GPS - Lands' End: Only Problems Ahead For This Struggling Retailer

2023-05-29 08:14:50 ET

Summary

- Lands' End, Inc. is a digital retailer that specializes in casual clothing, swimwear, outerwear, accessories, footwear, and home products.

- Revenue growth has been non-existent in the last decade, as consumer interest declines during a period of shake-up in the apparel industry.

- LE has an EBITDA-M of 4% and a NIM of (1)%. We see no immediate scope for margin improvement.

- LE has an ND/EBITDA ratio of 4.4x, with only a 1.9x interest coverage. This creates serious solvency and liquidity issues.

- With only negatives ahead, we rate this stock a sell.

Investment thesis

Our current investment thesis is:

- Lands' End, Inc. (LE) is an unattractive business that is struggling to maintain sales. Consumer interest has been declining over the last 10 years, reflected in a decline in internet clicks.

- Margins are highly unattractive with no scope for improvement. The company is in a negative spiral as margins are foregone in order to protect sales, which are on a negative trend.

- LE's balance sheet is bloated and its coverage of interest is poor.

Company description

Lands' End, Inc. is a digital retailer that specializes in casual clothing, swimwear, outerwear, accessories, footwear, and home products. They offer a wide range of brands, including Lands' End, Lands' End Lighthouse, Squall, Tugless Tank, Drifter, Outrigger, and Marinac, among others.

In addition to their main product line, the company also sells uniforms and logo apparel.

Share price

LE's share price has trended down in the last decade, with changing industry dynamics contributing to difficult trading conditions.

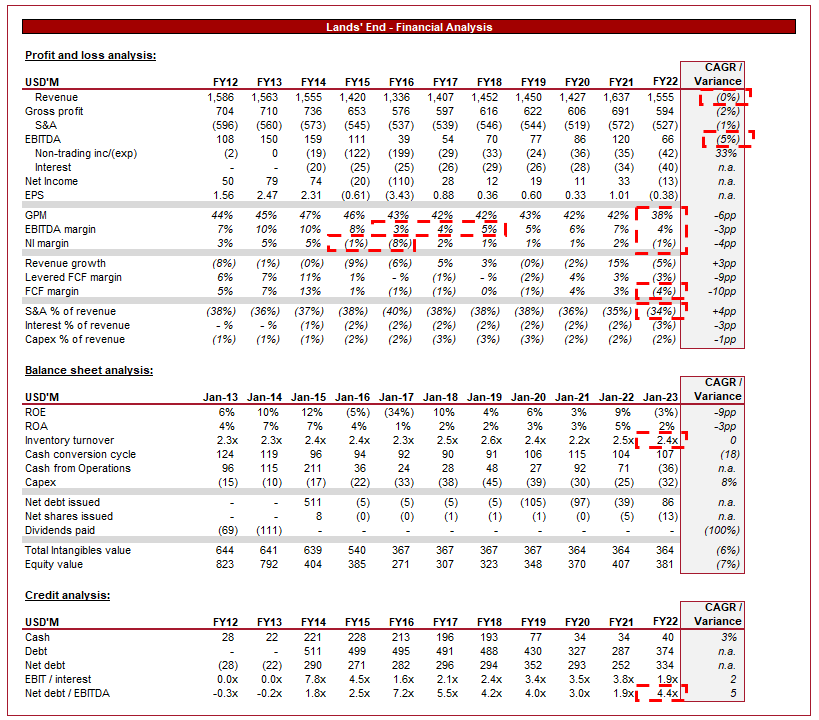

Financial analysis

Lands' End financials (Tikr Terminal)

{kind=link}

Presented above is LE's financial performance for the last decade.

Revenue

LE has achieved no revenue growth in the last decade, illustrating the struggles the company has faced. 8 of the last 10 years have seen negative growth, which illustrates the systemic issue the company faces.

