LDP - LDP: An Attractive Discount For This Preferred Fund

2023-08-08 12:37:24 ET

Summary

- Cohen & Steers Limited Duration Preferred and Income Fund (LDP) is an attractive preferred closed-end fund trading at a discount.

- Preferred investments took a big hit during the banking crisis earlier this year and haven't fully recovered, making them an attractive area of the market.

- LDP has trimmed its distribution to match declining coverage, but its interest rate swap hedges have provided offsetting gains.

Written by Nick Ackerman, co-produced by Stanford Chemist.

We recently covered Cohen & Steers Tax-Advantaged Preferred Securities and Income Fun d ( PTA ) , and that remains an attractive preferred closed-end fund to consider. However, Cohen & Steers ( CNS ) offers a couple of other preferred focused CEFs, one of those being the Cohen & Steers Limited Duration Preferred and Income Fund ( LDP ) , which is also looking equally as attractive at a tempting discount now.

The Basics

- 1-Year Z-score: -0.34

- Discount: -8.16%

- Distribution Yield: 8.67%

- Expense Ratio: 1.23%

- Leverage: 35.79%

- Managed Assets: $880.11 million

- Structure: Perpetual

LDP's investment objective is "high current income through investment in preferred and other income securities. The secondary investment objective is capital appreciation." As stated, they attempt to achieve this through investing in preferred and income securities, but they leave it quite flexible. That can include "U.S. and non-U.S. companies like banks, insurance companies, REITs, other diversified financials as well as utility, energy, pipeline and telecommunication companies."

Unlike PTA, LDP is a perpetual fund with no anticipated liquidation date in the future. This would be because this is an older CEF 1.0 fund that launched in July 2012. Funds launched after 2018 can be referred to as CEF 2.0 launches as these funds generally launch with term structures, and the launching costs are all absorbed by the fund sponsor launching the fund. As a quick reminder, before this, the fund itself bore the launch costs. That's why LDP launched at a $25 market price but a NAV inception of $23.83.

Despite being a small fund, the fund's expense ratio is lower than PTA's. LDP is about half the total assets compared to PTA at closer to $1.65 billion. LDP's total expense ratio climbs to 2.0 when leverage expenses are included. This is likely higher now and will be reflected in the next semi-annual report when it's posted. However, that's the data we have to go from as of the last annual report .

Performance - Tempting Discount

This is not a fund I've covered previously, as PTA generally has offered the better entry valuation based on the discount the fund had traded at. However, Their discounts have been tracking much more closely these days and are nearly identical to the latest closing.

YCharts

At one point, LDP commanded a premium, but that quickly changed as we entered this year. In particular, a massive hit in the preferred space with a couple of bank failures earlier in the year had turned the whole preferred space quite sour. Then you throw on a bit of leverage that LDP employs on top of that, and the results would have been under even more pressure.

Interestingly though, in the last year, in terms of total NAV returns, LDP has been able to outmaneuver the passively non-leveraged iShares Preferred & Income Securities ETF ( PFF ) - often seen as one of the broader benchmarks for the preferred space. LDP has been able to best its PTA sister too. This outperformance was at least partially likely attributed to due to the lower duration of LDP relative to PTA.

YCharts

In looking at the longer term over the last decade, LDP is now presenting investors with an opportunity to pick up shares well below its average discount. While interest rates have been low for most of the last decade, this difference compensates for some of that changing environment. The discount is more similar to the 2015-2016 levels that we saw before LDP started making its move toward a premium to NAV.

YCharts

Distribution - Trims As Coverage Declines Seem Appropriate

One reason for added pressure on LDP is that this fund has been cutting its distribution while they've continued to maintain PTA's same distribution. The latest distribution cut came in just this last quarter when it was announced for the July, August and September payouts.

In fact, I've found it odd that PTA has maintained its distribution, but perhaps it's because they are a newer fund. They don't want to scare investors away any more than the performance already has. Or alternatively, they are just banking on the gains they can produce going forward to eventually cover the payout.

These cuts seem appropriate as distribution coverage sunk due to rising borrowing costs.

{kind=link}

The new annualized rate for the distribution would come in at $1.572. The total shares outstanding at 29,079,221, and with that info, we can come up with the fund's distributions going forward coming out to around $45.713 million annually. In previous years the fund had issued shares due to trading at a premium; they aren't in a position where shares should be being issued anymore now that they are at a discount.

Fortunately, CNS was one of the fund sponsors that got out ahead of the rising interest rates by implementing interest rate swaps to help provide some hedging against the rising costs.

