LANC - Lancaster Colony: What To Make Of This Dividend King?

2023-06-27 06:47:13 ET

Summary

- Lancaster Colony Corporation is a dividend king with 60 consecutive years of dividend hikes, but its stock remains relatively unknown due to its small market cap of $5.5 billion.

- The company specializes in manufacturing and marketing specialty food products, with a strategic growth plan focused on accelerating base business growth, simplifying the supply chain, and expanding the core business.

- Despite a low yield of 1.7%, LANC's dividend is backed by a consistent growth track record, a net income payout ratio of 62%, and a history of outperforming the market.

Introduction

The Lancaster Colony Corporation ( LANC ) is a member of a very exclusive club. This dividend king has hiked its dividend for 60 consecutive years, which means it has been a dividend king for ten years.

However, the stock doesn't receive much attention, as the company is far from large. With a $5.5 billion market cap, it's a tiny player compared to some of the big guys in the consumer defensive sector.

If it weren't for a friend and reader of my articles, I would not be covering this stock today. So, thank you for reminding me!

In 2021, I covered the company. Back then, I gave the stock a buy rating. Looking at the coverage list , it was the last buy rating the stock received since then.

In this article, I want to shed some light on this company, discuss its qualities as a dividend stock, and re-assess the buy rating I gave back then.

So, without further ado, let's get to it!

What's LANC?

I like it a lot when readers bring up companies - especially when they line up with bigger economic topics that we have been discussing for a while on Seeking Alpha.

In this case, Lancaster Colony isn't just an interesting consumer stock, but it also tells us a lot about the industry it serves.

Right now, consumer staples are trying to balance input cost inflation and pricing power, which is a tough task.