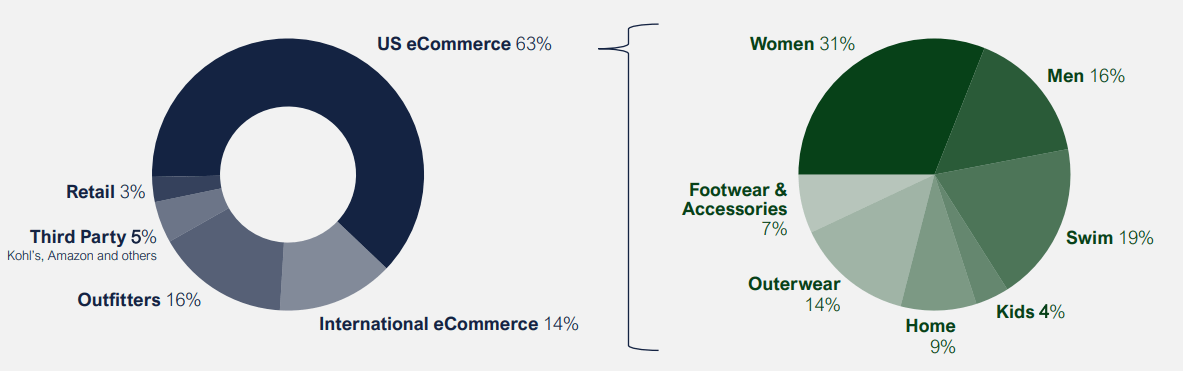

It is a fairly diversified company, both in its target market and distribution channel. The wide range of products allows LE to develop a "lifestyle" approach, which harmonizes its product range somewhat, encouraging cross-selling and multiple purchases.

Further, the company is heavily e-commerce focused, which allows the business to earn the lion's share of its profitability. The concern with retailers is that they take a cut, tightening margins. This is very impressive, as it is rare to see a retailer with such a large e-commerce presence.

The rise of e-commerce and the shift toward online shopping have significantly impacted the retail industry. Consumers are increasingly opting for the convenience of shopping online, and this trend has accelerated further due to the COVID-19 pandemic. Further, many e-commerce retailers have offset their overhead cost advantage by engaging in greater marketing / discounting as a means of gaining sales. In the case of LE, the e-commerce success is likely a reflection of its sticky customer base.

{kind=link}

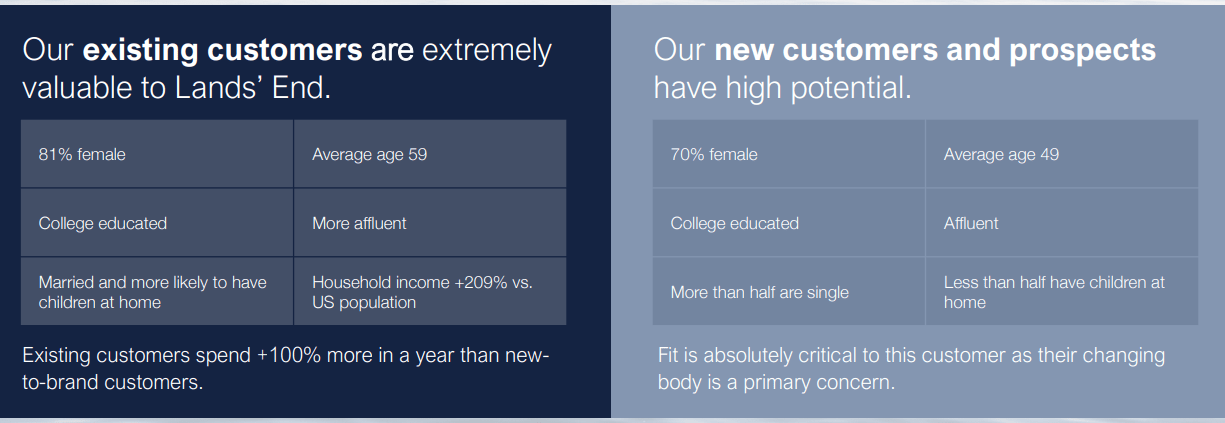

Further, LE's target customer is very focused, with sticky sales in this demographic. We like this as many retailers are too broad in their approach, contributing to difficulties with remaining competitive over time, as trends and tastes change.

Our only concern with this is that an aging customer base in conjunction with stagnating sales could contribute to a decline in interest within the demographic. The issue here is that LE may have become unattractive in its core segment.

