LAZY - Lazydays Holdings: An Uncertain Future

2023-11-27 02:55:31 ET

Summary

- Lazydays produces and sells recreational vehicles in the US with a strategy focused on dealership acquisitions expanding the company's network.

- The company's financials have been volatile due to the impact of the Covid pandemic, reflected in the turbulent stock price.

- The financial history doesn't indicate a clear sustainable margin level for Lazydays, making the investment case quite volatile and uncertain.

- At the moment, I see the stock price as reflective of a baseline earnings level, constituting a hold rating.

Lazydays Holdings ( LAZY ) produces and sells recreational vehicles in the United States. The company’s strategy revolves around acquisitions in the modestly growing RV industry. Due to a market that was largely boosted by the Covid pandemic, Lazydays’ financials have fluctuated significantly in past years, reflected in the turbulent stock price. After Lazydays merged with a SPAC called Andina Acquisition in 2017, the stock price has had a varied widely – since, the stock price has fluctuated between a low of $1.55 and a high of $25.74, currently being far from the highs but well above the low:

Stock Chart From SPAC Merger (Seeking Alpha)

A Quick Look at Lazydays & The Industry

Lazydays manufactures and sells recreational vehicles in the United States. In addition, the company provides financing, insurance, servicing, and parts for the sold vehicles. In Q3, the segments had the following contributions to revenues and gross profit:

Lazydays October Investor Presentation

The RV market as a whole is quite stable in the long-term, and has achieved a modest amount of growth in recent decades. From 1980 to 2022, the estimated CAGR in RV-owning households has been 2.1%, providing Lazydays with slight room for potential growth. The stable increases were disturbed by the pandemic into faster-than-average growth, resulting in a very good amount of growth in the industry’s sales in 2020 and 2021. From 2011 to 2017, the CAGR in RV-owning households was 2.0%, and from 2017 to 2022 the CAGR was significantly higher at 3.5%:

Lazydays October Investor Presentation

Strategy of Acquisitions and Investments - A Need For a Pause?

Lazydays’ strategy revolves around acquisitions improving the company’s nationwide footprint. So far in 2023, the company has acquired three dealerships – one in Nevada in Las Vegas, one in Tennessee , and one in Colorado . The acquisitions create economies of scale for Lazydays as the company integrates its already extensive network into the previously inefficient dealerships. In addition, Lazydays has expansion plans through organic investments – the company is constructing three dealerships as told in the company’s October presentation , with three additional ones that have recently finished construction and have opened. The strategy seems sound, as acquired dealerships seem to be bought for attractive valuations compared to their earnings capabilities under Lazydays’ management typical to consolidators in any industry.

The current investments should be able to grow the company's top line considerably when finished. Further acquisitions in the medium-term are currently quite uncertain due to Lazydays' leveraged balance sheet and poor current earnings, though; I would expect Lazydays' management to first stabilize operations, and only consider significant growth investments as earnings improve. The management seems to be in line with my expectation as per their recent earnings calls' communications.

Financials - Future Margins at Question

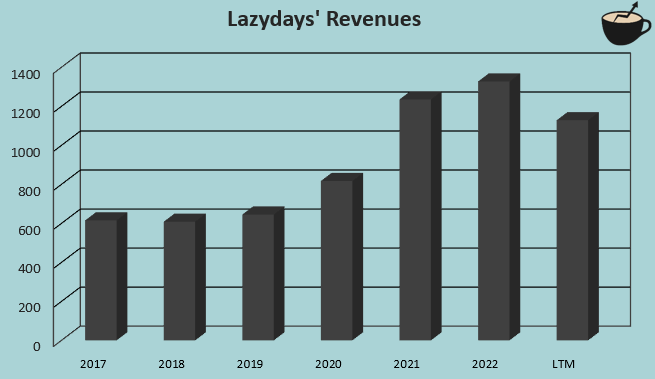

As a result of the acquisitions, Lazydays has achieved some growth. From 2017 to current trailing figures, the company’s revenue CAGR is 11.1% . I believe that Lazydays’ organic performance is quite stable when excluding the pandemic’s effects, and should be mostly in line with inflation in the long term.

