LCII - LCI Industries: Future Successful M&A And Large Target Markets Imply Undervaluation

2023-05-18 16:59:19 ET

Summary

- LCI Industries, through its subsidiary Lippert Components, supplies a wide range of engineered components for original equipment manufacturers in the recreation and transportation markets.

- I believe that reducing reliance on a single industry segment is strategically wise to ensure long-term sustainable growth in LCI Industries.

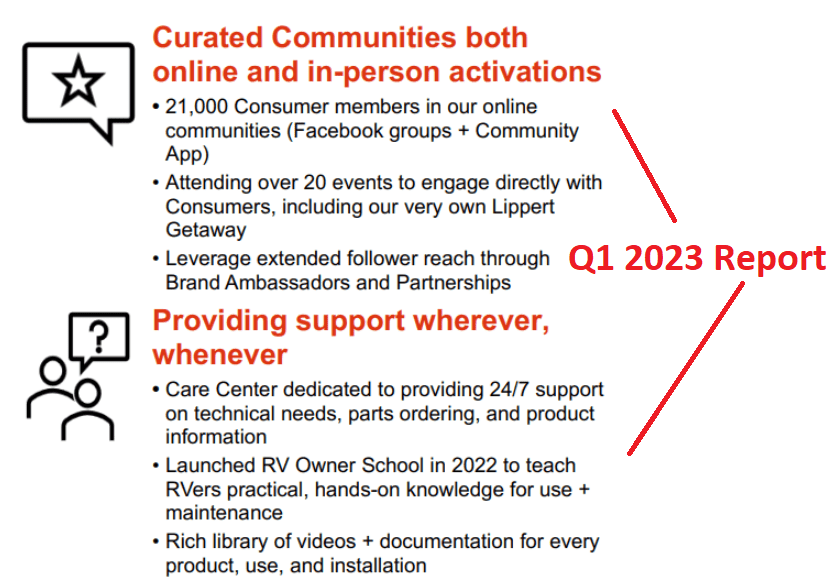

- In the last quarterly report, the company reported 21,000 consuming members in an online community on Facebook and several other apps as well as close to 20 events.

LCI Industries ( LCII ) intends to reduce its dependence on the recreational vehicle industry, and recently identified several target markets that offer close to $11 billion market opportunity. Besides, in the Q1 2023 report, management noted that it expects to introduce international products into the United States, and unlock cross selling opportunities through new acquisitions. I also think that further introduction of online efforts, like online communities and technical support, and more acquisitions could bring new customers and diversification. There are several risks from customer concentration, supply chain, or failed internationalization, however I believe that the stock could trade at higher marks.

