LE - Lands' End: Solid Q3 2023 Results But Still Not Cheap (Rating Upgrade)

2023-12-13 15:48:27 ET

Summary

- The company’s gross profit margin improved by 700 basis points in Q3 FY23 thanks to cost-cutting measures.

- In addition, net debt was down to $302.2 million thanks to improved inventory management.

- While sales are still falling, I think net income could be in positive territory as soon as Q4 FY23.

- However, I think that Lands' End still doesn’t look cheap despite the positive developments and that risk-averse investors should avoid this stock.

Introduction

I've written two articles on Seeking Alpha about US e-commerce-focused clothing retailer Lands' End ( LE ), the latest of which was in September when I said that the Q2 FY23 financial results were weak and the outlook for Q3 FY23 looked bad as the net loss was expected to be between $4 million and $6.5 million.

On December 5, the company released its financial results for Q3 FY23 and I think they were decent as the adjusted net loss came in at just $3.6 million as margins improved significantly thanks to cost-cutting measures. I find it encouraging that Lands' End expects to get back in the black in Q4 FY23, and I'm upgrading my rating on the stock to neutral. Let's review.

Overview of the Q3 FY23 Results

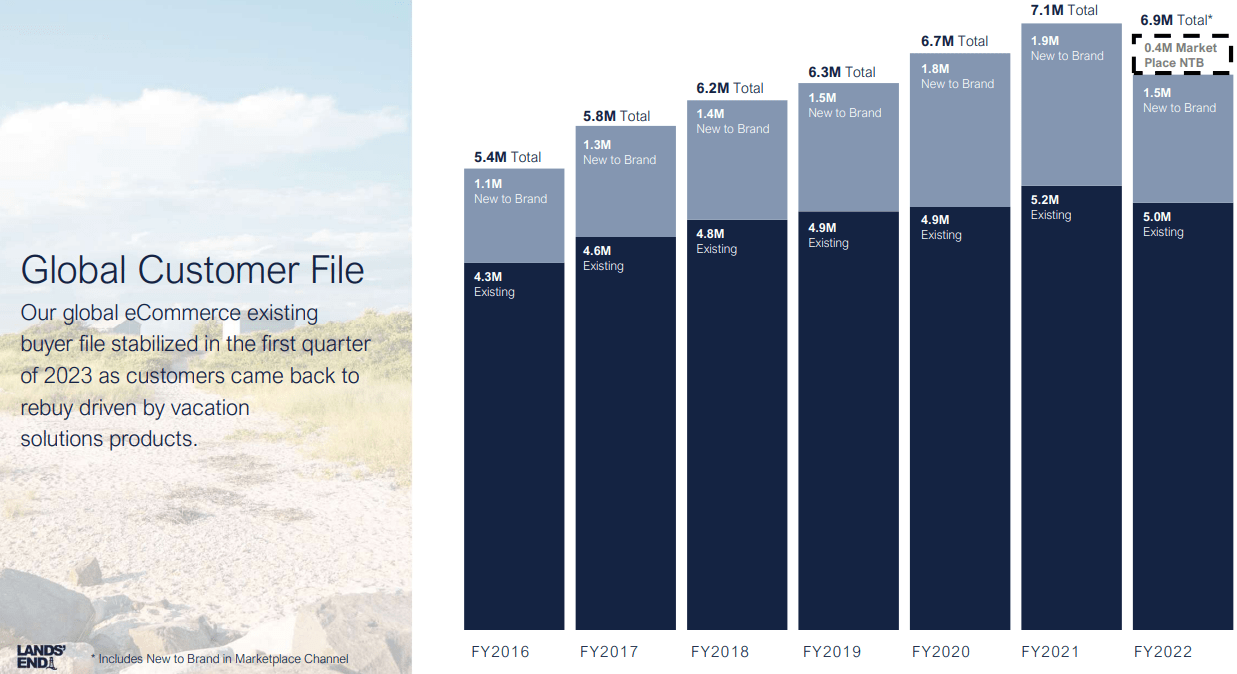

In case you are unfamiliar with the company or my earlier coverage, here's a quick description of the business. Lands' End was founded in 1963, and initially, the idea was to sell sailboat hardware and equipment by catalog. The company moved to clothing and was bought by Sears for $2 billion in 2002. As the latter started to struggle financially in the following year, it spun off the Lands' End's catalog business as a separate listed company in 2014. Today, the business model of Lands' End revolves around an existing buyer file with close to 7 million customers, and over 90% of its sales are made online. In addition, its outfitters segment sells uniform and logo apparel to businesses and to school households.

