LCII - LCI Industries: Temporary Headwinds Cloud Long-Term Earnings Level

2023-11-03 08:00:00 ET

Summary

- LCI Industries produces components for the RV industry, along with other segments.

- The company has experienced lower demand in recent quarters after a heightened demand during the pandemic.

- On a long-term basis, LCI has been able to grow organically and through constant acquisitions with mostly stable margins.

- My DCF model estimates the stock to be nearly fairly valued with long-term estimates that I see as reasonable, constituting a hold rating.

LCI Industries (LCII) produces components for the RV industry as well as other applications. The company has had tough quarters as LCI's customers have ordered a significantly lower number of components compared to the boosted financials caused by the pandemic. It is partly unclear, what sort of a revenue level LCI's operations will stabilize at. To estimate a fair value and an implied level of operations, I constructed a discounted cash flow model in my usual way.

The Company & Stock

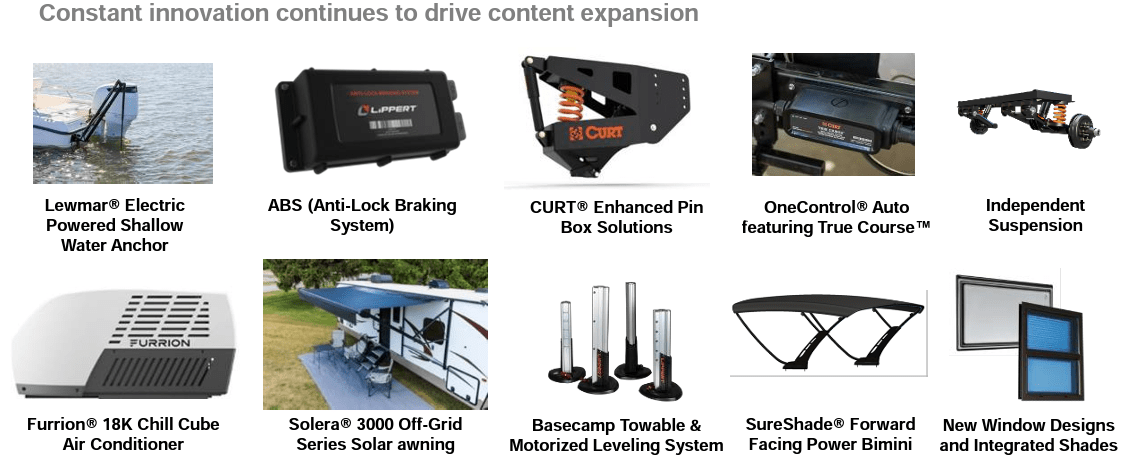

LCI Industries manufactures highly engineered components for RVs, buses, trailers, trucks, boats, trains, as well as other use cases. The company mostly sells its products to large OEMs. Historically, LCI began as a manufactured housing seller, but has turned its operations more into the current offering of selling components to vehicles. As can be seen, the components are quite complicated in terms of manufacturing and engineering, as LCI produces products such as ABS systems, air conditioners, and suspension systems:

{kind=link}

LCI's RV segment saw a massive increase in demand during the Covid pandemic. As OEMs saw a large increase in the demand for leisure-related RV orders, and supply chains were largely disturbed resulting in manufacturers stocking up inventories, LCI achieved a very good amount of growth in the period from 2020 to 2022.

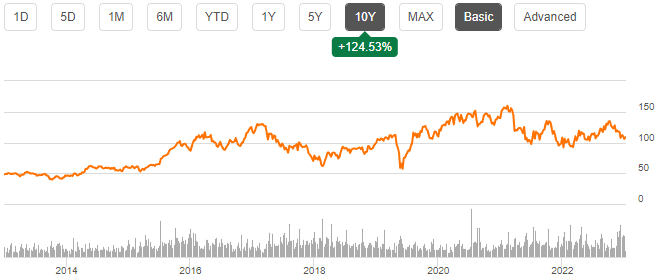

LCI's stock has performed quite well. The stock has appreciated by a CAGR of 8.4% in the past ten years, with an additional dividend yield on top. Currently, the stock yields a fairly good dividend with a forward figure of 3.87%.