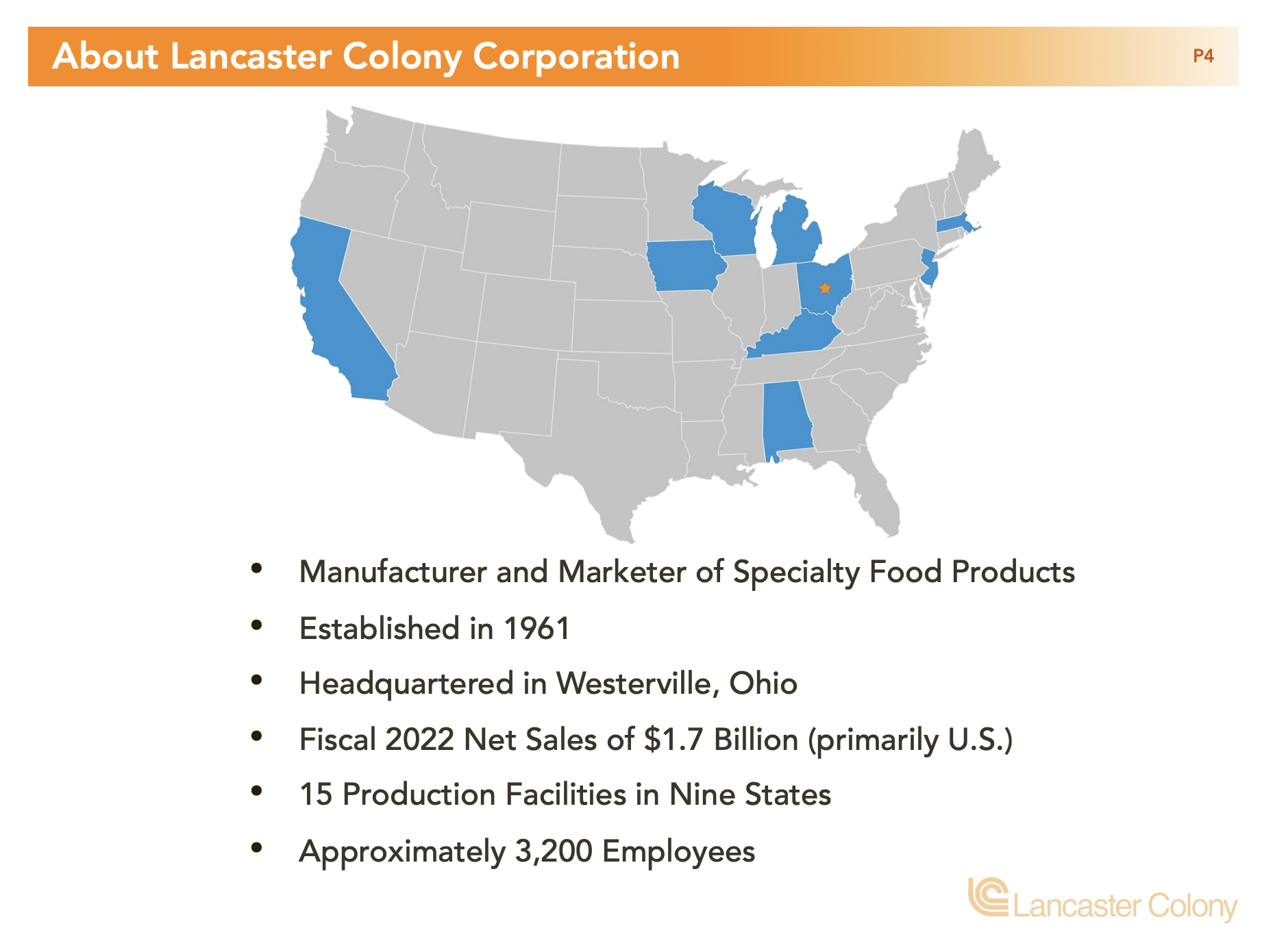

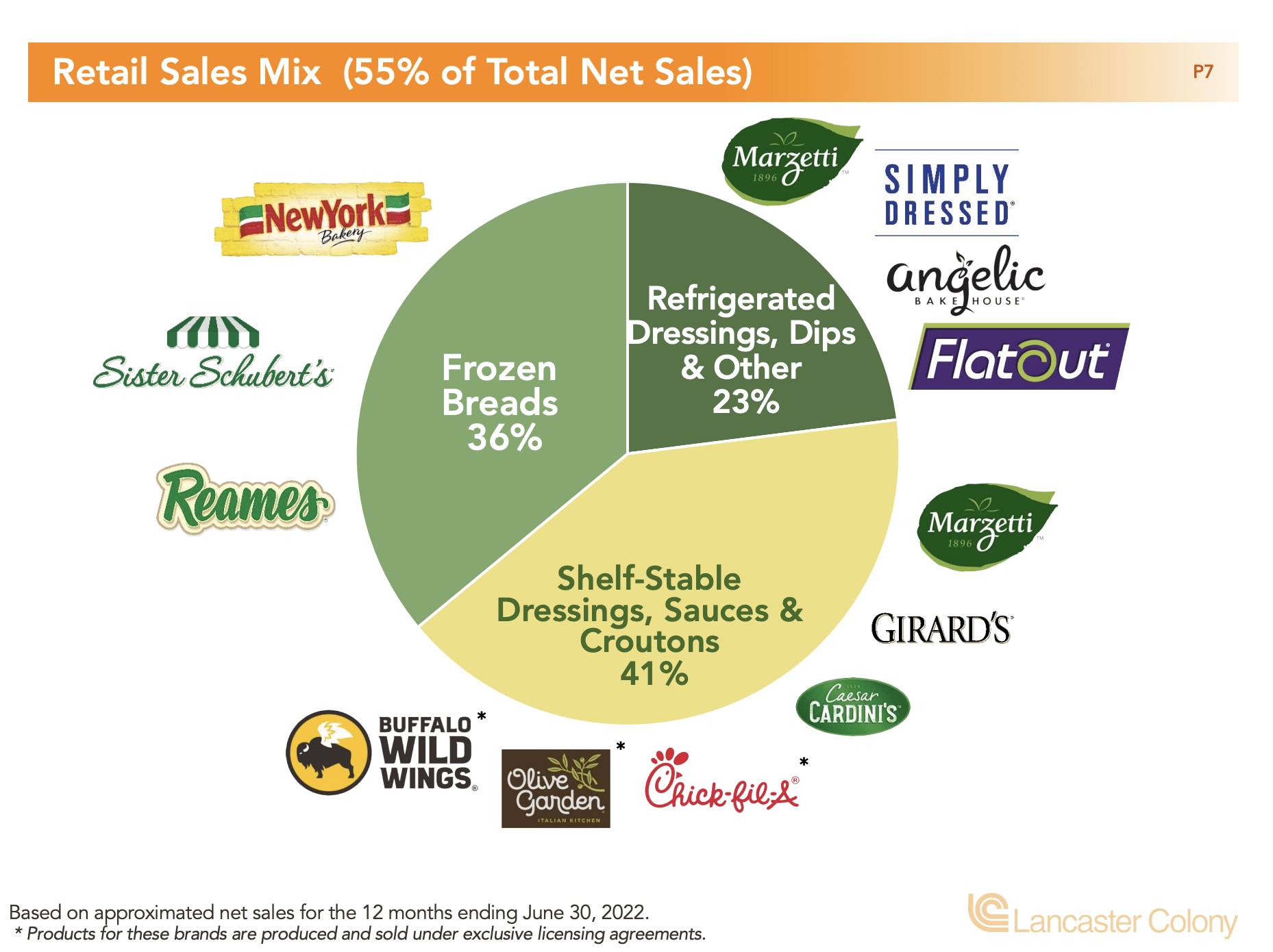

The Lancaster Colony Corporation is an Ohio-based company that specializes in manufacturing and marketing specialty food products for both retail and food service channels.

