LE - Lands' End: Weak Q2 FY23 Results And A Grim Outlook (Rating Downgrade)

2023-09-13 09:58:05 ET

Summary

- The company’s Q2 FY23 net revenue decreased by 7.9% to $323.3 million, while net loss more than tripled to $8 million.

- Lands' End is struggling with sales growth and an improving EBITDA margin and a lower net debt are being negated by higher interest rates.

- The short borrow fee rate is just 1.12%, but I’m concerned the short interest is 10.29% of the float and it takes over 12 days to cover.

- It could be best for risk-averse investors to avoid this stock.

Introduction

In February, I wrote a bearish article on SA about e-commerce-focused clothing retailer Lands' End (LE), in which I said that profits were being eaten away by interest expenses and that the company was experiencing headwinds as shoppers were returning to physical clothing stores following the end of COVID-19 lockdowns.

In my view, this is a good time to revisit the company, as it released its Q2 FY23 financial results on August 31. I think the results were weak as net revenue went down by 7.9% year-on-year to $323.3 million while net loss more than tripled to $8 million. The outlook for Q3 FY23 doesn't look good either as the net loss is expected to come in at between $4 million and $6.5 million. I'm cutting my rating on the stock to sell, and I think that opening a short position seems viable at the moment. Let's review.

Overview of the Q2 FY23 financial results

If you aren't familiar with the company or my earlier coverage, here's a short description of the business. Lands' End is a clothing retailer focused on the e-commerce segment and is the largest online retailer in the women's swimwear category in the US as well as the second largest online retailer in the total swimwear category in the country. The company was spun-off from Sears back in 2014 and today its business model relies on a global e-commerce existing buyer file with almost 7 million customers, with an average tenure of over 18 years. Also, Lands' End Outfitters corporate and school apparel business partners with some 4,500 schools for creating their uniforms and over 90% of the company's sales come from e-commerce. Lands' End has some 30 physical stores and part of its revenues also come from sales through partners. You could also say that the company has a strong focus on artificial intelligence ((AI)) as 90% of its marketing campaigns are engineered by it (see slide 10 here ).

{kind=link}

Turning our attention to the Q2 FY23 financial results, net revenue decreased by 7.9% to $323.3 million, which was near the low end of the $320 million to $335 million guidance given on June 1. Revenues in the USA inched down by 4.4% due to lower markdown inventory sales while the European business struggled due to assortment editing, reduced markdown inventory sales as well as a challenging macroeconomic environment. Lands' End Japan was closed at the end of FY22.

{kind=link}

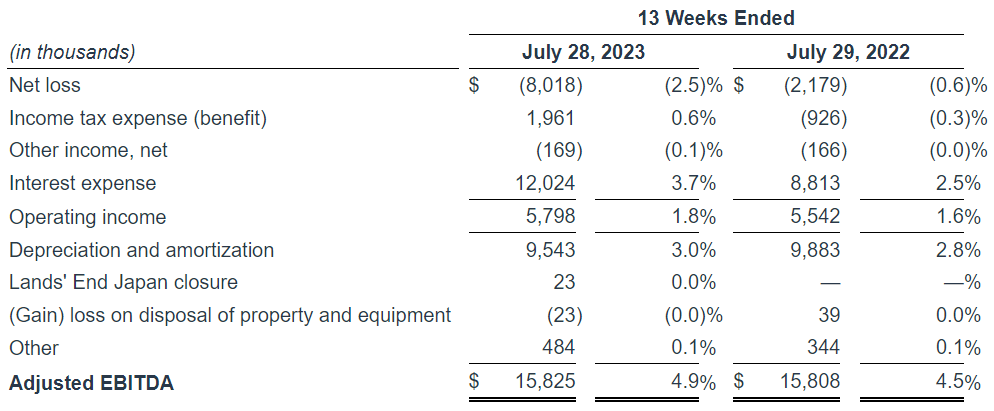

On a positive note, adjusted EBITDA remained unchanged compared to Q2 2022 at $15.8 million mainly thanks to cost-cutting measures but rising interest expenses pushed the net loss to $8 million. This was much higher than the guidance for the quarter, which was for a net loss of $2 million to $4.5 million.