{kind=link}

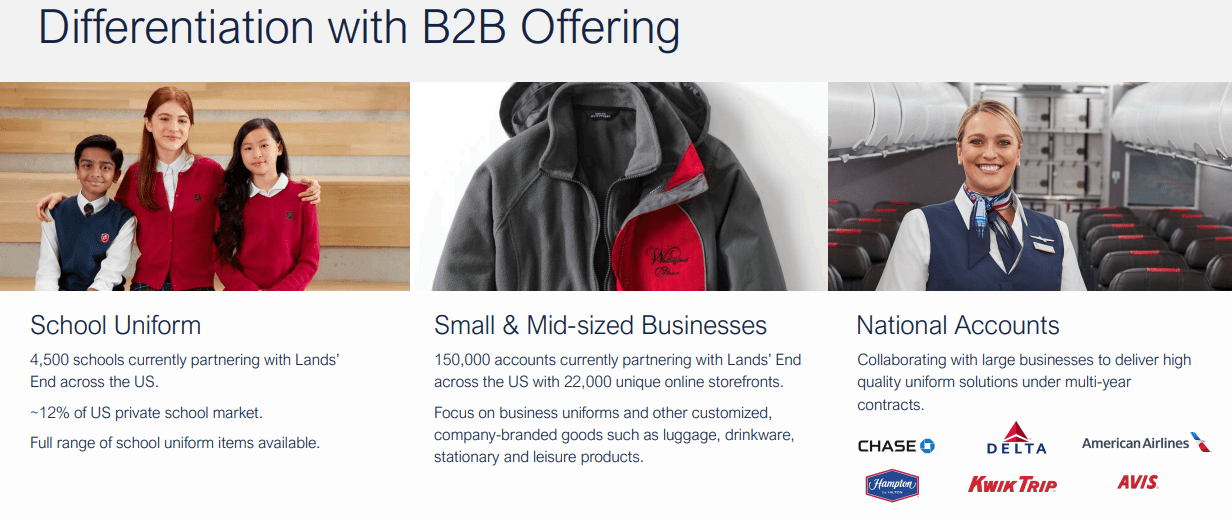

LE also benefits from its B2B offering, which is rare in retail. This gives the company a resilient portion of revenue that will grow in line with the success of its clientele.

{kind=link}

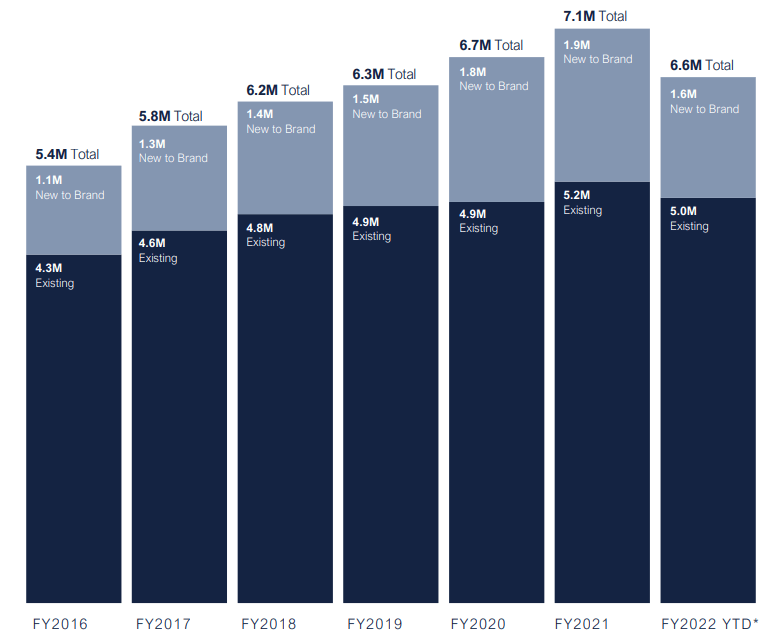

In recent years, the number of existing and new customers to the brand has been good, suggesting renewed strengths. This is a reflection of the improved marketing and an expansion of its B2B. This being said, the customer growth numbers exceed revenue growth, suggesting a reduction in the value of purchases per person.

{kind=link}

Omnichannel retailing is another trend impacting the industry. Consumers have not given up on brick-and-mortar retailers, instead, the value offering has transitioned. Consumers value a seamless shopping experience across various channels, including online, mobile, and physical stores. For example, purchasing a product online, picking it up and trying-on in store. LE does not wholly benefit from this, as it does not have a substantial national footprint, with <100 locations. This could be a contributor to the company's declining interest, as the lack of physical marketing leaves LE reliant on its retailers.

