LANC - Lancaster Colony: Solid Fundamentals Strongest Defense But Overpriced

2023-06-04 23:48:07 ET

Summary

- Lancaster Colony Corporation maintains strategic pricing and efficiency to stabilize revenues and margins.

- Its financial positioning is the solid foundation of its operations.

- It has high liquidity levels to sustain its capacity and deliver dividends.

- However, the stock price uptrend is too high for its fundamentals, so I'm rating it a hold.

Inflationary headwinds have been disruptive in the past year. And until now, its impact lingers through the still elevated prices and interest rates. It is no surprise consumer spending has cooled down since then. Despite the improved economic confidence, recession fears are still seeping through every household and business. Thankfully, Lancaster Colony Corporation (LANC) stays on the defensive mode. It protects its colony through its strategic pricing to offset sales volume and cost pressures. Even better, it maintains a healthy Balance Sheet, as shown by its well-managed cash and borrowing levels. Its excess liquidity allows it to sustain its current size and capital returns. With that, dividends remain well-covered with decent yields. Meanwhile, the stock price adheres to the fundamentals. But recently, its upward momentum appears to have slowed down. It is logical, though, given the overvaluation, limiting its upside potential.

Company Performance

Generally, food product manufacturers and marketers are part of macroeconomic staples. Lancaster Colony Corporation is one of them. But given its business model that caters to retail and food service, its risk exposure is also high. In a volatile economy, higher prices and interest rates may disrupt its growth potential. And now that a new recession may take place, it must be more cautious to stabilize its operations. Even so, the company seemed to have thought about it a hundred times. Some strategies were reflected in its most recent report. Well-balanced growth and margins demonstrated its prudence and efficiency.

