MFAIF - Leaven Partners Q2 2023 Letter To Partners

2023-10-13 04:45:00 ET

Summary

- Leaven Partners is a hedge fund management firm based in Michigan. The firm utilizes a deep value investing approach.

- Fund assets appreciated by 5.7% in Q3 2023, with a three-year return of 29.0% compared to the S&P 500's 34.1%.

- Core holdings performed well, contributing 7.2% to the total gross return, with Japanese holdings leading the way.

- The fund manager discusses the insufficient allocation to Japan by active fund managers and the opportunities it presents.

| Q3 2023 |

| YTD |

| 1 Year |

| 3 Year |

| Inception † |

| Leaven Partners, LP* |

| 5.7% |

| 12.1% |

| 15.0% |

| 29.0% |

| 33.6% |

| S&P 500 ( SPX ) |

| -3.2% |

| 13.0% |

| 17.2% |

| 34.1% |

| 70.8% |

| MSCI EAFE ( EFA ) |

| -4.9% |

| 6.9% |

| 23.9% |

| 17.4% |

| 15.3% |

| Vanguard Total World ( VT ) |

| -3.5% |

| 9.6% |

| 17.1% |

| 22.9% |

| 38.5% |

| *Leaven Partners, LP are time-weighted gross cumulative returns (unaudited) provided by our prime broker, Interactive Brokers. Performance data, (net of all fees and expenses), for each partner, is provided by Liccar Fund Services. †Trading began on March 16, 2018. |

Dear Partners,

In the third quarter of 2023, fund assets appreciated by 5.7%. For the three-year period at quarter end, the fund is up 29.0% [1] compared to the S&P 500 ( SP500, SPX ) return of 34.1%.

Return Contribution Q3

| Hedge Strategy: |

| -1.0% |

| Core Holdings: |

| 7.2% |

| FX Strategy: |

| -0.5% |

| Q2 2023 |

| 5.7% |

For the quarter, our core holdings performed well, contributing 7.2% to the total gross return. In a similar fashion to the last quarter, our Japanese holdings did much of the heavy lifting, contributing approximately 3.0% of the total gross return in the quarter, buttressed by strong results in Singapore. On the negative side, both the hedge and FX strategy performed poorly in the quarter.

Within our core holdings, Japan sits with the highest allocation, by country weighting, at 47%. Of course, the mandate of the fund provides me tremendous freedom to allocate funds wherever the best deals are to be found, but we are in rare air based on the consensus. When it comes to discretionary fund managers, no one wants to allocate to Japan. Over four fifths of all actively managed strategies tracked are not allocating to Japan in quantities commensurate with their stated strategies. [2] In other words, on average, active fund managers are allocating fewer assets in Japan than they should be allocating based on their mandate or stated strategy—and in some cases, by a wide margin. However, this insufficient allocation to Japan has been chronic for decades. Part of it has to do with the apparent multi-decade investor coma that ensued following the bursting of the real estate bubble and stock market bubble in the early 1990s; part of it has to do with the dearth of institutional coverage of Japanese equities; but the major cause of insufficient allocation to Japan, in my opinion, is based on the conclusion that because the Japanese stock market has not gone anywhere for decades, it will continue to go nowhere for decades. This is sloppy thinking.

{kind=link}

But sloppy thinking provides opportunity. It is not hard to find Japanese companies trading below their absolute and/or relative value. The question is, do we have the guts to stray from the herd? It is not an easy task. Just ask the majority of active fund managers.

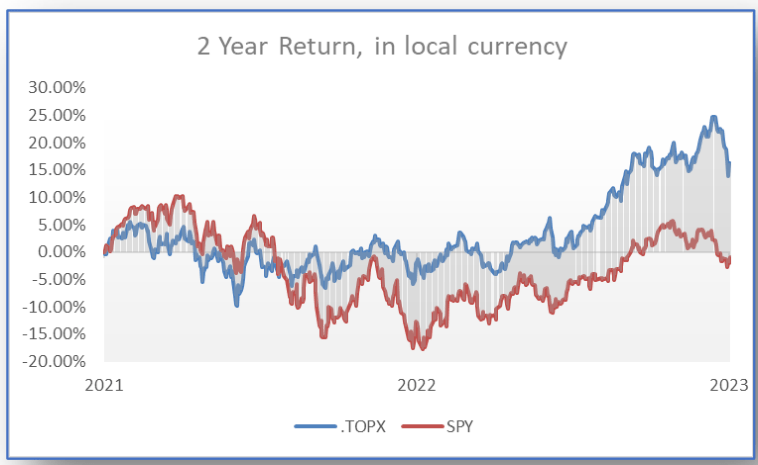

Certainly, there has been some positive movement in the Japanese stock market, despite the skepticism. For the past two years, Japanese equities (blue line) are up over 16% while the S&P 500 (red line) has practically gone nowhere. This has led many publications to print headlines that the Japanese market is finally heating up. In local currency terms, this is generally true.

