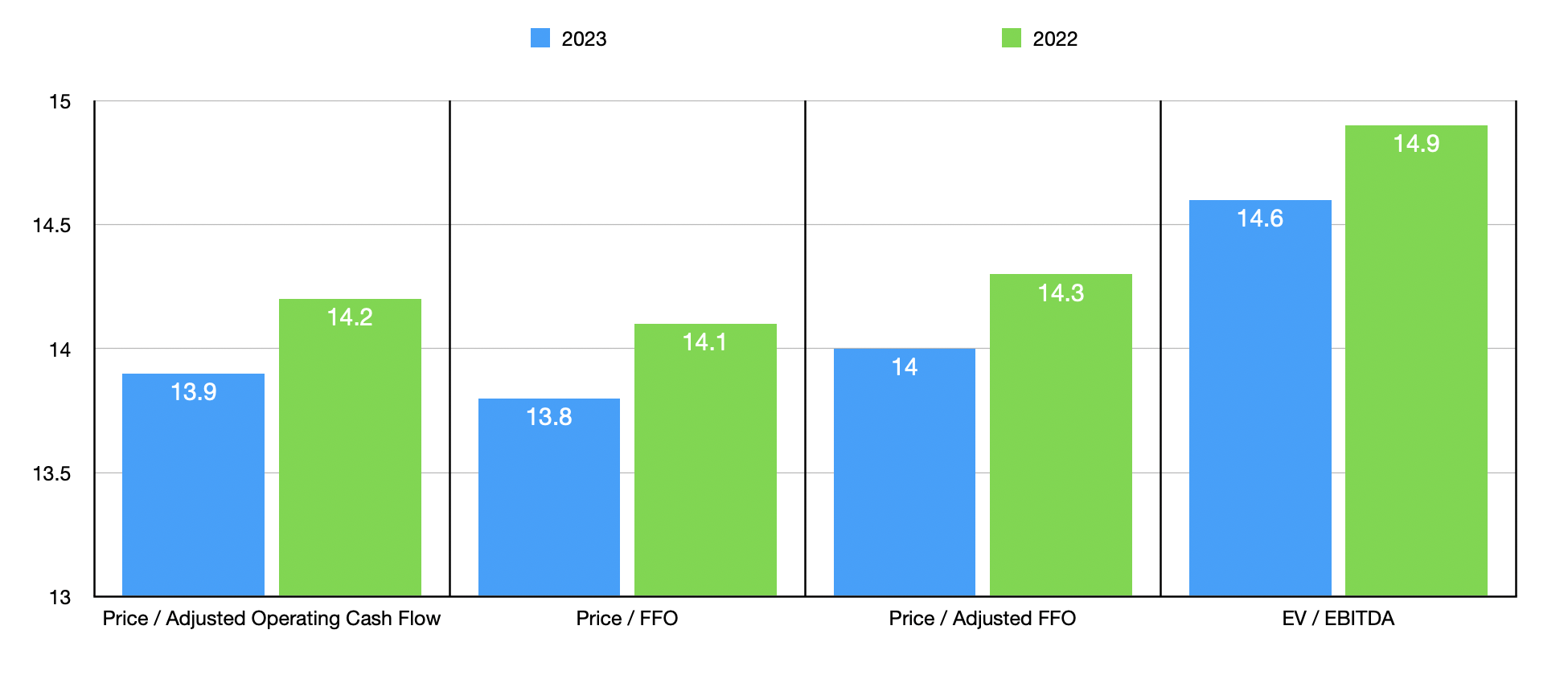

Based on these figures, we can easily value the company. In the chart above, you can see how the company is priced using data from both 2022 and 2023. Given where we are in the fiscal year and the uncertainty that the future holds, my primary focus will be on the data for 2022. But as you can see, the 2023 fiscal year does make the company look a bit more appealing. Taking this data, I then compared the company with two similar firms. These can be seen in the table below. A simple check will confirm that Lamar Advertising is the most expensive of the group from both a price to operating cash flow perspective and from an EV to EBITDA perspective.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Lamar Advertising |

| 14.2 |

| 14.1 |

| Outfront Media ( OUT ) |

| 10.5 |

| 12.4 |

| Clear Channel Outdoor Holdings ( CCO ) |

| 4.4 |

| 11.6 |

Takeaway

Leading into the first quarter earnings release, it's clear that analysts have something of a mixed view for the company. Revenue should climb year over year while profitability will likely drop. On the whole, however, the company is a strong player in its space and, in the long run, it will likely do well for itself. I do think that shares look reasonably priced. But relative to similar firms, they are a bit pricey. When you add on top of this the fact that there is heightened economic uncertainty, I would make the case that there probably are more appealing prospects that can be had right now.

For further details see:

Lamar Advertising: Shares Look Appropriately Valued Heading Into Earnings