{kind=link}

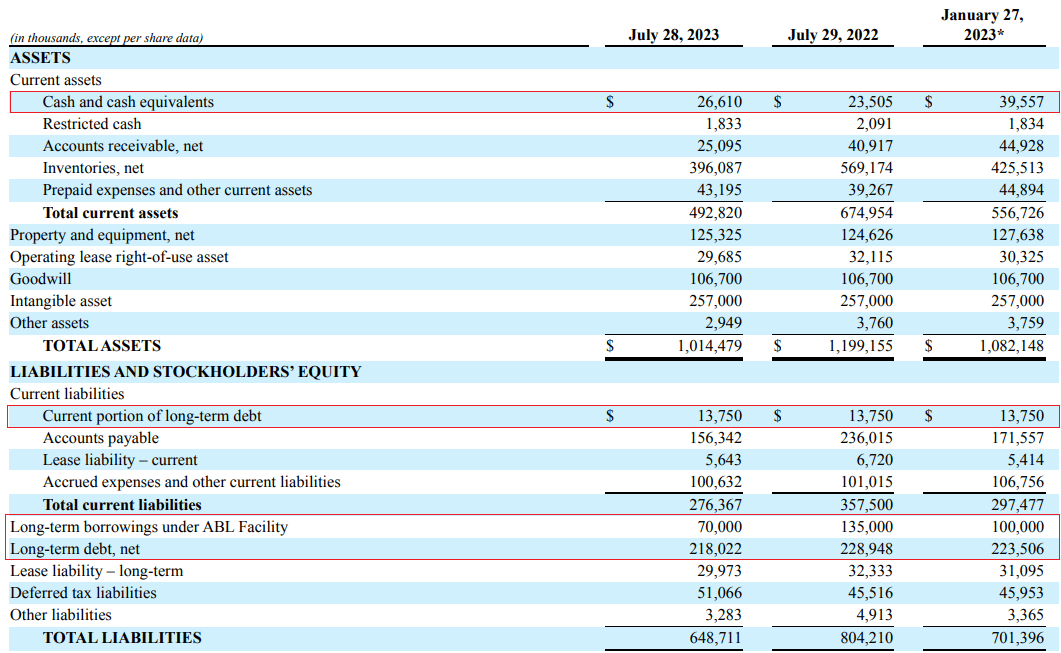

Looking at the balance sheet, Lands' End focus on disciplined inventory management enabled it to reduce inventories by 30.4% year-on-year to $396.1 million as of July 28. The free cash flow for the first half of FY23 was $32 million despite the rising net loss, and the company used the funds to buy back shares for $6.8 million as well as reduce its debt load. As of July 28, the net debt stood at $275.2 million compared with $297.7 million at the end of FY22 and $354.2 million a year earlier.

{kind=link}

While this is certainly a step in the right direction with rising interest rates, I'm concerned that there could be little room left for further inventory reduction and that Lands' End could struggle to get in the black over the next few quarters. Looking at what to expect for the future, the company's guidance for Q3 FY23 includes net revenues of between $340 million and $355 million and a net loss of between $4 million and $6.5 million, and I think the latter could be overly optimistic considering the interest rate on its term loan facility was approaching 15% as of July 28. This is why interest expenses have been increasing despite the lower debt load.

{kind=link}

Overall, I think this was a quarter to forget for Lands' End as the company is struggling to grow revenues in the US in a post-COVID world, Europe is inching closer to a recession while an improving EBITDA margin and a lower net debt are being negated by higher interest rates. I don't expect Lands' End to book a positive net income anytime soon unless the company finds a way to refinance its debts at a lower interest rate. Another possible path to improve the situation is a capital increase. Yet, there is no indication that either of these two options is being considered and the outlook is grim.

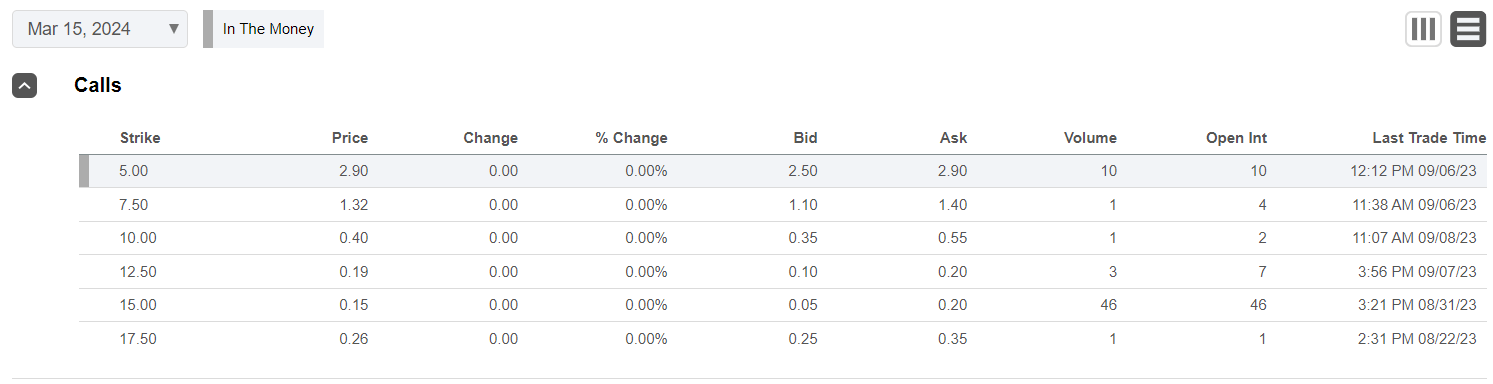

So, how do you play this one? Well, I think that short selling seems viable at the moment as data from Fintel shows the short borrow fee rate stands at just 1.12% as of the time of writing. In addition, the call options here seem relatively cheap. Hedging a short position using options is a popular and straightforward strategy, as explained here .

{kind=link}

That being said, the short squeeze risk could be significant as the short interest is 10.29% of the float and it takes over 12 days to cover. In my view, it could be best for risk-averse investors to avoid this stock.

Looking at the upside risks, it's possible that I'm overly pessimistic about the prospects of Lands' End and the company manages to beat its Q3 FY23 guidance, getting into the black. It's also possible that a debt refinancing deal is in the works and thus interest expenses decrease significantly soon. And as I mentioned, the short interest over 10% of the float, so the stock is a decent candidate for a short squeeze play by one or several institutional investors.

Investor takeaway

Lands' End has improved its margins and reduced its net debt since the last time I covered it but the financial situation of the company seems bleak at the moment. Lands' End is struggling with falling sales while rising interest expenses are eating away at the improved EBITDA margin and I expect net income to remain in the red for the next few quarters. In my view, the stock is a good candidate for short selling due to the low short borrow fee rate and relatively cheap call options. That being said, I'm concerned that the short interest is more than 10% of the float and I think that risk-averse investors should stay away from the stock.

For further details see:

Lands' End: Weak Q2 FY23 Results And A Grim Outlook (Rating Downgrade)