LDP Leverage Facts (Cohen & Steers)

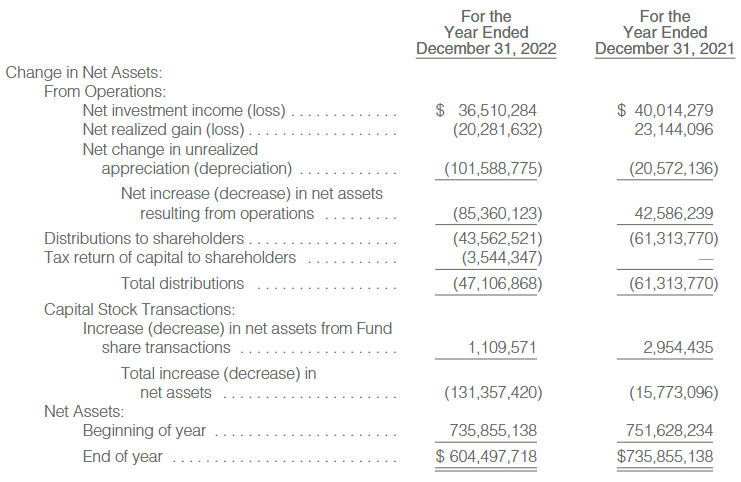

So that has meant that where net investment income has been coming to light, they've had these hedges in place to provide offsetting gains. Capital gains will still be required to cover their distribution despite the trims the fund has gone through.

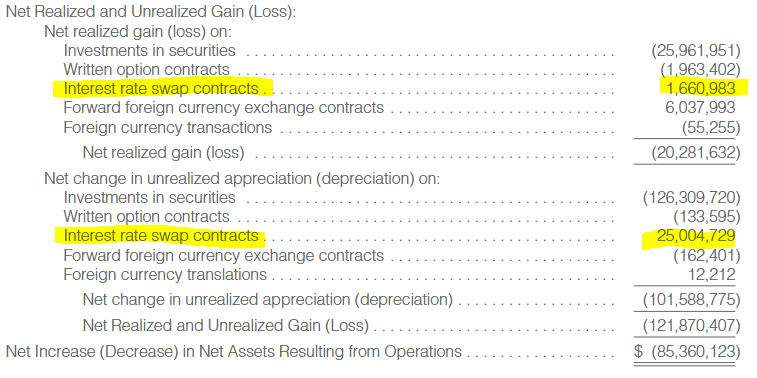

LDP Realized/Unrealized Gains/Losses (Cohen & Steers (highlights from author))

{kind=link}

In addition to the interest rate swap derivatives, the fund has also implemented options writing in the form of "swaptions" and binary options. Unfortunately, that had produced losses for the fund in the prior year.

The Fund also engaged in “swaptions,” which are options to enter into interest rate swap contracts with the intention of managing interest rate risk. Additionally, the Fund invested in binary options (currency and European Index put options) with the intention of managing volatility in certain European holdings. These contracts did not have a material effect on the Fund’s total return for the 12-month period ended December 31, 2022.

LDP's Portfolio

They're fairly active in terms of turnover for this fund, with the latest portfolio turnover rate at 47%. That was fairly consistent with the prior year's 48% but slower than 2020 when turnover came in at a relatively elevated 72%.

The "limited duration" part of the fund's name is in reference to seeking a limited duration for its portfolio. To be exact, they are looking for a duration of 6 years or less. This is in an effort to reduce the impact that rising interest rates would have on the fund. The average modified duration as of their last fact sheet for the period ending June 30th, 2023 , came to 3.3 years.

For some context, PTA's duration was reported at 4.6 years, and its other sister, Cohen & Steers Select Preferred and Income Fund ( PSF ), came in at 5.5 years. So relatively speaking, LDP is fairly limited in terms of its duration. However, with the banking failure, that limited duration seemed of little support when everything in the preferred space was crashing.

This is because, similar to most other preferred and income CEFs on the market, they are dominated by banking and insurance companies. Financial companies often issue preferred because it can help with their regulatory ratios when they issue non-cumulative perpetual preferred.

LDP Sector Exposure (Cohen & Steers)

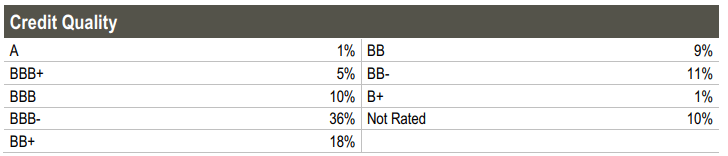

The majority of the portfolio is rated investment-grade, though they carry a fair bit of below-investment-grade rated holdings as well. Despite having a generally higher credit quality portfolio, that also did little in terms of blunting the downside moves in March.

