LTMAQ - LATAM Airlines Has 95% Downside

- It would be wise, in my view, to sell LATAM airlines as soon as possible.

- The airline emerged from Chp 11 on July 5th, 2022 with a reorganization plan that grants controlling shareholders the right to acquire 99.9% of the company at US$0.02.

- At the current stock price and on full diluted shares, the market cap is US$166bn, more than the combined value of all the airlines in the US.

- This price distortion is not likely to last forever.

LATAM emerges from Chapter 11

LATAM Airlines ( LTMAQ ) emerged from Chapter 11 on July 5th after a 6-month legal battle in NY courts. Unfortunately, the reorganization plan includes US$10.3bn in new equity with a 99.9% share dilution that should drive the share price to US$0.02 from the current US$0.27.

The reorganization plan calls for an US$800m capital increase at US$0.017 per share or 73.8bn new shares. It also allows the three main shareholders, the Cueto family, Qatar Airways and Delta ( DAL ) to acquire convertible bonds for US$9.5bn at a strike price of US$.012 or 532bn new shares. On a fully diluted basis, the capital increase and debt for equity swap increase total shares to 616bn from 606m a 99.9% share dilution. The three convertible bonds are for different amounts, but all lose 50% of their share swap ratio if not converted within 60 days of issue. This means the share dilution should occur soon.

The share price does not reflect share dilution

The funny, sad and perplexing thing is that the share price is still incredibly overvalued post reorganization approval. It has declined from US$.33 to US$.27, but still not near the US$0.02 it should be. Speaking with several local Chilean brokers and even retail shareholders, it seems that most are yet unaware of the massive share dilution. Others do not want to sell given the 80%+ losses already inflicted in many cases. At the current share price and with fully diluted share outstanding, the market cap is US$166bn!

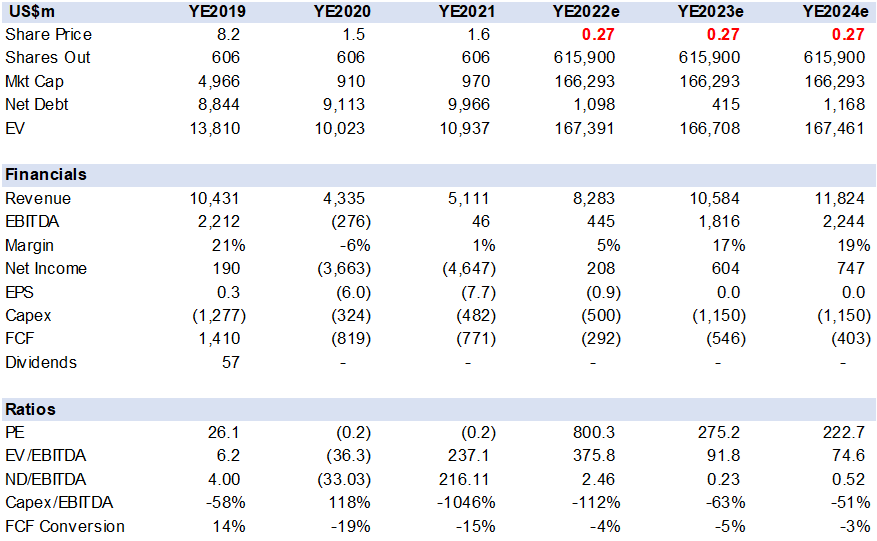

LATAM Financial and Valuation Summary (Created by author with data from Capital IQ and LATAM)

{kind=link}

The table above highlights the impact that the pandemic had on LATAM with over US$8bn in losses during 2020 and 2021. The company entered Chapter 11 protection in May 2020. Consensus estimates and company guidance point to a full recuperation by YE24. On the positive side, operations are leaner after 2yrs of crisis cost management while the airline emerges virtually debt-free.

However, the airline operating model carries significant risk given its high fixed cost component. An emerging market airline has an even greater margin risk on currency mismatch. I estimate that 80% of opex is in USD, that includes debt, leases, fuel, maintenance, ground and in-flight services. While USD originated revenue is the inverse, around 20%. The passenger base is predominantly in Latin America (Brazil, Chile, Peru, Colombia and Argentina). This means that customer purchasing power is in a local currency. FX devaluation cuts into passenger demand, especially the leisure segment, which is 60% of RPK (revenue passenger kilometers). Thus, airline margins are highly macro sensitive. Competition from ultra-low-cost airlines and other legacy carriers on outbound traffic caps airfare pricing maneuverability. The Delta JV/code share is positive on long-distance routs to US.

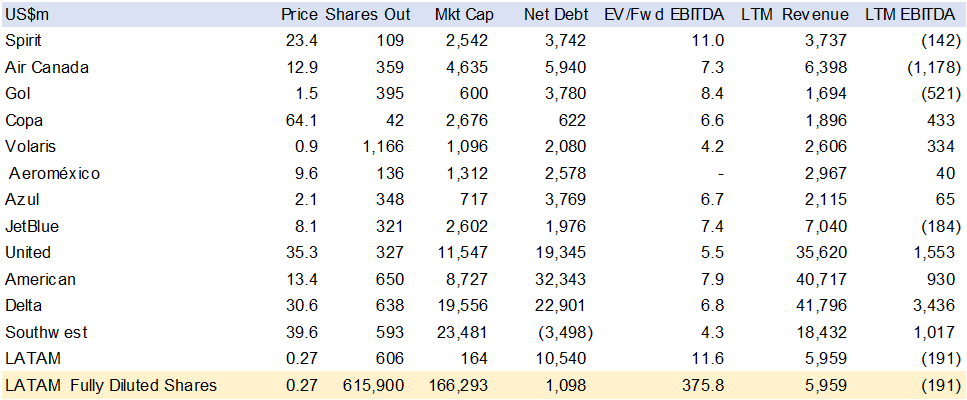

Peer comparison highlights price distortion

Looking at peers in Latina America and the US market, it becomes evident that LATAM's massive share dilution is not priced. Average EV/EBITDA for the sector is around 7x. Southwest ( LUV ) is the highest valued airline at 11.6x EV/EBITDA with a US$23.4bn market cap vs LATAM US$166bn on fully diluted shares. Note that the debt reduction does come close to offsetting the share dilution. The price set by shareholder in the capital increase and the convertible bond swap destroy minorities.

Peer Comps in US and Latam airline sector (Created by author with data from Capital IQ and LATAM)

{kind=link}

At what price is LATAM reasonably valued?

Once and if LATAM's share price reflects this share dilution and declines to US$0.02 the shares would trade at 7x EV/EBITDA on YE23 consensus estimates, a far more reasonable valuation in my view.

LATAM valuation at US$0.02 a share (Created by author with data from Capital IQ and LATAM)

Conclusion

In summary, the current share price of LATAM does not factor in massive share dilution and should decline 95% in the short term. If/when the shares price in this dilution, at US$0.02, the valuation approaches fair value multiples on YE24 estimates. However, it's likely the shares may never recuperate above today's share price levels.

For further details see:

LATAM Airlines Has 95% Downside