LDP - LDP: Earn Income With This CEF

2023-05-19 17:13:36 ET

Summary

- Investors today are desperate for more income as the rising cost of living in most countries has strained the budgets of many people.

- Cohen & Steers Limited Duration Preferred and Income Fund, Inc. invests in a portfolio of high-yielding preferred stocks and bonds in order to provide a high level of current income for its investors.

- The LDP closed-end fund has been affected significantly by rising interest rates, although the portfolio has held up much better than the fund's share price.

- The fund yields 9.57% but it has failed to cover its distribution in both of the past two years, which is quite concerning.

- The Cohen & Steers Limited Duration Preferred and Income Fund, Inc CEF currently has a reasonably attractive valuation.

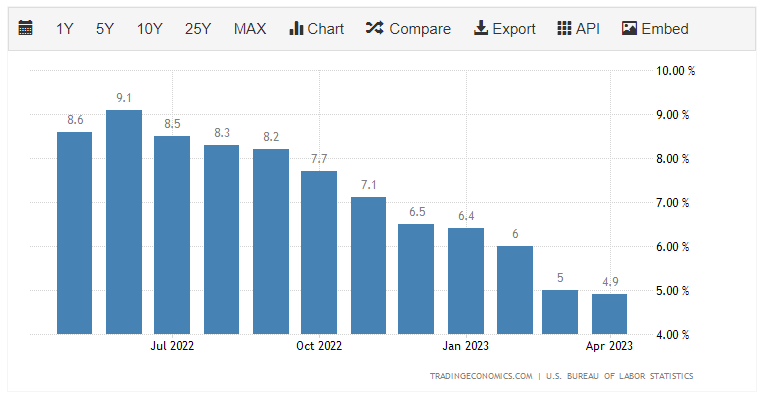

There can be little doubt that one of the biggest problems the average American household faces today is the rapidly-increasing cost of living. This is evidenced by the consumer price index, which claims to measure the cost of a basket of goods purchased regularly by an average person. As we can see here, the index has posted at least a 6% increase year-over-year in ten of the past twelve months:

{kind=link}

Although the reported rate of inflation has fallen in recent months, it still remains well above the 2% that policymakers consider to be healthy. As I pointed out in a recent blog post too, the reported rate of inflation is somewhat misleading because it has been entirely caused by the decline in energy prices that we have seen over the past few months. The core consumer price index, which excludes food and energy prices, has proven to be much more resistant to drops. This has caused stress for consumers, especially those with limited financial means. According to Bloomberg , 89.1 million Americans were found to experience difficulty paying their expenses between late April and early May, representing a significant increase over the same period last year. That is surprising considering that energy prices are much lower now. The point here is that many Americans are desperate for extra sources of income just to keep their bills paid and their bellies full.

As investors, we are not immune to this. After all, we have expenses as consumers just like anyone else. However, we do have the ability to put our money to work for us to earn the extra incomes that we need to maintain our lifestyles. One of the best ways to accomplish this is to purchase shares of a closed-end fund, or CEF, that specializes in income. These funds are unfortunately not very well-followed in the investment media, so it can be difficult to obtain the information that we would like to have in order to make an informed decision. This is a shame because these funds have a number of advantages over open-ended and exchange-traded funds. In particular, they have the ability to employ certain strategies that can boost the yields of their portfolios above that of any of the underlying assets or indeed pretty much anything else in the market.

In this article, we will discuss the Cohen & Steers Limited Duration Preferred and Income Fund, Inc. ( LDP ), which currently boasts a very impressive 9.57% yield. That is easily enough to appeal to any income-seeking investor. I have discussed the LDP closed-end fund before, but a great deal of time has passed since then. As such, several things have changed. This article will therefore focus specifically on these changes as well as provide an updated analysis of the fund's finances.