LCI

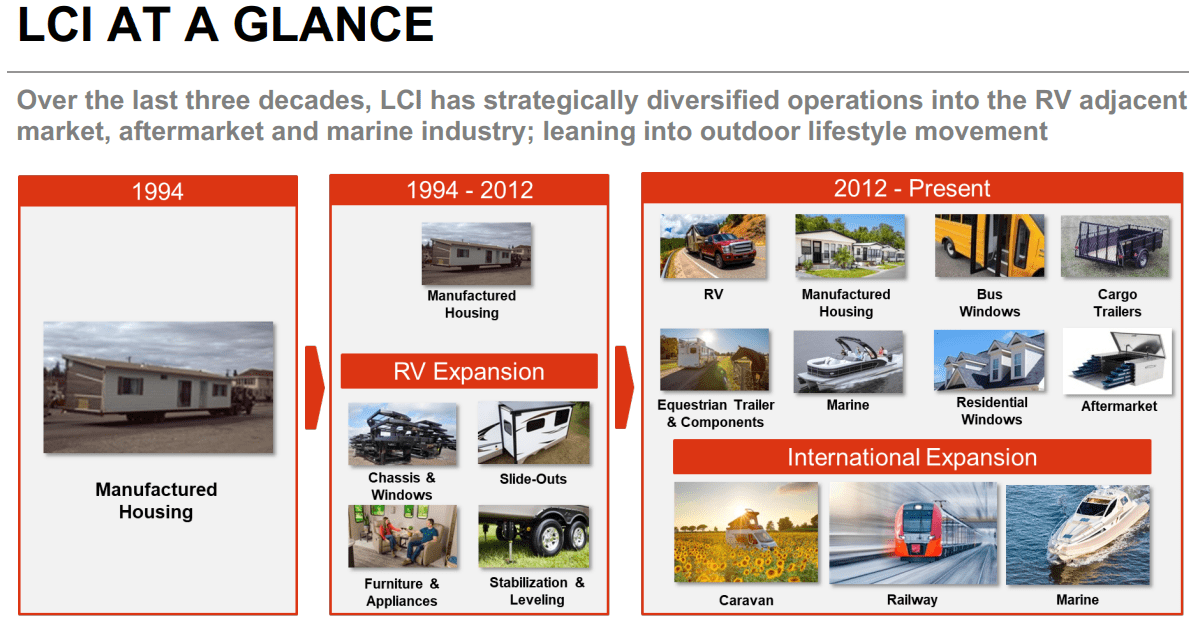

LCI Industries, through its subsidiary Lippert Components, supplies a wide range of engineered components for original equipment manufacturers in the recreation and transportation markets.

{kind=link}

Source: Investor Relations

Its products include steel chassis, axles, suspension solutions, thermoformed baths, windows, leveling systems, doors, furniture, steps, awnings, trailer and truck accessories, electronic components, air conditioners, television, water heaters, and other accessories. These products are used in RVs, boats, buses, trailers, trucks, trains, manufactured homes, and modular homes. LCI focuses on meeting the needs of the industry with quality and variety of products.

{kind=link}

Source: 10-K

LCI Industries' business model is based on supplying a wide range of engineered components to leading OEMs in the recreation and transportation markets. In addition to OEM sales, many of its products are marketed through aftermarket channels, such as retail distributors, wholesalers, and service centers, as well as direct sales to retail customers over the Internet.

The company offers technical, product, and installation training, and provides marketing support to its after-sales customers. It also has call centers to provide quick responses to delivery and technical support needs. The aftermarket segment includes a variety of products such as accessories, spare parts, and services, catering to customer needs in different seasons.

With that being said about the products of LCI, I turn my attention to the significant number of communities created by management. In the last quarterly report, the company reported 21,000 consuming members in an online community on Facebook (FB) and several other apps as well as close to 20 events to engage directly with consumers. Besides, the Care Center is dedicated to providing 24/7 support on technical needs and product information. In my view, feedback received from clients through events and these communities and technical support will help develop better products and strengthen its relationships with new customers.

