LAZY - Lazydays Holdings: Still Not The Best Time To Buy The Dip

2023-09-07 10:06:25 ET

Summary

- In 2Q23, the company's revenue decreased by 17.4% YoY, while operating margin decreased to 4.1%.

- Pressure on consumer real incomes due to macro headwinds continues to weigh on recreational vehicle sales.

- I expect pressure on the company's financials to continue in the coming quarters, so my recommendation is HOLD.

Introduction

Shares of Lazydays Holdings ( LAZY ) have fallen 5% YTD. Since my publication , where I spoke about the absence of growth catalysts, stock prices have decreased by 2.6%, while the S&P index has shown growth by 3%. In my article, I would like to analyze current trends and update my view on the company's shares.

Investment thesis

Although the company's financials have improved slightly from the previous quarter, I believe that this is still not the best time to go long. I expect pressure on business growth and margins to continue in the coming quarters as consumers continue to experience high inflation and pressure on real incomes, which could contribute to a decline in recreational vehicle sales in quantitative terms. Also, I do not expect margins to recover to last year's levels, despite the first signs of a recovery in new recreational vehicle (RV) prices, because lower sales volumes could lead to lower sales of additional products such as financing and insurance.

Company overview

Lazydays Holdings sells and services recreation vehicles (RV) in the US market, as well as financing and insurance products. The main revenue segments are new vehicle retail (59% of revenue) and pre-owned vehicle retail (30% of revenue). The company was founded in 1976.

2Q 2023 Earnings Review

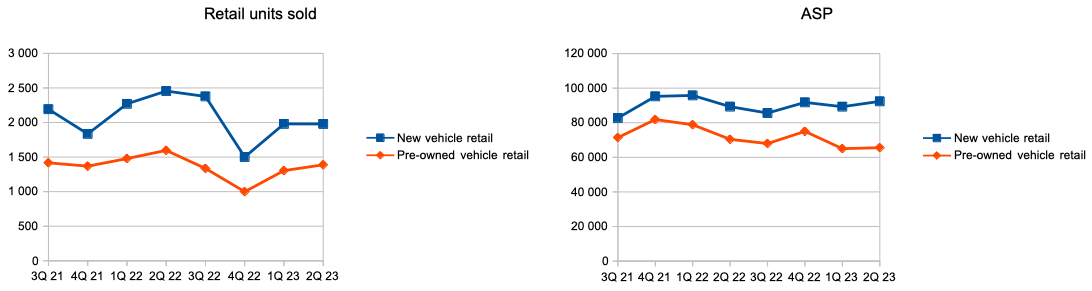

The company's revenue decreased by 17.4% YoY . The largest contribution to the decline in revenue was made by the "pre-owned vehicle retail" and "new vehicle retail" segments, where sales decreased by 19% and 17%, respectively, due to a decrease in the number of cars sold. Thus, car sales in quantitative terms in the "pre-owned vehicle retail" and "new vehicle retail" segments decreased by 13% and 19%, respectively. However, in the new vehicle retail segment, we saw little support from the average selling price ((ASP)), which increased by 3.4% YoY, while in the pre-owned vehicle retail segment, the ASP decreased by 7% YoY.

Retail units sold & ASP (Company's information)

{kind=link}

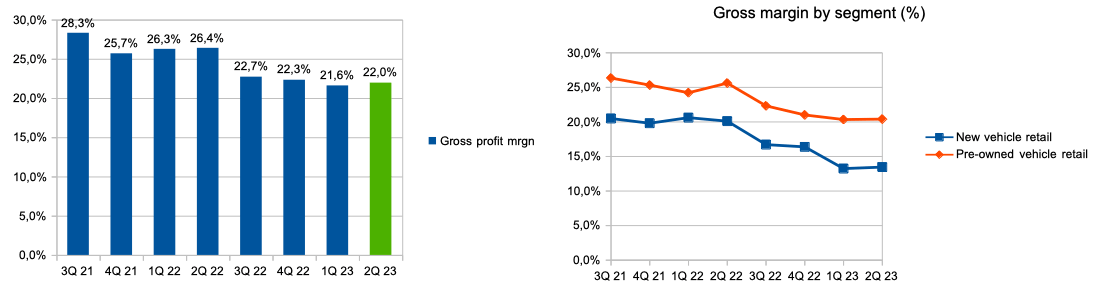

Gross profit margin decreased from 26.4% in Q2 2022 to 22% in Q2 2023. If we look in more detail, in the "new vehicle retail" and "pre-owned vehicle retail" segments, the gross profit margin decreased from 20.1% to 13.5% and from 20.1% to 25.6% to 20.4% respectively. You can see the details in the charts below.

