LCII - LCI Industries: Recent Declines Ignore Real Strength

- LCI Industries has followed the market lower in recent months, but this has occurred even as fundamental performance improves.

- At present, shares of the business look cheap and they aren't overvalued even if we assign results from 2022 to the business.

- This seems to offer investors a good buying opportunity right now even though near-term pain might still be on the table.

When it comes to the automotive market, one of the companies that I find most attractive at this time is LCI Industries ( LCII ). The company produces a variety of products, such as steel chassis, axles, thermoformed baths, kitchens, and other products, and other related offerings for recreation and transportation customers, largely focused on RVs and other related vehicles. For the most part, the fundamental performance of the company has been robust. But that has not stopped the company's share price from taking a beating as the broader market has declined. Today, shares of the business are much cheaper than they were previously. And this ignores the prospect of a strong 2022 fiscal year. So while I wouldn't be surprised at fundamentals eventually weakening if the economy truly does suffer some blows, I do think the long-term outlook for shareholders is favorable at this time.

The market is ignoring the fundamentals

Both a positive and negative thing about the market is that, when fear permeates, even high-quality companies can experience some pain. The downside to this is that investors who already own shares in the companies in question see a short-term hit to their portfolios. But the positive side is that it gives you the opportunity to buy into a firm that you liked previously at a price that is even more appealing than it was before. This latter example might be exactly what we are seeing today with LCI Industries. You see, back in January of this year, I wrote a bullish article about the enterprise. In that article, I acknowledged that the company had experienced an increase in price in the prior months, eliminating much of the upside potential the company offered. Having said that, I was impressed by its fundamental condition and I felt that while shares were not as cheap as they were previously, it still warranted a ‘buy’ rating. Since then, things have not played out exactly as I would have anticipated. While the S&P 500 is down by 17.7%, shares of LCI Industries have dropped by 19.2%.