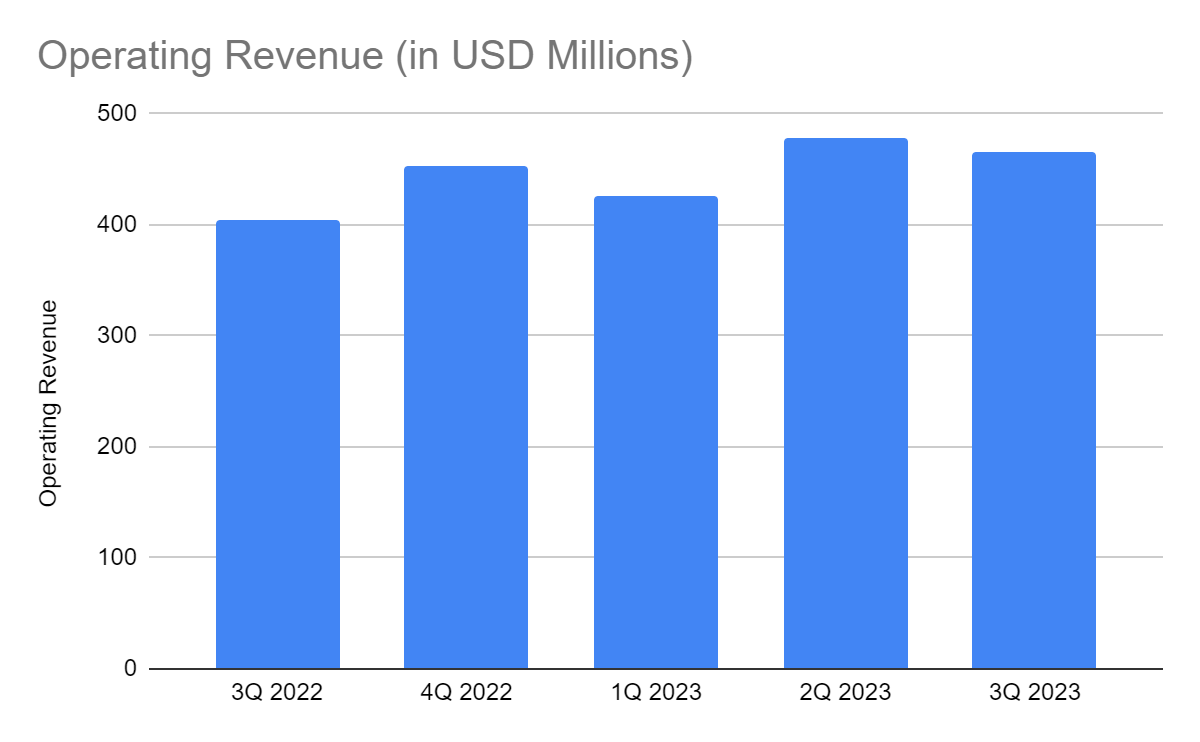

Its operating revenue in 3Q reached $464.94 million . It showed a notable decrease from 2Q 2022, but we can associate it with seasonality and higher prices. Also, it was a 15% year-over-year increase, showing its sustained strength amidst disruptions. Both its retail and food service showed double-digit growth. We can attribute this uptrend to several factors. The changing consumer behavior was an essential factor to consider. Although it may be unquantifiable sometimes, we can focus on certain aspects. For example, the eating and sleeping patterns of consumers have changed since the pandemic. Many have become more health conscious to improve their immunity. In a study, more than half of the respondents said they have changed their meal frequency and snacking habits since the pandemic. High-protein and high-mineral food products became the top choices for a healthier lifestyle. This trend had a positive impact on LANC since it produces nutritious food. These include salad dressings and toppings and vegetable and fruit dips. The UK showed the same trend, with Uber Eats claiming 2,800 healthy food orders daily. It was higher than in 2021 with 1,800 and in 2020 with 1,400. The prevalence of hybrid work setup also drove their preference for healthier and easy-to-prepare meals. Working at home could have meant more time to prepare food for the family. But it did not become a popular trend. In another study, 57% of employees said they were too busy or engrossed with work to maximize their lunch break. Meanwhile, 53% of respondents with children said they made an error at work while preparing meals for their family. It is no surprise that over 80% said food delivery services are here to stay.

{kind=link}

Operating Revenue (MarketWatch)

But of course, things did not go smoothly as inflation kept increasing. Given this, its active product repricing was strategic for the company. It helped stabilize demand by helping its customers maintain their purchasing power. Although it seemed that LANC was already at the top end of price changes, the relaxing inflation had an impact. It did not materialize in near-term performances, but it increased consumer confidence. Even better, there was a sustained uptrend in average hourly wages , helping employees in their cost-of-living adjustments. It was more important in discretionary spending even if LANC’s products were part of consumer staples. Easter holiday was vital in increasing the advanced shipments of its products. With that, there was a 6% volume growth in the retail segment and a 14% volume growth in the food service segment.