{kind=link}

Some 80% of existing customers are women, and the average age is close to 60. Lands' End is currently the biggest online retailer in the women's swimwear category in the USA, and the second-largest online retailer in the total swimwear category. The company's product offering also includes coats, bottoms, and school uniforms among others.

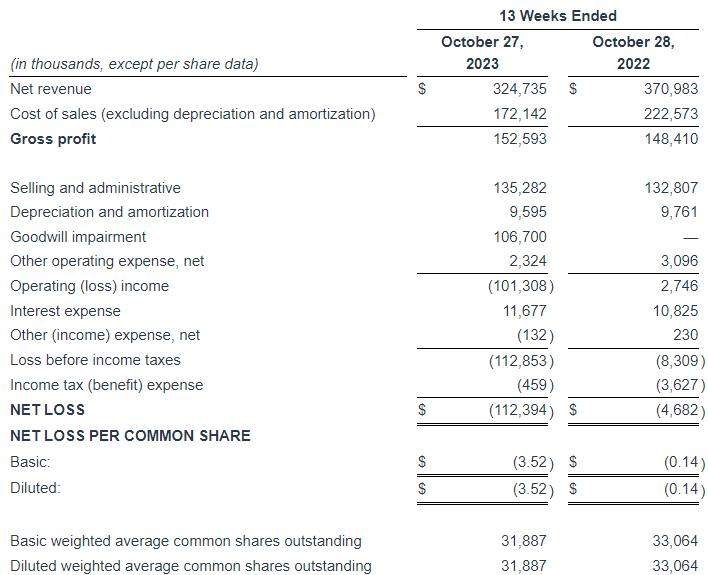

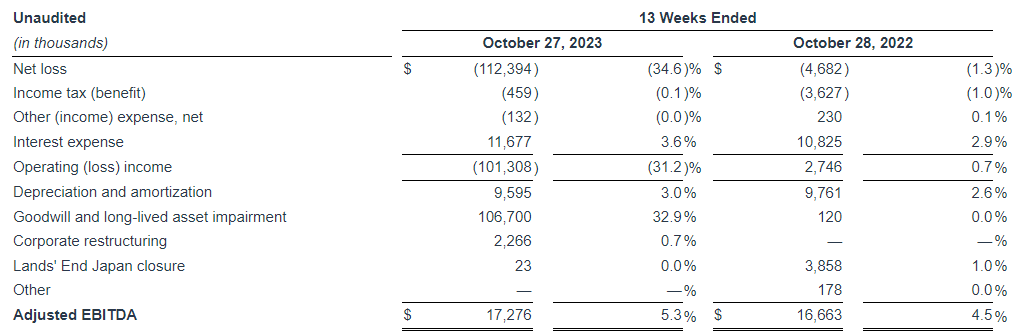

As of October 27, there were just 26 physical stores in the USA (see page 26 here ). The focus on e-commerce boosted the results of Lands' End during the COVID-19 lockdowns, but the company has been struggling to compete with physical clothing stores since the USA reopened. I was expecting Q3 FY23 to be another underwhelming quarter, but I was positively surprised to see the adjusted gross margin grow by 700 basis points year on year and the adjusted EBITDA margin remaining above 5%. While revenues are still falling by double-digit percentages, it seems that cost-cutting measures are paying off as reduced promotional activity and less clearance inventory sales led to a significant improvement in margins. That being said, I find it disappointing that selling and administrative expenses increased by $2.5 million due to higher incentive-related personnel costs. It's worth noting that Lands' End booked about $2.3 million in severance costs under other operating expenses as it decreased its corporate positions, mainly in the Hong Kong sourcing office (see page 21 here ).

{kind=link}

{kind=link}

As you can see from the tables above, there was a $106.7 million goodwill impairment during the quarter and Lands' End said that this was due to the decline of its share price and adverse market and macroeconomic conditions (see page 26 here ).