Author's Calculation Using Seeking Alpha Data

{kind=link}

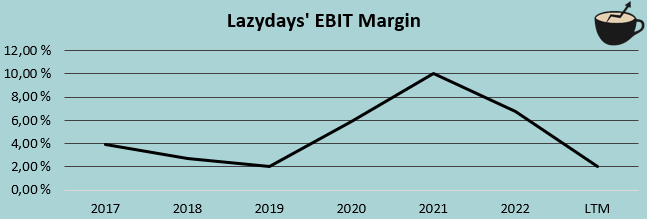

Lazydays’ revenue performance should be mostly predictable on a long-term basis, but the same can’t really be said for the company’s margins – from 2017 to trailing figures, Lazydays’ EBIT margin has varied widely between single-digit figures:

Author's Calculation Using Seeking Alpha Data

{kind=link}

With a current trailing figure of 2.1% as an EBIT margin, Lazydays’ performance doesn’t seem too impressive. The current margin is seemingly a result of a pandemic hangover in demand, and a more challenging macroeconomic situation that has resulted in decreasing sales and deteriorating margins – the 2.1% shouldn’t represent the company’s long-term margin very well as it is caused by current headwinds. A more representative margin is largely at question – the higher 2020-2022 margins don’t necessarily represent a fair estimate either as they were achieved in a favorable market.

Concerning margins, the finance & insurance segment is very valuable for Lazydays. Although the revenues for the segment are very low, the segment contributes very significantly to Lazydays’ bottom line as costs are minimal in the segment. Lazydays has efforts to increase the attachment of finance & insurance services to the sold vehicles, as the segment is still currently performing poorly - in Q3, finance & insurance revenues decreased by 19.7% . As interest rates are rising, offering financing is becoming more expensive for Lazydays as well as the customer. Customers will prefer to pay in cash as the financing option becomes worse. Also, the current base of RV financing has higher costs to finance. As interest rates have begun declining after a peak in October, I believe that a recovery in the segment is imminent, improving Lazydays' margins considerably - investors should keep an eye on interest rates, as they affect Lazydays' performance greatly.

Although not a perfect match in terms of a sales mix and overall offering, a look into Camping World Holdings' ( CWH ), Lazydays' significant competitor's, margins seems advantageous. From 2013 to 2022, Camping World has achieved an average EBIT margin of 7.5% with a current trailing margin of 4.9% - a recovery into historical levels for Camping World would increase the EBIT margin by 2.7 percentage points. For Lazydays, a similar margin expansion would correspond to a long-term EBIT margin of 4.8%. This estimate is a very rough value, though - for one, Lazydays' recent acquisitions likely still contribute negatively to margins compared to a long-term level of operations. Secondly, if Lazydays' improvement in financing earnings proves worthy with declining interest rates, the margin could have better leverage than the figure estimates - as a baseline scenario, I believe the estimate of 4.8% is slightly pessimistic, but provides context to an achievable level.

A good financial performance is crucial for Lazydays. The company currently has interest-bearing debts totaling $503 million, of which the majority is in short-term borrowings. The amount seems excessive compared to Lazydays' diluted market capitalization of $115 million. In addition, the interest expenses exceed Lazydays' achieved operating income with trailing figures.