{kind=link}

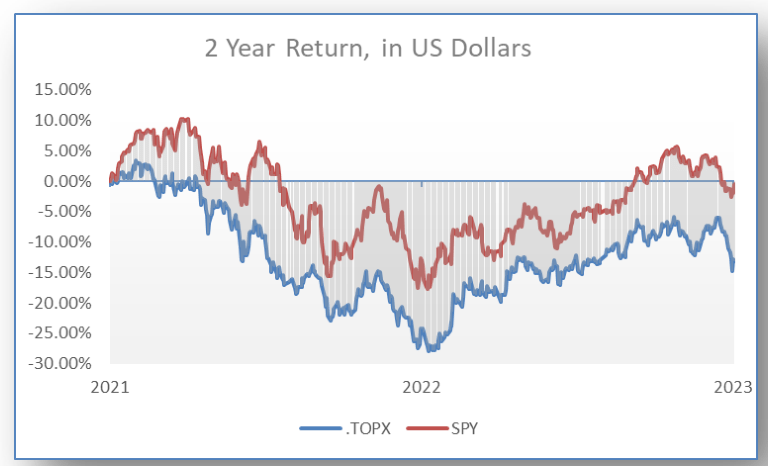

However, for those of us who spend US Dollars every day, things are not as they seem at first glance. The yen has collapsed significantly against the dollar, which has created tremendous headwinds when we report our Japanese holdings in US Dollar terms. If we look at the same period but express Japanese equities (blue line) in US Dollars, Japanese equities are now woefully underperforming the S&P 500 (red line)—which of course remains unchanged as it is expressed in US Dollars by default. Although the Japanese markets are gaining traction in the mainstream headlines, when viewed through the eyes of the US Dollar, it is underperforming. There are two takeaways: (1) our Japanese holdings are performing very well despite significant currency headwinds, and (2) our fund returns would be even better had it not been for the devaluation in the yen [3] .

To address the currency headwind, I employ a partial hedge on the yen to counterbalance some of the negative effects. We are not fully hedged to the yen at all times. The strategy aims to take some, not all, of the sting out of the yen devaluing and to enjoy the ride when the yen appreciates. Year to date, our FX strategy has lessened the blow by providing a positive contribution of approximately +2% to overall results. Because we are not always fully hedged against the yen, when it devalues against the dollar, (and based on various circumstances), we will face some near-term headwinds due to imperfect timing. In my opinion, our core holding returns would be materially higher had the yen remained flat relative to the dollar this year. [4] On the positive side, we should see a reversal in trend at some unforeseen point in time. Then, the wind will be at our backs.

In the quarter, I sold out of one position in the fund: Playmates Toys Ltd ( PMTYF , 0869.HK). Founded in 1966 and based in Hong Kong, Playmates Toys has been in the business of manufacturing and selling toys primarily to American and European children since the 1970s. After selling dolls for over a decade, the company hit paydirt in the late 1980s when it decided to manufacture action toys for a new cartoon series called Teenage Mutant Ninja Turtles (TMNT). Having the foresight to obtain exclusive licensing rights to the brand, Playmates has enjoyed the multi-decade run of an iconic brand. To offset lost revenue when the TMNT franchise periodically laid dormant, Playmates diversified into many other licensing agreements with franchises, such as Godzilla vs. Kong , Star Trek , and the recent Netflix hit, Miraculous: Tales of Ladybug & Cat Noir , (which is also a major hit with my children!).

I first took note of the company in late 2019 after the company reported poor operating results with the stock price headed in the wrong direction. Then COVID-19 hit. Needless to say, no one was going out to the movies or buying toys. Compounding the problem was that the TMNT brand was in a planned hiatus (with no scheduled toy releases) and there was nothing else to pick up the slack, including the much-anticipated Godzilla vs Kong movie release that was now delayed until 2021. In August 2020, Playmates reported dreadful semi-annual results and posted an operating loss of over -$6 million [5] —its worst half-year result in nearly a decade. I built a material position [6] in the stock at an average cost of HK$0.254 per share.

