AANNF - LEG Immobilien: Unexpected Dividend Suspension Changes Investment Case

2023-03-09 17:24:44 ET

Summary

- LEG is a German real estate company focused in the German residential market, which has reported good financial figures related to 2022.

- However, due to higher balance sheet leverage and the need to save cash, it decided to suspend the annual dividend.

- Its investment case is no longer geared to income, but it offers value due to a depressed valuation.

LEG Immobilien ( LEGIF ) reported good figures related to 2022, but the company’s focus has switched to cash preservation and decided, unexpectedly, to suspend its annual dividend. This is a strong blow to its investment case, but there is still value for long-term investors.

As I’ve covered in a previous article , within the German residential sector I like LEG Immobilien as a good long-term play, and it was supposedly also a good income pick. However, despite a good operating performance during the last year, the company decided to take a conservative approach and suspended its annual dividend to save cash and strengthen its balance sheet.

I was not expecting this decision, as the company’s dividend was sustainable based on its dividend policy, thus I think it’s now a good time to revisit its investment case to see if LEG remains a compelling play within the European real estate sector or not.

Earnings Analysis

LEG Immobilien Group reported its 2022 earnings today, which can considered to be quite positive considering the challenging operating backdrop in recent quarters. Due to the rising interest rate environment, investor sentiment has been much more negative in recent months toward the real estate sector, which led to lower property values and much tougher funding conditions.

Indeed, while over the past few years the excess liquidity situation in the capital markets and the low interest rate environment were supportive for the sector, this changed completely last year with inflation at sky-high levels, rising interest rates, the Ukraine war, and broader economic slowdown.

Given this backdrop, property values in Germany stopped their rising trend and activity on the real estate market plunged, with most operators now being focused on asset sales to improve their cash position. Additionally, the European bond market has also been shut for these companies, which led to some capital increases recently to strengthen the balance sheet, like the ones performed by TAG Immobilien ( TAGOF ) and more recently Castellum ( CWQXF ).

Taking into account this operating environment, it is no surprise that LEG’s portfolio has not changed much in 2022, ending the year with 167,040 apartments, a small increase of 0.5% YoY. Despite that, its property value increased to more than €20 billion (+5.3% YoY), showing the quality of its units. However, the situation throughout the year was not linear, as strong property uplifts in the first half of the year (+6.1% YoY), were partially offset by lower valuations in the second half (-4% YoY) across its property portfolio.

Property valuation (LEG )

During the year, the transaction market was quiet, allowing only for small acquisitions and disposals, which the company did at book value. At the end of the year, LEG’s EPRA NTA amounted to €153 per share, an increase of 4% from the previous year, while the portfolio’s vacancy rate reduced to 2.4%, from 2.6% at the end of 2021, another positive sign regarding the quality and competitiveness of its residential units during a tough period.

LEG’s in-place rent also increased in the year to €6.32 per square meter, an increase of 3.1% YoY on a like-for-like basis, which is supportive for the company’s top-line. This increase is justified both by market rents going up and the company’s efforts to modernize and re-letting its units, which contributed to 1.3% of rent increases.

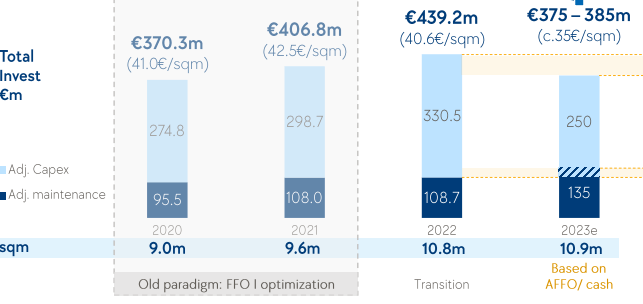

Capex (LEG)

Due to acquisitions, but also organic growth, LEG’s rental income increased to €799 million in 2022, an increase of 16.8% YoY, or €115 million in absolute terms driven by portfolio growth (+€95 million) and organic growth (+€20 million). Due to good cost control, its EBITDA was €598 million, also up by 16.9% YoY, which means its EBITDA margin was flat during the year at 74.9%.

Free funds from operations (FFO) was €482 million (+13.9%), representing an FFO margin of 60%, and FFO per share was €6.56 (+12.3% YoY). Regarding investments, LEG spent €439 million in the last year (+7.9% YoY) in capex and maintenance, and to save cash is guiding for a reduction in 2023, to between €375-385 million. This will reduce its spending per square meter to about €35, from more than €40 in 2022.

{kind=link}

Capex (LEG)

While the company’s earnings were good, the uncertain market environment and lower valuations are major issues for its management. Its business focus has now switched from growth to cash preservation, which ultimately led to a dividend suspension related to its 2022 earnings, the first time this happened since it became a listed company in 2013.

