SMPL - Lancaster Colony Corporation: Near The Tipping Point

2023-03-21 11:40:31 ET

Summary

- Lancaster Colony Corporation has had a great run, with sales, profits, and cash flows all rising higher and pushing the stock up.

- While it's great to see quality performance rewarded, it's unclear how long market conditions will prove bullish for the firm.

- And irrespective of market data, shares are looking quite pricey at this point in time, perhaps pushing the company to the point where it deserves a downgrade.

While academics often like to paint the picture of an efficient market, my experience has been that the market can be rather inefficient. I don't mean this just from time to time. I mean quite often. For instance, in some cases, companies that look rather pricey sometimes continue to appreciate, even when some fundamental data shows a weakening in the bullish case. One great example of this, in my opinion, involves Lancaster Colony Corporation ( LANC ), a producer and seller of food products like frozen breads, refrigerated dressings, dips, croutons, and more. Sales, profits, and cash flows for the business have been on the rise over the past year or so. This, combined with a robust balance sheet, has been instrumental in pushing the stock up over the past few months. However, there are some signs of weakness ahead. And this weakness could ultimately prove to come back to bite those who are long the stock. Though for full transparency, I don't think the pain the company should experience will occur just yet. Rather, I suspect that it will develop as the year progresses.

Robust results… sort of

Back in October of last year, I decided to analyze Lancaster Colony again. Leading up to that point, the company had demonstrated consistently growing revenue, but its bottom line figures had come in rather mixed. In the long run, I felt as though the firm would be just fine. But because of how pricey shares were, I could not rate the business anything more than a ‘hold’. Since then, the company has defied expectations, with shares soaring 18.9% at a time when the S&P 500 has appreciated 4.5%.

