LNTH - Lantheus: Growth Well Priced In Profitability Next Hurdle (Rating Downgrade)

2023-08-30 16:00:30 ET

Summary

- Lantheus Holdings, Inc. stock sold off sharply after Q2 numbers, and is now trading at July '22 range.

- Q2 earnings showed solid growth, but LNTH's economic profitability and market technicals are concerning.

- LNTH divested its RELISTOR royalties, providing extra liquidity but removing future income.

- Net-net, revise to hold.

Investment updates

The equity stock of Lantheus Holdings, Inc. ( LNTH ) sold off sharply after its Q2 numbers, seeing it sell at July '22 range. We've been at these levels before in LNTH—it rallied with authority off its January '23 lows, marched from $48 to $100 by May, where it peaked, and investors likely booked profits in the long account. Since the February publication , I've closed out LNTH positions in the same steed.

The company's Q2 numbers weren't enough to introduce new demand and those holding LNTH inventory in their portfolios are finding it difficult to sell to this market at higher bids. The stock trades at compressed multiples of 11x forward earnings and just 7.3x forward EBITDA as a result. Based on the economic characteristics discussed here today, I'm advocating against buying LNTH based on these 'cheap' multiples alone. The upside risk is that it surprises to the upside in its H2 numbers, but one also has to consider the multitude of selective opportunities trading at attractive prices right now as well. Net-net, I revise LNTH to a hold.

Figure 1.

{kind=link}

Critical factors to revised thesis—Q2 numbers, economic profitability, market technicals

1. Q2 earnings breakdown

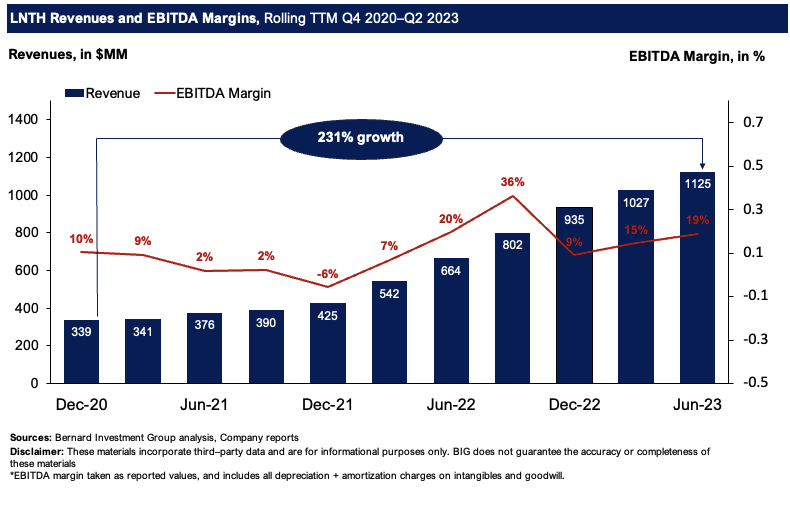

LNTH put up revenues of $322mm for the quarter, up 44% YoY on earnings of $1.54 per share—a 74% YoY gain. It was a solid Q2 for LNTH and the numbers are there to prove it. This continues a long period of growth that begun in 2021 and extended to the present day. Figure 2 shows the rolling revenue clips on TTM basis from 2020–date, along with the reported EBITDA margin. Sales are up 231% over this time, on reported EBITDA margins of 19%.

Figure 2.

{kind=link}

The divisional highlights are as follows:

- Radiopharmaceutical oncology sales pulled to $211mm and were up 610bps YoY. PYLARIFY continues to be the major breadwinner for LNTH. Sales were up 62% YoY to $210mm, backed by sequential growth across its existing accounts and new additions. Beyond the numbers, PYLARIFY's clinical differentiation is a standout in my eyes. It's the only prostate-specific membrane antigen ("PSMA") PET imaging agent to effect substantial changes in patient management for 99% of participants in a critical biochemical recurrence study.

- Its precision diagnostics business posted revenues of $97.6mm, a 12% increase on last year. Noteworthy DEFINITY sales printed $70.5mm, up around 13.2% YoY. Additionally, TechneLite, LNTH's technetium–based radiopharma product, put up $21.6mm in sales and grew 11.1%. Finally, the company also booked ~$13mm in strategic partnerships and other revenue, underscored by contributions from MK-6240 and the RELISTOR royalty.

Figure 3.

{kind=link}

In fact, the RELISTOR royalty forms one of two critical factors that are relevant for LNTH—and investors—going forward. As a reminder, LNTH divested its RELISTOR royalties earlier this month. The tiered and sales-based royalty stream was acquired by HealthCare Royalty partners, and will provide LNTH with cash up front to purchase of the stream of income. Further details regarding the sale of the RELISTOR royalty stream are as follows.