About The Fund

According to the fund's webpage , the Cohen & Steers Limited Duration Preferred and Income Fund has the stated objective of providing its investors with a high level of current income. This makes a great deal of sense as the name of the fund implies that it will be investing primarily in preferred stocks or other fixed-income securities. The portfolio composition confirms this strategy as the fund is currently invested primarily in bonds, although it does have a substantial allocation to preferred stock:

CEF Connect

The reason that this objective is not surprising is that these securities deliver their returns primarily through direct payments made to shareholders. A bond simply makes regular coupon payments to its shareholders and then pays the face value at maturity. A preferred stock pays a fixed dividend to its shareholders on a regular schedule. As neither one of these securities has any link to the growth and prosperity of the issuing company, neither one promises any capital gains potential. In fact, anyone purchasing a brand-new bond at issuance and holding it to maturity is guaranteed not to realize any capital gains. Thus, it makes a great deal of sense for any fund investing in these securities to target the provision income for their shareholders as an investment objective.

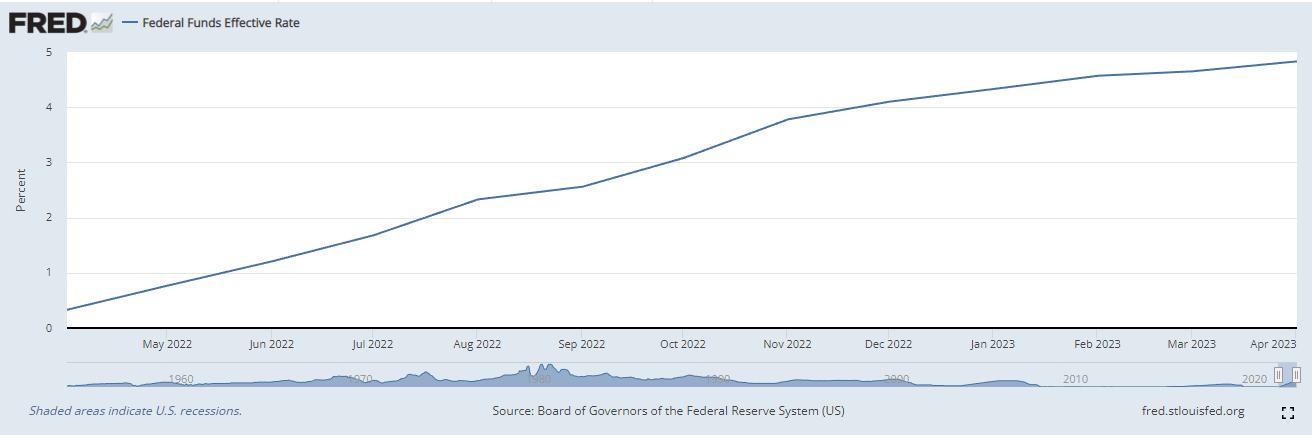

At this point, readers will undoubtedly point out that several bond funds have a history of producing capital gains for their investors. This comes from the fact that both bond and preferred stock prices vary based on interest rates. It is an inverse relationship, so when interest rates go up, bond prices go down and vice versa. That is something that is very important today because the Federal Reserve has been aggressively raising interest rates to combat the incredibly high inflation in the United States. As we can see here, the effective federal funds rate has risen from 0.33% a year ago to 4.83% today:

{kind=link}

We see a similar trend in many other nations, as China and Japan are the only two nations in the G20 that have not raised interest rates over the past year. The Federal Reserve has been somewhat more aggressive than other major central banks though, and it has an outsized impact on global bond markets due to the reserve currency status of the U.S. dollar.

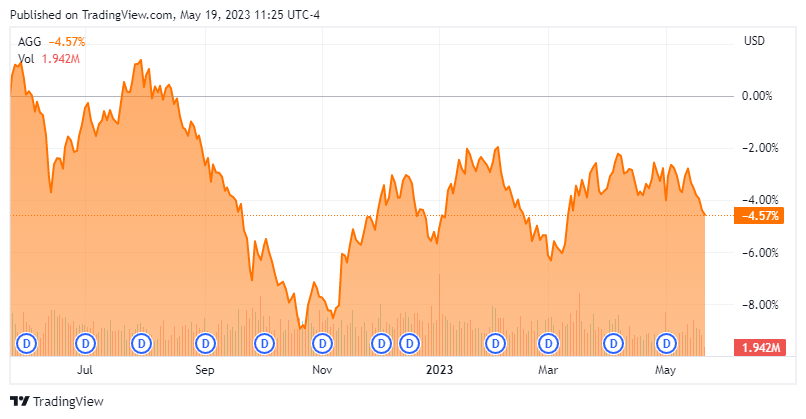

As we might expect because of the just-mentioned relationship between interest rates and bond prices, the bond market was devastated by the Federal Reserve's actions. Over the past year, the Bloomberg U.S. Aggregate Bond Index ( AGG ) has declined by 4.57%:

{kind=link}

We can see that the index was down much more during October and November of last year, but has since rebounded. This rebound was mostly due to the market expecting that the U.S. economy will enter a recession that will force the Federal Reserve to start quantitative easing once again. However, recent comments by the Federal Reserve suggest that this outcome is unlikely. Thus, we could see a correction in bond prices if the optimistic scenario currently being priced in does not play out.

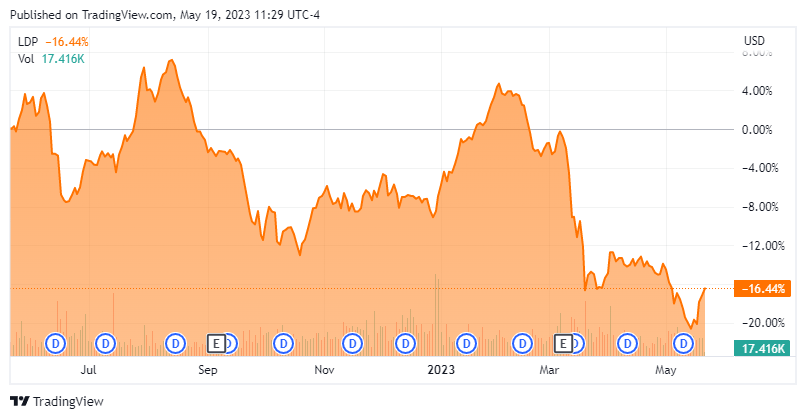

The Cohen & Steers Limited Duration Preferred and Income Fund has certainly not been spared from the carnage that we have seen in the bond market. This fund is down significantly more than the index, falling 16.44% over the past year:

{kind=link}

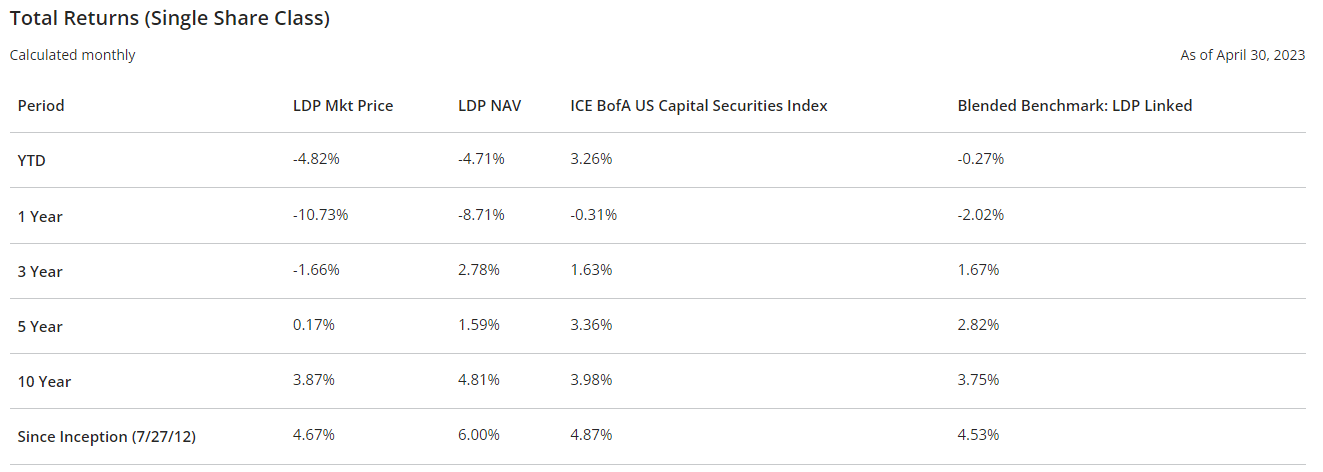

The fact that this fund has underperformed the index so significantly over the past year will likely prove somewhat disappointing. However, this may be somewhat misleading. First, the fund possesses a much higher yield than the aggregate bond index, which offsets some of the declines that we see above. Indeed, someone that reinvested the fund's distributions would not have lost anywhere close to 16.44% over the past year. During the full-year period that ended on April 30, 2023, the fund's shares had a total return of -10.73%:

{kind=link}

That is disappointing and still represents an underperformance of the bond index, but it is not nearly as bad as implied by the share price performance alone. As I have pointed out before, it is not uncommon for shares of a closed-end fund to underperform the fund's own portfolio. This is because a closed-end fund does not continually offer and redeem shares to maintain a link between the portfolio and the market price. As we can see above, the fund's actual portfolio only delivered a -8.71% total return over the trailing one-year period, which is a better performance than the shares delivered in the market. The fact that the shares do sometimes underperform the actual portfolio can sometimes create an opportunity to purchase the fund's assets for less than they are actually worth, which we will discuss later in this article.

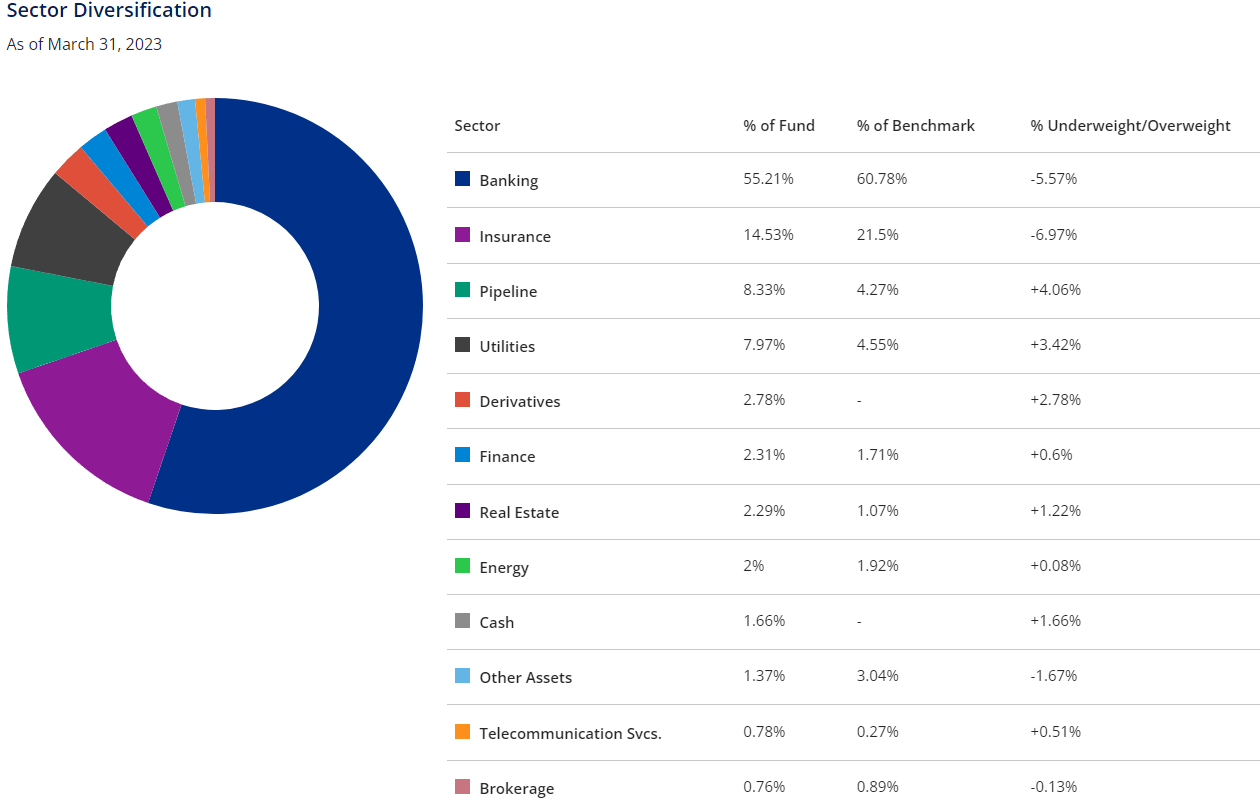

In my previous article on this fund, I pointed out that the Cohen & Steers Limited Duration Preferred and Income Fund is heavily weighted toward the banking sector. This is still the case, as 55.21% of the fund is invested in the banking sector:

{kind=link}

This is something that may be concerning to some readers today considering that there have been several bank failures over the past month. In fact, 2023 is the worst year for bank failures in history when measured by the assets of the failed banks. However, the fund's allocation to banking has dropped significantly from the 63% that it had the last time that we looked at the fund. Thus, the fund appears to be reducing its exposure to the sector in light of the risks that have emerged recently. That shows that management is being proactive, which will probably be somewhat comforting for investors.