{kind=link}

Source: Investor Relations

Balance Sheet

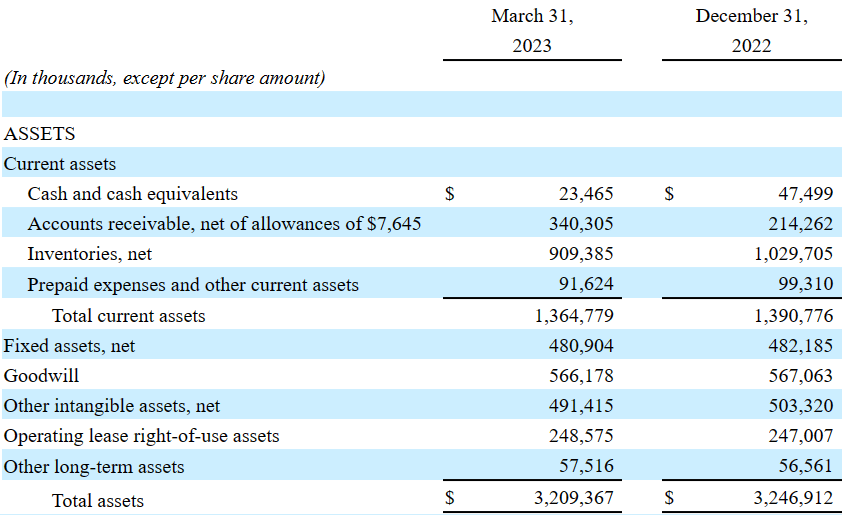

The balance sheet reported in March 2023 doesn't differ from that in December 2022. The total amount of assets decreased just a little bit, driven by a decrease in cash and cash equivalents and a decrease in inventories. The amount of goodwill and the amount of other intangible assets decreased too. With regards to the list of liabilities, the long-term indebtedness as well as the total amount of liabilities decreased slightly.

As of March 31, 2023, LCI reported cash and cash equivalents close to $23 million, with accounts receivable worth $340 million and inventories of $909 million. Prepaid expenses and other current assets stood at $91 million with total current assets worth $1.364 billion. The total amount of assets is three times the total amount of current liabilities. Hence, I think that LCI does not seem to have liquidity issues.

Long term assets include goodwill of $566 million, other intangible assets of $491 million, operating lease right-of-use assets close to $248 million, and total assets of $3.209 billion. The asset/liability ratio stands at close to 2x.

{kind=link}

Source: 10-Q

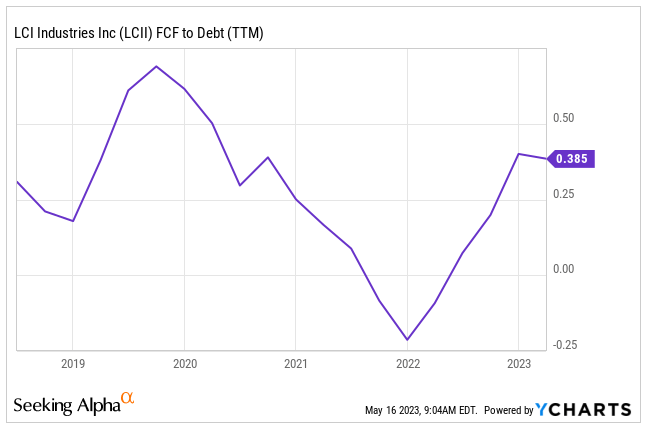

I do not think that the total amount of leverage is worrying. With FCF to TTM debt of close to 0.3x, I believe that future FCF justifies the total amount of debt.

{kind=link}

Source: YCharts

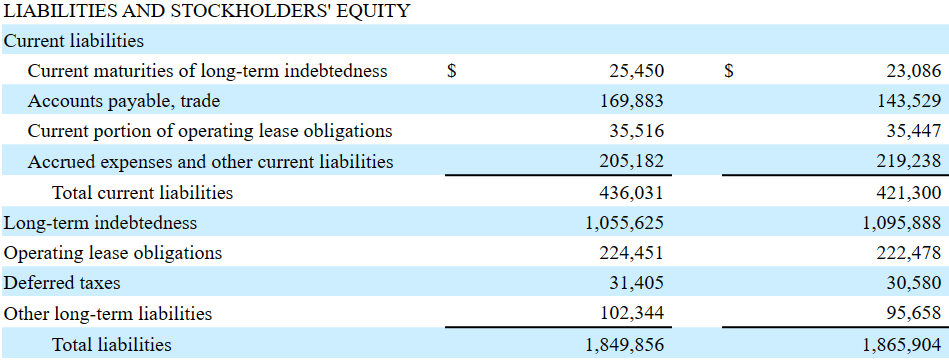

In the last quarterly report, the company noted current maturities of long-term indebtedness of $25 million, accrued expenses and other current liabilities worth $205 million, long-term indebtedness of about $1055 million, operating lease obligations worth $224 million, deferred taxes of $31 million, and total liabilities of $1849 million.

{kind=link}

Source: 10-Q

I also found the table of contractual obligations, which the company reported in a recent annual report. I do not see any current obligation to worry about. Most obligations appear to be long-term obligations.