- Retail Segment: Shelf-stable dressings, sauces, and croutons accounted for 22% of net sales in 2022, frozen bread for 20%, and refrigerated dressings, dips, and other products for 13%.

- Foodservice Segment: Dressings and sauces contributed 34% of net sales in 2022, while frozen bread and other products accounted for 11%.

{kind=link}

LANC is a supplier to 17 of the top 30 national restaurant chains in the United States, it has a growing licensing program, and it's just one of 13 companies in the US that have increased the regular dividend for 60 consecutive years.

In its licensing business, the company sells sauces from companies/brands like Buffalo Wild Wings, Olive Garden, and Chick-fill-A.

{kind=link}

Lancaster Colony operates 15 food plants throughout the United States, where the majority of its products are manufactured and packaged. The company places a strong emphasis on efficient and cost-effective production, with a focus on lean six sigma practices. Additionally, certain products are manufactured and packaged by third-party entities in the United States, Canada, and Europe. This, too, is quite common for a company like LANC.

When it comes to its customer breakdown, we're dealing with 18% net sales exposure to Walmart ( WMT ) and 11% exposure to McLane, a company owned by Buffett, which is a wholesale distributor.

The company has a number of strategic goals, like producing high-quality foods resulting in high customer satisfaction while performing well financially. In order to achieve these somewhat obvious goals, the company has a strategic growth plan consisting of three pillars:

- Accelerating base business growth.

- Simplifying the supply chain to reduce costs and increase margins.

- Expanding the core business through a Retail licensing program and strategic mergers and acquisitions.

This brings me to its dividend.