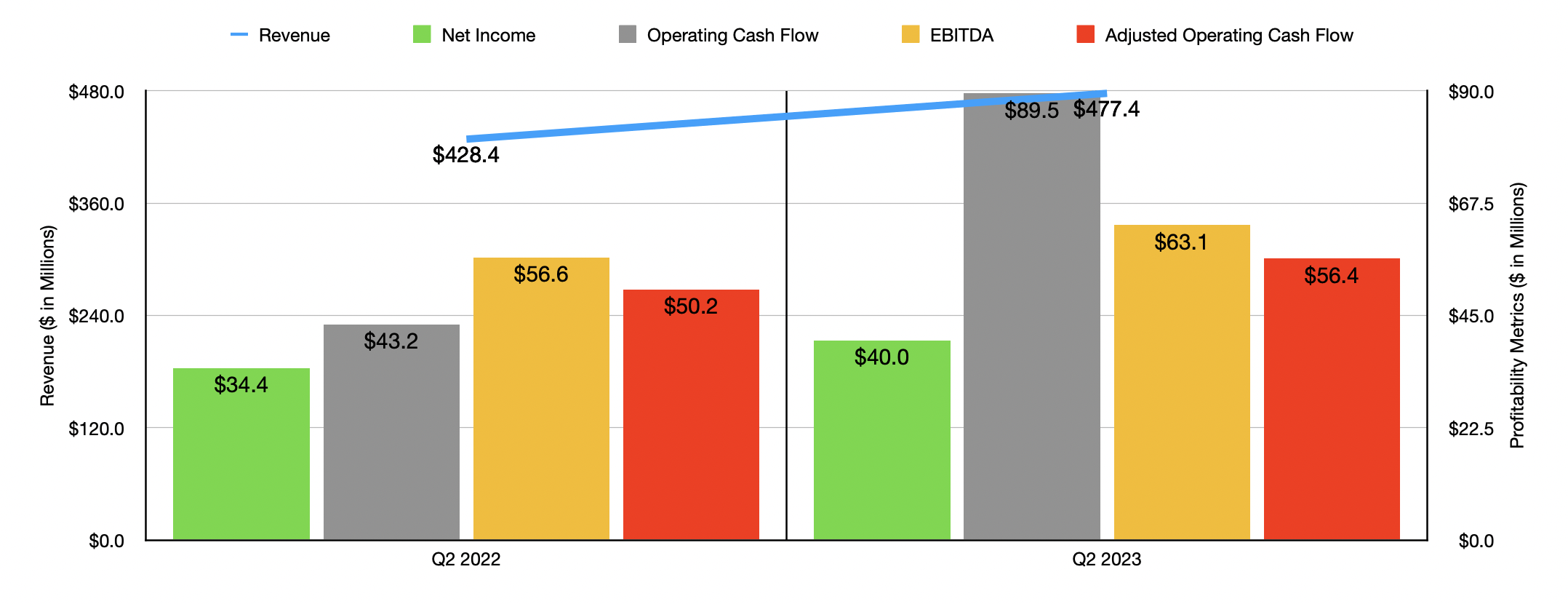

In my opinion, a lot of this upside can be chalked up to the data provided by management covering the second quarter of the company's 2023 fiscal year that was reported in February of this year. For that quarter, sales of the company came in at $477.4 million. That's an impressive 11.4% higher than the $428.4 million reported the same time one year earlier. Bottom line results for the company also came in strong. Net income, for instance, rose from $34.4 million to $40 million. Operating cash flow more than doubled from $43.2 million to $89.5 million. Though if we adjust for changes in working capital, it would have risen more modestly from $50.2 million to $56.4 million. Meanwhile, EBITDA for the firm expanded from $56.6 million to $63.1 million.

{kind=link}

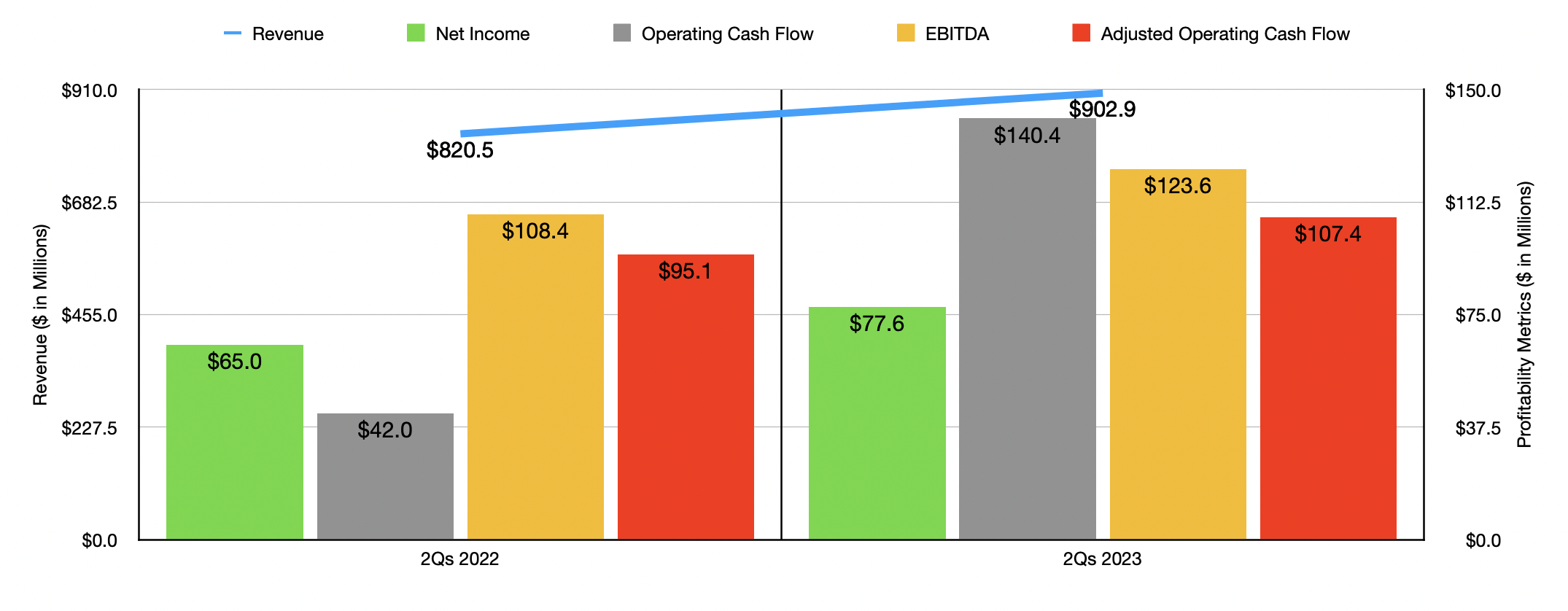

All of these results can be seen in the chart above. Meanwhile, in the chart below, you can see how the company has performed for the first two quarters of the 2023 fiscal year as a whole. Revenue of $902.9 million was 10% higher than the $820.5 million reported the same time one year earlier. Profitability metrics also improved at a rate that was similar to what was seen for the second quarter of the year on its own. In fact, every profitability metric was up year over year, indicating that the picture for the business looks solid.