The Priced-In Scenario

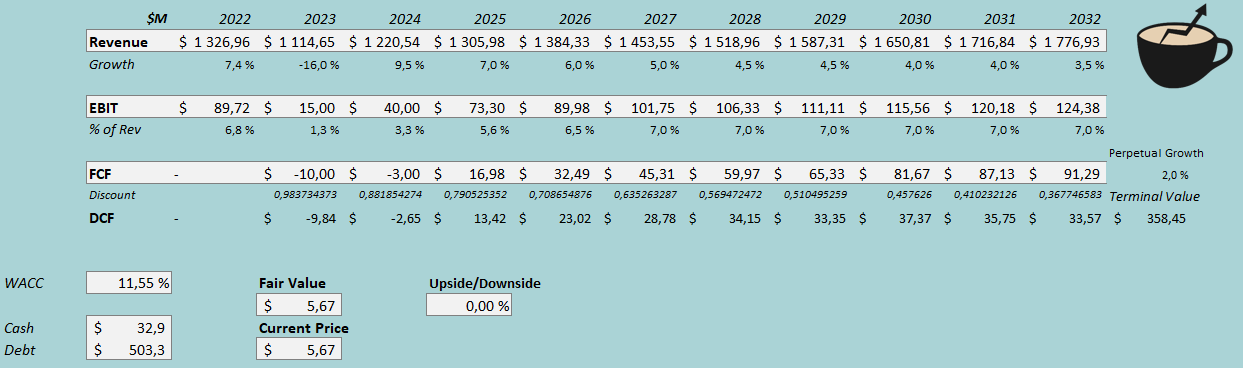

The investment case for Lazydays is very turbulent. To contextualize the valuation, I constructed a reverse discounted cash flow model – in the DCF model, I factor in a financial scenario in which the stock is currently fairly valued with the stock price at the time of writing. The model accounts for a modest number of further acquisitions in coming years, that eventually slow down into no further acquisitions. I believe that factoring in acquisitions is constituted, as the strategy is integral to Lazydays’ operations.

For revenues, I estimate a rebound of 9.5% in 2024 after the bad 2023 result as the macroeconomic situation starts to improve with decreasing interest rates, as the organic investments start to contribute to revenues. After the year, I estimate the acquisitions to still happen but slow down in steps, slowing down the revenue growth as well. The acquisitions stop in 2032, making the company’s perpetual growth rate 2%. Altogether, the revenue performance from 2023 to 2032 represents a CAGR of 5.3%, which seems very reasonable with further acquisitions.

Lazydays’ margin history doesn’t provide a very clear direction for a sustainable long-term margin. In the model, I factor in a margin expansion after the weak 2023 figures into an eventual EBIT margin of 7.0%. I believe that this margin could be achievable for the company in the long term as the economy improves and Lazydays realizes benefits of scale, as well as achieves a higher level in sold financing as interest rates improve. The priced-in margin seems to be mostly in line with my previous rough lining of an EBIT margin above 4.8%, although the 2.2 percentage point increase does seem quite wide.

With the mentioned estimates along with a cost of capital of 11.55%, the DCF model estimates Lazydays’ fair value at the stock price of $5.67, Lazydays’ stock price at the time of writing. In addition, the model factors in outstanding shares as well as prefunded warrants and preferred shares, but doesn’t account for exercisable options as their weighed average exercise price is well above the current stock price.

DCF Model (Author's Calculation)

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In the most recent reported quarter, Lazydays had $9.0 million in interest expenses. With the company’s current amount of interest-bearing debt, Lazydays’ annualized interest rate comes up to 7.12%. The company’s equity valuation is currently very low compared to the amount of debt; estimating a long-term debt-to-equity ratio is quite challenging. I believe that an estimate of 40% is fair, as the company seems to leverage a large amount of short-term borrowings in the operations.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.42% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Lazydays’ beta at a figure of 1.84 . Finally, I add a small liquidity premium of 0.4%, crafting a cost of equity of 15.69% and a WACC of 11.55%.

Takeaway

Currently, Lazydays’ investment case is very volatile. Investors should remain highly cautious of Lazydays’ balance sheet and the company’s margin capabilities - the company's investors should be ready to follow the investment very closely. The issues in margins, partly caused by issues in selling financing to RVs, need to subside in order for the stock to be a worthy investment. Due to the leveraging, the equity's fair valuation varies widely on the actual future financials. I believe that the stock price will bounce as earnings recover, but as the timing of the recovery and the stock price's bottom are very unsure, the recovery could be unworthy of waiting for.

The priced-in scenario seems to mostly have reasonable expectations of Lazydays’ financials, although my reverse DCF model does factor in quite a good margin performance in comparison to the company’s current level. At the moment, I don’t have a thesis that significantly skews the risk-to-reward to either a weak or strong one – for the time being, I have a hold rating for the stock.

For further details see:

Lazydays Holdings: An Uncertain Future