The LANC Dividend

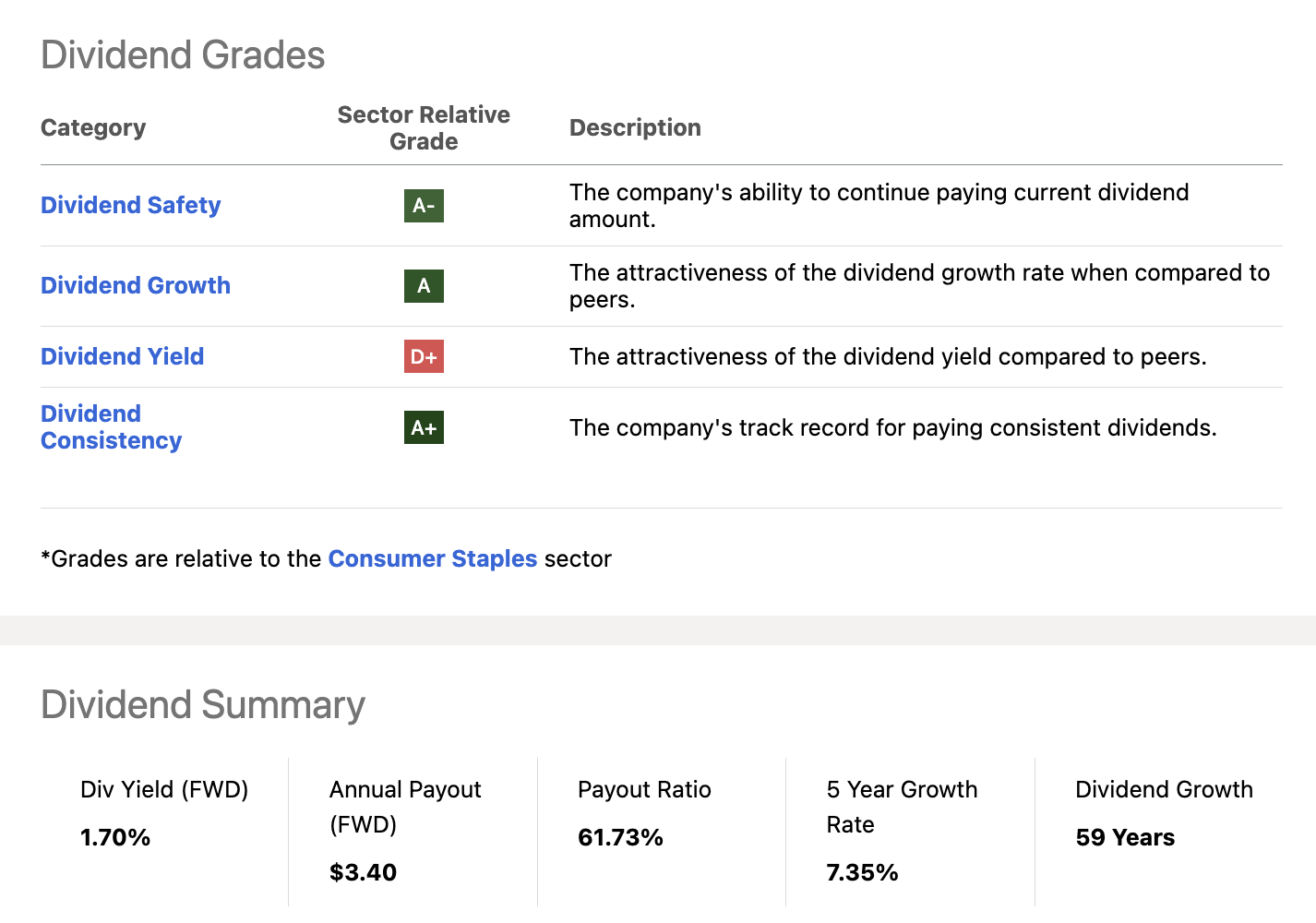

Lancaster Colony has a fascinating dividend scorecard. We see one big red spot in a sea of red. In this case, the company scores high on dividend consistency, growth, and safety. Unfortunately, it scores low on its yield.

{kind=link}

In this case, the company yields 1.7%, which is below the median sector yield of 2.6%.

However, this yield is backed by an LTM net income payout ratio of 62%, 7.4% average annual dividend growth over the past five years, and one of the most consistent dividend growth track records in the world.

