REVG - Lazydays Holdings: Some Caution Is Warranted

Summary

- Lazydays Holdings has seen a significant decline in sales as of late, with market demand for RVs plummeting after years of strength.

- The firm also seems to have excess supply on hand, which could create additional pain moving forward.

- Add on top of this its hefty debt load, and it wouldn't necessarily be a bad idea for investors to turn cautious on the firm.

When it comes to investing, it's important to be at least somewhat pliable. This isn't to say that you should be changing your mind every other day. But when new data comes to the foray, you need to assess that data and let it lead you to the proper conclusion. It's through this process that I have returned to re-evaluate a company called Lazydays Holdings ( LAZY ), an enterprise that operates RV dealerships. Recent financial performance reported by management shows that conditions for the company are worsening. At the moment, shares of the company are still very cheap on an absolute basis. But with the way that the space is turning, shares could very well start to look more or less fairly valued in the next quarter or two. Out of an abundance of caution and because of this most recent data, I've decided to downgrade the company from a ‘buy’ to a ‘hold’ to reflect my view that shares are likely to generate upside or downside more or less in line with the broader market moving forward instead of beating the broader market.

Disappointing data

In early December of last year, I found myself still bullish on Lazydays Holdings. Even at that point, the company was demonstrating continued sales growth, though it is true that rising costs were hitting its bottom line. Given how cheap shares were, I felt quite bullish about the company, to the point of rating it a ‘buy’. Since then, however, shares have taken quite a tumble, resulting in a loss for investors of 12.3%. By comparison, the S&P 500 is down only 2.2% over the same window of time.