{kind=link}

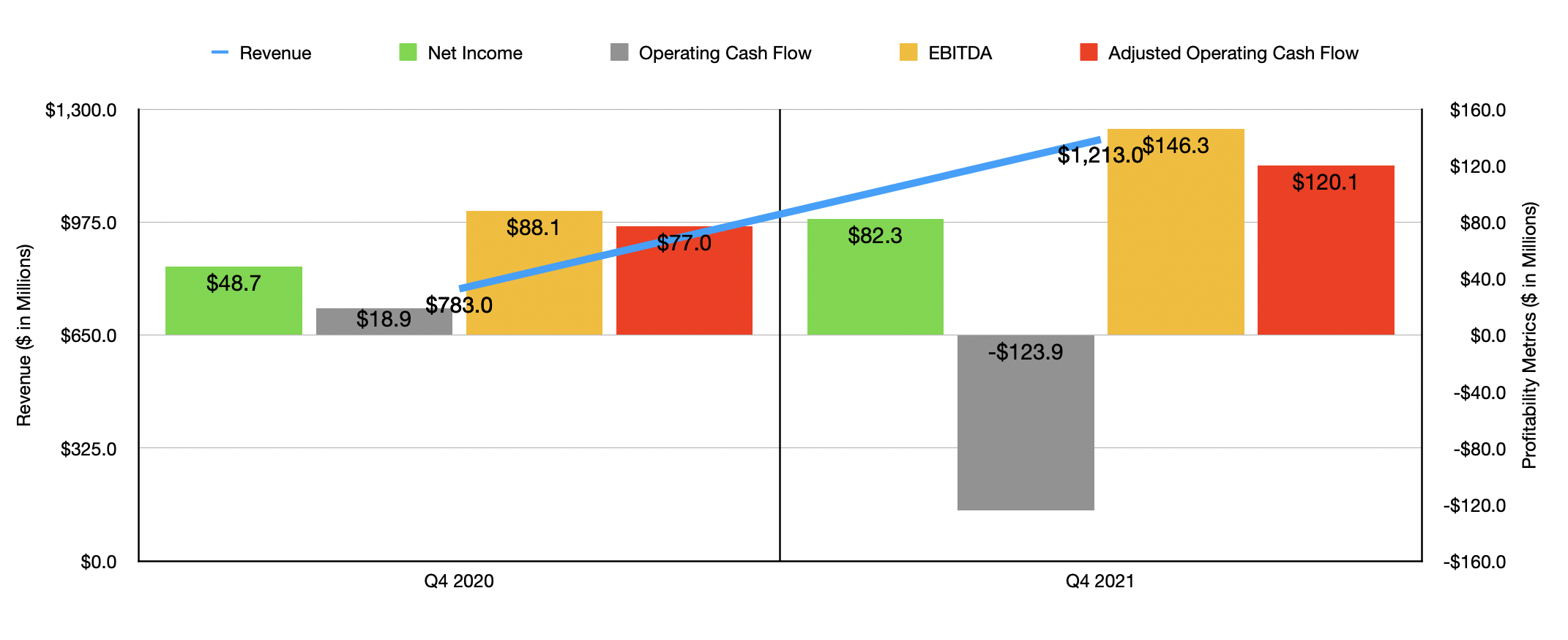

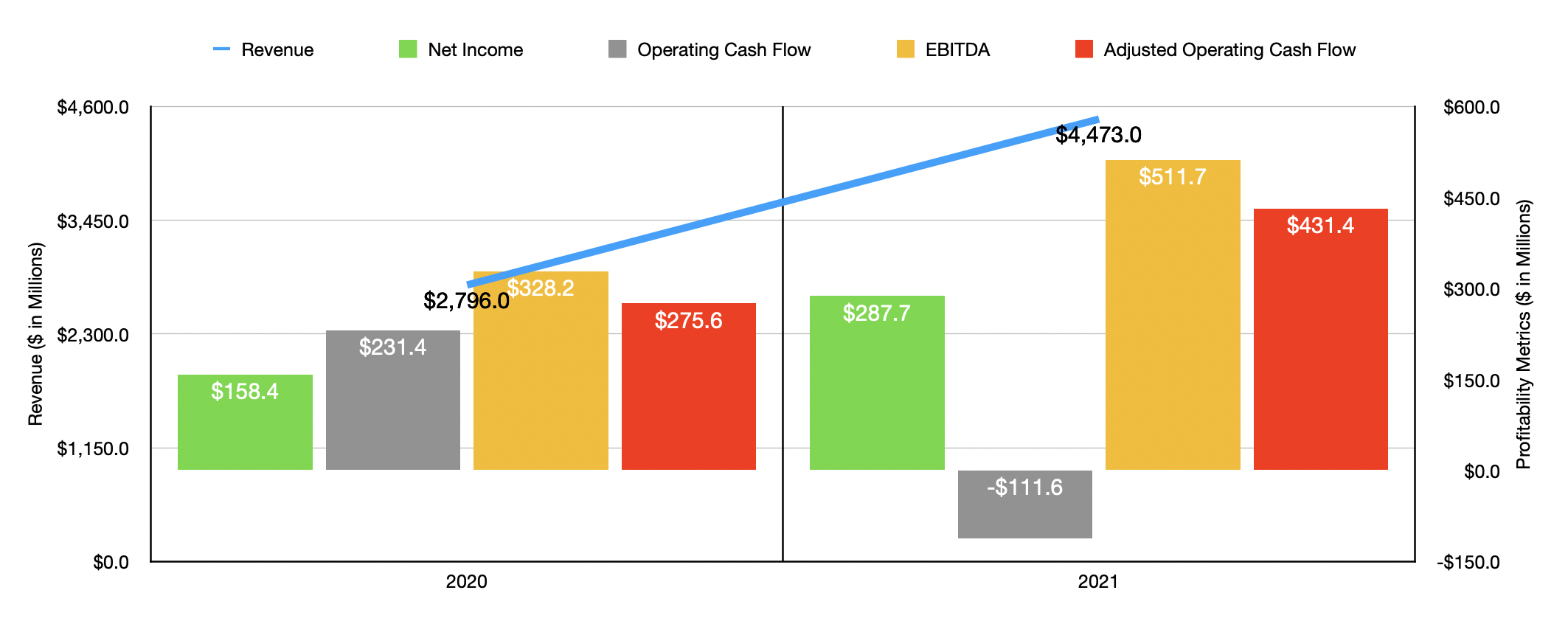

Given this decline, you would be forgiven for thinking that the fundamental condition of the company was worsening. But the exact opposite is true. When I last wrote about the firm, we only had data covering through the third quarter of its 2021 fiscal year. Today, that data now extends through the first quarter of its 2022 fiscal year. To start with, let's touch on how the company ended 2021 . For the final quarter of that year, sales came in at $1.21 billion. That represented a 54.9% increase over the $783 million reported just one year earlier. As a result of this robust performance, total revenue for the year came in at $4.47 billion. That's 60% higher than the $2.80 billion reported for the 2020 fiscal year. This was driven in large part by strong demand across the RV industry, with the increase in units attributable to wholesale customers totaling 40%, while for the retail space demand rose by 10%. The company also benefited from various acquisitions that, combined, added $269.9 million to the firm's revenue last year.

{kind=link}

Profitability for the company followed a similar path. Net income of $82.3 million in the final quarter of 2021 dwarfed the $48.7 million reported the same quarter one year earlier. This brought total net profits for 2021 up to $287.7 million. That's 81.6% above the $158.4 million reported for 2020. Other profitability metrics came in strong as well. While operating cash flow declined from a positive $231.4 million to a negative $111.6 million, the picture changes if we adjust for changes in working capital, with the metric climbing from $275.6 million to $431.4 million. Meanwhile, EBITDA increased from $328.2 million to $511.7 million. Once again, these were aided by largely strong and positive results in the final quarter of 2021 compared to the same quarter of 2020.