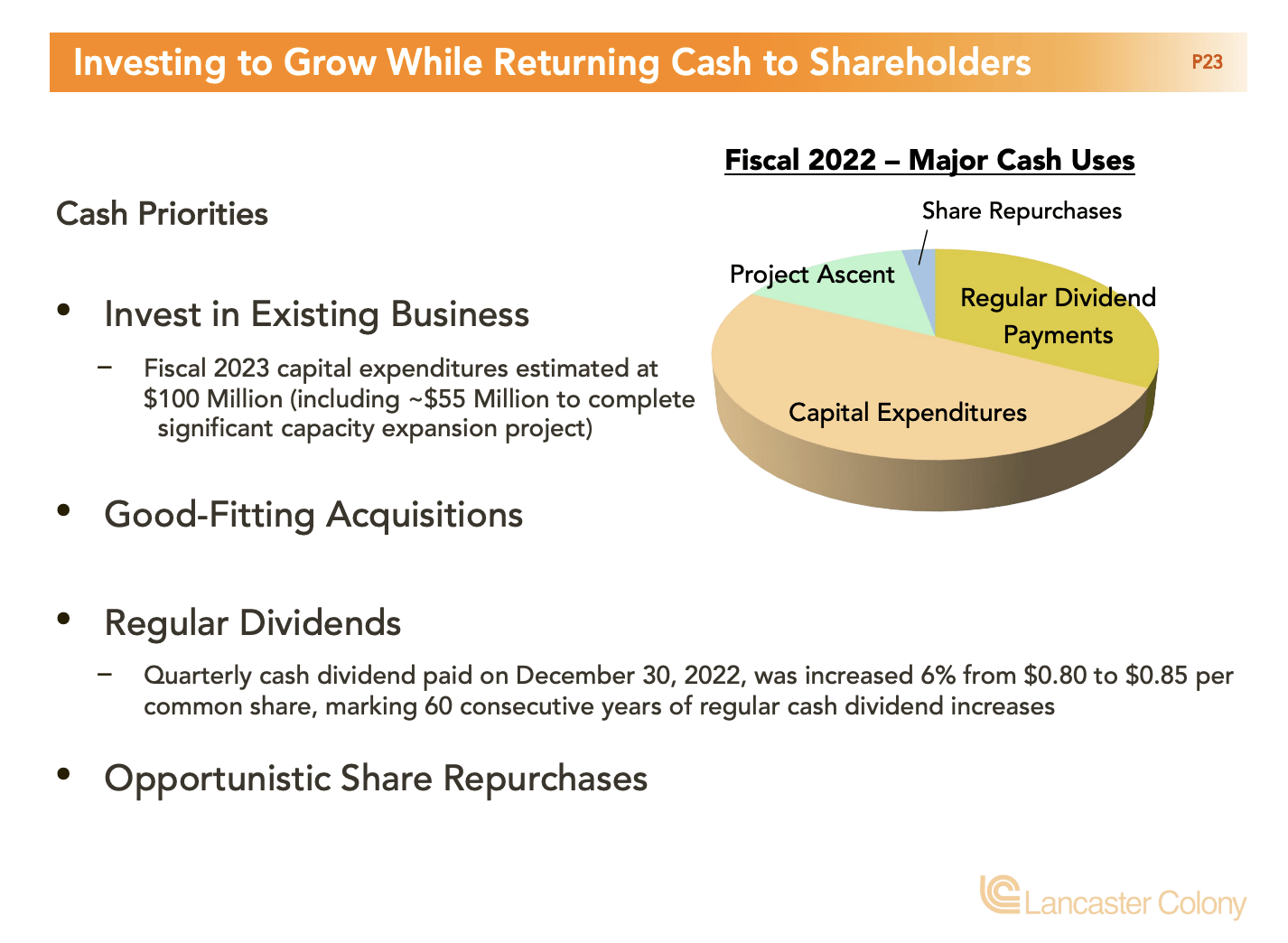

The company's dividend is its third cash priority after organic and acquired growth.

{kind=link}

A consistent dividend growth track record not only benefits investors when it comes to income generation but is also a sign that investors are dealing with a high-quality company. It's a stamp of approval, so to speak.