Gross profit margin & gross profit margin by segment (Company's information)

{kind=link}

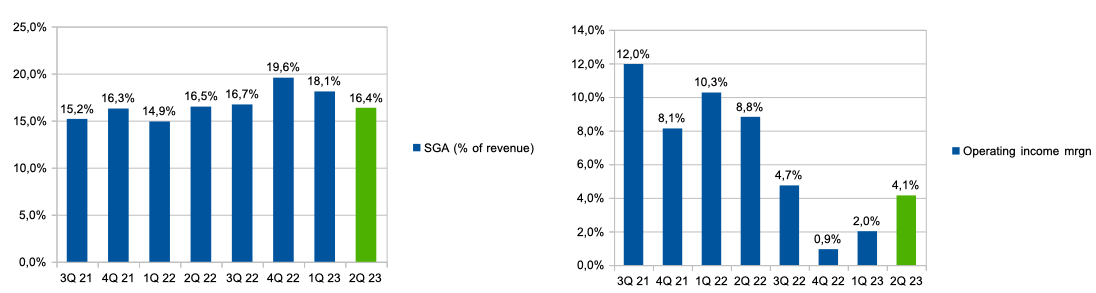

SGA spending (% of revenue) decreased slightly from 16.5% in Q2 2022 to 16.4% in Q2 2023. Thus, the operating margin decreased from 8.8% in Q2 2022 to 4.1% in Q2 2023.

SGA (% of revenue) & op. margin (Company's information)

{kind=link}

In the 2nd quarter, cash on the company's balance sheet decreased by 41% QoQ to $24.2 million due to additional expenses on CAPEX (fixed assets for new properties in Arizona, Ohio and Florida) and the acquisition of a dealership. However, an additional $61 million of liquidity is available to the company under the Floorplan and the facility, and approximately $61.2 million that could be secured by real estate owned by the company.

My expectations

Despite the fact that the rate of decline in revenue is starting to slow down, I think that the rate of revenue growth will continue to be under pressure in the coming quarters. First, the slowdown in revenue is due to a decrease in the base of comparison compared to last year, when the company faced a sharp increase in demand for products. Secondly, I don't expect to see a recovery in consumer spending in the next 2 quarters that could boost RV sales in quantitative terms because inflation continues to be relatively high and consumers continue to face higher interest costs. payments, food and rent.

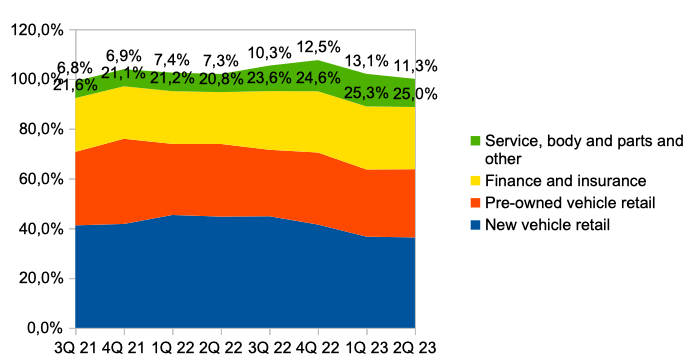

In addition, I expect operating margins to continue to be under pressure, despite the fact that we saw a 3.4% YoY price increase in the new vehicle retail segment. I believe that the decline in sales of new recreation vehicles will continue to put pressure on the gross margin in terms of lower potential sales of cross-products such as finance & insurance and service, which account for about 36% of gross profit in 2Q 2023.

Every unit that we sell has an F&I opportunity, obviously. But importantly, many of them come with trades and all of them become then potential customers in our service department down the road. And so this is a unique retail business in that there aren't many retailers that sell stuff and then fix them too down the road.

Gross profit mix (Company's information)

{kind=link}

Moreover, I believe that the potential to reduce the cost of SGA (% of revenue) is quite limited, since most of the company's expenses (rent and salary) are fixed.

Risks

Margin: decreasing cross-selling due to lower number of RVs sold, investment in prices (seasonal discounts) and reduced economies of scale could contribute to lower operating margins in the coming quarters.

Macro (general risk): a decrease in real consumer income due to high inflation may lead to a decrease in consumer spending in the discretionary segment, which may have a negative impact on revenue growth in the future. In addition, rising interest rates make credit instruments more expensive, while some consumers use borrowed funds to buy recreational vehicles.

Valuation & Conclusion

Valuation Grade is A-. Under EV/Sales ((FWD)) and P/S ((FWD)) multiples, the company trades at 0.6x and 0.1x respectively, which implies a discount to the sector median of around 53% and 85% respectively, but under EV /EBITDA ((FWD)) the company trades at 16.6x, implying a premium to the sector median of around 74%. I believe that investors should not make a buying decision based only on a relatively cheap valuation according to multiples, as stock prices may continue to be under pressure in the absence of clear catalysts for growth (recovery of RV sales in quantitative terms, recovery of profitability).

Thus, I would like to confirm my Hold recommendation. I think the company's financial performance will continue to be under pressure in the coming quarters.

For further details see:

Lazydays Holdings: Still Not The Best Time To Buy The Dip