LANC - Lancaster Colony: Licenced Brands Create Room For Growth

2023-11-29 06:55:12 ET

Summary

- Lancaster produces and sells food products through the retail and foodservice sales channels.

- The Company is leveraging partnerships with foodservice brands to drive growth in the retail segment with licenced brands, providing Lancaster with an intriguing growth alley.

- The stock seems to be priced for modest growth in the future along with recovering margins, which is in line with my financial expectations.

Lancaster Colony Corporation ( LANC ) produces and sells food products. The company divides its sales into retail and foodservice sales channels, both of which contribute almost equally to revenues. The retail sales are further divided into segments - Shelf-Stable Dressings, Sauces & Croutons with 44% of retail revenues, Frozen Breads with 35% of retail revenues, and Refrigerated Dressings, Dips & Other with 21%. The foodservice sales channel on the other hand focuses mainly on servicing fast-food restaurants.

Lancaster's stock has appreciated by around 94% in the past ten years, making the stock's CAGR 6.9% through appreciation alone. In addition, Lancaster pays out a dividend with a current yield of 2.20% . Impressively, the company has a history of increasing dividends for 59 years in a row, making Lancaster a dividend king.

{kind=link}

Growth in Licenced Brands' Sales

Of the two main revenue channels, the retail segment seems to have more ambition for growth. Lancaster has found a useful strategy of leveraging partnerships with foodservice brands such as Chick-fil-A, Arby's, Buffalo Wild Wings, and Olive Garden - Lancaster sells sauces and flavorings with the brands' names through a licencing agreement, giving the products a sizable edge in terms of branding on retail shelves. In my opinion, the licencing benefits both Lancaster and the fast food chain well - Lancaster has great knowledge in producing sauces and flavorings making Lancaster a great partner, and the brand name on store shelves makes the brand name more prominent, also helping Lancaster through creating a growing sales channel for the business.

Lancaster's management seems to push the licencing growth as a significant opportunity - estimated trailing retail sales for Lancaster's licenced products' sales is $418 million, compared to an addressable market estimated at $13 billion. As many of the licenced products have hit the shelves in the spring of 2023, I believe that the sales should continue to grow significantly for Lancaster - customers' spending habits tend to take time to form with new products. The company is expanding its production capacity to make more room for growth.

Financials

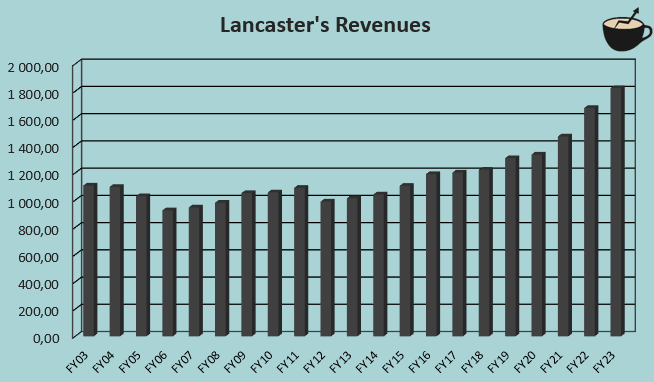

The licenced brand retail sales along with a high level of inflation have contributed well to Lancaster's growth in recent years. From FY2003 to FY2023, Lancaster has had a revenue CAGR of 2.5%, but from FY2021 forward the CAGR is significantly better at 11.1% to current trailing revenues .

{kind=link}

Due to the promising licencing sales, I would estimate some growth to continue into at least the medium-term future despite slowing down inflation. In Q1/FY2024, retail revenues grew by 8.5% mostly due to a strong performance in the licenced sales, as told in Lancaster's Q1 earnings call with Buffalo Wild Wings and Chick-fil-A being the main contributors to the achieved growth.

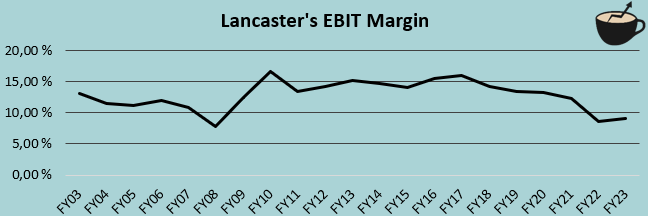

Lancaster has had an average EBIT margin of 12.9% from FY2003 to FY2023 but has achieved a significantly poorer margin level in recent years - currently, the trailing EBIT margin stands at 9.4%. The margin has begun recovering after FY2022 as a result of a higher revenue level and the management's select margin initiatives. Currently, Lancaster is focusing on supply chain management through the thorough implementation of an ERP system, improving the manufacturing plants' cost-effectiveness, and looking for lower raw material cost solutions in packaging and ingredients. I believe that these initiatives should affect the EBIT margin going forward, as the initial implementation of the ERP system seems to have already scaled the margin back by a small amount. A sustainable long-term margin is yet to be seen, but I would expect a recovery back to low double-digit margins. For example in Q1/FY2024, Lancaster reported an EBIT margin of 12.3%, or a 0.7 percentage point increase year-over-year showing good progress.