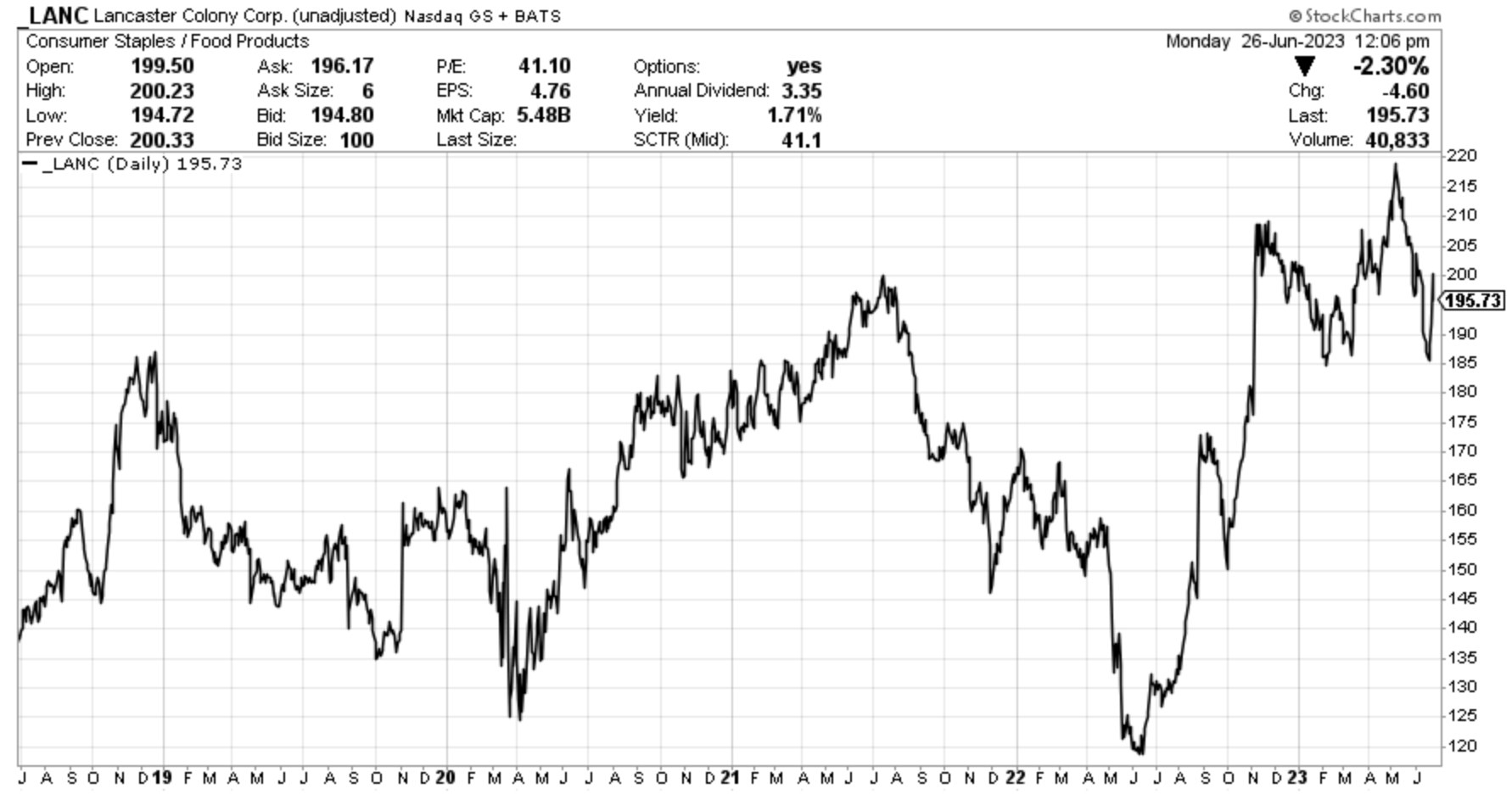

Generally speaking, these companies tend to outperform the market. While it was hard for consumer staple companies to outperform the market during the past ten years due to the huge technology benefit of the S&P 500, LANC did return 224% since June 2013, which is more or less in line with the total return of the market.

The company beat its peers by a wide margin, albeit with higher volatility.

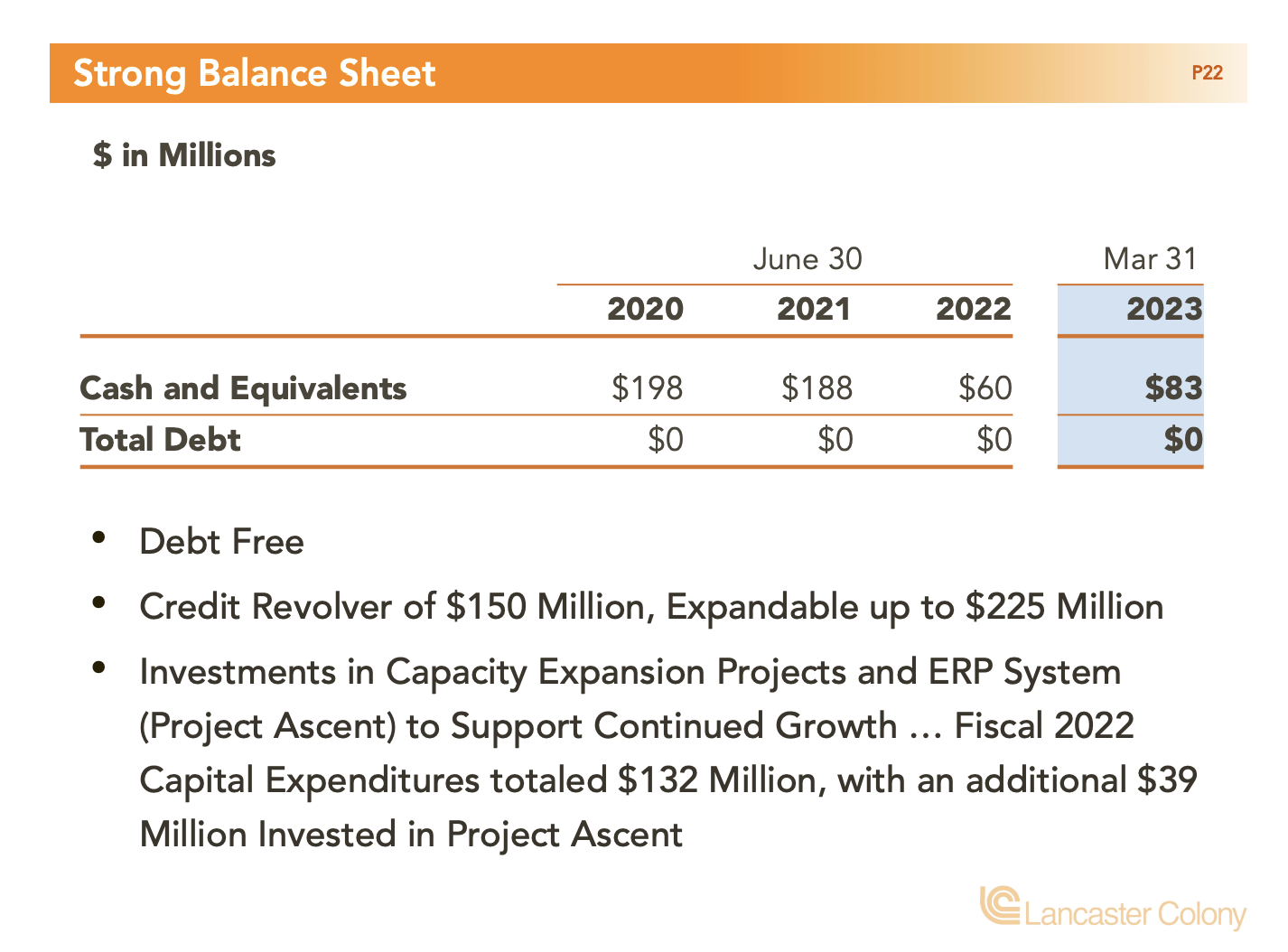

Furthermore, the company has a healthy balance sheet, which means it can focus on shareholders over debtholders.

