KHC - Lamb Weston: Good Growth Prospects

2023-03-22 14:49:09 ET

Summary

- Net sales should benefit from price increases, good demand, capacity expansion, and an increase in global footprint.

- Margins should benefit from price increases and productivity savings.

- Valuation is lower than the historical average.

Investment Thesis

Lamb-Weston Holding, Inc ( LW ) is expected to benefit from price increases and strong demand for french fries in quick-service restaurants (QSRs) and retail channels, as they are a low-cost substitute for dining in an inflationary environment. Additionally, the company's revenue growth should be aided by capacity expansion and an increasing global footprint following its acquisition of Lamb-Weston/Meijer in Europe. The company’s margin is expected to benefit from price increases in the coming year. Over the medium to longer term, margins should also benefit from the easing supply chain constraints. Furthermore, the stock is currently trading below its historical average valuation, which combined with good growth prospects, makes it a good buy.

Revenue Analysis and Outlook

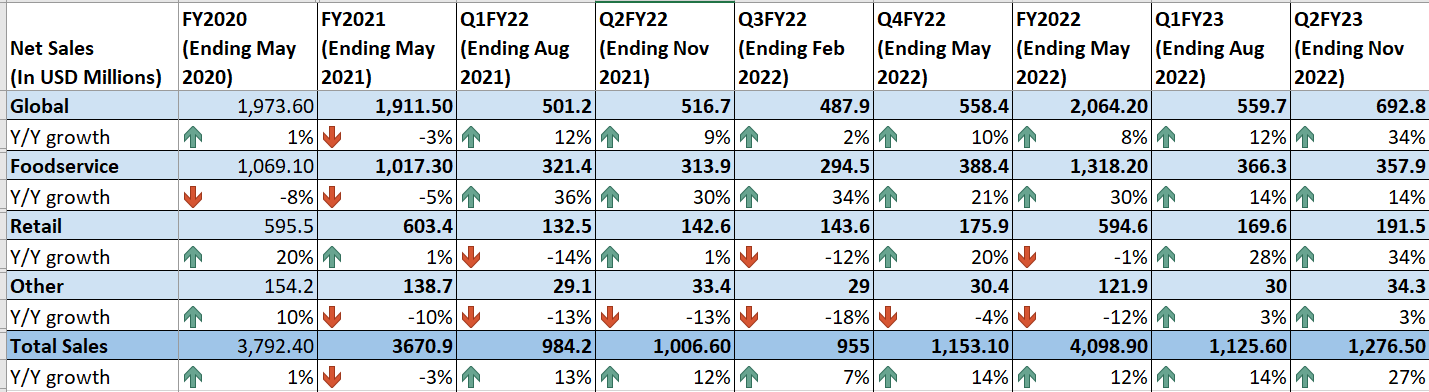

After getting impacted by COVID in FY20 and FY21, Lamb Weston's sales have seen good growth in FY22 and year-to-date in FY23 thanks to the increase in consumer demand due to easing travel restrictions and price increases.

In the second quarter of FY23, sales growth has continued to benefit from price increases and strong demand in quick-service restaurants (QSRs) and retail channels. However, it was partially offset by volume decline resulting from lower production (caused by labour and commodity shortages) and a slowdown in demand from full-service restaurants. Overall, net sales increased by 27% YoY to $1.28 billion, with a 30% benefit from price/mix impact and a 3% decline in volume.

{kind=link}

LW’s Historical Net Sales (Company Data: GS Analytics Research)

Looking ahead, I believe that Lamb Weston is well-positioned to grow its sales, with benefits from pricing increases, strong demand at quick-service restaurants (QSRs) and retail channels, capacity expansion, and an increase in global footprint.

Like many companies in the industry, LW has increased prices for its products to cover inflationary costs. These price increases have significantly benefited the company's sales growth over the last year, and the company expects to continue driving pricing actions across its portfolio to support sales growth moving forward.

In addition to price increases, LW's end-market demand remains healthy. In an inflationary environment, consumers tend to look for less expensive dining options or opt for quick takeaways, which has led to increased foot traffic at QSRs and strong demand for LW's frozen potato products. Additionally, the retail channel is also experiencing good demand as consumers with tight budgets look for at-home and ready-to-eat options, driving demand for frozen french fries at retail channels.

While there has been a slowdown in demand at full-service restaurants, I believe that the demand at QSRs and retail channels should offset this slowdown. Overall restaurant foot traffic is up YoY, and the food industry generally stays somewhat resilient in a recessionary environment, so I expect the end-market demand to remain healthy over the coming years and drive LW's sales growth.