{kind=link}

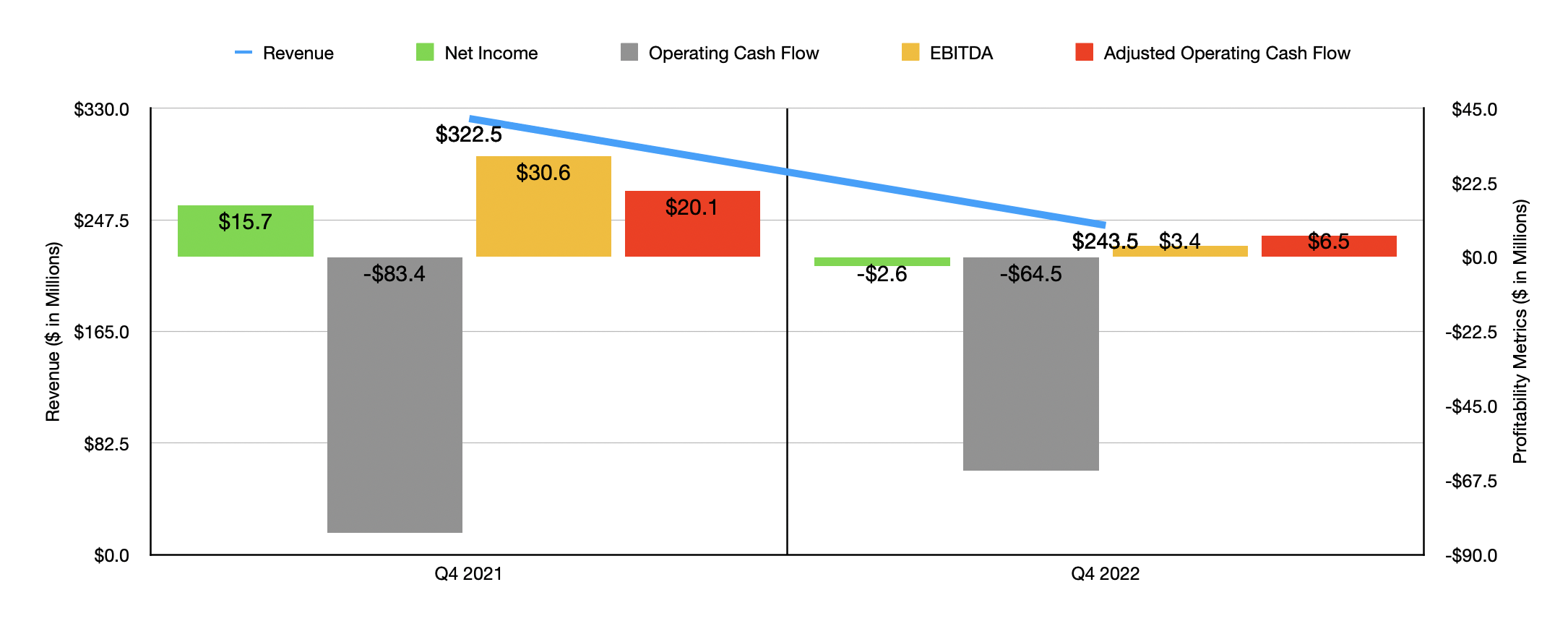

From my experience, the market does often push shares of any given business up or down unreasonably in the short run. But this doesn't mean that every price fluctuation is a false indication for shareholders to ignore. In this case, the move lower was largely attributable to real data that paints a rather bearish picture of things in the short run. The data in question covers the final quarter of the company's 2022 fiscal year. During that time, revenue for the company came in at only $243.5 million. That represents a 24.5% plunge compared to the $322.5 million generated the same time one year earlier. This decline was driven in large part by a plunge in the number of vehicles the company sold. New vehicle retail units sold dropped by 18.2%, while the number of used vehicle retail units sold plummeted 27%. All combined, this worked out to a 21.9% decline in units sold. The company also experienced some pricing pressure. For new vehicle retail units, prices achieved by the company during the quarter fell 3.6% year over year. For used vehicle retail units, that number dropped 8.4%.

Truth be told, this is not all that surprising. For a couple of years now, the industry has experienced significant demand, largely because of increased spending during the COVID-19 pandemic. The RV space flourished because of the desire for individuals who have the money to detach themselves from society more broadly and to utilize the social distancing opportunity to explore the great outdoors or to travel more by vehicle. Unfortunately, things aren't looking that great even after a rather rocky quarter. As of the end of the 2022 fiscal year, the company had 250 days worth of supply of new vehicle inventory. That's up from 84 days reported one year earlier. For used vehicle inventory, it stands at 78 days compared to 58 days one year ago. Absent a change in circumstances, a change that is unlikely because of rising interest rates and persistent inflation, these numbers suggest that the company will have to further decrease prices in order to attract customers.