{kind=link}

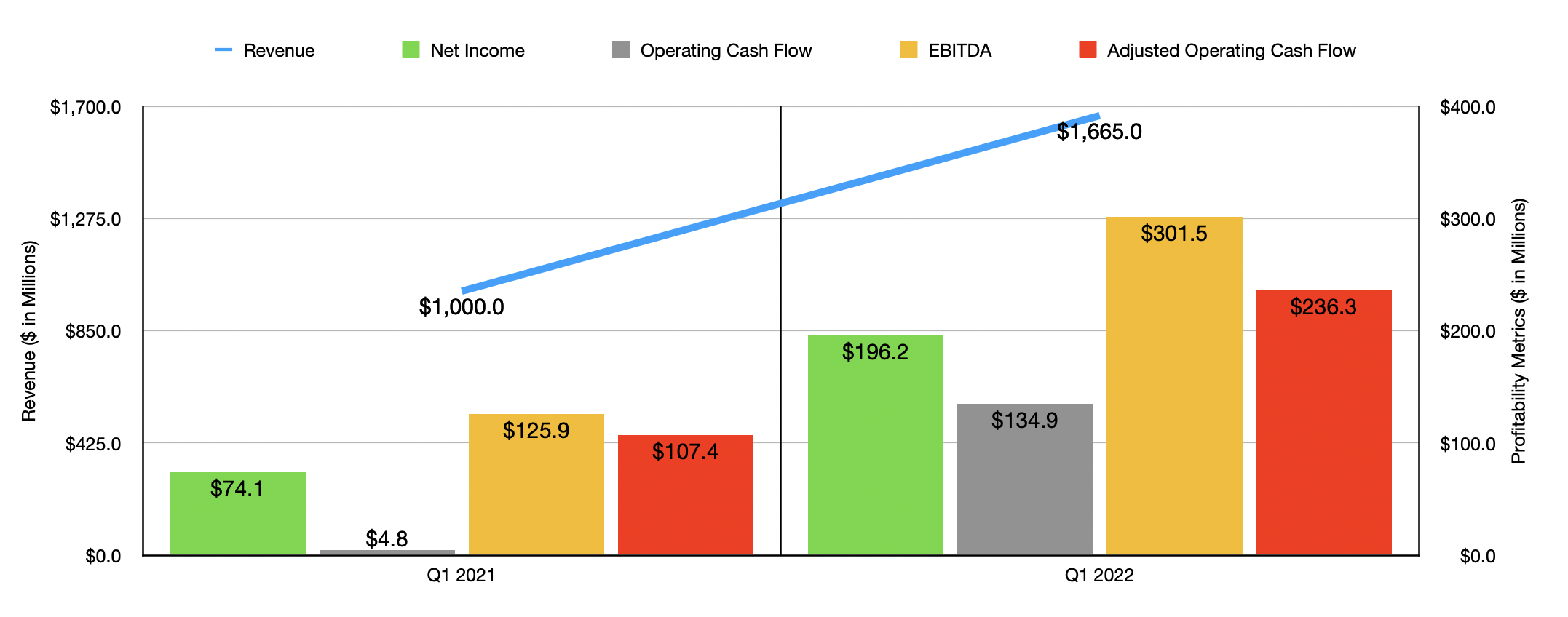

Growth for the company has continued into the 2022 fiscal year. Revenue for the first quarter came in at $1.67 billion. That's roughly 66.5% higher than the $1 billion reported just one year earlier. According to management, wholesale unit volumes for RVs increased by 16%, even as retail demand dropped by 18%. The company also benefited from price increases as well as from a particular acquisition that added $79 million to its top line year-over-year. As revenue increased, profitability rose as well. Net income increased from $74.1 million to $196.2 million. Operating cash flow surged from $4.8 million to $134.9 million. If we adjust for changes in working capital, it would have risen from $107.4 million to $236.3 million. Even EBITDA showed improvement, skyrocketing from $125.9 million to $301.5 million. Although these year-over-year improvements may seem unbelievably strong relative to the increase in sales, the beauty of capital-intensive companies that have fairly low margins is that even a small improvement in price and volume can have a large impact on the company's bottom line.

