LSCC - Lattice Semiconductor: High-Quality Business But Valuation Is Too Generous

2023-09-04 03:03:54 ET

Summary

- Lattice Semiconductor is a high-quality business with consistent revenue growth and strong profitability metrics.

- LSCC has a solid balance sheet and consistently repurchases its own stocks.

- The valuation is too generous, and the company's substantial exposure to international markets poses a risk in current geopolitical tensions.

Investment thesis

Lattice Semiconductor ( LSCC ) is a no doubt high-quality business. I like the company's focus on innovation, which enables it to deliver consistent revenue growth and demonstrate top-cohort profitability metrics. The balance sheet is solid, and the company consistently repurchases its own stocks as well. But the valuation looks way too generous. I also consider the company's substantial exposure to international markets as a massive risk in the current geopolitical tensions between the developed and the developing worlds. All in all, I assign Lattice a "Hold" rating.

Company information

Lattice Semiconductor Corporation and its subsidiaries develop technologies related to programmable logic semiconductor products, system solutions, design services, and licenses.

The company's fiscal year ends on December 31 with a sole operating segment. LSCC disaggregates revenue by end markets. According to the latest 10-K report , the company generated 70% of its sales in Asia.

LSCC's latest 10-K report

Financials

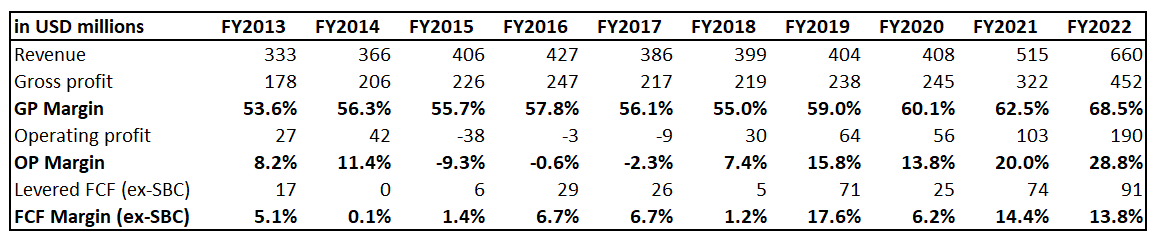

Lattice has demonstrated impressive financial performance over the past decade. Revenue compounded at an 8% CAGR, which is solid considering the ten-year horizon. As the business scaled up, profitability metrics have improved significantly. It is a good sign because expanding margins suggest that the management has been efficient in driving growth, and investors can expect further profitability metrics improvement if the business grows further. In recent years, the free cash flow [FCF] margin has gone double digits even with stock-based compensation [SBC] deducted.

{kind=link}

The company reinvests substantial sales in innovation, which is a good sign for long-term investors. Lattice's R&D to revenue ratio has been consistently above 20% over the past decade, which is massive. The management's commitment to innovation means it strives to widen the company's technological moat and build sustainable shareholder value. Overall, I like the company's capital allocation balancing between reinvesting in innovation, stock buybacks, and maintaining a healthy balance sheet. The company has a meager leverage ratio and is in a solid net cash position. Liquidity metrics are also in excellent shape.

Seeking Alpha

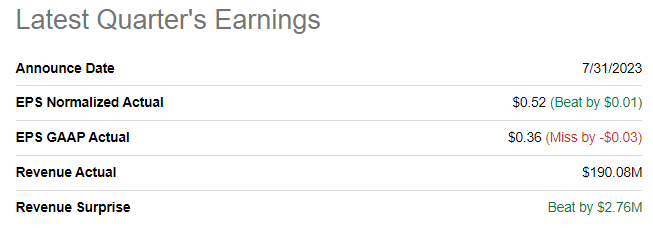

The current growth momentum is strong. The company delivered YoY double-digit revenue growth in ten straight quarters, which is quite impressive in the challenging environment we have been experiencing since the beginning of 2022. The latest quarterly earnings were released on July 31, when the company topped consensus revenue and the adjusted EPS estimates. Revenue demonstrated a solid 17.8% YoY growth, and the adjusted EPS expanded notably from $0.42 to $0.52.