The company is debt free with $83 million in cash/equivalents and up to $225 million in available credit.

{kind=link}

So, how is the company doing in light of ongoing challenges?

Recent Events & Outlook

I own one consumer staple company: PepsiCo ( PEP ). One reason why I own it is its ability to use pricing to offset inflationary headwinds. Despite tough competition, PepsiCo has a relatively large moat that comes with high consumer retention, even when it has to raise prices rather aggressively.

In general, however, consumer stocks are in a tough spot, as it's a low-margin business with a lot of competition. High inflation is one of the worst things that can happen to this anti-cyclical industry.

With that said, as its stock price suggests, LANC is doing quite well in this environment.

{kind=link}

In 3Q23, the company reported record sales and higher profits.

- Consolidated net sales increased by 15.2% to $465 million, while consolidated gross profit improved by 37.9% to $94.2 million.

- Operating income reached $29.4 million compared to an operating loss of $7.6 million in the previous year. The prior year's operating income included a restructuring and impairment charge of $22.7 million.

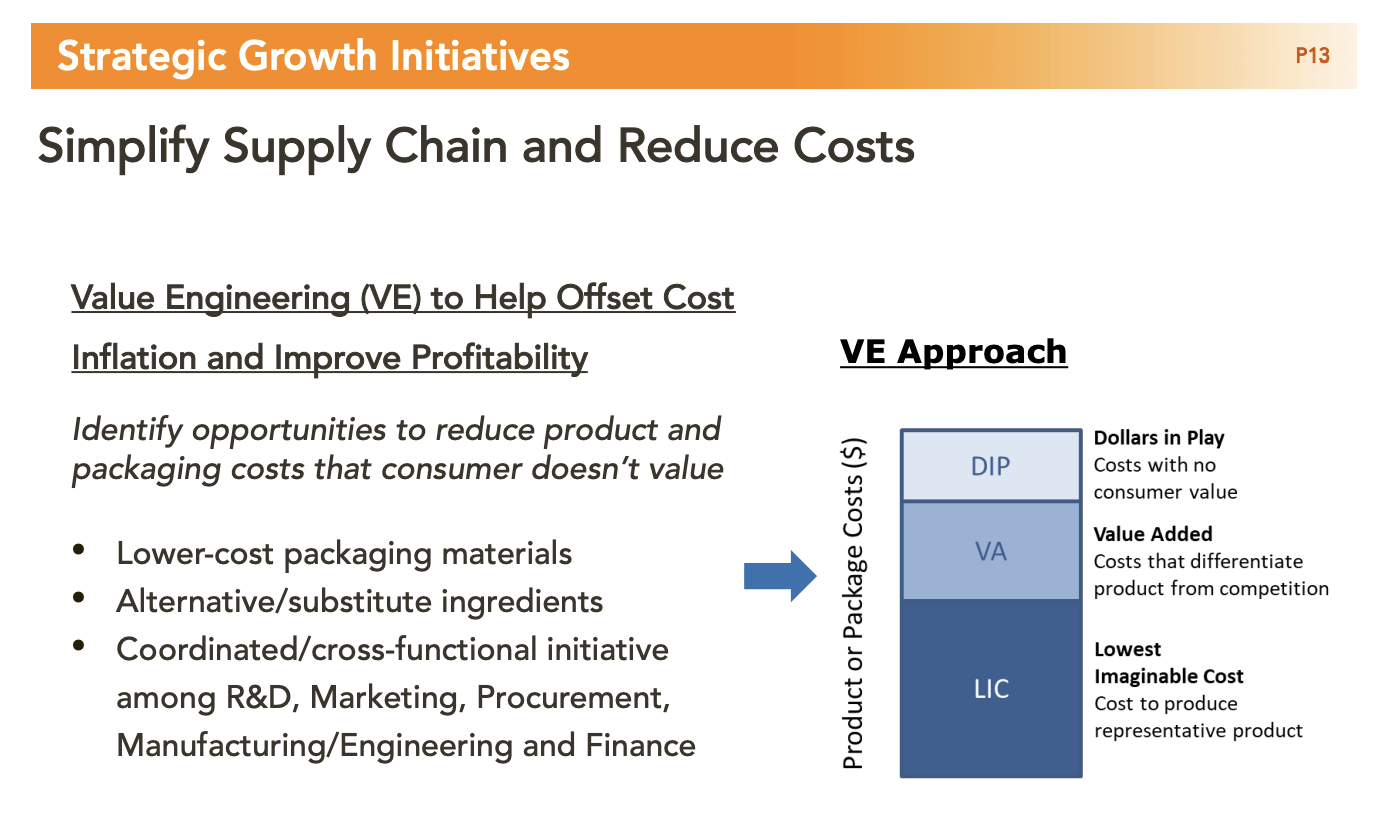

Gross profit increased by $25.9 million or 37.9% to $94.2 million, reflecting favorable PNOC (pricing net of commodities), improved supply chain performance, and higher volume.

Especially supply chain efficiencies are key, as the company has been focused on reducing packaging materials and certain ingredients without sacrificing consumer value.

{kind=link}

In the Retail segment, net sales reached $247 million, which is a 16% increase. Growth was driven by the favorable impact of pricing actions to offset inflation and strong volume growth of 6%. The volume growth was caused by the success of the licensing program and double-digit growth for the New York Bakery frozen garlic bread products.

As I already briefly mentioned, licensing partnerships with brands like Buffalo Wild Wings, RV sauces, Chick-fil-A, and Olive Garden contributed to the volume growth.

The Foodservice segment also saw positive results, with net sales growing over 14% to $218 million. This growth was driven by pricing actions, volume gains for national account customers, and increased demand for branded food service products.

Foodservice segment volume increased by less than 1%, excluding discontinued product lines from the previous year. When these less profitable product lines were excluded, food service volume grew by over 4%.

So far, what we're dealing with here is a company that was able to use higher pricing without sacrificing volumes, which is a sign that it does have a strong position in its market.

Furthermore, in addition to investing in a more efficient supply chain and lower-cost products, the company is adding new capacities to expand production in the dressing and sauce segments. This year, the expansion is expected to be completed, which should allow the company to reduce CapEx from more than $120 million to less than $80 million per year.