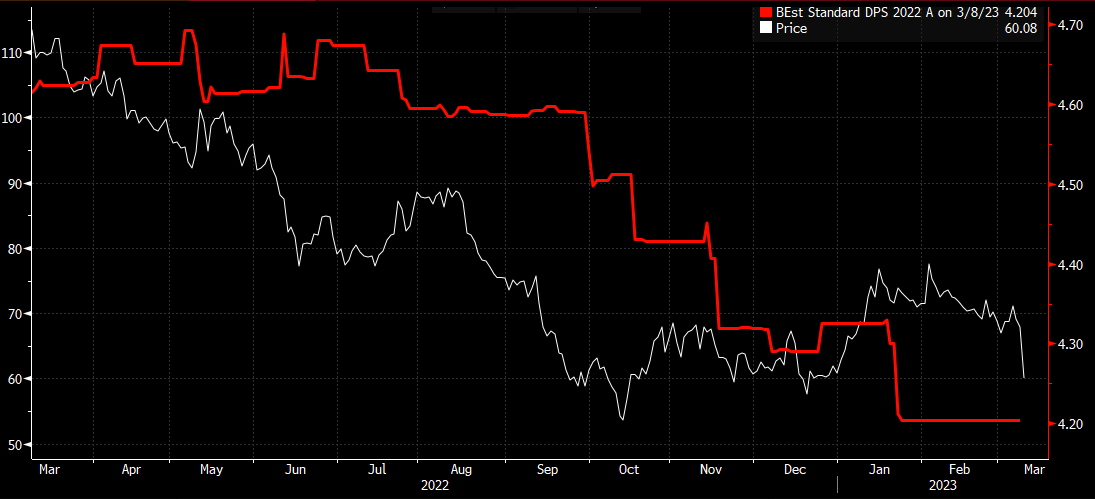

This was unexpected by me and the market given that, as shown in the next graph, current consensus was for a dividend of €4.20 per share (red line). This would represent an increase of 3.2% from the previous year, but LEG’s management decided to suspend the annual dividend to save €337 million of cash outflow.

{kind=link}

Dividend estimates (Bloomberg)

Moreover, the company also changed its dividend policy from a payout based on FFO to adjusted FFO (AFFO), which means going forward it will set its dividend based on cash flows after capex spending. While previously its dividend policy was to distribute some 70% of annual FFO to shareholders, in the future it expects to distribute 100% of AFFO. Therefore, if the company decides to resume a dividend payment in 2024 (related to 2023 earnings), this should amount to €1.60 per share based on its AFFO guidance for 2023.

Free funds from operations (LEG)

This would be a big dividend cut compared to 2021 (€1.60 vs. €4.07), and at its current share price would lead to a dividend yield of about 2.70%. This means that LEG’s investment case is no longer geared to income, as visibility regarding a 2023 dividend is low, and its potential yield would not be that attractive.

This decision to suspend the dividend payment is largely explained by LEG’s focus on balance sheet management, as higher interest rates are putting pressure on the real estate sector.

Indeed, real estate companies borrow heavily to finance their properties due to the long-term life of its assets, and have geared balance sheets to some extent. The most important metric on this factor is the loan-to-value (LTV) ratio, which increased to 43.9% at the end of 2022, compared to 41.9% in 2021.

Investors should note that this ratio can increase because of two main reasons, namely higher debt levels or lower property valuations. While LEG’s property values increased during the last year, this was not enough to offset an increase of about €1 billion in net debt (from €8.1 to €9.03 billion), leading to a higher LTV ratio.

As one of the company’s goals is to maintain an investment grade credit rating, which generally requires an LTV ratio below 45%, a dividend payment would be negative for its LTV ratio and this explains why the company decided to suspend the dividend despite reporting good operating figures.

Regarding its debt maturities profile, LEG has already rolled over the majority of its 2023 maturities, while it has close to €1 billion maturing both in 2024 and 2025. At the end of 2022, its cash position amounted to €362 million (-46% YoY), which barely covered the potential dividend payment, while it has €600 of credit revolving facility outstanding. This means upcoming loans and bond maturities need to be rolled over and refinanced using alternative instruments, as current funding conditions remain difficult for real estate companies in the bond market.

This is an issue that is not specific to LEG, thus its decision to suspend the dividend has some read-across to its peers, namely Vonovia ( VONOY ) that also has a similar LTV ratio. Other German company that I also expect to suspend, or cut, its annual dividend is Aroundtown ( AANNF ), as I’ve recently analyzed here .

Conclusion

While LEG continues to report positive operating trends and has good fundamentals, its need to preserve cash led to an unexpected dividend suspension. Its shares are reacting quite badly today, down by some 11%, but I still see value over the long term. Its shares are trading at only 0.39x NTA, a very distressed valuation due to cyclical factors, which means LEG’s fundamentals are not currently reflected in its share price as the market is pricing more short-term woes rather than long-term business prospects.

For further details see:

LEG Immobilien: Unexpected Dividend Suspension Changes Investment Case