- LNTH has retained the right to receive any future milestone payments and has received an initial cash payment of c.$98mm (pre-tax) in exchange for the royalty stream.

- The transaction will reduce revenues by $13mm in revenue and earnings by ~$0.14/share, management says.

- Whilst it gives LNTH ~$100mm in extra liquidity, there are mixed feelings from this prudent investor on the deal. Indeed, it does give LNTH the opportunity to unlock value today—provided it uses the cash wisely, and invests in high-return projects. But it does remove a fairly decent set of future income. It booked $22mm in royalty revenue in '22, and another $13.2mm in H1 this year, which contributed ~$0.13 in EPS. Hence, time will tell on the outcome of this decision.

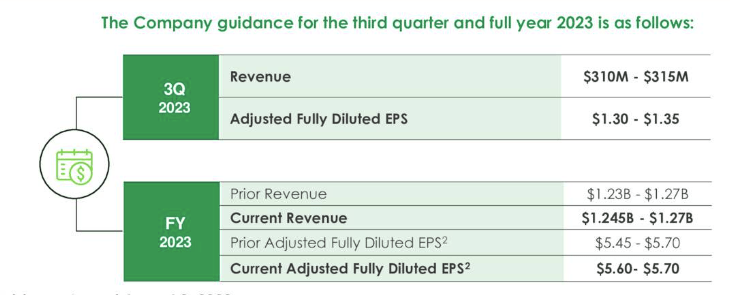

Management updated guidance and expects full-year revenue of $1.245Bn—$1.27Bn, increasing the lower end of range. It bakes in PYLARIFY sales of $835mm—$860mm on this, up from the previous range of $820mm—$860mm.

Figure 4.

{kind=link}

2. Additional economic levers

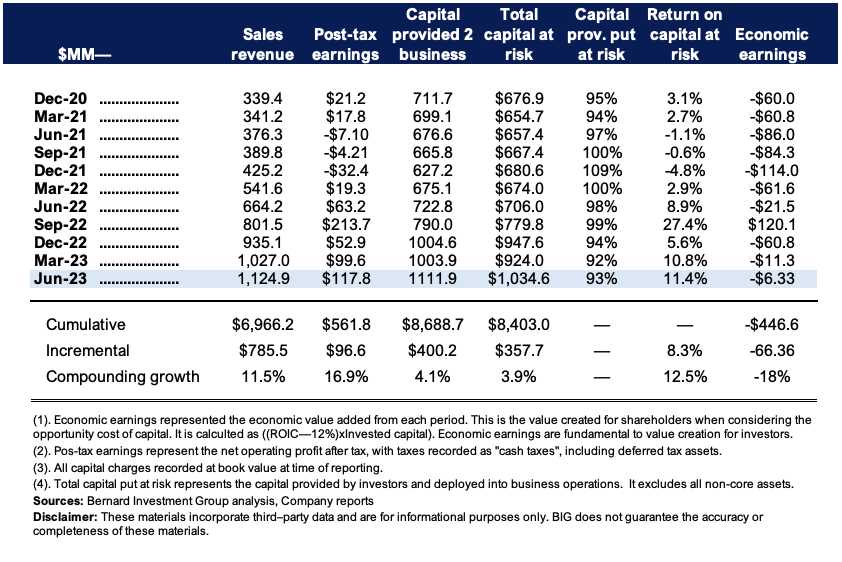

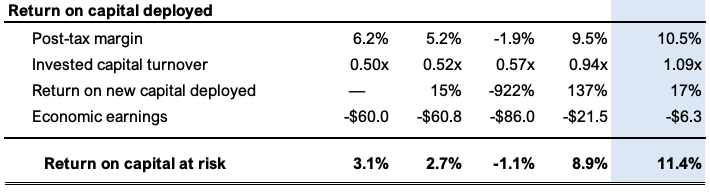

The company's profitability , measured as a percentage of capital infused into its operations, displays a degree of volatility. Figure 5 outlines the flow of sales and earnings after-tax produced on LNTH's capital at risk on a rolling TTM basis. Around 93–95% of the provided money has been effectively deployed, resulting in $117.8mm in after-tax income from an investment of $1.03Bn last period. This translates to an 11.4% return on investment, marking an increase over the preceding two quarters.

These returns remain below our established hurdle rate of 12%, which mirrors long-term market benchmarks (the S&P 500 index). It is not a recent trend either—over the testing period, returns on capital deployed have been mostly below the 12% mark. In order to create value within our portfolios, I'd need to see it doing >the 12% benchmark. Because this threshold has not been exceeded, it's resulted in LNTH throwing off negative economic earnings—those earnings generated on the $1.03Bn of business capital and above the 12% hurdle—are negative, despite the company's reported earnings.