{kind=link}

In the current quarter (4Q23), Lancaster Colony expects modest overall volume growth for the consolidated business and the possibility of mid-single-digit volume growth on the organic basis for the retail business.

Valuation

Over the past ten years, a big part of LANC's total returns has come from a higher valuation. In 2014, shares were trading at roughly 11x EBITDA (EV/EBITDA). Now, that number is 24.4x EBITDA.

As one might expect, EBITDA has been fairly consistent during this period.

The good news is that in the 2024 fiscal year, EBITDA is expected to reach $300 million, boosted by current investments in growth and organic growth.

This would imply an 18x valuation, which is fair.

Given that I expect the company to maintain strong growth, backed by both volume and pricing, I agree with Loop Capital, which gave LANC a $237 price target on June 23. The consensus price target is $230, which is 16% above the current price.

On a long-term basis, I expect LANC to outperform its peers in the consumer staples ETF ( XLP ). However, I'm not sure this stock can keep up with the market. That's a tough job.

In addition, the rationale behind my current decision to refrain from purchasing LANC, despite recognizing its potential undervaluation over the next 2-3 years, is due to my existing ownership of PEP. At the moment, I am not actively seeking to increase my exposure to the consumer staples sector.

Takeaway

Lancaster Colony may be a small player in the consumer defensive sector, but it's a hidden gem with remarkable qualities. As a member of the exclusive dividend king club, LANC has increased its dividend for 60 consecutive years.

With a focus on specialty food products for retail and food service channels, the company boasts strong customer relationships, strategic partnerships, and efficient manufacturing practices.

Despite challenges faced by the consumer staples industry, LANC has performed well, reporting record sales and higher profits.

Its consistent dividend growth track record, strong balance sheet, and focus on shareholder value make it an attractive investment.

While the stock's yield may be lower than the sector average, its dividend consistency, growth potential, and safety make it an attractive dividend stock.

With a positive outlook and a fair valuation, LANC has the potential to outperform its peers in the long term.

Pros & Cons

Pros:

- Consistent dividend growth for 60 years.

- Strong financial position and focus on shareholder returns.

- Positive financial performance with record sales and higher profits.

- Growth opportunities through expansion and investments.

Cons:

- Low dividend yield compared to the sector average.

- The small market cap may result in higher volatility.

- Industry challenges and competition.

For further details see:

Lancaster Colony: What To Make Of This Dividend King?