OUT - Lamar Advertising: Secular Growth At A Cyclical Multiple

2023-07-18 06:25:03 ET

Summary

- Surviving the pandemic largely unscathed, LAMR has proven its mettle.

- We portend market share capture for OOH which will lead to increase in revenues.

- This trend will play out over the years and create long-term growth.

The Buy Thesis

Lamar Advertising ( LAMR ) operates in a secular growth niche within the otherwise volatile advertising landscape. Barriers to entry combined with shrinking competing substitutes implies long term increased demand for its billboards. We believe LAMR is incorrectly priced at 13X AFFO which is a multiple typical of REITs with either high risk or low growth. As a stable, low debt, large cap we believe LAMR will trade up to a significantly higher multiple as the growth trajectory is revealed.

Specifically, we see fair value at $121 or about 16X current year FFO and there is a dividend catalyst that could help it get there. We shall begin by discussing the out of home (OOH) niche within advertising, and follow with company specific analysis. We will conclude with valuation and assessment of risks.

Out of home advertising as it fits in the overall ad market

Advertising as a whole is quite cyclical. There are multiple ways to break down the overall sector, but there are a few distinctions which are particularly relevant to LAMR’s niche within the market

- National ads versus local ads: different motivations, different payers, and different audiences.

- Untargeted or targeted by either audience or location.

- Pricing is phrased as CPM (cost per 1000 impressions)

National and local ad spending both tend to grow in-line with GDP but LAMR’s opportunity lies in capturing market share in local. Thus, I believe they will have that GDP baseline growth plus CPM growth in local as OOH becomes closer to the only game in town. Allow me to walk through the logic behind the hypothesis.

Targeting in itself is never a negative. Regardless of the product or service being advertised there are certain people it appeals to more than others so a targeted ad has more value per impression than an untargeted ad.

Different ads make sense for different platforms. The clear role for targeted ads is in products that appeal to a very specific population. Consider a drug which treats a rare disease. Advertisements to those with the disease or their families might be quite effective, but at the same time it would be almost useless to advertise that to the general public.

In contrast, when advertising products that have broad appeal, it behooves the advertiser to go for the lower CPM methods. There is little reason to pay 10X as much to target specific people when your target market is everyone.

Due to this natural divide in when targeting makes sense there is always going to be a split of ad dollars between those that should be targeted by audience and those that should not.

I posit that the targeted ad market is getting crowded from a platform standpoint. Social media companies are tripping over themselves to collect as much user data as possible on their users such that they can sell that data to advertisers to make targeting ever more precise.

Meta Platforms’ ( META ) new app “Threads” is likely to not even be directly monetized with its main source of revenues being collecting easily scrapable text data from conversations such that they can provide better targeting on Instagram and Facebook and raise the CPMs they charge.

It might work well for them, but there are so many companies trying to go this same high data collection route for high CPM audience targeted ads.

I believe there is going to be a surplus of digital advertising platforms going after the subsection of advertisers that want to target specific audiences and as a result CPMs are likely to come down in that space.

Targeted ads are better, but there is a limit to how much better it is and right now the ratios of cost are rather stretched.