{kind=link}

Looking only at this surface-level data, we get a rather bullish impression of the company and its prospects. But when you look under the hood, you start to see some issues. These issues are pretty much the same in both the most recent quarter, as well as in the first half of the year as a whole. So for the sake of being comprehensive, we will focus on the first half of the year. During this time, revenue for the business was driven higher not because of increased demand, but because of increased pricing. This pricing occurred across both of the company's operating segments. For instance, under the Retail segment, overall revenue rose by about 3%. This increase was driven entirely by higher prices charged to customers and occurred even in spite of an $11 million timing issue with certain sales. But because of the higher prices, overall sales volumes as measured in pounds shipped, plunged 9% year over year. That compares to the 7% increase experienced the same time of the 2022 fiscal year. When it comes to the Foodservice segment, sales spiked roughly 20%, in spite of the fact that sales volumes dropped 6%. For context, the same time one year earlier, the company saw sales volumes rise 5% year over year.

What this suggests to me is that the business is experiencing issues because it has transferred more than its inflationary pressures onto its customers. This is obvious when you look at the net profit margin of the business which, in the first half of 2022, totaled 7.92%. That compares to the 8.59% reported one year earlier. This is actually a common theme that I have seen in many food-oriented firms that I've looked at recently. But at some point, the negative associated with decreased volumes will more than offset the benefit of higher pricing.

Of course, this could take some time to fully play out. According to the USDA , for instance, all food prices in 2023 are expected to climb by about 7.9%, with a lower range of 5.5% and a higher range of 10.3%. Food at home prices will be the most severe, climbing 8.6% compared to the 8.3% anticipated for food away from home prices. By comparison, in 2020 and 2021, food prices grew a much more modest 3.5% per annum. Then, in 2022, a combination of factors such as higher energy prices, supply chain issues, and a highly pathogenic variant of the avian flu, sent food prices spiking 9.9%. But with recent economic turmoil creating uncertainty and a real possibility of a recession if things get out of hand, and with companies already seeing volumes of product sold decreased, I suspect that is only a matter of time before a firm like Lancaster Colony is forced to adjust accordingly.