{kind=link}

Source: 10-K

Further Diversification Of The Business Model, Internationalization, And Investments In The Aftermarket Segment Would Imply A DCF Valuation Of $158 Per Share

I believe that the growth of the strategy of LCI is quite appealing. It includes allocating capital to areas with the highest growth return and reducing leverage.

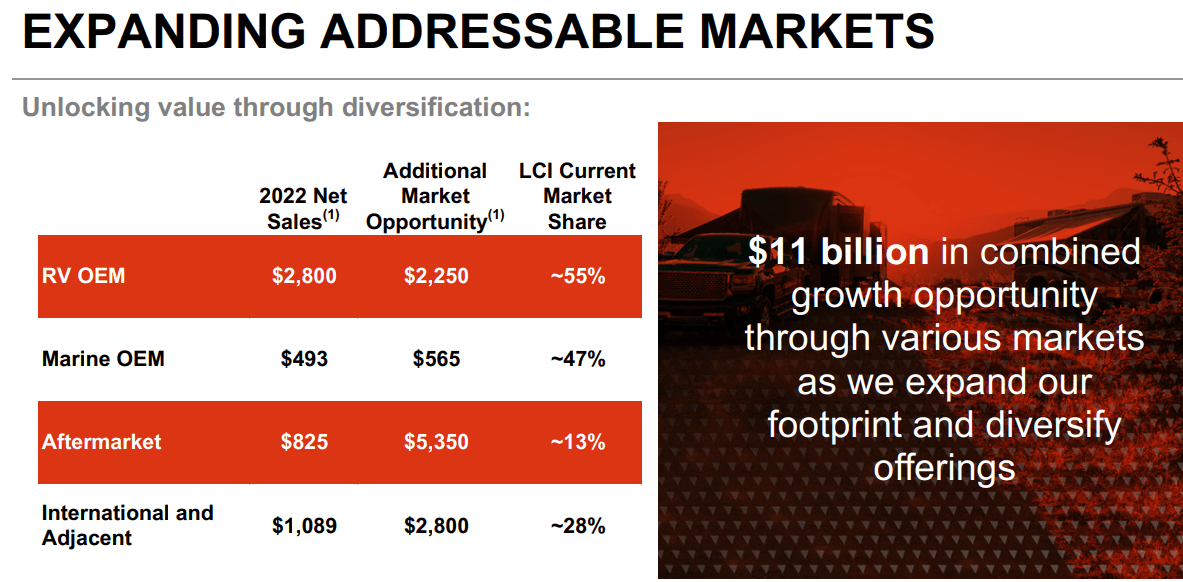

The business strategy is also focused on diversifying its markets beyond the recreational vehicle OEM industry in North America. In 2022, approximately 46% of its net sales came from outside the North American RV OEM market, compared to 47% in 2021.

I believe that further expansion into new markets and reducing its dependence on a single industry segment will most likely strengthen its position in the long term. In my opinion, investors would most likely appreciate it.

Besides, management expects to introduce international products into the United States, and unlock cross selling opportunities through new acquisitions. Under successful implementation of these strategies, I would expect an increase in business growth, revenue growth, and free cash flow growth.

With regards to expansion in new markets or existing markets, I would highlight the additional market opportunity in the aftermarket services as well as the international and adjacent markets. In the last quarterly report, the company reported an $11 billion combined opportunity of growth in several markets.