{kind=link}

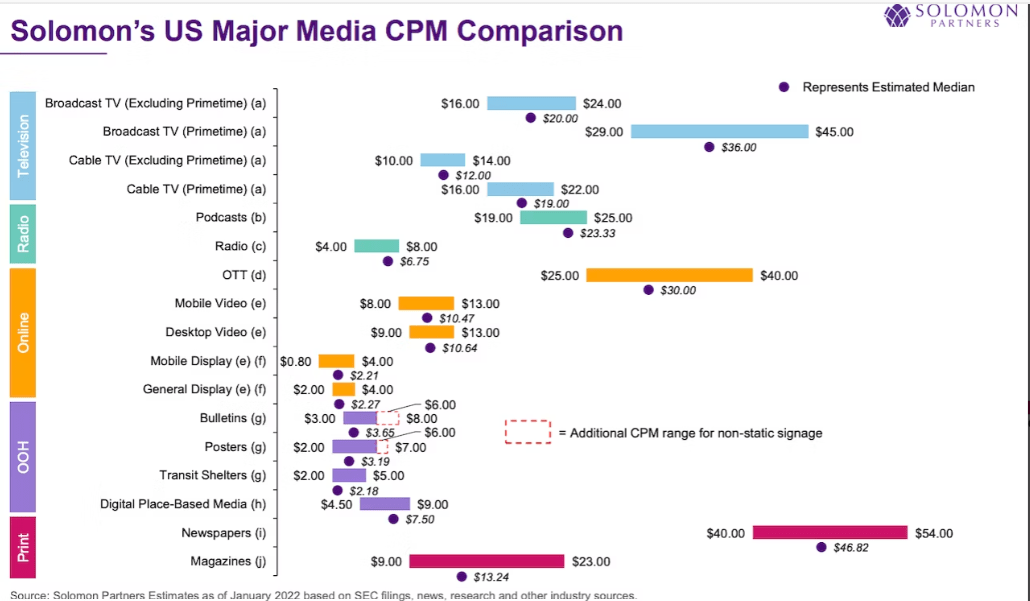

OTT (streaming) advertising costs $30 per thousand impressions. Podcasts also tend to have specific audiences for targeting and they cost about $23 CPM. In contrast, one of most untargeted forms of advertising is a banner ad on a broadly used website. These are low value impressions, but they do come cheap at about $2.00 CPM.

So advertisers can choose to target audiences for an expensive rate or go untargeted and get more impressions for cheaper.

A third option is to target by location rather than audience. This is where broadcast TV and newspapers come in as these platforms alter their ads by location. On these platforms, targeting by location is just as expensive as targeting a certain audience. Newspapers have $46 CPM while linear TV sits at $36.

Out of home advertising, such as billboards, is the far cheaper option and just as effective at targeting locally. It provides impressions in a specific location at about $3 CPM.

Consider a McDonald's ( MCD ) billboard on a highway 2 miles before an exit with a McDonald's. Every single person driving by is potentially hungry and due to the specificity of location every single impression is on a person within the catchment radius of the McDonald's.

So that is the niche in which billboards are the most effective form of advertising - broad audience with a specific location.

As of right now, they compete in that niche with linear TV, physical newspapers, and radio. We have all heard of the wave of cord cutting. Linear TV is rapidly losing viewers. Radio is not faring as poorly as TV but it is losing much of its listeners to Spotify and podcasts. Newspaper subscriptions are rapidly moving to digital rather than physical print.

Growth drivers for Lamar

As the substitutes for OOH shrink it could lead to a significant increase in market share for OOH in location specific advertising. Over time, this will increase occupancy and CPM for Lamar’s assets. Additionally, the billboards themselves are becoming more effective as they move to LED displays. This increases NOI in 2 key ways:

- Lower capex. The LED ad can be changed easily.

- Time specific targeting

Beyond location specificity, LED displays allow advertisers to target ads for specific times.

At 7:00 A.M. the billboard displays an Egg Mcmuffin with hashbrowns and coffee. At 11:00 it switches to a Big Mac and Coke.

LED ads even allow for split billboard use. Perhaps that sign advertises MCD products during the lunch hour but in the evening switches to concert tickets for a local stadium.

There are ways to extract significantly more rental dollars out of each billboard.

The moat

With most forms of real estate, when revenues per square foot rise, it incentivizes construction. For example, there was a wave of apartment construction commencing in 2022 as rental rates went up 15%.

Billboards are a bit trickier than that. While the physical cost of construction is quite low, it is very difficult to get new billboards through all the red tape. Existing billboards are grandfathered in and allowed to keep operating, but new ones are challenging.

With supply constrained, growth in revenues is likely to accrue to incumbent billboards and LAMR is the market share leader in the space.

Valuation

The median REIT trades at 14.5X 2023 estimated AFFO. Within that there is a dispersion of multiples in which the higher quality and faster growing should trade at the higher end of the earnings multiple bell curve. In an efficient market they would, but the market is drastically mispriced right now. There are some junky REITs trading at the high end of the multiple range and some really high quality trading at the discounted end.

Lamar is among that badly mispriced group as it is high quality, reasonably low risk, and has secular growth yet it trades below the index multiple. It should trade at a premium and I intend to demonstrate these quality attributes below.