Figure 5.

{kind=link}

Critically, despite the sales growth outlined earlier, there's been no pull-through to margins or capital turnover.

Firms can increase their profitability via these two measures. Figure 6 shows LNTH is lagging on both fronts. Post-tax margins (NOPAT margin) are ~10.5% in the TTM, although up from 5.2% 2 years ago. Capital turnover is at ~1x, having gained from 0.52x in 2021.

The fact both are increasing is commendable. But on absolute terms, they are small. It suggests LNTH enjoys neither consumer nor production advantages to improve its competitive advantage. Ideally, you'd see one of the other at fairly high marks to suggest an ability to compound value—margins >25%, or capital turns at 1.5x+, for example (having both 'high' is exceptionally rare). Hence, I'd need to see LNTH driving any one of these metrics north for it to grow the business sustainably, without relying on external capital to finance growth.

Figure 6.

{kind=link}

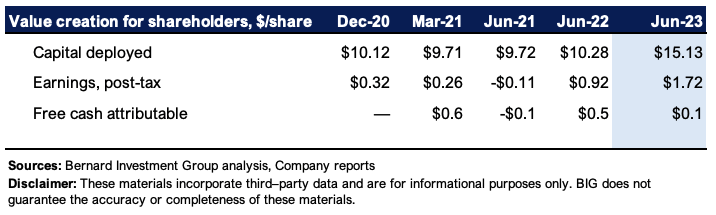

Figure 7. Note: Figure 7 consolidates the economic data into a per-share basis. $15.13/share of capital deployed produced $1.72/share in NOPAT last period on a TTM basis. Both figures are up, but it took $5/share to grow earnings $0.8/share, 16% return on incremental investment.

{kind=link}

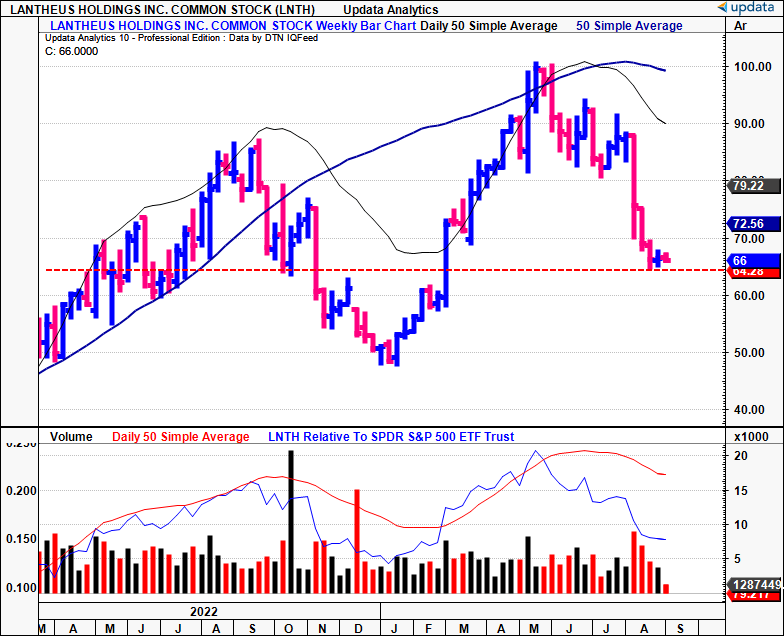

3. Technical take

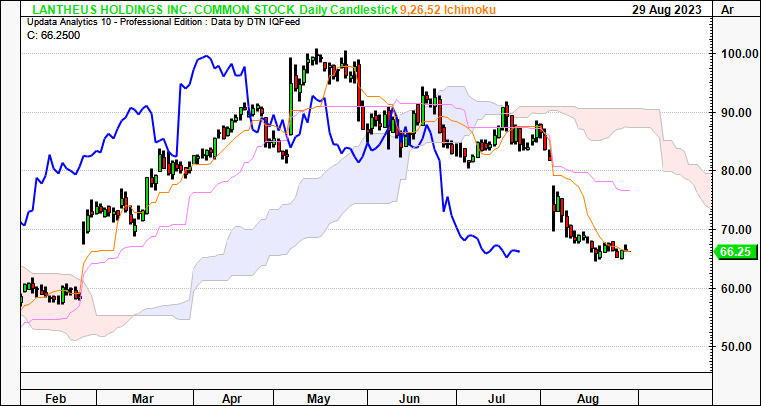

Price structure has broken down for LNTH these past two months.