It is not unusual for a fund that focuses on preferred stocks to be heavily invested in the banking sector. This is because banks are by far the biggest issuers of preferred stock due to international banking regulations. In short, regulations require that banks maintain a certain percentage of their assets in the form of Tier One capital. Tier one capital is that portion of a bank's total assets that are not simultaneously a liability to someone else, such as a depositor or a creditor. When regulations require a bank to increase its Tier One capital, it must issue either common stock or preferred stock. Most banks will opt to issue preferred stock in order to avoid diluting the common stockholders. As companies in other sectors do not have these regulations, they will usually issue debt when they need to raise capital as debt is much cheaper than preferred stock.

Thus, banks are the largest issuers of preferred stock in the market by default, and any preferred stock fund will have an outsized allocation to the sector. As shown above, this fund is actually underweight to the sector compared to its benchmark index, which is another sign that the fund is doing what it can to minimize its exposure to the sector right now.

Leverage

In the introduction to this article, I stated that closed-end funds like the Cohen & Steers Limited Duration Preferred and Income Fund have the ability to employ certain strategies that can boost their effective yields well beyond that of any of the underlying assets. One of these strategies is the use of leverage. Basically, the fund borrows money and uses that borrowed money to purchase preferred stock and bonds. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will normally be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This may be one reason why the fund and its portfolio fell more than its benchmark indices did over the past year. As such, we want to ensure that the fund is not using too much leverage because that would expose us to too much risk. I do not usually like a fund's leverage to exceed a third as a percentage of its assets for this reason.

Unfortunately, this fund does somewhat exceed this limit, as its levered assets comprise 36.49% of the portfolio as of the time of writing. While this is not exactly what we were hoping to see, fixed-income funds can carry a bit more leverage than equity funds because their assets are somewhat less volatile. Thus, this fund is probably okay in terms of the balance between the risk and the reward but I would still be more comfortable with slightly less leverage.