Consistent and reliable

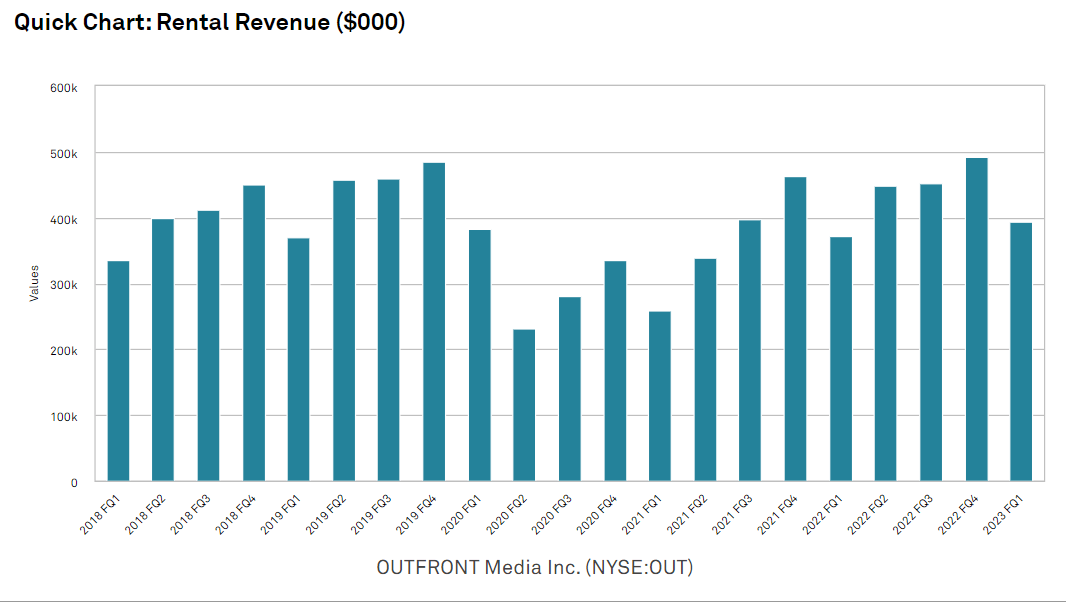

The REIT market seems to be a bit afraid of the advertising REIT subsector. I think this fear is driven by what happened to Outfront Media ( OUT ) during the pandemic.

{kind=link}

While it is true that the reduced road traffic hurt billboards nationally, the impact was amplified on OUT for 2 reasons:

- High leverage

- NYMTA contract

OUT has a huge contract with the New York Metro Transit Authority (NYMTA) to put various forms of advertising throughout the city’s transportation system.

Public transportation traffic plummeted during the pandemic to a significantly greater degree than personal car usage which tends to be the driver for billboards. As such, OUT’s revenues got clobbered while its costs remained. This earnings volatility resulted in people fleeing the sector.

Lamar is a much bigger company with much lower leverage so it is inherently less volatile. It also focuses less on metro transit and more on its own billboards and signage. As advertising spending is cyclical, the pandemic and related recession did still impact LAMR, but to a much lesser extent.

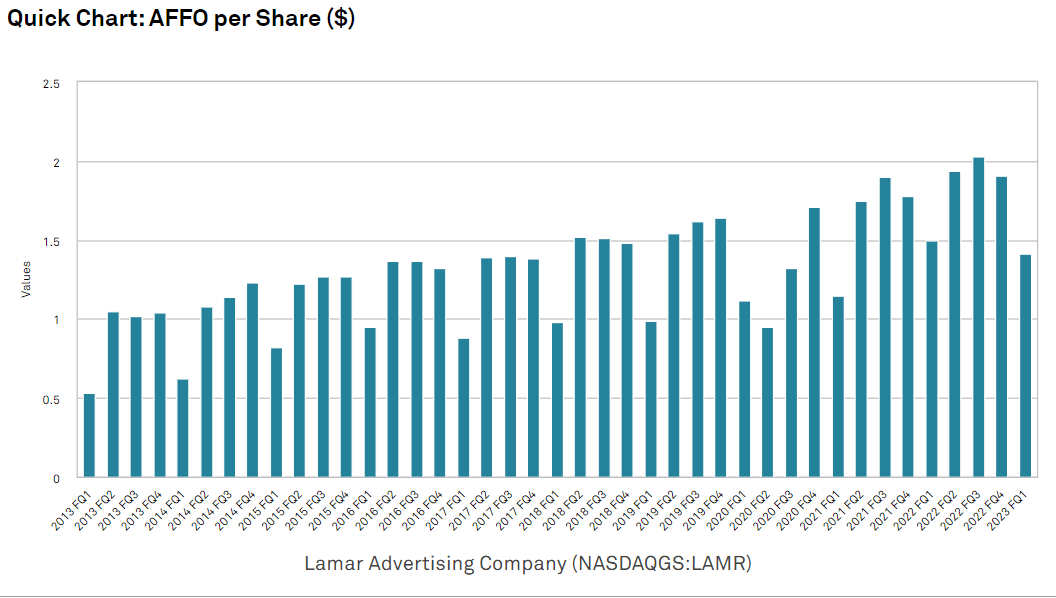

AFFO/share briefly dipped slightly and then rebounded to well above pre-pandemic levels.

{kind=link}

That is a steady uptrend from about a buck a quarter in 2013 to about $2 a quarter in 2022. There is some seasonality with 1Q consistently coming in weak which I suspect is just due to people driving less in the winter.

I really like battle tested companies and the pandemic was a fantastic test for billboards. Not only was it a recession, but it was one in which people specifically did not leave their homes so out of home as a category was hit to an unusual extent.