The daily cloud chart shows this well, in Figure 8. Both price and lagging lines broke the cloud this month, and gapped to the downside. There's considerable distance from the cloud to both lines. The further the break lower, paradoxically, the more likely it will enter the cloud and potentially catch a bid.

But we look to be a ways off from this. You'd be looking to a move to $72.00/share by end of September to suggest it could turn off its lows. The daily chart looks to the coming weeks, and we see this mark on the chart.

Figure 8.

{kind=link}

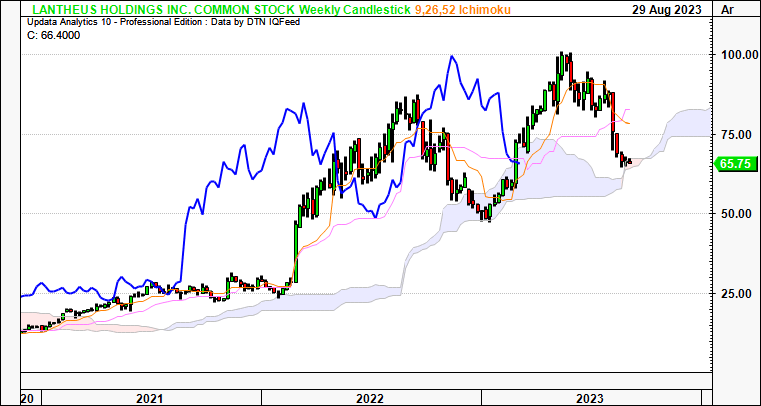

The weekly isn't much more constructive. Notice the breakdown in structure, coming off highs at pace. The price and lagging lines both now test the cloud top. A break lower would certainly see both trade below the cloud.

If that were to be the case, the bullish outlook for LNTH's equity stock would be muted over the coming months in my view. Weekly charts look out to the months ahead. The $72–$74.00 mark appears here as well as key psychological zones. You'd need this by December on the weekly to indicate a bullish reversal. To me, these charts support a neutral view.

Figure 9.

{kind=link}

Price targets have therefore formed to the downside on the point and figure studies below. P&F charts remove the intra-trend volatilities, so we get a clean eye on the validity of each directional move.

You'll note these studies have eyed the move off $100, LNTH's double-top in May this year. They have caught each of the legs down, adding weight to their validity. The next target is to $59.50. A break lower would almost certainly activate this target. I'm looking to this zone as the next objective, cognizant it is a divergence from the $72–$74 marks outlined earlier. Again, this supports a neutral view.

Figure 10.

Data: Updata

Valuation and conclusion

The stock sells at 11.7x forward earnings and just 7.3x forward EBITDA. These are incredibly cheap—41% and 44% discounts to the sector, respectively.

The question is—why the discount?

Here's where the profits earned on capital deployed comes to bite LNTH's corporate value in my opinion. The company trades at 8.2x book value. Normally, I'd be intrigued on this, as it implies the market values its net assets highly.

A more pragmatic view is needed though. LNTH trades at just 4.5x EV/invested capital—still potentially attractive, but well off the former multiple. I'd be looking for a high EV/IC—anything above 1–2 is great, in fact. It implies the market expects plenty of growth off a firm's capital investments. But again, more thoughtful analysis is needed.

Without the profits produced off the cash invested, this is less meaningful. The ratio of ROIC to the 12% hurdle is 0.95x, otherwise, not accretive to value. You'd need >1 to imply any sort of economic profitability. The discrepancy in EV/IC to ROIC/12% of 4.8x implies expected growth rates have been priced into LNTH's equity stock, and then some. A figure of 1 or less is more attractive, implying the potential growth hasn't been fully priced in. Hence, the growth projections outlined by management appear richly priced in LNTH in my opinion.

For reference, LNTH would need to be pushing 55% trailing return on capital at risk to see it's future growth fairly priced at its current market value (0.55/0.12 : 4,720/1,034 = 1.0x).

Figure 11.

BIG Insights

In short, LNTH caught a tremendous bid cross 2022—'23, providing shareholders with excellent gains on equity investment. Superb earnings throughout early '23 supported this view, backed by a fantastic growth outlook. The issue though, it appears this, and the mid-term growth in LNTH's arsenal appears priced in as I write. We looked at the firm's economic characteristics in a different light, and noted potential headwinds 1) in capital intensity and 2) growth at the margin. With $1.72/share in earnings produced on $15.13/share of capital at risk I'd like to see this stretch up before coming involved again. Net-net, reiterate hold.

For further details see:

Lantheus: Growth Well Priced In, Profitability Next Hurdle (Rating Downgrade)