{kind=link}

Source: Investor Relations

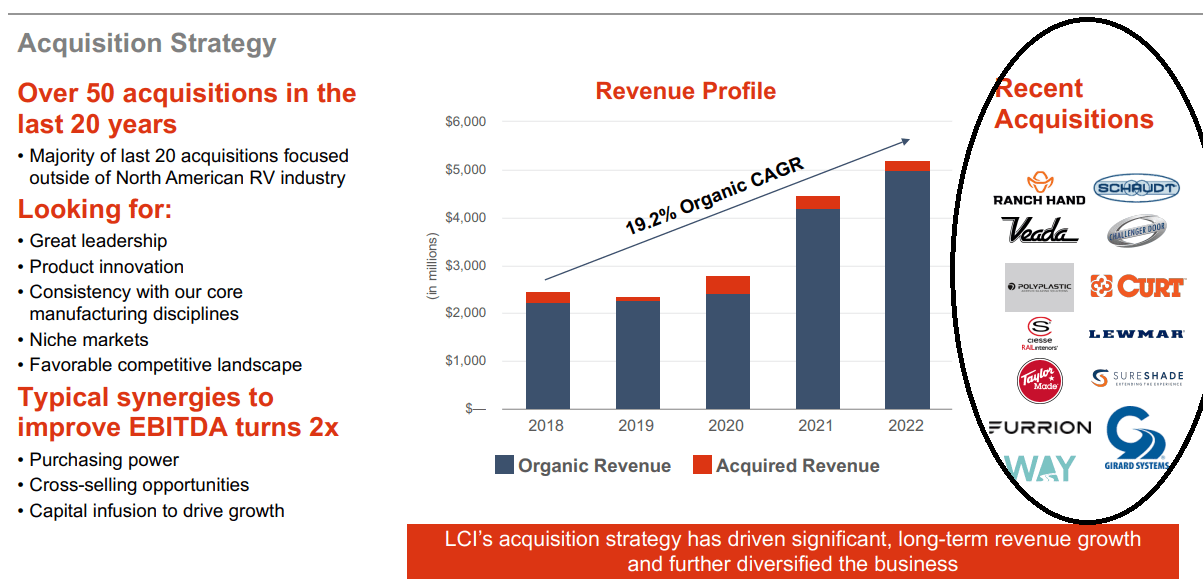

Having said that about the organic growth shown by LCI, I believe that the acquisition strategy reported by management is very relevant. We are talking about over 50 acquisitions in the last 20 years, mainly looking for leadership, product innovation, new products in niche markets, and a favorable competitive landscape. Considering the expertise in the M&A markets, I believe that we can expect new transactions in the coming years. In my view, new track sections would most likely lead to free cash flow growth.

{kind=link}

Source: Investor Relations

As online shopping becomes the preferred way to purchase products, in my view, customers have made LCI Industries their one stop shop for over 50,000 items available. In my opinion, it is a fast growing part of the business, even though it's a very small part of the business. My belief is that in the long term it will probably be the number one revenue producer.

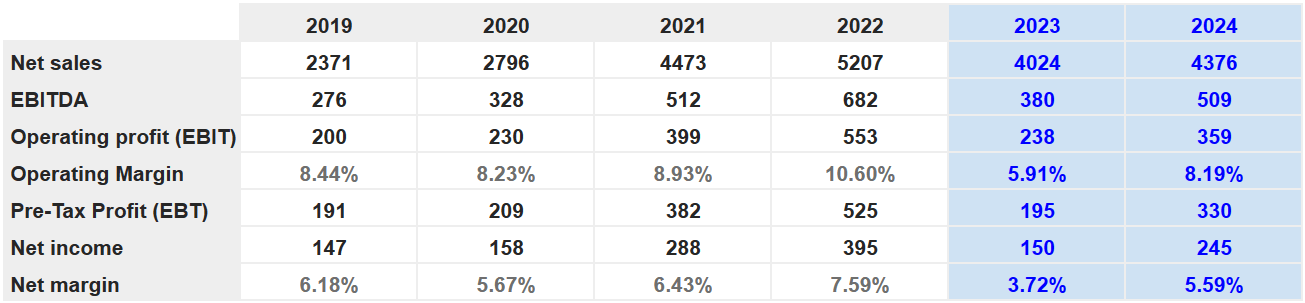

I took into account the forecasts of other financial advisors in order to design my financial model. Other investors expect 2024 net income of $245 million, net margin of 5.59%, and 2024 EBITDA close to $509 million. My figures are a bit more conservative than that of other financial forecasters.