{kind=link}

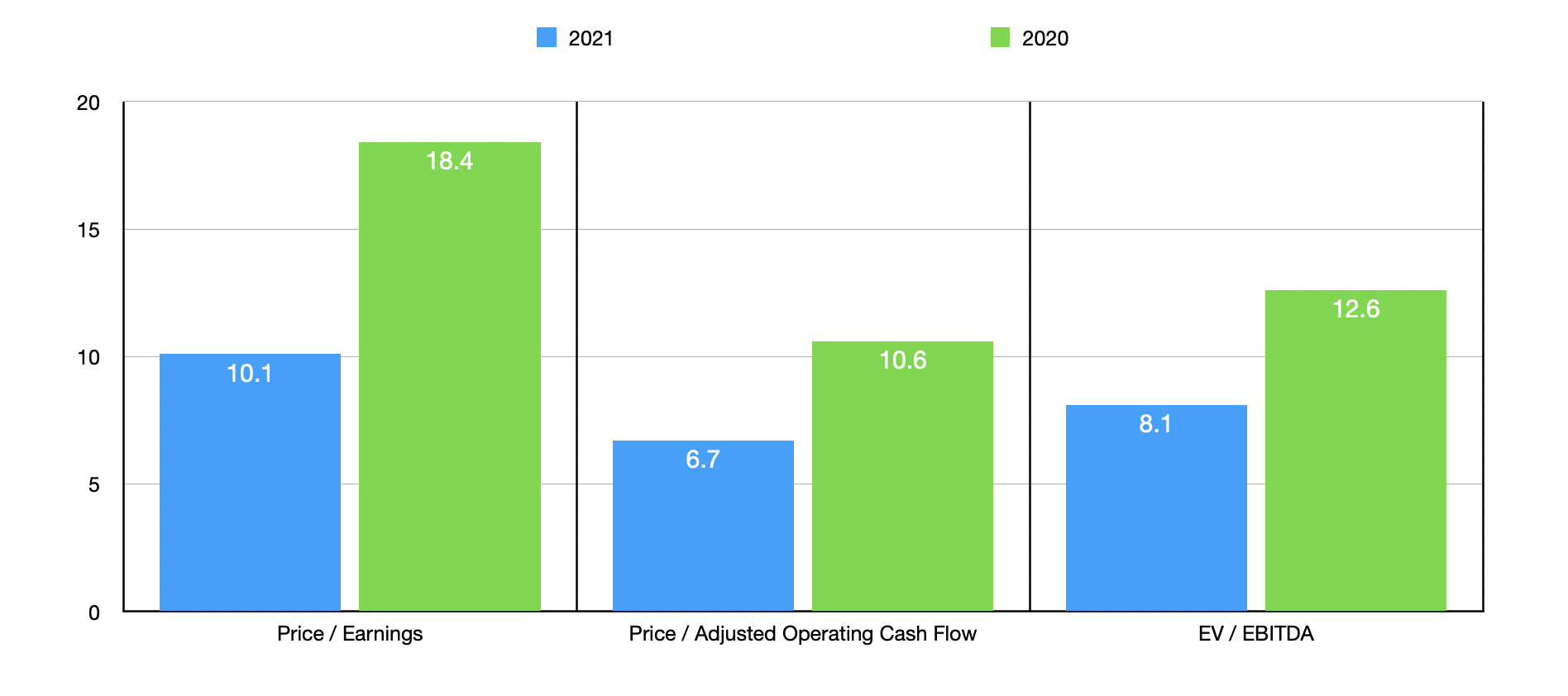

We don't really know what to expect for the rest of the current fiscal year. But instead of projecting out what that picture might look like, I have decided to take the more conservative approach and value the company based on 2021 results, as well as on 2020 results for those who are concerned that the business may experience a return to more normal levels of profitability. Using the 2021 results, the firm is trading at a price-to-earnings multiple of 10.1. This compares to the 18.4 reading that we get if we use the 2020 figures. The price to adjusted operating cash flow multiple should be 6.7. That's down from 10.6 using its 2020 figures. And the EV to EBITDA multiples declined from 12.6 in 2020 to 8.1 for 2021. To put the pricing of the firm into perspective, I compared it to five similar companies. On a price-to-earnings basis, these companies ranged from a low of 3.7 to a high of 61.9. Using the price to operating cash flow approach, the range was from 1.4 to 111.4. In both cases, only one of the companies was cheaper than LCI Industries. Using the EV to EBITDA approach, meanwhile, the range was from 3.1 to 17.2. In this scenario, two of the five companies were cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| LCI Industries |

| 10.1 |

| 6.7 |

| 8.1 |

| Visteon ( VC ) |

| 61.9 |

| 111.4 |

| 15.0 |

| Adient ( ADNT ) |

| 3.7 |

| 20.7 |

| 3.1 |

| Fox Factory Holding Corp ( FOXF ) |

| 20.9 |

| 65.9 |

| 15.3 |

| Dorman Products ( DORM ) |

| 26.6 |

| 34.7 |

| 17.2 |

| Superior Industries International ( SUP ) |

| N/A |

| 1.4 |

| 3.8 |

Takeaway

Although investors are experiencing some pain right now, I do think that the best solution might be to consider doubling down on the company. Shares have gotten much cheaper than they were previously and this ignores the possibility of a stellar 2022 fiscal year. Given how cheap shares are and the very high probability that even a return to 2020 levels would still see the company trading at attractive prices, I cannot help but to retain my ‘buy’ rating on the business at this time. This point is further bolstered by the fact that, in May of this year, management announced a new $200 million share buyback program. At current prices, that would buy back roughly 6.9% of the company's outstanding stock. That is a further reward for investors at a time when shares are quite cheap.

For further details see:

LCI Industries: Recent Declines Ignore Real Strength