VT - Leading Indicators Are Deteriorating; It's Time To Sell The Indices

2023-07-11 06:16:12 ET

Summary

- Bottom-up investing is becoming much harder as stocks trade in different ways to how they have historically.

- Up to 80% of single stock flows are now driven by index and industry level moves.

- Having a comprehensive view of the macro environment is now key to competing in the modern markets and minimizing opportunity cost.

- The outlook for Global GDP is grim, overall, with India as the lone bright spot.

- This has negative implications for S&P 500 / global stock performance over the next 6 months or so. We establish a case for trimming positions and waiting for a clearer economic picture.

When it comes to managing a portfolio of assets, some investors approach things from the "bottom up", analyzing individual stocks with a one-at-a-time approach. In this framework, new potential investment ideas are sourced via casual browsing, and then as companies become sufficiently interesting, they're dug into on a deeper level.

As a result, many analysts end up covering a "stable" of their favorite stories for long periods of time, keenly aware of business drivers and, to some degree, the effect that the larger economy has on earnings and financial performance. Many investors, Warren Buffett included, have found success with this method.

Bottom Up Is Getting Harder

However, if you're anything like us, you may find it difficult to operate in the financial markets like this.

With over 4,000 publicly listed equities in the United States alone, it's impossible to cover them all. The potential for high opportunity cost is tremendous. Plus, when it comes to resources, everyone has a finite amount of time and effort.

Even more importantly, being a bottom-up investor isn't as effective as it once was.

As trillions have been sucked into indexing and passive investing ( SPY , VT ), there has been a massive shift in the way markets work.

Before, individual companies each had robust markets for their stock, and their stock alone.

Now, many stocks without mega cap status or highly interesting company narratives, like Tesla ( TSLA ) are very thinly traded. Fund flows, which used to be derived from the performance of underlying stocks, are now the driver of a majority of trades in most stocks on most days.

Things are now operating in reverse.

But why does this matter?

Back when we worked as professional traders, we had an informal observation that we often referenced on our desk: the "50/30/20" rule. It stood for this:

- 50% of flows are driven by the Index

- 30% of flows are driven by the Sector

- 20% of flows are driven by the Stock Itself

Broken down a little more, we often felt that about 50% of order interest in any given stock was driven by market index fund flows. 30% of interest, or thereabouts, we felt came from industry/sector fund flows, and then the remainder of order interest appeared to come from individuals or institutions that actually wanted to trade the single stock in question.

In short, we saw that funds were deciding how they felt about the market as a whole, and then these trades would trickle down to the underlying stocks which then move in the direction of this view.

This isn't true when there's news, obviously, but for most stocks, on most days, this has become the paradigm.

This is why Buffett, the greatest investor of all time, has struggled to outperform the market meaningfully over the last decade plus:

{kind=link}

Top Down Is The Way

Given these insights, there are two key takeaways.

First; it stands to reason that many single stocks are potentially mispriced as a result of the dominance of market-wide flows.

If companies are overlooked as the majority of trades are driven at a macro level, then clearly, it's possible that there are opportunities in under-followed single stocks. The catch is that this doesn't mean that any specific company will re-rate unless the stock becomes "re-discovered" by institutions. Things can stay stagnant for a long period of time as there are less "eyeballs" on single stocks due to the time and brainpower constraints we mentioned above.

Secondly, and more importantly, the most important thing to have, nowadays, is a macroeconomic view. If 80% of the orders that affect the market are coming from views about broader economies or industries, then it pays to be on the same page as the "smart money".

Operating in the modern market without first getting an idea about the direction of the global economy is like playing chess in the dark, which is why we prefer a Top-Down approach.

Approaching the market from the top down can also more quickly tell you where to begin digging for gold.

The Global Economy

This is all a long-winded way to say that today, we'll be breaking down where the global economy is headed, and how this directly affects your money.

When it comes to stocks at a broad level, the price of the market is largely a function of two things: GDP and Liquidity.

If a P/E for a stock is comprised of the earnings (fundamental) and the price (multiple), then the P/E for the market is comprised of GDP growth (fundamental) and liquidity (multiple).

GDP growth comprises the "value", and liquidity conditions often dictate how much to pay for it. Today, we'll take a look at GDP growth. But why does GDP growth affect market fundamentals?

In short, as an aggregate, the profitability of all companies is derived from the size of the economy as a whole.

Bigger economy, more profits.

Smaller economy, less profits.

Thus, predicting GDP is key to predicting the direction of the market.

But how does one predict GDP?

By looking at leading economic indicators.

The Major Economic Regions

While we could look at all global economies to solidify our assessment of the major stock indices, we'll be focusing today on the 6 largest economic regions that drive a majority of business for most U.S. based and global large cap businesses.

This includes: The US, EU, and the UK, as well as China, Japan, and India.

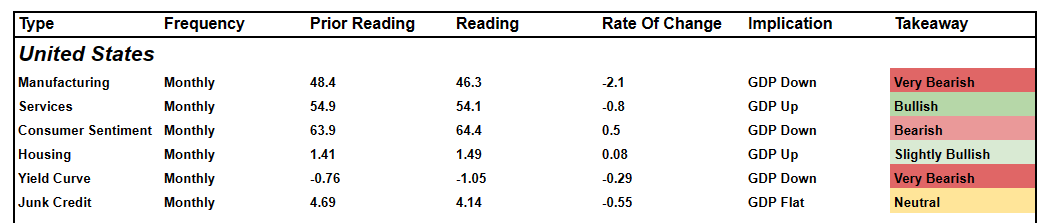

The United States

{kind=link}

Overall, right now, the outlook for U.S. GDP is mixed but deteriorating. Housing improved last month, and Services is still reporting growth with a bullish reading of 54.1, although that did come down from May's reading of 54.9.

