LEGIF - LEG Immobilien: A Resilient Income Play In The European Real Estate Sector

Summary

- LEG is a German real estate company focused on the German residential market.

- The company has strong fundamentals and a defensive operating profile.

- It offers a dividend yield above 6%, which is sustainable over the long term.

LEG Immobilien ( LEGIF ) is a good high-yield play within the European real estate sector, due to its business being highly geared to the German residential segment, which is not much sensitive to economic cycles.

Company Description

LEG Immobilien Group is a German real estate company, focused on the residential market segment. At the end of last June, its property portfolio consisted of some 166,000 units, mainly in a specific German region called North Rhine-Westphalia (NRW). The company's roots are based in this region, but its strategy in recent years has been to diversify its portfolio across other German regions.

LEG was incorporated in 1970, through the merger of four public real estate companies, and later privatized in 2008. It has been listed since 2013 and has nowadays a market value of about $4.8 billion. Its main listing is in the German stock exchange, where it has good liquidity, but also trades in the U.S. on the over-the-counter market.

The German housing market is quite different from other European countries, given that it is highly fragmented and has one of the lowest rates of homeownership. This means that the rental market is responsible for a large segment of the housing market, which leads to lower speculative appeal and housing prices that are, generally, cheaper than compared to other European countries. Another reason for cheaper prices in Germany is rent restrictions, which are determined by regulators, and have a significant impact on housing supply.

This backdrop explains why there are relatively large residential property companies in Germany while other large European real estate companies are mainly focused on commercial centers or offices.

Business Strategy

LEG's business strategy has been focused on the organic development of its portfolio, while actively managing its properties through acquisitions and disposals to create long-term shareholder value. At the end of last June, its property portfolio had some 16,000 units with a portfolio value of more than €19 billion, distributed across high-growth, stable, and high-yielding markets. Its portfolio has a gross yield of 4% and a vacancy rate of only 2.2%, which means that almost all of its portfolio is generating income.

Due to a strong macroeconomic background in Germany and a relatively tight supply-demand situation in the housing market, German residential prices have been increasing consistently during the past few years, especially in the affordable housing segment.

This has been a supportive background for LEG's net asset value ('NAV') growth, plus the low interest rate environment and the company's acquisition and disposal strategy. As shown in the next graph, LEG's NAV increased at a CAGR of 14.9% since its listing in 2013, which is a very good growth rate for a company that operates in the most defensive segment of the real estate market.

NAV ((LEG))

This strong growth achieved during the past few years is supported by several structural factors, including the lack of supply of affordable housing in Germany, a low level of unemployment, low interest rates led to strong demand for real estate assets, and low mortgage rates were supportive of higher housing prices.

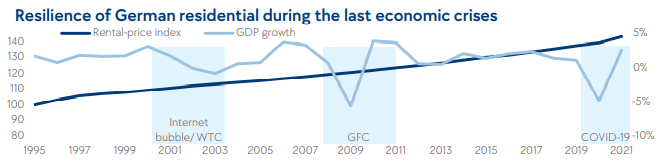

As can be seen in the next graph, the German residential market is highly resilient and not much exposed to economic cycles, with prices following a growing path over the long term supported by strong economic fundamentals, and not exhibiting speculative periods of rapid price increases followed by sharp drops, like happened in other European countries such as Spain or Ireland.

{kind=link}

This bodes quite well for a company like LEG that has some 98% of its property assets in the residential market, a business strategy that is not expected to change much in the foreseeable future. While interest rates are rising in Europe and the prospects of an economic recession are increasing, LEG should continue to report strong fundamentals and maintain a stable business, backed by its defensive and highly recurring income profile.

Additionally, the Ukraine war led to many refugees moving to Germany, creating even more demand for affordable housing in the country while the national construction targets (400,000 units per year) are not easy to achieve due to higher material costs in recent months and the lack of qualified personnel. Therefore, vacancy rates are expected to remain at structural low levels (LEG is at 2.2% vs. 2.4% for the housing sector), and the tight supply-demand situation in the market is not expected to change over the medium term.

Construction ((LEG))

Financial Overview & Dividends

Regarding its financial performance, LEG has reported a positive operating backdrop over the past few years, supported by a strong housing segment in Germany and its organic growth initiatives.

During the first six months of 2022 , LEG's operating momentum remained quite good, considering that revenue increased at a strong pace. Indeed, its adjusted rental income increased by 13% YoY to €311 million, while its free funds from operations (FFO) were up by 10.6% to €241 million. This represented an FFO margin of close to 61%, showing that LEG's business is highly profitable. This growth is justified by a growing portfolio (residential units +15% YoY), but also due to higher like-for-like rental income (+2.6% YoY), and a lower vacancy rate (2.2% vs. 2.5% at the end of June 2021).

On the other hand, high inflation levels are a negative driver for LEG's earnings growth, both from increased staff costs and higher costs of building materials, explaining why FFO growth was lower than net rental income growth, putting negative pressure on its business margins.

Another potential headwind is higher interest rates, as real estate companies borrow heavily to finance their properties, due to the long-term life of its assets. While LEG and its peers have benefited from record-low interest rates over the past few years, rising interest rates are now negative for future earnings and cash flow generation, even though the impact is not worrisome in the short term.

This happens because property companies have generally extended their debt maturity profiles in recent years, and borrow mainly in fixed rates, which means that interest costs are largely inelastic to market rates. Indeed, LEG has an average debt maturity of 7.1 years at a cost of only 1.15%, which means that higher interest rates are not very meaningful for its interest costs in the coming quarters, and only by 2024, it has significant debt maturities and its average cost of debt should gradually increase after that.

Regarding its balance sheet, its loan-to-value (LTV) ratio, a key measure of leverage within the real estate sector, was 42.1% at the end of last quarter, an acceptable level compared to its peers. This ratio is below its maximum target of 43%, which means that LEG's financial position is comfortable and can distribute a great part of its cash flow generation to shareholders.

Indeed, a growing dividend has been part of its business strategy since its IPO, as the company has consistently increased its annual dividend over the past few years.

Dividends ((LEG))

LEG has delivered a dividend growth rate of about 11% per year since 2013, which is a good dividend history and bodes well for future dividend growth. Its dividend policy is to distribute some 70% of FFO to shareholders, which seems sustainable over the long term, as the company's business is highly recurring and its financial leverage is acceptable.

Its last annual dividend was €4.07 per share, an increase of 7.7% from the previous year, and based on this dividend, LEG currently offers a dividend yield above 6%. This yield is expected to increase next year, as the company is likely to raise its annual dividend, which according to analyst estimates could be about €4.42 per share related to 2022 earnings. This means that LEG's forward dividend yield is close to 6.8%, being quite attractive to income investors.

Conclusion

LEG is a company with strong fundamentals and a defensive business profile, as the company is only present in the German residential market segment. This makes its business highly resilient to economic cycles, contrary to other real estate companies that are significantly exposed to economic downturns.

Therefore, LEG's high-dividend yield is sustainable over the long term and is quite attractive for income investors in the current uncertain economic environment, as the likelihood of dividend cuts in the future is quite low, providing a safe income stream over the coming years.

For further details see:

LEG Immobilien: A Resilient Income Play In The European Real Estate Sector