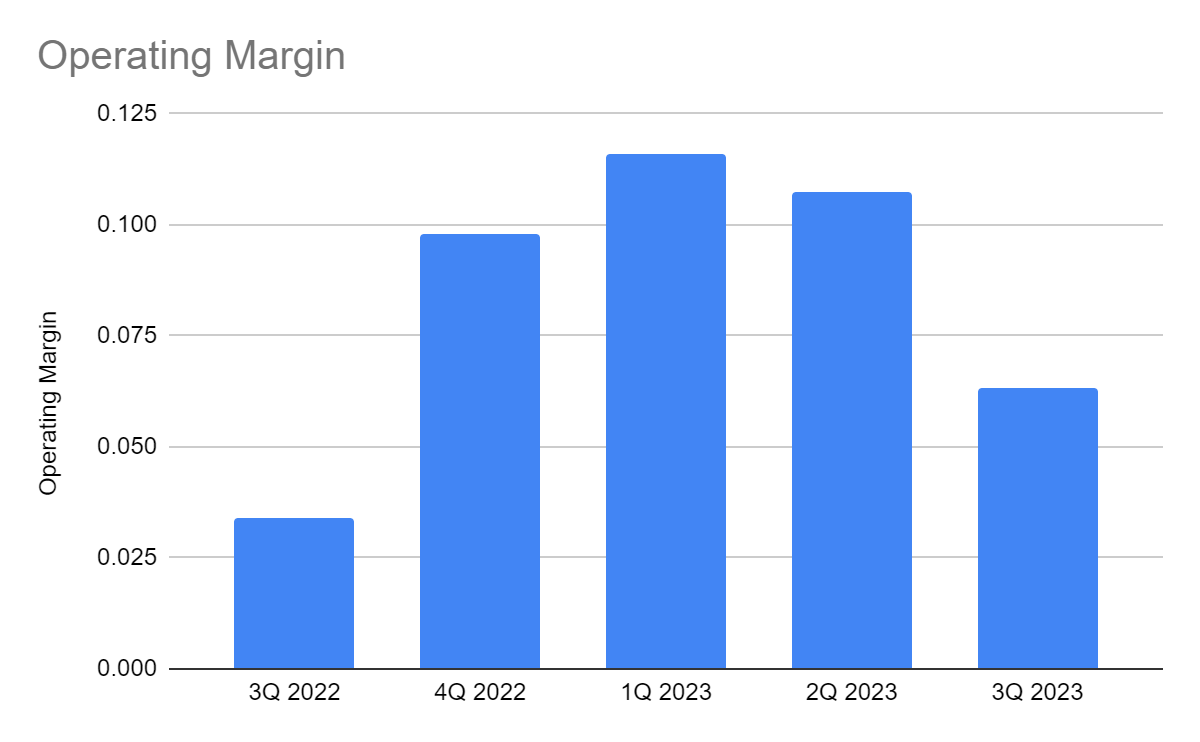

Its effective pricing strategy also helped offset cost pressures, which could have squeezed margins. Most importantly, it showed improved efficiency. Its operating costs remained relatively flatter with an increase of 10%, so revenue growth easily offset it. Yet, the increase in SG&A was sharper at 20%. Despite this, we can attribute the increase to labor-related expenses. It was essential for the company, given the higher volume in the quarter. The higher number of employees and wages led to higher productivity. Also, the operating leverage increased from 14% to 15%, showing better business scalability. The company managed variable costs better, which was a crucial aspect amidst the rising prices. Hence, the operating margin stayed manageable at 6.3% versus 3.4% in 3Q 2022.

{kind=link}

Operating Margin (MarketWatch)

In its FY 2024, Lancaster may have to deal with the same challenges. The fierce competition in the market is one factor to consider. The impact of recession fears may intensify in the second half. But some opportunities must not be downgraded as inflation relaxes more. The following section will cover its core competencies and potential risks and opportunities.

How Lancaster Colony Corporation May Stay Secure This Year

In its 3Q 2023 performance, Lancaster Colony Corporation exuded durability despite market headwinds. But it must not become too complacent as macroeconomic disruptions are still far from over. Prices are still increasing, so LANC’s flexibility may tighten more. Interest rate hikes remain persistent, which can drive another recession. The consolation is that its borrowing levels remain low and stable, suitable in a high-interest environment.