{kind=link}

Financials

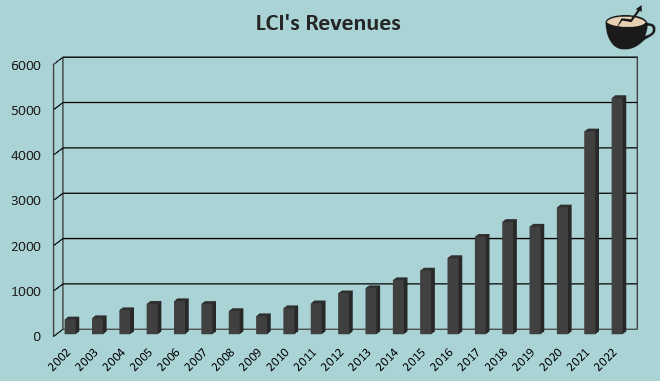

LCI's revenue history is very good. The company has had a compounded annual growth rate of 14.9% from 2002 to 2022, with more challenging periods during the great financial crisis and in the current year. Altogether, the clear trend has been a mostly consistent level of growth:

{kind=link}

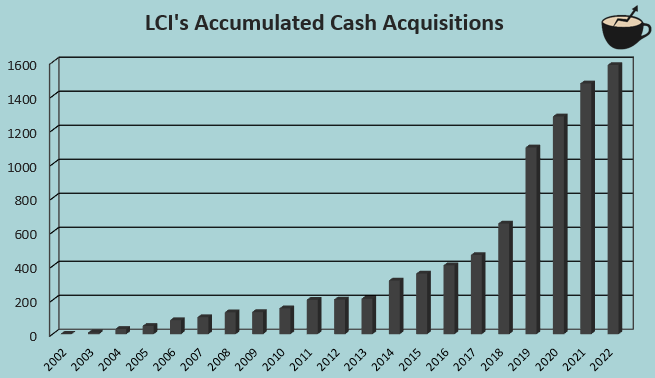

The achieved growth is partly a result of a large number of acquisitions. In total, LCI's cash acquisitions have added up to a figure of almost $1.6 billion from 2002 to 2022. The acquisitions add up to a significant part of the current company, as LCI's current market capitalization is around $2.7 billion. LCI does boast an organic CAGR of 19.2% from 2018 to 2022 in the company's August presentation , but I don't see the period as representative of LCI's sustainable growth rate; from 2020 to 2022, revenues grew sharply due to the pandemic.

{kind=link}

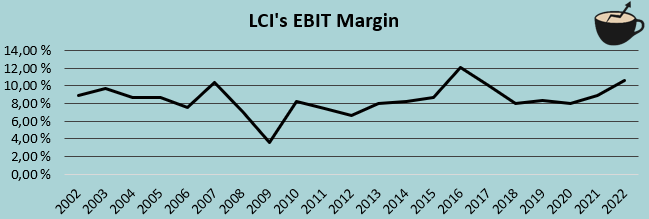

LCI has had a mostly consistent EBIT margin. From 2002 to 2022, the average margin has been 8.5% with a margin of 10.6% achieved in 2022:

{kind=link}

On a more short-term basis, LCI has had troubles in the company's financials. In the second half of 2022, the company's revenues decreased by -14.8%, and in the first half of 2023, the decreases widened to a figure of -37.5%. As LCI's revenues were extremely boosted during the pandemic with a 2021 growth of 60%, the current decreases are mostly a normalization in LCI's operations. As the revenues took a leap down, LCI's EBIT margin has also decreased massively to a current trailing figure of 3.5%, significantly below the company's long-term average. I would expect the margin to recover partly in 2024 and forward, but the future revenue level is somewhat unclear.

Valuation

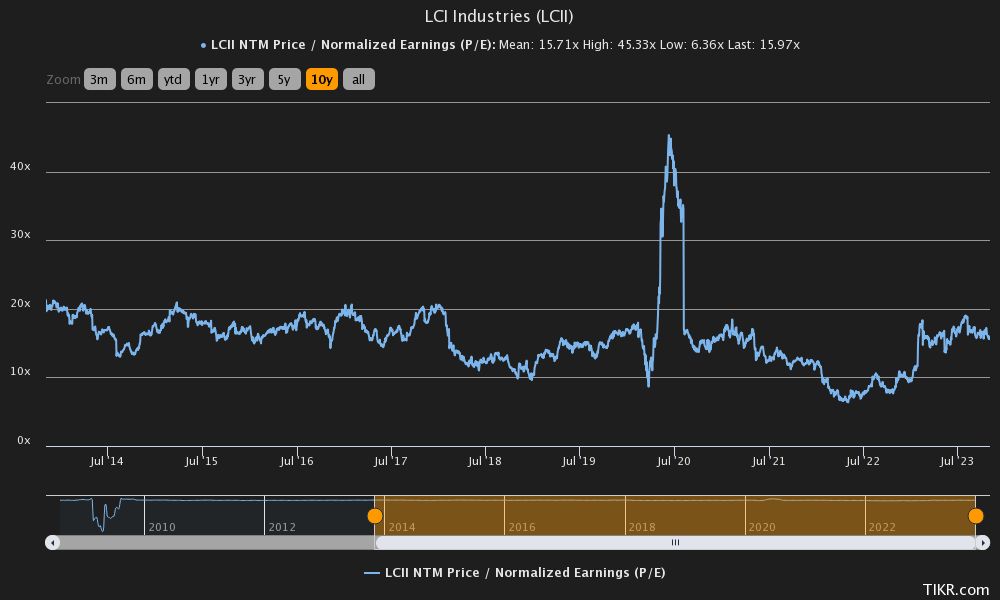

LCI currently trades at a forward P/E ratio of 16.0. The ratio is extremely near the company's ten-year average of 15.7:

{kind=link}

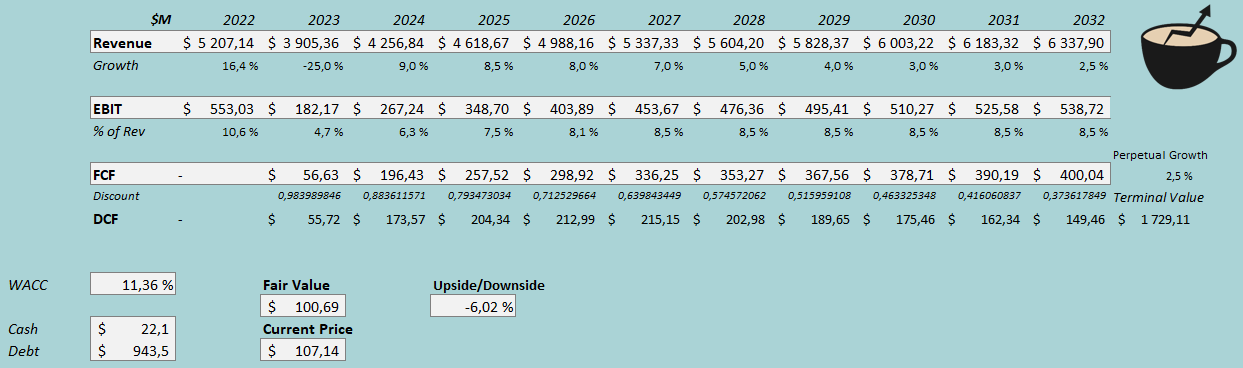

As usual, I constructed a discounted cash flow model to analyse the company's valuation further and to estimate a rough fair value for the stock. In the model, I estimate LCI's revenues to decrease by 25% in 2023, near the current analysts' consensus estimate . The estimate implies a lower decrease in H2 of 2023, which I see as likely as comparison figures are already soft. After 2023, I estimate LCI's revenues to jump back by 9% in 2024 as OEM inventories normalize and demand for RVs increases. Beyond 2024, I estimate the growth to slow down in steps into a perpetual growth rate of 2.5%. Altogether, the estimates represent a CAGR of 5.0% from 2023 to 2032.

After a challenging 2023 in terms of margins, I believe that LCI's EBIT margin should recover in the coming years. For 2023, I estimate a margin of 4.7%, widely below LCI's long-term average and 2022 margin. After 2023, I estimate the margin to scale back in steps into a margin of 8.5% - the estimated margin is LCI's average EBIT margin from 2002 to 2022. The margin of 8.5% is achieved in 2027 in the model.

The mentioned estimates along with a weighted average cost of capital of 11.36% craft the following DCF model with a fair value estimate of $100.69, around 6% below the price at the time of writing. It seems that markets are pricing in a future for LCI that I see as a reasonable level to estimate. It is important to note, that the DCF model doesn't account for further value-adding acquisitions, as the model only factors in organic performance - the estimated value could be lower than with the acquisitions accounted for.

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, LCI had $10.3 million in interest expenses. With the company's current amount of long-term debt, LCI's annualized interest rate comes up to 4.35%. The company uses a good amount of debt despite operating in a quite cyclical industry - I estimate LCI's long-term debt-to-equity ratio to be 25%. On the cost of equity side, I use the United States' 10-year bond yield of 4.85% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the United States, made in July. Yahoo Finance estimates LCI's beta at a figure of 1.49 . Finally, I add a small liquidity premium of 0.4% into the cost of equity, crafting the figure at 14.06% and the WACC at 11.36%.

Takeaway

As LCI's operations have fluctuated due to the heightened Covid pandemic demand and weak revenues afterward, LCI's sustainable revenue level is partly unclear. I believe that the stock currently prices in the company's earnings capabilities quite correctly, as my DCF model estimates would correspond to a fairly valued stock. For the time being, I have a hold rating for the stock.

For further details see:

LCI Industries: Temporary Headwinds Cloud Long-Term Earnings Level