Although I typically do not jump at the chance to buy a money-losing enterprise, there were a few factors that led me to do so. First, the financial difficulties were caused primarily by an exogenous shock that I did not perceive to be indefinite. In similar logic to our holding in Ming Fai International Holdings Ltd ( MFAIF , 3828.HK), I did not anticipate a change in their business post-COVID: things would go back to normal. At the end of the day, Godzilla vs Kong would eventually hit the big screen and kids would want the action figures. Second, Playmates had licensing agreements in place. I felt reasonably comfortable that, when things got back to normal, there would still be toys to make. Third, even with the wheels coming off during the Covid pandemic, in 18 months Playmates had only burned through a little over $10 million. At the time, Playmates had $125 million in the bank with practically no debt. In addition, Playmates subcontracts out the manufacturing of the toys, so its cost structure is quite variable. In other words, it had greater flexibility to batten down the hatches, weather the storm, and conserve cash. Although I did not know how long the COVID pandemic would last, I felt comfortable knowing Playmates would outlast it! Fourth, the company has had a history of treating its shareholders fairly. And, lastly, the stock price was enticing. At our average purchase price, the company was trading for the bargain basement price of $38 million. To put that in perspective, the cumulative operating cash flow generated by the company for the previous 5 years was a little shy of $90 million. To me, at a $38 million sales price, we were getting a pretty good deal with little risk of permanent loss of capital.

Since 2020, Playmates has returned to profitability, more than doubling revenue in 2021 and generating around $14 million in combined operating cash flow in the past 30 months. Last week, Paramount Pictures released Teenage Mutant Ninja Turtles: Mutant Mayhem to positive reviews, reaping $180 million at the box office. As is customary with TMNT releases, Playmates introduced a new line of TMNT toys based on the new movie. On a lesser note, in July, Miraculous: Ladybug & Cat Noir, The Movie was released in theaters internationally and on Netflix, with Playmates supplying the accompanying toys. The near future appears bright for Playmates, but it is hard to predict. The last major TMNT up-cycle, around the release of the 2014 Michael Bay film, saw a significant increase in sales and earnings—although it did not pan out to what analysts were forecasting at the time. In their most recent report to shareholders, management “continues to be optimistic about the second half of the year” based on the release of both movies. Although I could easily find ways to be optimistic as well, our strategy is focused more on the value of the assets of the company rather than the expected future earnings. [7] Based on the liquid assets at Playmates, what was once a screaming deal has now become reasonably valued due to the appreciation in the stock price. I decided it was better to move on to another cheaply priced asset. [8] I sold our shares at an average price of HK$0.84 per share.

Whenever asked to prognosticate about future events, the great Benjamin Graham would respond: “The future is uncertain.”

In Closing

I am grateful for your participation in Leaven Partners, and that you have entrusted me to manage your assets. I look forward to reporting to you at our next quarter-end.

In the meantime, if there is anything I can do for you, please do not hesitate to contact me.

Sincerely,

Brent Jackson, CFA

Footnotes[1] This equates to an approximate 8.8% annualized gross return for the 3-year period. [3] A devaluing yen would benefit some Japanese companies that export to the US, for example, as it has benefited some of the companies we own—albeit difficult to quantify precisely. But, in total, it has been a negative. [4] Again, difficult to prove. There are a lot of variables at play here. But the yen devalued from ¥131 to ¥149 so far this year— which is significant. It is my opinion that this has played more of a negative role than any positive economic benefit some of our Japanese holdings may have capitalized on. [5] Although Playmates reports in Hong Kong Dollars, as a reminder, in my letters I will commonly convert to US Dollars to make it easier on the eyes for the general readership. [6] Based on AUM at the time. [7] Not to say, of course, that I entirely ignore expected future earnings. [8] I am also probably biased by my concerns about the current state of the American consumer and their ability to generate discretionary spending over the near term. DISCLAIMERThe information contained herein regarding Leaven Partners, LP (the “Fund”) is confidential and proprietary and is intended only for use by the recipient. The information and opinions expressed herein are as of the date appearing in this material only, are not complete, are subject to change without prior notice, and do not contain material information regarding the Fund, including specific information relating to an investment in the Fund and related important risk disclosures. This document is not intended to be, nor should it be construed or used as an offer to sell, or a solicitation of any offer to buy any interests in the Fund. If any offer is made, it shall be pursuant to a definitive Private Offering Memorandum prepared by or on behalf of the Fund which contains detailed information concerning the investment terms and the risks, fees and expenses associated with an investment in the Fund. An investment in the Fund is speculative and may involve substantial investment and other risks. Such risks may include, without limitation, risk of adverse or unanticipated market developments, risk of counterparty or issuer default, and risk of illiquidity. The performance results of the Fund can be volatile. No representation is made that the General Partner’s or the Fund’s risk management process or investment objectives will or are likely to be achieved or successful or that the Fund or any investment will make any profit or will not sustain losses. As with any hedge fund, the past performance of the Fund is no indication of future results. Actual returns for each investor in the Fund may differ due to the timing of investments. Performance information contained herein has not yet been independently audited or verified. While the data contained herein has been prepared from information that Jackson Capital Management GP, LLC, the general partner of the Fund (the “General Partner”), believes to be reliable, the General Partner does not warrant the accuracy or completeness of such information. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Leaven Partners Q2 2023 Letter To Partners