{kind=link}

Source: S&P

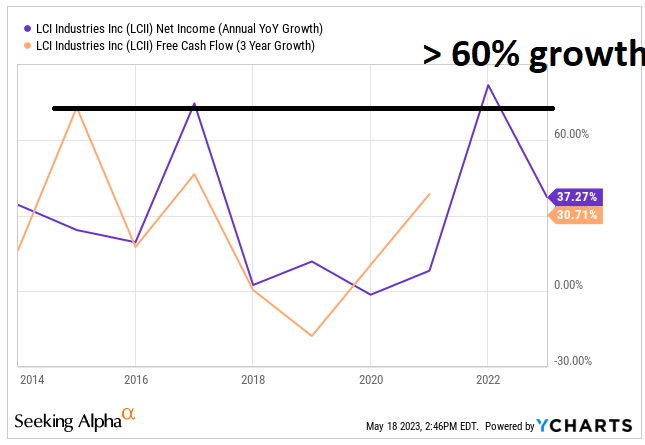

For the calculation of future FCF, and net income growth, I also took into the optimism of management about the year 2023, and future years , and previous FCF growth, and net income growth.

Our strong cultural foundation, veteran operational leadership, and dedicated team members keep us on track in our efforts to create long-term value for all stakeholders throughout 2023. Source: Quarterly Press Release

{kind=link}

Source: YCharts

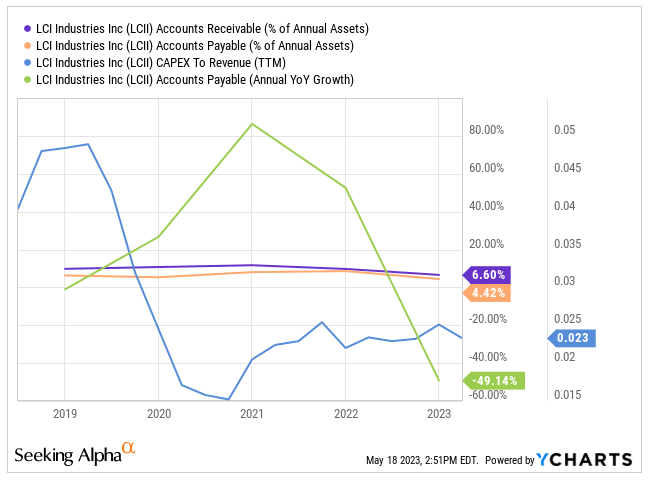

For the calculation of future changes in accounts receivable, capex, accounts payable, and other future assumptions, I used growth seen in the past.