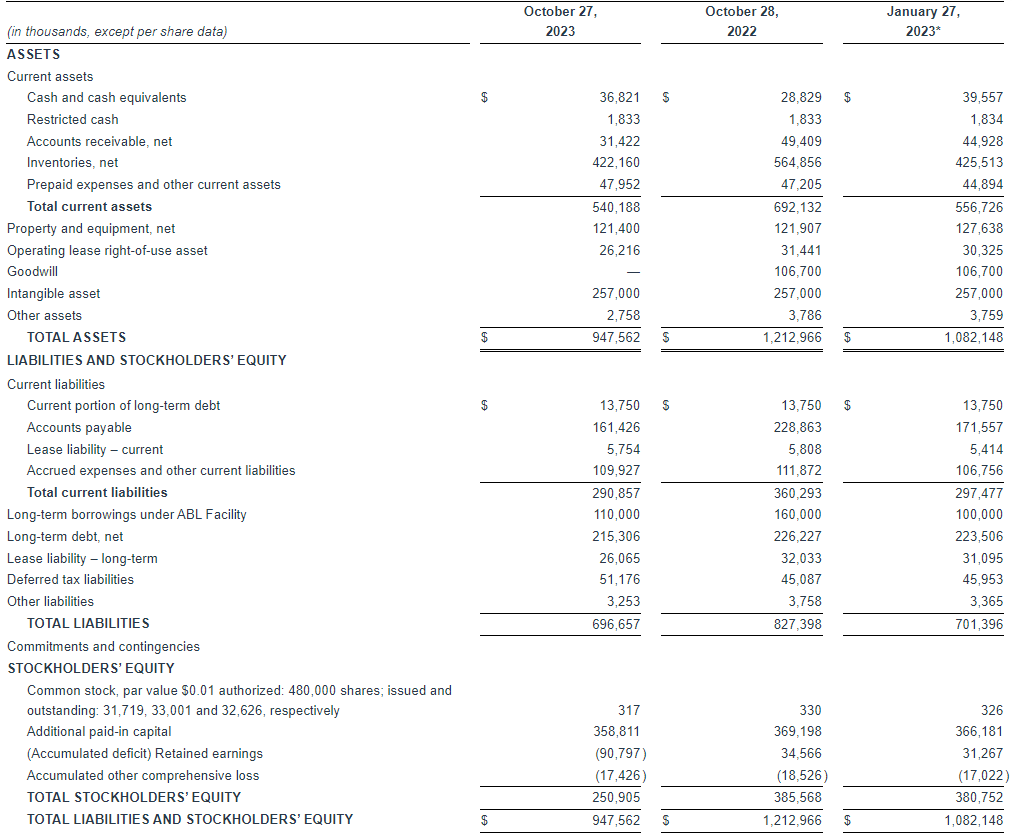

Turning our attention to the balance sheet, Lands' End has been focusing on improving inventory management over the past few quarters and this resulted in a boost to inventory turns as well as a reduction of inventory levels by just over a quarter compared to a year earlier to just above $422 million. Thanks to this, free cash flow for the first nine months of FY23 was $8.1 million. Another positive effect from the reduced inventory is the significant decrease in debt levels - net debt stood at $302.2 million as of October 27, 2023, versus $371.1 million a year earlier.

{kind=link}

Overall, I think this was a strong quarter for Lands' End as cost-cutting measures helped the company improve margins despite the loss of economies of scale. In addition, the balance sheet looks much healthier compared to a year ago thanks to improved inventory management. Looking at what to expect for the future, I'm optimistic that net income could be in positive territory in Q4 FY23 and I think the company's guidance for the quarter looks achievable. Lands' End forecast net income of between $4 million and $7 million for Q4 FY23 as well as adjusted net income of between $8 million and $11 million.

Yet, I think Lands' End still doesn't look cheap despite the positive developments. Even if adjusted EBITDA came at the top of the guidance range of between $27.5 million and $31.5 million for Q4 FY23, that would bring the adjusted EBITDA for the full fiscal year to just $84 million. With an enterprise value of $569.5 million as of the time of writing, this translates into an EV/adjusted EBITDA ratio of 6.8x, which I think is high for an online apparel retailer. Personally, I don't feel comfortable buying shares of a clothing retailer at an EV/EBITDA ratio of over 5x.

Investor Takeaway

In my view, Lands' End booked solid Q3 FY23 results as margins are improving rapidly thanks to cost-cutting measures. The balance sheet has been strengthened, and positive net income seems to be just around the corner. That being said, the company still doesn't look cheap, and I want to see at least two consecutive quarters before I start considering opening a position. I think risk-averse investors should avoid Lands' End stock for the time being.

For further details see:

Lands' End: Solid Q3 2023 Results But Still Not Cheap (Rating Upgrade)