Furthermore, in late February, the company completed its acquisition of a 100% stake in the Lamb-Weston/Meijer (LWM) joint venture in Europe. Previously, LW had a 50% stake in LWM joint venture. This transaction opens up many doors for growth opportunities for the company in the medium to longer term. LWM is one of the leading suppliers of frozen potato products in Europe, the Middle East, and Africa, and this acquisition should help LW to expand its global footprint in the EMEA region and capture the benefits of growing global demand for french fries without the operating restrictions associated with the joint venture.

Moreover, Lamb-Weston/Meijer had annual sales of ~$840 million in the last fiscal year and adds meaningfully to the company’s inorganic growth. This acquisition should also help the company in the medium to long term through good revenue synergies.

The company has seen some headwinds due to lower production rates as a result of supply constraints. However, it is actively working to increase its production capacity to meet the demands of the end market. To this end, LW is investing in new french fry facilities in China (anticipated completion mid-FY24), Idaho (anticipated completion mid-FY24), and Argentina (anticipated completion mid-calendar year 2024). Additionally, the acquisition of Lamb-Weston/Meijer should also help LW expand its manufacturing capacity. Lamb Weston/Meijer has six processing facilities, and together, the companies estimate a total production capacity of around 8 billion pounds (up from LW’s current 6 billion pounds) across 25 processing facilities. These capacity expansions should help drive the company's volume and sales growth beyond fiscal 2023.

I am optimistic about the company’s sales growth prospects and management has guided for 17% to 19.5% sales growth for fiscal year 2023. I believe is achievable given price increases and strength in QSR and retail categories.

Margin Analysis and Outlook

Over the last couple of years, Lamb Weston’s gross margin was negatively impacted by high raw material costs and logistic costs. However, over the last few quarters the company was able to sequentially improve its gross margins thanks to continuous price increases.

In the second quarter of fiscal 2023, although inflationary costs remained elevated year-over-year, the gross margin continued to benefit from the company’s pricing actions. Additionally, a favorable customer and product mix and productivity savings contributed to gross margin expansion. As a result, the company saw a 950 basis points year-over-year increase in gross margin to 29.9%.

LW’s Historical Gross Margin (Company Data: GS Analytics Research)

Looking ahead, Lamb Weston still faces near-term headwinds from higher potato prices, shortages of key ingredients and spare parts, and onboarding newly hired production workers. However, the company should be able to offset these challenges through its pricing actions. In the first half of fiscal 2023, LW accelerated many multi-year global customer contract renewals and successfully renegotiated them to accelerate pricing actions. During the second quarter earnings call, management indicated that they have only 25% of these contracts left for renegotiation, with renegotiations going on at a faster pace than typically anticipated. This should help margin growth, as the company expects the benefit of renegotiated pricing to reflect in margins during the second half of fiscal 2023, and it continues to renegotiate remaining contracts.

Furthermore, the company's efforts to expand its capacity to reduce supply chain challenges should help it expand margins in the medium to long term. With the Lamb-Weston/Meijer acquisition, the company has gained access to a global supply chain and can strengthen its global manufacturing footprint by leveraging Europe's infrastructure to serve key international markets. This should increase efficiency, improve productivity, reduce costs, and help in margin expansion.

Valuation and Conclusion

Lamb Weston is currently trading at a forward P/E multiple of 25.76x and 21.78x based on FY23 and FY24 consensus EPS estimates of $3.87 and $4.57, respectively. The stock is trading below its historical 5-year average forward P/E of 27.69x. With good growth prospects for the next few years, including price increases, resilient demand for the french fries category, capacity expansion, and an increasing global footprint, the company is well-positioned for growth. Although the stock is trading at a premium to its peers, Lamb Weston is also expected to have better EPS growth, thanks to good revenue and margin growth prospects.

| Peers |

| FY23 P/E |

| FY24 P/E |

| FY23 EPS growth |

| FY24 EPS growth |

| The Kraft Heinz Company ( KHC ) |

| 13.94x |

| 13.21x |

| -1.85% |

| 5.57% |

| Conagra Brands, Inc ( CAG ) |

| 13.62x |

| 12.95x |

| 13.29% |

| 5.22% |

| General Mills, Inc ( GIS ) |

| 19.29x |

| 18.34x |

| 6.25% |

| 5.17% |

| Kellogg company ( K ) |

| 16.04x |

| 15.20x |

| -3.50% |

| 5.53% |

| Campbell Soup Company ( CPB ) |

| 17.96x |

| 17.16x |

| 5.68% |

| 4.65% |

| Lamb Weston Holdings Inc ( LW ) |

| 25.76x |

| 21.78x |

| 85.99% |

| 18.25% |

The company operates in an oligopolistic industry which has so far exhibited rational pricing by all players. Further, I like the long-term global growth potential of the french fries category. Due to these characteristics, the stock has typically traded in the mid-20s P/E range. Given LW stock is trading at a meaningful discount to its historical valuation range on consensus EPS estimates for FY24 (ending May), I believe it offers a good opportunity.

For further details see:

Lamb Weston: Good Growth Prospects