{kind=link}

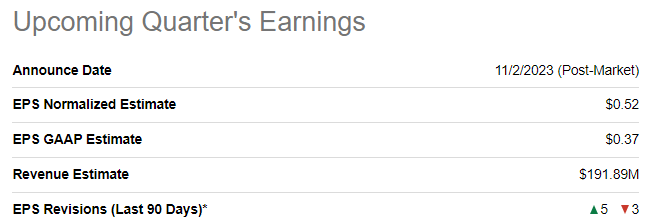

The upcoming quarter's earnings are scheduled to be released on November 2. Revenue growth is expected by consensus to decelerate substantially, though it is forecasted to demonstrate a solid 11% YoY growth. The adjusted EPS is expected to be flat sequentially at $0.52.

{kind=link}

Now, let me share my thoughts from the big-picture perspective. First, let me start with the positive points. I like the company's focus on innovation. I firmly believe that the most innovative companies win over the long term, and Lattice's substantial R&D to revenue ratio says a lot to me. As a result of the company's innovative approach, it has built a solid portfolio of offerings aimed at diverse end markets. This diversification protects the company from the vulnerability to economic cycles and differentiates the company from competitors.

{kind=link}

I also like the company's stable and strong profitability metrics. The ability to charge premium prices on its offerings is also thanks to the company's cutting-edge technologies, which are standing out due to substantial investments in innovation. Seeking Alpha Quant assigns the company an "A" profitability grade, meaning Lattice is in the top cohort of the semiconductor industry from the profitability ratios perspective.

From the "cons" perspective, I see the company as relatively small-scale. The company was founded forty years ago, in 1983, and has not reached $1 billion in annual sales yet, despite its massive investments in R&D. That said, the company competes directly and indirectly with semiconductor giants, which possess much greater resources and can invest in innovation much larger resources, in absolute terms.