{kind=link}

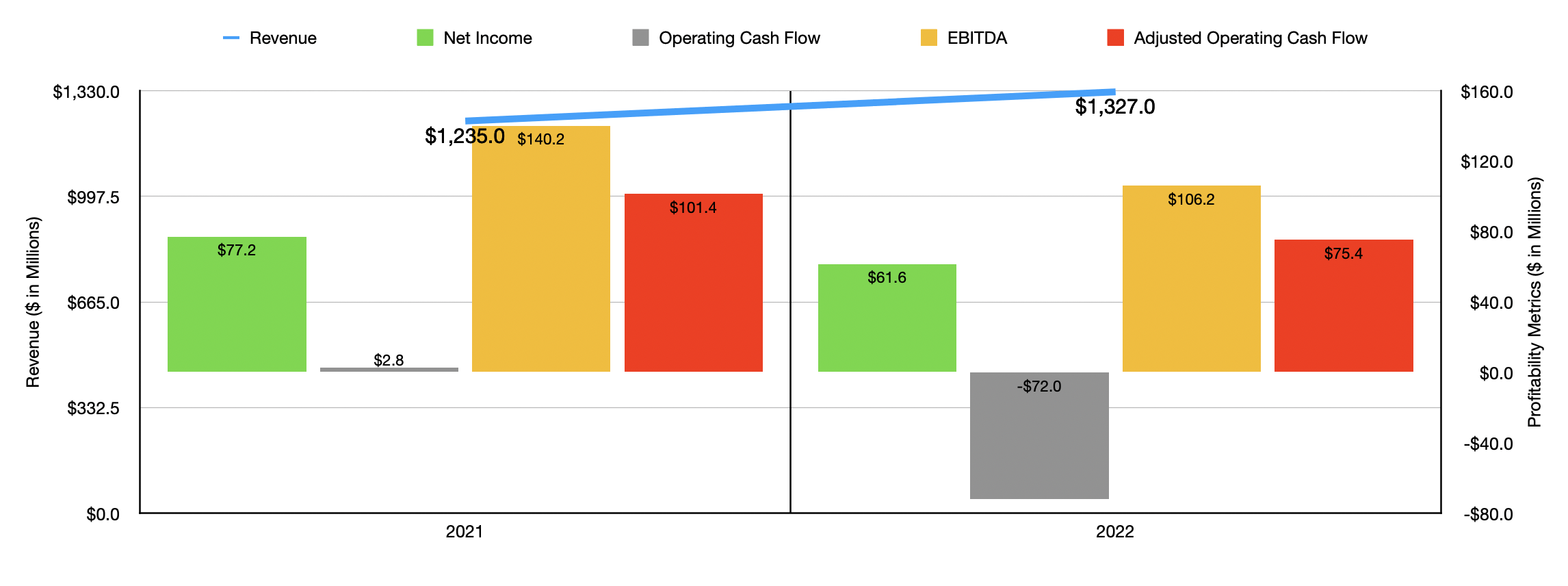

This drop in sales brought with it a worsening of the company's bottom line. Net income went from a positive $15.7 million in the final quarter of 2021 to a negative $2.6 million in the final quarter of 2022. Operating cash flow did improve, turning from negative $83.4 million to negative $64.5 million. But on an adjusted basis, it plunged from $20.1 million to $3.4 million. Meanwhile, EBITDA for the company fell from $30.6 million to $6.5 million. As you can see in the chart above, the results experienced during the final quarter of the year were instrumental in pushing some results down for the 2022 fiscal year as a whole relative to the 2021 fiscal year. While sales for the company are still higher year over year on a full-year basis, profits, cash flows, and EBITDA have all turned lower.