On the flip side, Manufacturing is negative and worsening, Consumer Sentiment remains depressed, and the Yield Curve continues to invert, now negative by more than a full percentage point.

Junk Credit retains its "Neutral" rating, which is somewhat surprising to us.

In a normal market, we would be leaning bearish given this combination of information. However, the recent rally in AI stocks and big tech ( MSFT , NVDA , AAPL , META , GOOG , AMZN , TSLA ) has complicated the picture for most investors, fooling many into thinking the market is writing off the economic malaise. In our view, investors are simply speculating on a secular business trend that has unclear implications for productivity on a broad basis.

Thus, we remain bearish and think now presents a great time to trim a position in the indices.

The Euro Area

{kind=link}

The Euro Area and the remaining economic zones have a smaller direct impact on U.S. GDP and S&P 500 performance, but they're still important for determining the ultimate potential direction of all global stocks ( VT ).

In short, the Euro Area seems to be in even worse shape than the U.S., with significantly negative Manufacturing, Housing, and Consumer Sentiment readings.

Combined with a negative (and worsening) Yield Curve, it's tough to see how the only positive metric, Services, can bring any hope to the outlook overall; especially as it fell again this month back towards a neutral reading of 50.

There could be an interesting "Long U.S. Services, Short EU Manufacturing / Housing" trade in the cards for savvy long/short portfolio managers who are so inclined.

We think the Eurozone will likely see slower GDP growth over the next few years as consumer sentiment remains a permanent drag on growth. Although given how far beaten down the region is, any hopeful signs could spark a rally.

The United Kingdom

{kind=link}

The UK's outlook has worsened considerably from May, as Manufacturing, Services and housing all came in lower month-over-month.

Also worrying; the UK's Yield Curve, which inverted by more basis points than any other region this month.

While Services remains a bright spot, we're very dour on the UK's picture overall. We'd steer clear of any prominent cyclical stocks and stick with defensive names for the foreseeable future, especially as the larger EU GDP picture remains iffy.

China

{kind=link}

China is, albeit bumpily, continuing to get its groove back.

Manufacturing remains in growth territory (if only slightly), and services remains a strong point with a reading over 50, although it did weaken month-over-month. Consumer sentiment is also still weak, but the picture continues to improve somewhat from a rate of change perspective.

Our main concern here is Chinese Housing. Housing starts are well behind last year's numbers, and given how important this sector is to the Chinese economy, less starts may mean less demand for commodities, which could trickle into global GDP.

Some expect the government to launch stimulus, but given the demographic / supply situation, we don't see any moves here being particularly effective. Are China's green shoots a strong enough signal to counteract the West's malaise?

We don't think so.

Japan

{kind=link}

After a few strong months of readings, Japan seems to be taking a bit of a breather in June.

We see weakening across the board in Manufacturing, Services, Housing, and the Yield Curve - only Consumer Sentiment improved. However, most of the readings, from a "flat" perspective, are still bullish, which is a positive sign for the Asian island nation.

We're more bullish on Japan than most other regions, but it seems doubtful that relative strength here can offset other data points coming out of in the US, EU, and China.

India

{kind=link}

If there's one region to get excited about, it's India. In short, India remains in an envious global position.

Manufacturing numbers are strong, Services are still indicating growth, and Housing continues to expand at an average rate YoY. Consumer Sentiment is still under 100, but it's growing steadily back towards that number, and the Yield Curve, while somewhat flat, remains positive.

Of all of the global economies, India seems like the best place to hide, and could present interesting positioning opportunities for the remainder of 2023 for tactical traders and portfolio managers. The problem here from a Global GDP perspective is that India is simply too small to move the scale enough, despite its relative strength.

Our View

As we alluded to, net net, we remain somewhat bearish on Global GDP, including major U.S. Equities ( SPY ) as well as global stocks overall ( VT ).

Some have recently made the argument that things remain depressed, and thus good news could surprise to the upside and catalyze a rally. However, considering that things are mostly still getting worse from a rate of change perspective (including the U.S. PMI diving to ~46!), we're not ready to buy into that narrative yet.

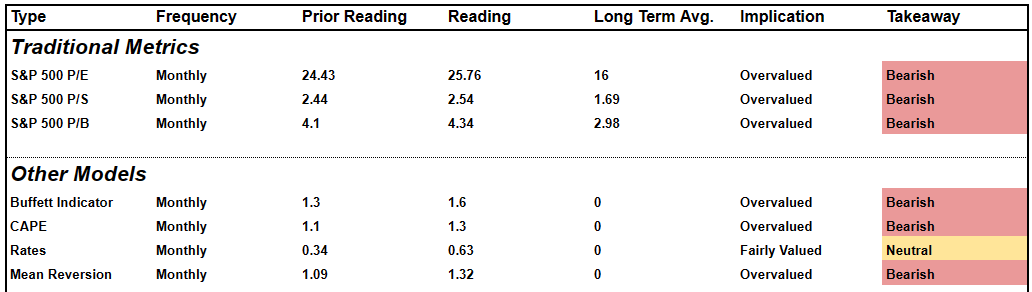

Combined with a pricey overall valuation environment...

{kind=link}

...and the risk seems firmly to the downside at this point. We think that trimming positions here and waiting for a clearer macro-outlook is the best course of action.

Cheers!

For further details see:

Leading Indicators Are Deteriorating; It's Time To Sell The Indices