{kind=link}

Valuation

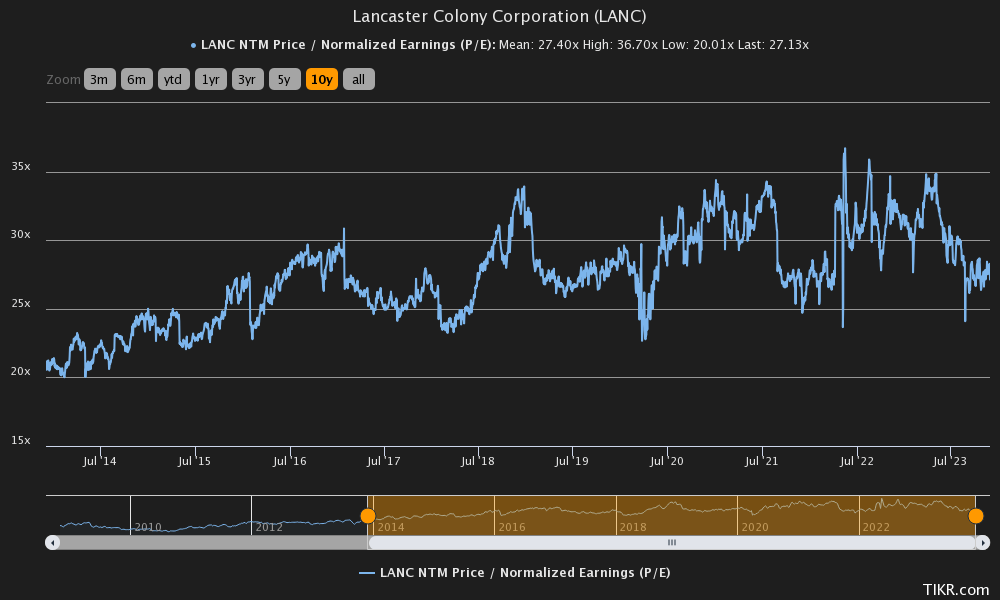

Lancaster trades at a forward P/E multiple of 27.1. The multiple seems quite high, but is in line with the company's ten-year average of 27.4:

{kind=link}

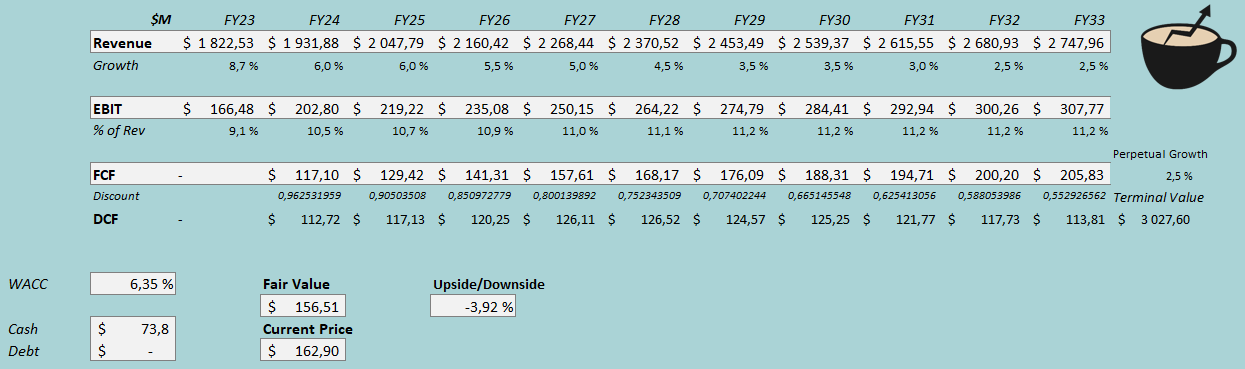

A historical P/E level isn't a very good indicator of a stock's fair valuation, though - higher-than-average interest rates and the current licencing growth initiatives make the current fair value different than historically. To estimate a rough fair value for the stock, I constructed a discounted cash flow model in my usual manner. In the model, I estimate Lancaster to grow well through the growing licenced sales - for FY2024, I estimate a growth of 6%, slightly lower than the reported Q1 growth of 8.5%. After the year, I estimate the growth rate to come down in steps into a perpetual growth rate of 2.5%, in line with Lancaster's long-term history. Altogether, the revenue estimates represent a CAGR of 4.2% from FY2023 to FY2033.

I believe that the margin initiatives should be able to yield results in coming years along with a higher revenue level - I estimate the EBIT margin to rise from a level of 9.5% in FY2023 into an eventually achieved level of 11.2%. The estimate is still below Lancaster's long-term average, but I don't see a full recovery into the FY2003-FY2023 average of 12.9% as likely.

With the discussed estimates along with a cost of capital of 6.35%, the DCF model estimates Lancaster's fair value at $156.51, around 4% below the stock price at the time of writing. The financial assumptions seem to be in line with the stock market's expectations - the estimated future would most likely return a good enough return, but not an outperformance.

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Lancaster doesn't leverage interest-bearing debt on the company's balance sheet . I believe that this method of financing is inefficient - debt could provide cheap leverage to the financing, and as Lancaster's operations are very stable with little to no operational risk from macroeconomic turbulence, a modest amount of debt would be very safe as well. I don't see a change in the financing as very likely at the moment - I estimate a long-term debt-to-equity ratio of 0%.

For the risk-free rate on the cost of equity side, I use the United States 10-year bond yield of 4.38% . The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the United States, made in July. Yahoo Finance estimates Lancaster's beta at a figure of 0.30 . Finally, I add a small liquidity premium of 0.2%, crafting a cost of equity and WACC of 6.35%.

Takeaway

Lancaster should be poised for growth through the signed, as well as potential new licence agreements with fast food restaurant chains. Through the agreements, I would expect Lancaster to see good single-digit growth rates in entire revenues in the medium term. As Lancaster is focusing on improving margins, the margin expansion also drives for an improved earnings level. I believe that the earnings growth factors are priced in, though, as my DCF model estimates the stock to be valued fairly. It is important to note that the DCF model also utilizes a very low WACC - Lancaster's operations are very low-risk, also lowering the required return on the stock. The stock seems to be priced for a required return and mostly fits investors looking for stable picks. As I believe the stock's risk-to-reward to be balanced, I have a hold rating for the time being.

For further details see:

Lancaster Colony: Licenced Brands Create Room For Growth