{kind=link}

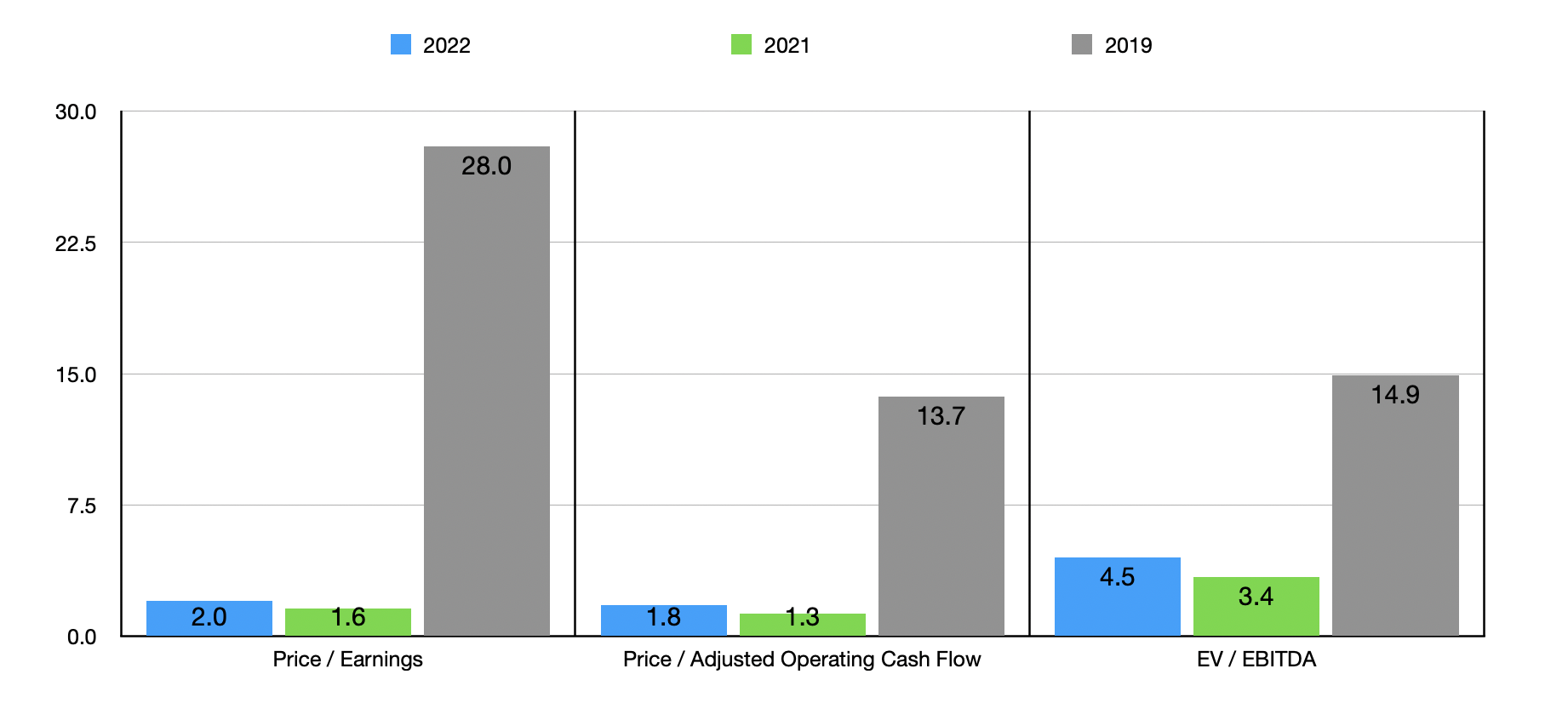

Previously, I pointed to exactly how cheap shares of the company were. Using data from the 2022 fiscal year, we can see that the firm is trading at a price-to-earnings multiple of 2. The price to adjust and operating cash flow multiple is even lower at 1.8, while the EV to EBITDA multiple comes in slightly higher at 4.5. The chart above also shows pricing using data from 2021, as well as the pre-pandemic year of 2019. Given recent developments, it wouldn't be surprising if financial performance gets even worse than what the company saw back then. In that case, shares might be more or less fairly valued. But because we don't know exactly how bad the bottom is going to get, it's not unthinkable that the situation could be even worse.

Using the data from the 2022 fiscal year, I did decide to value the company next to similar firms. The five firms that I picked were trading at price-to-earnings multiples of between 4.9 and 45.9. They were also trading at price to operating cash flow multiples of between 4.8 and 9.6. In both cases, Lazydays Holdings was the cheapest of the group. Meanwhile, using the EV to EBITDA approach, the range would be from 3.8 to 13.7. In this case, two of the five firms were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Lazydays Holdings |

| 2.0 |

| 1.8 |

| 4.5 |

| Winnebago ( WGO ) |

| 6.0 |

| 5.7 |

| 4.1 |

| THOR Industries ( THO ) |

| 4.9 |

| 4.8 |

| 3.8 |

| LCI Industries ( LCII ) |

| 7.3 |

| 4.8 |

| 5.8 |

| Camping World ( CWH ) |

| 5.2 |

| 9.6 |

| 4.6 |

| REV Group ( REVG ) |

| 45.9 |

| 7.9 |

| 13.7 |

Takeaway

When I wrote about Lazydays Holdings stock previously, I understood that the financial picture for the business was going to worsen to some degree. The way I saw it though, shares were so cheap that, even if they saw some pain, they shouldn't be any worse than fairly valued. Given the recent drop in sales that the company experienced, however, I do think that the picture might be a bit worse than what I thought it would be. In the long run, I still do think the firm will be just fine. For those who have a five-year investment horizon or longer, I suspect that the outcome for the company will be fine so long as the downturn we are going into does not last for an extended period of time. But with debt in excess of cash right now of $297.2 million and the pain the company saw in just a single quarter, I do think a ‘hold’ rating is more appropriate at this time.

For further details see:

Lazydays Holdings: Some Caution Is Warranted