{kind=link}

Perhaps it's a small consolation because Silicon Valley bank failed when it was rated as investment grade. First Republic was taken over and sold to JPMorgan ( JPM ) , and it, too, was considered investment-grade when initially heading into that crisis. A good reminder that looking at credit ratings from a rating agency is only one metric to consider of many and not where due diligence ends.

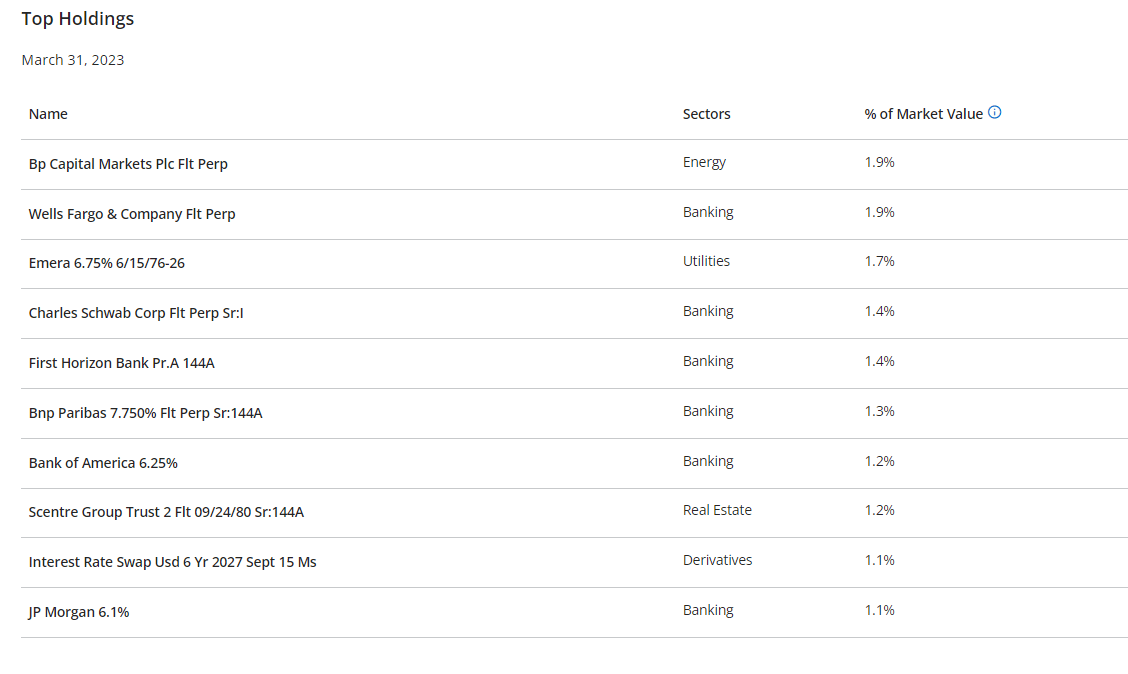

In looking at the largest holdings, we see some exposure to some of the largest financial institutions in the world. That includes JPM, Bank of America ( BAC ) and Wells Fargo ( WFC ) . These are the "too big to fail" banks, as it would send devastating ripples throughout the entire economy if we were ever in a scenario where one of these failed. Therefore, they could be seen as quite safe - albeit that doesn't always mean that shareholders and debt holders couldn't participate in some losses.

{kind=link}

On the other hand, another way to stay safer is to stay highly diversified, and LDP offers exposure to 267 different holdings. While concentrated within the financial industries of banks and insurance, that can still offer some comfort with the expectation that not everything should fail simultaneously.

Conclusion

LDP trades at an attractive discount and offers exposure to a preferred and income-oriented portfolio. They've trimmed their distribution to better match coverage in the net investment income being earned. That is to say, as NII has decreased, the distribution should also ideally decrease.

At the same time, their interest rate swap hedges have effectively provided offsetting gains to hedge against some losses. Given the financial stability has returned compared to the uncertainty we had earlier this year in the banking crisis, preferreds can still offer an attractive area to invest. This is particularly true if an investor is under the expectation that the Fed is close to being done hiking interest rates. At the same time, LDP is in a position with a lower duration that should help make it relatively less interest rate sensitive.

For further details see:

LDP: An Attractive Discount For This Preferred Fund