{kind=link}

Source: YCharts

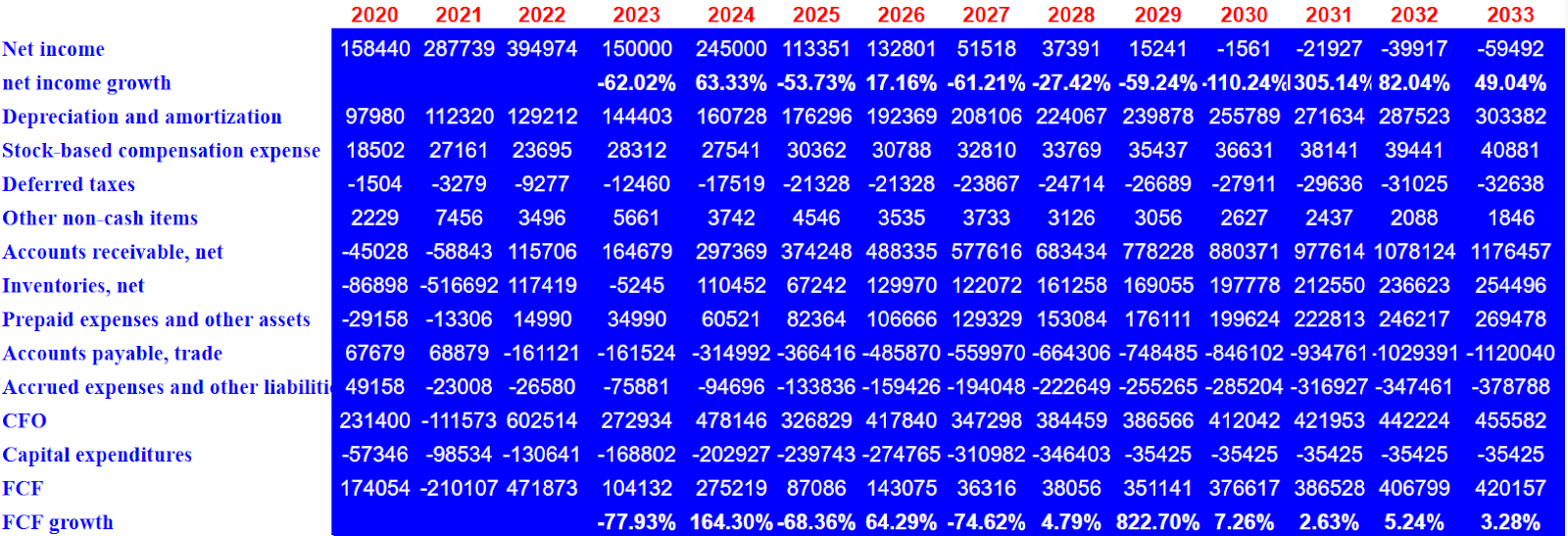

My cash flow model includes 2025 net income of $113 million. I also assumed 2025 depreciation and amortization of $176 million with stock-based compensation expenses of $30 million. Also, with changes in accounts receivable of $374 million, changes in inventories of $67 million, and changes in prepaid expenses of $82 million, 2025 CFO would stand at close to $326 million. If we also include 2025 capital expenditures of -$240 million, 2025 FCF would be close to $87 million.

For the year 2033, I included net income of -$60 million, depreciation and amortization of $303 million, and stock-based compensation expenses of $40 million. Also, with changes in accounts receivable of $1176 million and changes in inventories worth $254 million, I assumed prepaid expenses close to $269 million. Finally, the 2033 CFO would be close to $455 million, and the FCF would be close to $420 million.