Valuation

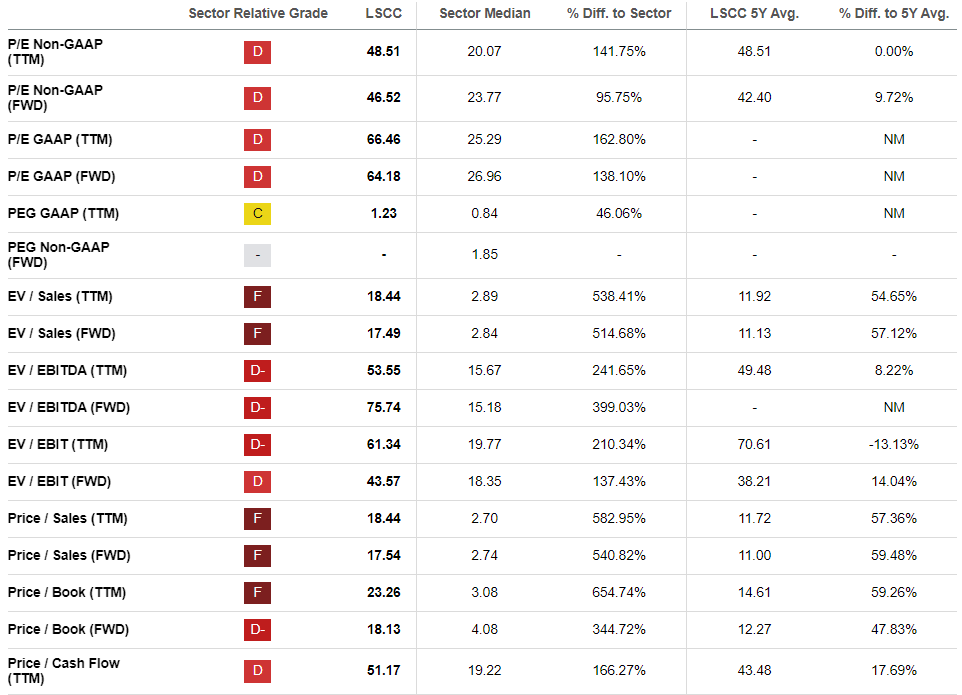

The stock rallied 51% year-to-date, significantly outperforming the broader U.S. market. Seeking Alpha Quant assigns the stock the lowest possible "F" valuation grade due to its multiples, which are substantially higher than the sector median and are mostly higher than historical averages. That said, from the valuation ratios perspective, the stock looks significantly overvalued.

{kind=link}

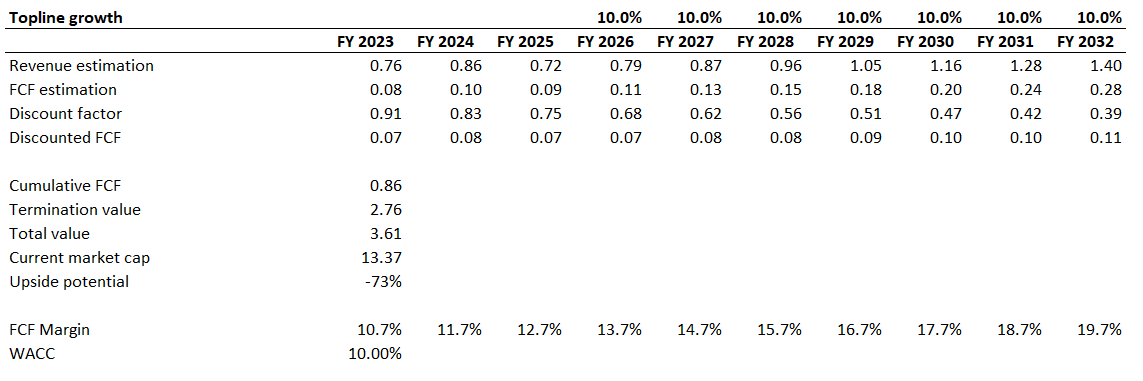

Let me move on to the discounted cash flow [DCF] simulation. I use a 10% WACC for discounting. I have revenue consensus estimates for the three upcoming fiscal years and project a 10% revenue CAGR for the years beyond. I use the last five years' average for the FCF margin, which is at 10.7%. I expect it to expand by one percentage point yearly.

{kind=link}

According to my calculations, the stock is about threefold overvalued. The business's fair value is $3.6 billion, much lower than the current $13.4 billion market cap. LSCC's net cash position would not help much to improve the company's fair value. That said, the stock is massively overvalued.

Risks to consider

According to the company's financial statements, it generates only 14% of its sales in the United States. That said, the company faces significant risks related to international trade. The most apparent risk is the foreign exchange risk. Unfavorable fluctuations in the foreign exchange market are highly likely to affect the company's earnings adversely. Relying heavily on international trade also means that there is a risk that changes in international trade regulations, rules, and tariffs might disrupt the company's operations and earnings.

In FY 2022, the company generated 45% of its total revenue in China. In the current environment of escalated geopolitical tensions between the U.S. and China, LSCC faces significant risks. Several American semiconductor companies were restricted from selling some of their products in China. That could also be a big problem for Lattice, given the extensive exposure of sales in China.

Bottom line

I like the company's fundamentals, but I am not ready to buy at the current stock price. LSCC definitely deserves to be on long-term investors' watchlists, but the current stock price is far above the fair value, even considering the company's strong market position and stellar profitability. Risks related to international trade, and especially trade with China, are substantial. To conclude, I assign the stock a "Hold" rating.

For further details see:

Lattice Semiconductor: High-Quality Business But Valuation Is Too Generous