If the above impact to AFFO is all that LAMR felt, that is a very reliable company. No company is immune to macro factors, but the strong ones bounce back quickly which Lamar did. It has been around for over a hundred years, is the market share leader and has a solid balance sheet with fairly low debt.

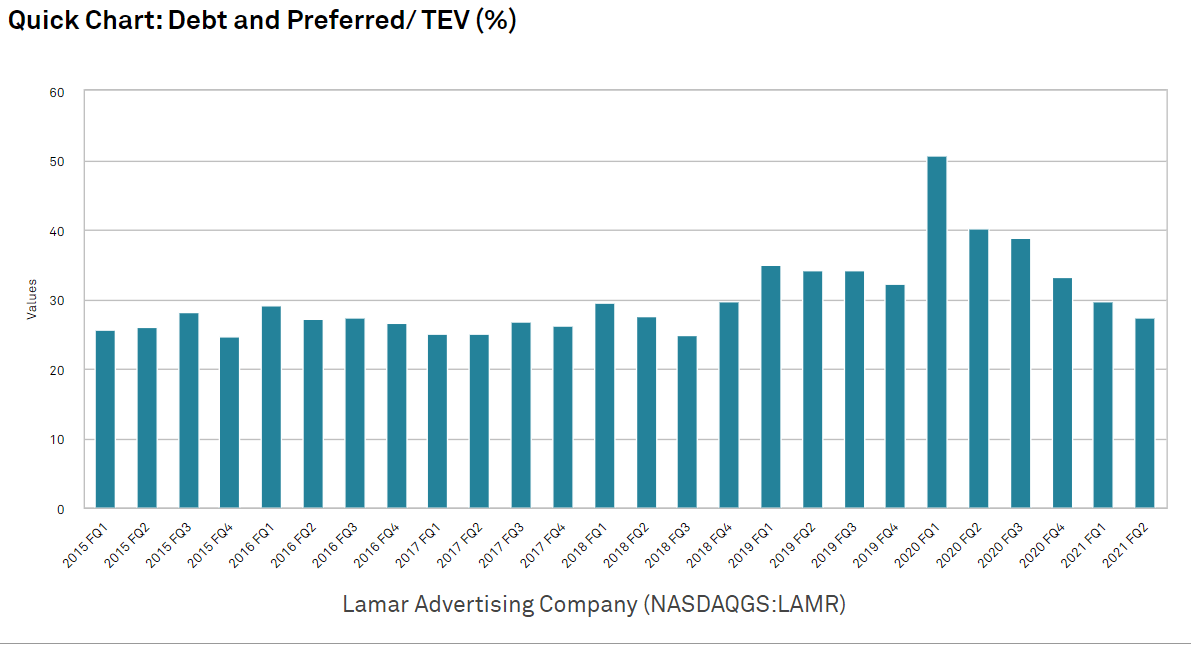

{kind=link}

Debt to total enterprise value in the 20s is quite low for a REIT with most closer to 40%.

Growth has been consistent over time and analyst consensus calls for continued growth going forward.

{kind=link}

That is a good pace and I think it could come in faster if I am right about OOH taking market share from TV and radio.

Given this combination of reliability and growth I think Lamar should trade at a premium to the index. This implies an AFFO multiple of at least 16X which would be just over 20% upside from today’s price.

Catalyst to help the stock get there

I believe REITs should be viewed as total return investments, but the REIT market tends to overly focus on dividends. As such, Lamar’s market price has been held back by its low AFFO payout ratio. Its dividend yield is only 5% even though its cash flow yield is much higher.

In the next few years, however, the company is likely to be forced to raise its dividend substantially. As you know REIT tax laws require the REIT to pay out 90% of taxable income as dividends.

LAMR has been able to keep its dividend low through use of NOL carryforwards. Through using these, they are paying out a much smaller percentage of their income. Well, the NOL carryforwards are being depleted and absent large transactions will run out in the next couple years.

When they run out, tax law will force LAMR to raise its dividend up to that 90% payout threshold which would be a significant raise.

Lamar’s dividend is already above pre-pandemic levels, but the spike upon NOL depletion could really entice the market.

Risks to thesis

Even though I am bullish on Lamar stock I do like to give equal consideration to what could go wrong. In my opinion, the biggest risks would be anything that reduces the number of people driving by billboards.

- Permanent work from home

- Oil prices going to $120

- ICE vehicles getting banned?

It is hard to foresee all the possible scenarios. The above just represent the categorical types of things that would hurt OOH to varying degrees.

Overall, I think LAMR presents excellent total return potential relative to its risk.

For further details see:

Lamar Advertising: Secular Growth At A Cyclical Multiple