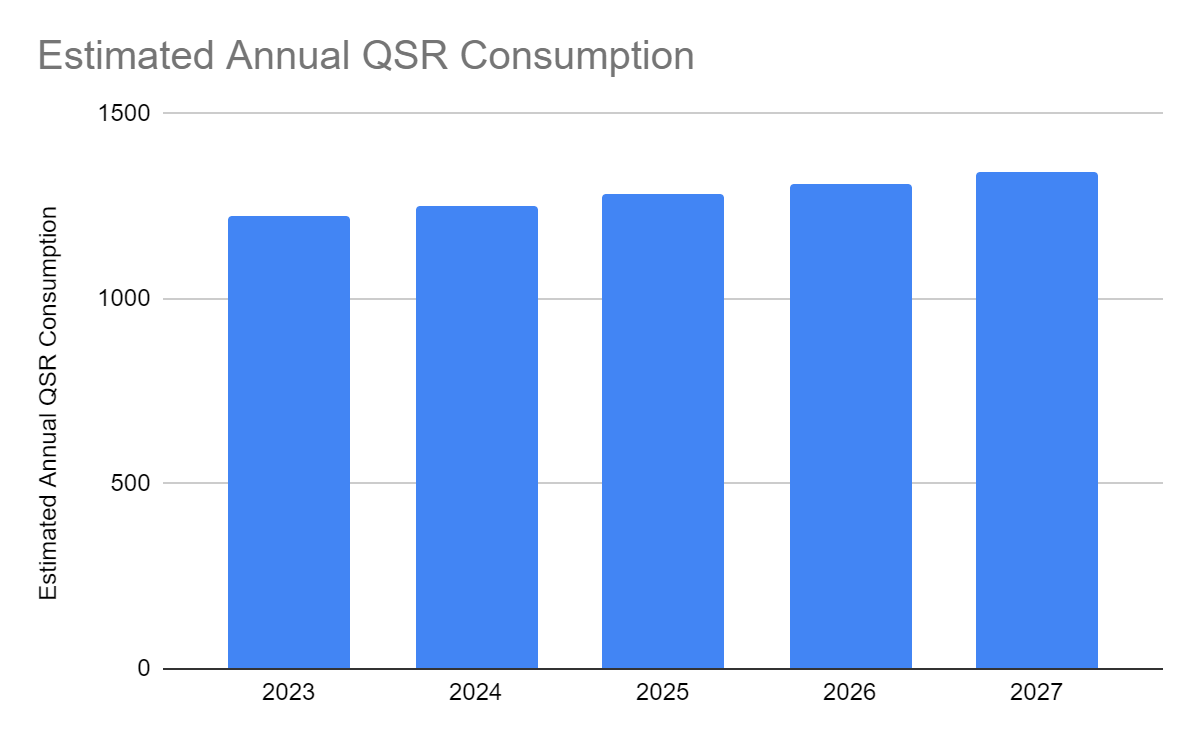

On a lighter note, inflation has relaxed at 4.9% , a 46% difference from the 2022 peak of 9.1%. This downtrend was faster than thought, and if it continues, economic confidence may rebound. It can help slow down or even halt interest rate hikes. It can also improve the purchasing power of customers and help the company determine more strategic pricing. So if volume decreases, a more strategic pricing can offset its impact to maintain revenues or minimize revenue decreases. It can also manage its operating costs and expenses better. Doing so may help stabilize margins and returns. Its foodservice segment may also see tailwinds as more companies plan to adopt hybrid work setups. We already saw the positive correlation between work flexibility and food delivery. In the US, 72% of companies have started investing in technologies to help them shift to hybrid work. Another 74% said they plan to adapt to hybrid work setups. It is no surprise that QSR spending per American reached $1,200 in 2022. Estimates show that it may keep rising by 2.2%, reaching $1,226 this year. This trend may be advantageous since LANC also produces sauces for QSR brands like Buffalo Wild Wings and Chick-fil-a. The potential problem it may face is the impact of the backlash the Chick-fil-a faces. Like Anheuser-Busch InBev ( BUD ) and Target ( TGT ), it also takes beating after its diversity efforts resurfaced.

{kind=link}

Estimated Annual QSR Consumption (Budget Branders)