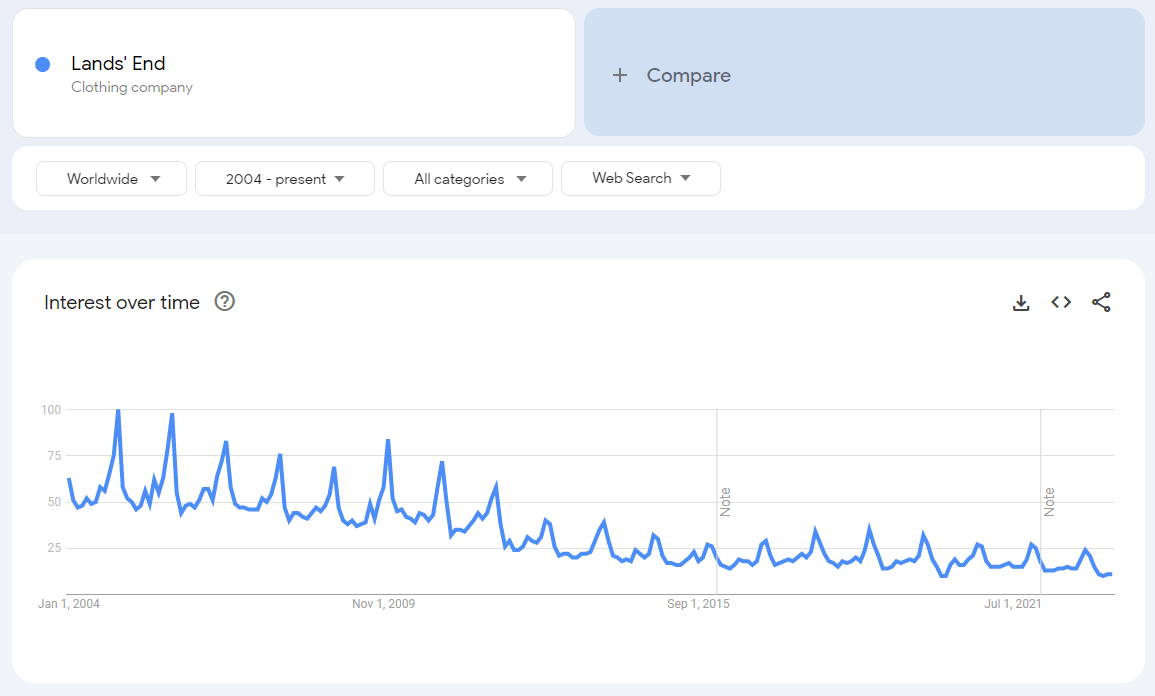

Influencer marketing and social media platforms are currently the primary drivers of growth. Brands are investing heavily in reaching customers and importantly competing against many others. LE has performed poorly in this regard, with interest consistently declining across the last decade. This aligns with the lack of growth we have seen from the brand.

{kind=link}

Finally, fashion has been materially impacted by the rise of Fast fashion. Consumers can now get fashion forward designs at a fraction of the cost and rapidly. This has negatively impacted many traditional brands that have fallen out of favor due to a commitment to their designs / approach. Our view is that LE is likely in this bucket given the decline in relevance.

Economic considerations

Current inflationary pressures are contributing to a slowdown in retail spending, as consumers commit a large proportion of income to servicing living costs. This is likely a primary reason for the 5% decline in FY22. Given that macro conditions remain uncertain, we suspect LE will face a difficult FY23. With weakness in the historical period in mind, we forecast a further decline in sales.

Margin

LE's margins have rapidly declined in the last decade, with an EBITDA-M of 4% and a NIM of (1)%.

This decline is likely due to Management seeking to defend declining interest, contributing to greater discounting and pricing changes. This is illustrated by GPM, which has fallen to below 40%.

Further, the company has faced inflationary pressures with rising production and transportation costs. This looks to be subsiding with China reopening and inflation declining in the US. We are not certain LE can easily win back its margins, however, given the level of competition in the industry.

Q1

LE is due to release its Q1 earnings in a few days. In recent weeks, we have seen many retailers posting poor financial results / growth concerns, such as American Eagle ( AEO ). Given the weaker position of LE relative to the industry as a whole, we expect sales to fall further and losses to continue.

Management and analysts are guiding the following .

" For the first quarter ahead, the apparel retailer expects net revenue to be between $295M and $310M and a diluted loss per share to be between $0.15 and $0.09. Analysts had forecast a $289.8M in revenue and a $0.31 per share loss. "

Balance sheet

A rare positive for LE is that its inventory turnover has remained flat across the period, which implies Management has a strong ability to foresee changes in demand and adapt accordingly.

LE is highly levered with a ND/EBITDA ratio of 4.4x. This restricts the company's ability to raise further debt. We are highly concerned about both solvency and liquidity issues given the company's EBIT/Interest ratio is only 1.9x.

Valuation

LE's valuation (Tikr Terminal)

LE is currently trading at 9x LTM EBITDA and 9x NTM EBITDA. This is significantly lower than its 10-year average, reflecting a period of sustained decline.

This valuation is comparable to other retailers who have faced issues in the last decade, such as The Gap ( GPS ) and American Eagle Outfitters (AEO).

The difference we see is that those businesses have scope to turn around their fortunes. With LE, we are less confident. The company is highly levered and despite some attractive qualities, LE has far too many issues.

Final thoughts

LE is not completely hopeless. The company has attractive commercial qualities, be it its sticky customers, its high-earner client base, and its B2B operations. However, almost everything else is highly concerning. There is a serious growth issue, margins are very poor, and the balance sheet is bloated with debt.

We see no real positive catalysts ahead and believe sales will decline further in the coming year. For this reason, we rate the stock as a sell.

For further details see:

Lands' End: Only Problems Ahead For This Struggling Retailer