{kind=link}

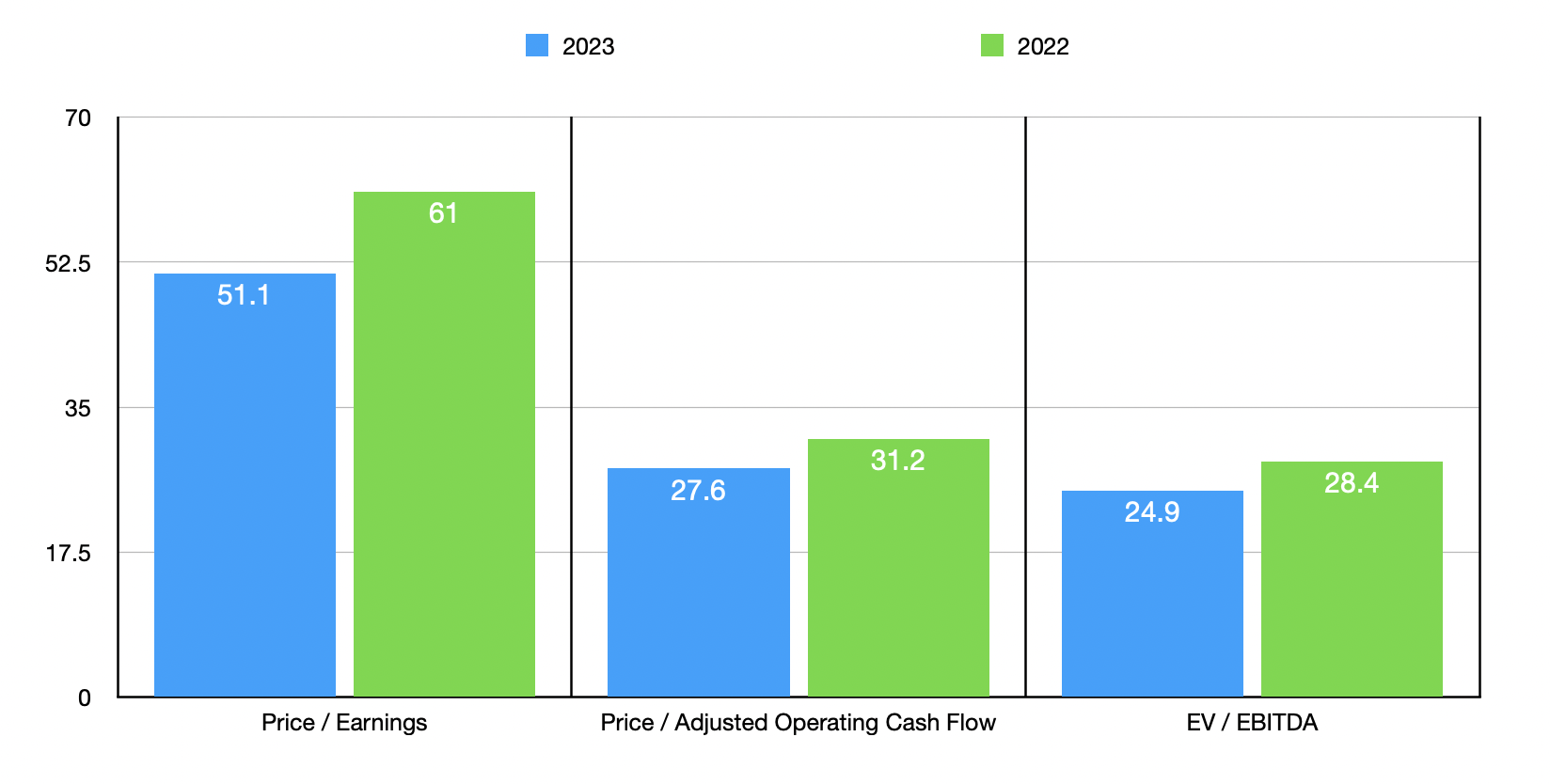

From an investment perspective, situations like this don't normally bother me. I will often buy into a company that I know is going to experience some difficult times ahead. However, I don't do that when shares of the business already look expensive. By my estimate, Lancaster Colony is trading at a forward price-to-earnings multiple of 51.1. The forward price to adjusted operating cash flow multiple is 27.6, while the forward EV to EBITDA multiple should be 24.9. If you think these are high, consider the data using the 2022 fiscal year, which is also shown in the chart above. Not only are shares of the business expensive on an absolute basis, they are also pricey relative to similar firms. As you can see in the table below, using the price-to-earnings multiple, and using the EV to EBITDA multiple, Lancaster Colony is more expensive than the five food businesses I compared it to. Using the price to operating cash flow approach, only one of the firms was more expensive. It is true that the company benefits from having no debt and enjoying cash and cash equivalents of $95.5 million. But even that excellent balance sheet condition does not justify such a lofty price when the future is likely to deteriorate to some degree.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Lancaster Colony Corporation |

| 51.1 |

| 27.6 |

| 24.9 |

| Flowers Foods ( FLO ) |

| 24.9 |

| 15.8 |

| 14.0 |

| Hostess Brands ( TWNK ) |

| 20.6 |

| 13.6 |

| 13.6 |

| The Simply Good Foods Company ( SMPL ) |

| 30.2 |

| 29.5 |

| 19.4 |

| Cal-Maine Foods ( CALM ) |

| 5.6 |

| 5.4 |

| 3.3 |

| The Kraft Heinz Company ( KHC ) |

| 19.7 |

| 18.8 |

| 13.7 |

Takeaway

Based on the data provided, I must say that Lancaster Colony is an interesting business. But it's not one that I have an interest in owning shares of today. I think the company is incredibly healthy and it's likely that, in the long run, it will continue to grow. It surely is benefiting from current market conditions, and investors should be happy about that. But there's also a dark side to this recent performance. Add on top of that just how pricey shares are, and I cannot personally touch the business now. In fact, if LANC stock gets any more expensive, I will likely downgrade it. But as things stand, I still believe that a ‘hold’ rating is appropriate at this time.

For further details see:

Lancaster Colony Corporation: Near The Tipping Point