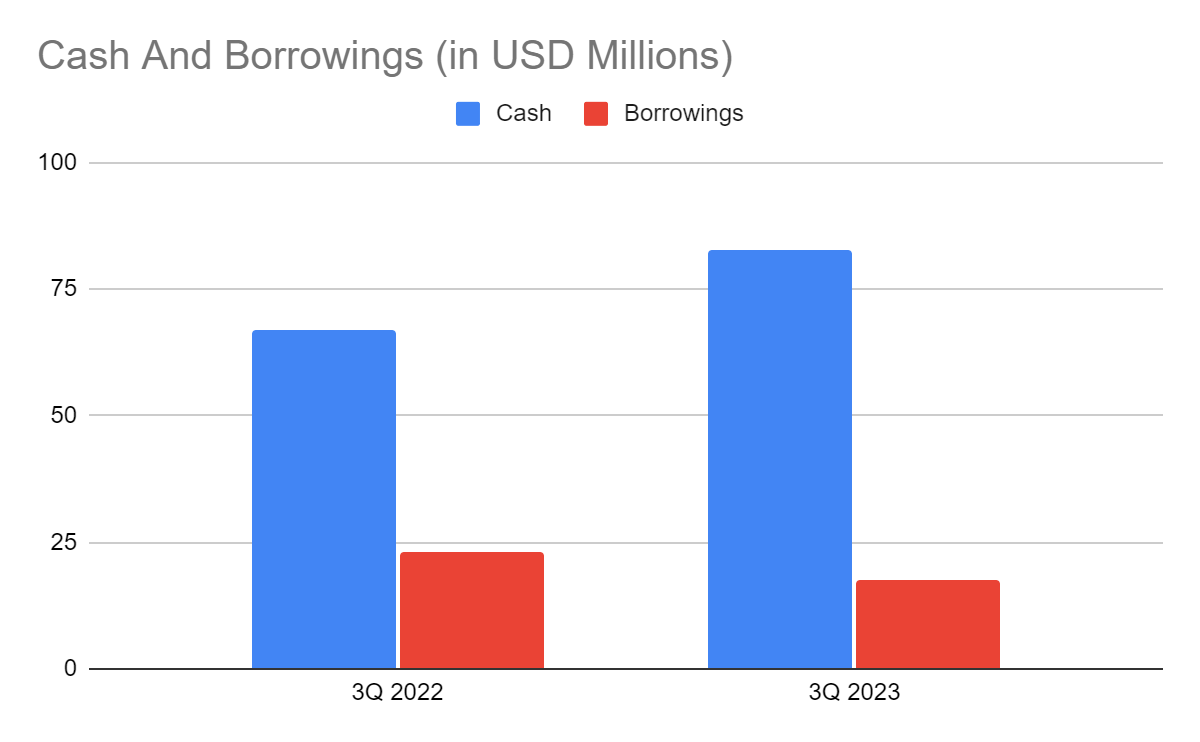

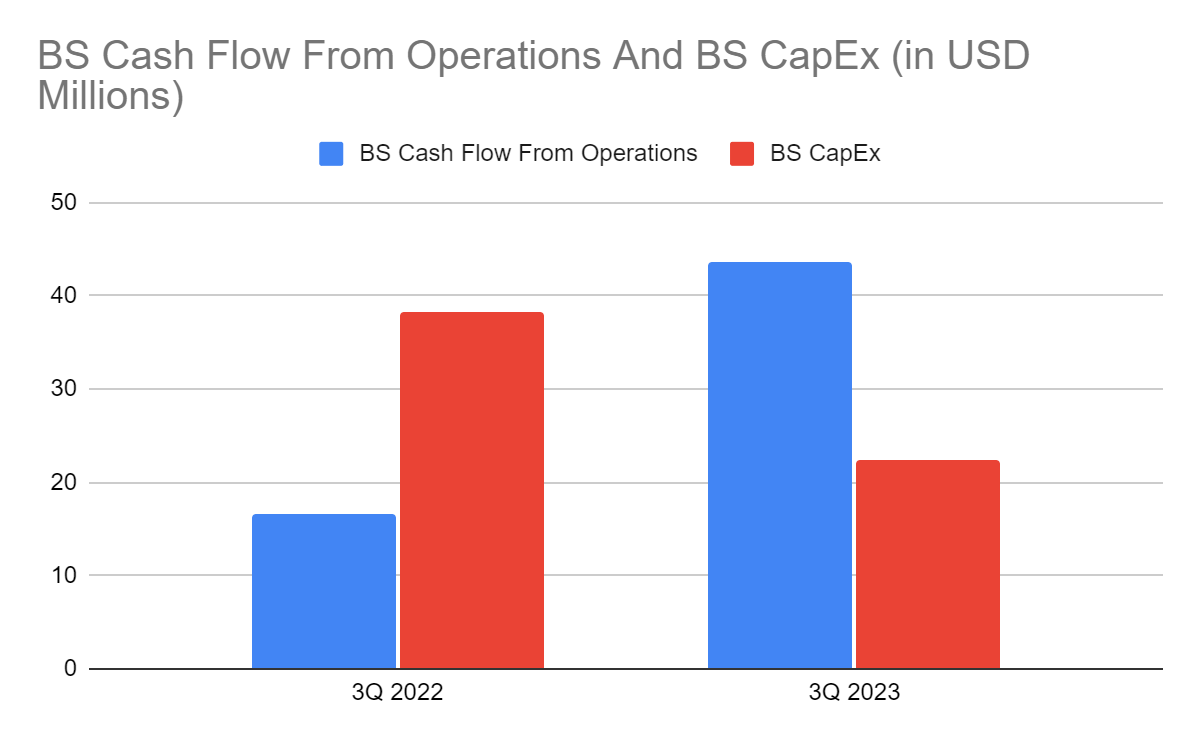

Amidst all these, the cornerstone of its operations is its solid financial positioning. Its healthy Balance Sheet shows its sound fundamental health. Its excess liquidity demonstrates how it can sustain its capacity even if it does not generate net income or cash inflows. The cash levels of the company remain adequate at $82.9 million, a 24% increase from the comparative quarter. Also, it is way higher than borrowings of only $17.4 million. LANC may cover all borrowings in a single payment. None of its borrowings will mature this year, so it does not have to worry about its interest expenses. The remaining amount can also cover capital returns through dividend payments and share repurchases. We can confirm its high liquidity levels in the Cash Statement. It had a higher cash flow from operations, while CapEx decreased. Meanwhile, its FCF of $21.4 million verifies the increase in cash levels. As such, a substantial portion of sales went into cash. The company maintains the balance between growth and viability with sustainability.

{kind=link}

Cash And Equivalents And Borrowings (LANC 3Q Report)

{kind=link}

BS Cash Flow From Operations And BS Capex (LANC 3Q Report)

Stock Price Assessment

The stock price of Lancaster Colony Corporation has increased over the years. It slowed down in recent months, but the uptrend remained visible. At $201.32, the stock price is 73% higher than last year’s value. However, the upside potential becomes narrower due to potential undervaluation. We can see it in the PB Ratio, given the current BVPS and PB Ratio of 31.73 and 6.36x. But if we use the current BVPS and the average PB Ratio of 5.76x, the target price will be $182.59.

