LAUR - Laureate Education: Not A Value Buy

2023-09-18 09:28:28 ET

Summary

- Laureate Education provides an opportunity for an education play in growing emerging markets of Mexico and Peru.

- While the company raised its guidance for the year, it missed estimates, and we are concerned on the margin profile for H2, which implies sequential deterioration.

- The uncertain macro environment and increasing competition in online education provides limited visibility in the near term.

- We initiate at Hold as the current multiple provides limited margin of safety.

Investment Thesis

Laureate Education ( LAUR ) provides an opportunity into an emerging market play with a large market and improving participation rates in Higher Education, particularly in Mexico. It has emerged leaner within the COVID era, having sold its Australia and New Zealand operations due to increasing competitive landscape as well as its Brazil operations as it struggled with shutting down of the colleges. The shares are up 20% on the back of an improving operational profile reflected in the recent results, benefiting from its strong double digit primary intake in Mexico last fall, however, still falling short of the consensus estimates in recent quarters. While the company reported margin expansion, part of it was a result of the timing expenses, which would have otherwise lead to a contraction in EBITDA margins on a consolidated basis. We expect the return to campus will continue to squeeze margins and an increasingly uncertain macro environment provides limited visibility on the enrollment in the near to medium term. With shares trading at a slight premium to its peers and limited potential for rerating or an outsized potential for growth, we initiate at Hold, however, we will closely watch the primary enrollment figures in Q3 in Mexico.

Company Background

LAUR is a leading education institution operating 5 higher education universities in Mexico and Peru. It offers a wide range of undergraduate and graduate degrees through campus-based, online as well as hybrid programs across business management, STEM, medicine and health sciences, art and others with an enrollment of about 400,000 students.

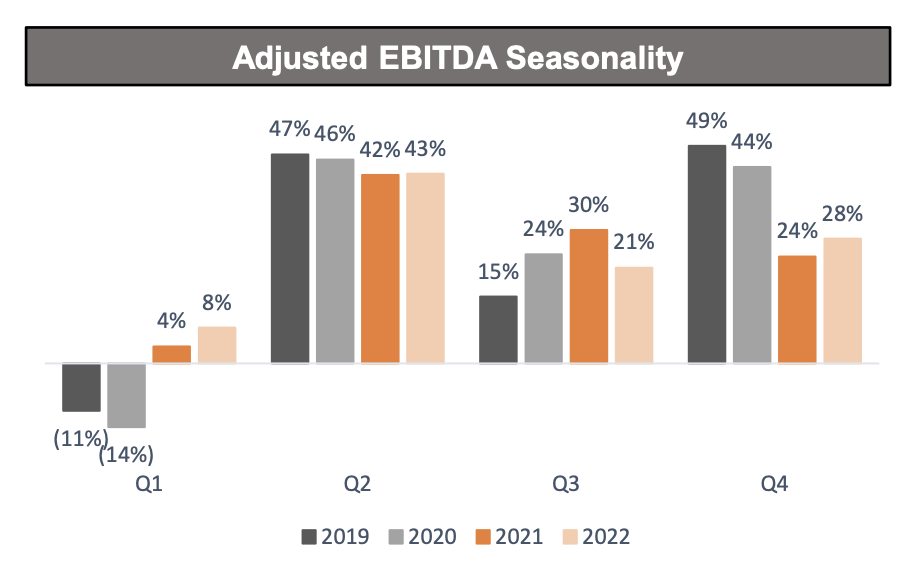

Mixed Earnings

LAUR reported mixed set of earnings in Q2 with total enrollment growth of 9% while new enrollment growth were flat as second quarter is not a large intake period. The new enrollment was driven by strong secondary intake in Mexico across all brands, while total enrollment growth was driven by strong primary intake, along with double-digit enrollment growth in Peru across all brands. It reported revenue growth of 20% YoY (14% on a constant currency basis) implying 5% price mix. Adj. EBITDA margin expanded 57 bps, primarily driven by revenue growth and productivity gains partially offset by return to campus costs as well as timing differences. The margin expansion was driven by a substantial 630 bps uptick in Mexico driven by productivity gains while also timing difference in certain costs which were to be phased in H2. EBITDA margins in Peru declined 247 bps as a result of an increase in return to campus costs. This implies that the EBITDA margin would have contracted on an organic basis, excluding any timing differences.

With Q2 being the largest contributor to the full year EBITDA as a result of achieving the benefits of ramp up happening in Q3, we are a bit concerned on the margin profile going forward which likely hinges on the enrollment figures in Mexico in Q3 which also laps tough comp (17% enrollment growth last year)

{kind=link}

In all, the company reported an EPS of $0.35 significantly missing the estimates with the company having missed estimates several times in the past few quarters.

EPS Beats and Misses

{kind=link}

Balance sheet position remains stable with the company ending up with cash and cash equivalent of $112 mn and total debt outstanding of $210 mn providing required flexibility for its capital allocation priorities.

Management increased FY23 guidance which remains a key positive and now expects revenue of $1,489 mn (vs $1,420 mn previously) and Adj. EBITDA of $423 mn (vs $403 mn previously) at mid point, still implying a 170 bps sequential deterioration in the margin. We believe the enrollment figures in Mexico might not be significant as it laps tough comps (17% enrollment growth last year), rising education costs amidst an uncertain macro environment and competition from value for money skills ready diplomas and courses from several traditional and ed tech companies.

Education CPI for Mexico

{kind=link}

Valuation

LAUR trades at 17x Forward P/E, at a slight premium to its peers. We believe while the company has done well emerging from the COVID with a leaner and focused portfolio paring its debt, strengthening its balance sheet and transitioning to online and hybrid presence. We are positive on Mexico and Peru's long term economy and increasing participation rates in higher education. However, we believe the current uncertain macro environment along with increasing competitive intensity within online and hybrid programs provides limited visibility in the near term. Initiate at Hold.

Risks to Rating

1) Its operations in Mexico and Peru predominantly is exposed to significant macro and political risks with varying degrees of GDP growth which can significantly impact enrollment

2) Unemployment rate is expected to improve in Peru and decline in Mexico and any significant change in unemployment rates can have an impact on the enrollment rates

3) Its inability to transition to changing demands providing courses requisite for the job market can lead to significantly affect enrollment

4) Increasing competitive intensity within the online education market from traditional and Ed tech players can have a sizeable impact on its enrollment figures

4) Enrollment in Mexico begins in Q3 and any significant change in new enrollments can have a sizeable impact on the overall growth profile

Summary

Laureate Education has been challenged in the last few years, as the onset of COVID led to colleges shutting down while it looked to boost its online presence. It has raised its guidance for the year driven by strong enrollment growth in Q1 and stable follow through in Q2, however, rising return to office costs has likely led to a squeeze on EBITDA margins, and we believe given the company does not pay any dividend, there could be limited price appreciation at the current levels as the valuation remains at a slight premium providing limited margin of safety.

For further details see:

Laureate Education: Not A Value Buy