Distribution Analysis

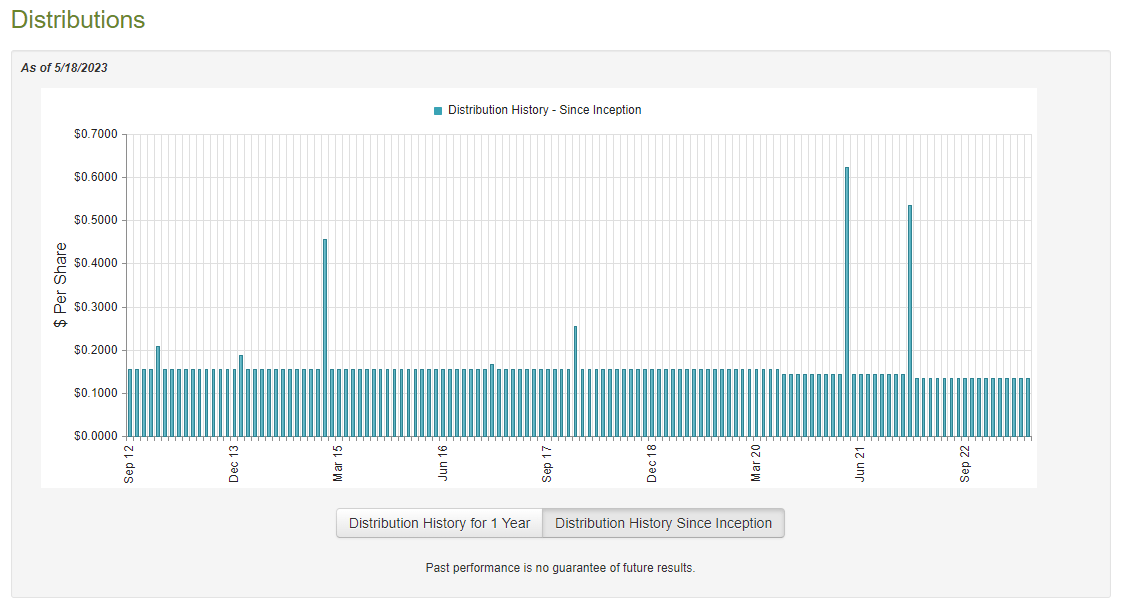

As stated earlier in this article, I stated that the primary objective of the Cohen & Steers Limited Duration Preferred and Income Fund is to provide its investors with a high level of current income. In order to achieve this objective, the fund purchases preferred stock and bonds, which tend to have reasonable yields as they provide their investment return primarily through direct payments to the investors. This fund then applies a layer of leverage on top of these securities to boost the effective portfolio yield. As such, we might assume that the fund itself would boast a very high yield. This is certainly the case, as it pays a monthly distribution of $0.1350 per share ($1.62 per share annually), which gives the fund a 9.57% yield at the current price. This fund has been reasonably consistent about its distribution over the years, but it has not been perfect:

{kind=link}

For the most part, this distribution history is better than most fixed-income funds. However, we can see that the fund has cut its payout twice over the past three years (although not in the past twelve months). This might prove to be a turn-off for any investor that is seeking a stable and secure source of income to use to pay their bills or finance their lifestyles. However, anyone buying the fund today does not have to worry about the fund's history, as they will be receiving the current distribution at the current yield. As such, the most important thing for anyone buying shares of the fund today is how well it can afford to maintain the current distribution. Let us investigate that.

Fortunately, we have a relatively recent document that we can consult for that purpose. The fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. This is a much newer report than the one that we had available the last time that we reviewed this fund, which is nice because this report will give us a much better idea of how well the fund navigated the challenging market climate last year. During the full-year period, the Cohen & Steers Limited Duration Preferred and Income Fund received $44,938,375 in interest and $7,602,976 in dividends from the assets in its portfolio. This gives the fund a total investment income of $52,541,351 over the period. It paid its expenses out of this amount, which left it with $36,510,284 available for shareholders.

That was, however, not nearly enough to cover the $47,106,868 that the fund actually paid out during the period. This is something that is likely to be concerning at first glance, as the fund did not have sufficient net investment income to cover its distributions.

However, there are other ways through which the fund can obtain the money that it needs to cover the distributions. For example, it might be able to earn some money via capital gains that can be paid out to the investors. As might be expected given the harsh bond market last year, the fund failed at this task. During the full-year period, it reported net realized losses of $20,281,632 and had another $101,588,775 net unrealized losses. Overall, the fund's assets fell by $131,357,420 after accounting for all inflows and outflows. This follows a $15,773,096 decline that the fund's portfolio suffered in the full-year 2021 period.

Thus, the Cohen & Steers Limited Duration Preferred and Income Fund, Inc failed to cover its distribution for two consecutive years. That is certainly not encouraging and could be a sign that it may have to cut the payout again in the near future.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Cohen & Steers Limited Duration Preferred and Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of May 18, 2023 (the most recent date for which data is available as of the time of writing), the Cohen & Steers Limited Duration Preferred and Income Fund had a net asset value of $18.85 per share, but the shares currently trade for $16.96 each.

That gives the Cohen & Steers Limited Duration Preferred and Income Fund, Inc's shares a 10.03% discount to net asset value at the current price. This is somewhat better than the 8.62% discount that the shares have averaged over the past month, so the price certainly looks reasonable today.

Conclusion

In conclusion, the Cohen & Steers Limited Duration Preferred and Income Fund appears to be a reasonable way for an investor to earn a high level of income today. The fund's high exposure to the banking sector may be concerning given the numerous high profiles that we have seen in that sector over the past several months, but the fund is taking steps to reduce its risks and it has less exposure to the sector than it had a few months ago. The biggest concern here is that this fund has failed to cover its distribution for two consecutive years, so it may be forced to cut its payout at some point. The price for Cohen & Steers Limited Duration Preferred and Income Fund, Inc. is reasonable, though, so it might still be worth buying today.

For further details see:

LDP: Earn Income With This CEF