{kind=link}

Source: My DCF Model

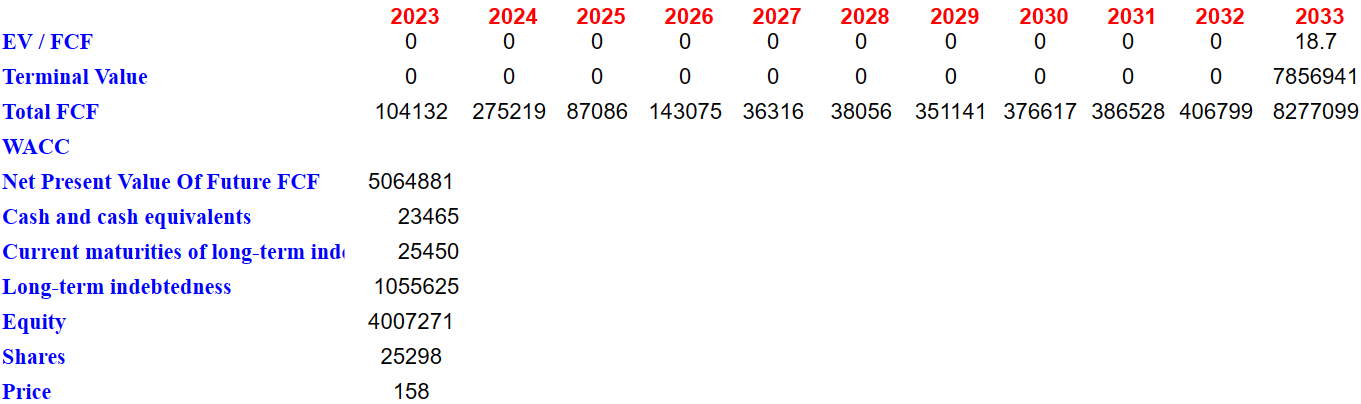

If we assume an EV/FCF multiple of 18.71x, the terminal FCF would be close to $7856 million. Besides, with a WACC of 76.2%, the implied net present value of future free cash flow would be $5.064 billion. If we add cash and cash equivalents of $23 million, and subtract current maturities of long-term indebtedness of $25 million and long-term indebtedness of $1055 million, the implied equity valuation would be $4007 million. The fair price would be close to $158 per share.

{kind=link}

Source: My DCF Model

The Barriers To Entry Do Not Seem Low

In the recreational vehicle industry, LCI Industries faces intense competition from both RV manufacturers and component suppliers. Market entry is primarily based on compliance with standards, codes, safety requirements, and the initial capital investment required to establish manufacturing operations.

The RV industry is highly competitive, both among manufacturers of RVs and the suppliers of RV components, generally with low barriers to entry other than compliance with industry standards, codes and safety requirements, and the initial capital investment required to establish manufacturing operations. Source: 10-K

Competition focuses on product quality and reliability, innovation, price, customer service, and customer satisfaction. Although no definitive data is available, LCI considers itself a leading supplier of trailerable RV components.

Lack Of Demand, Loss Of Key Customers, Or Lack Of Raw Materials Would Bring The Implied Valuation Down

I believe that reduced availability of wholesale financing may limit demand for the products of LCI. Besides, LCI suffers risks from excess inventories and declining industry shipments, which could also affect demand. If clients purchase less products from LCI, management may have to lower prices, and the cash flow statement may deliver lower FCF growth.

Loss of key customers could also bring violent decline in sales. It is worth mentioning that there are two customers that account for more than 19% of the total amount of sales. One of these customers is Berkshire Hathaway Inc. ( BRK.B ). In my view, future customer count increase would be appreciated by investment participants.

{kind=link}

Source: 10-K

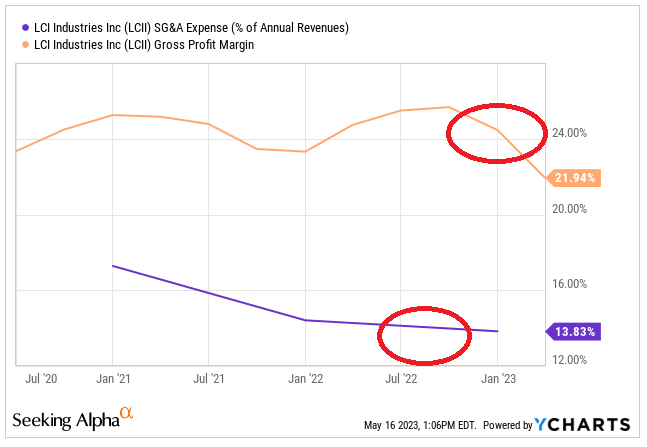

I also believe that volatile raw material costs, supply chain disruptions, and labor shortages could also pose risks. If LCI does not deliver further decreases in the SG&A/Revenue ratio and the gross profit margin because of an increase in salaries or an increase in raw materials’ pricing, FCF will likely decrease. As a result, I believe that investors may sell their stakes.

{kind=link}

Source: YCharts

Opinion

I believe that reducing reliance on a single industry segment is strategically wise to ensure long-term sustainable growth in LCI Industries. Besides, new M&A operations, more efforts around ecommerce, internationalization, or expansion of the aftermarket segment will likely bring FCF growth. I also see intense competition and risks associated with the availability of financing, fluctuating demand, and supply chain disruptions. With that, considering the know-how accumulated throughout the years, innovation, and efforts to reach customer satisfaction, the leading position is not recognized by the market. I believe that the share price could be worth more than what the market currently discloses.

For further details see:

LCI Industries: Future Successful M&A And Large Target Markets Imply Undervaluation