Despite this, the company is still an ideal dividend stock with consistent payouts and yields of 1.73%. It is higher than the S&P 400 average of 1.7%. They are well-covered since cash reserves are more than thrice the value of the dividends. Moreover, investment returns are high using the cumulative EPS and the average stock price change since 2019. The cumulative EPS reached $22.54, while the average stock price change was $45.47. With that, a $1 increase in EPS led to a $2.01 increase in the stock price. It also showed the consistency between company fundamentals and the stock price. To assess the stock price better, we will use the DCF Model.

FCFF $204,250,000

Cash $82,860,000

Borrowings $17,470,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 27,523,000 Stock Price $201.32

Value Target $171.19

The derived value adheres to the supposition of a potential overvaluation. There may be a 15% downside in the next 12-18 months. While the fundamentals are solid, the stock price exceeds the intrinsic value. There may be risks in the stock price. So, investors may have to wait for a better entry point.

Bottom line

Lancaster Colony Corporation remains a solid company despite its high risk exposure to macroeconomic volatility. Its sturdy fundamentals show it can withstand market blows, cover its operating capacity, and distribute capital returns. It has adequate cash levels and low borrowings, which fit the current environment. However, the stock is overvalued with reasonable downside potential, not a good bargain now. The recommendation, for now, is that Lancaster Colony Corporation stock is a hold.

For further details see:

Lancaster Colony: Solid Fundamentals, Strongest Defense But Overpriced