VST - Legacy Ridge Capital Partners Equity Fund I 2022 Mid-Year Letter

- Legacy Ridge Capital Management are contrarian investment managers who believe successful results can be achieved through a focused, long-term investing.

- The gross return for the fund in the first half of 2022 was 0.9%.

- Europe cannot be reliant on Russian energy and the world cannot continue to fund Russian imperialism.

- The situation thus far is akin to the proverbial frog in boiling water: things progress slowly then quickly become critical.

To June 30 th 2022: LRCP Equity Fund I S&P 500 Russell 2000 MSCI World Index

Gross

| Trailing 6-month Total Return: |

| 0.9% |

| -20.0% |

| -23.5% |

| -20.3% |

| Trailing 1.5-yr Total Return: |

| 43.1% |

| 2.9% |

| -12.1% |

| -2.4% |

| Trailing 2.5-yr Total Return: |

| 58.2% |

| 21.8% |

| 5.5% |

| 13.6% |

| Trailing 3.5-yr Total Return: |

| 62.2% |

| 60.3% |

| 32.4% |

| 45.5% |

| Trailing 4.5-yr Total Return: |

| 56.0% |

| 53.3% |

| 16.3% |

| 35.4% |

The figures above are on a cumulative basis, are gross of performance fees, and are unaudited. Future results will also be presented on a cumulative basis in this section. Annual results will be illustrated below for those who wish to measure us based on 12-month cycles. However, we view the cumulative results as most meaningful since we are trying to build wealth far into the future and the annual results are only important in as much as they contribute to a 3, 5, 10, and 20-year track record.

Annual/Interim Results: LRCP Equity Fund I S&P 500 Energy AMZ XAL

Gross

| 1H22: |

| .9% |

| 31.8% |

| 9.9% |

| -31.7% |

| 2021: |

| 41.8% |

| 53.3% |

| 39.9% |

| -1.7% |

| 2020: |

| 10.6% |

| -33.7% |

| -28.8% |

| -24.2% |

| 2019: |

| 2.5% |

| 11.8% |

| 6.5% |

| 21.3% |

| 2018: |

| -3.8% |

| -18.1% |

| -12.4% |

| -22.4% |

To reiterate, our goal is to have good absolute returns first and foremost, which should lead to good relative returns versus the broader markets. However, I also think it’s important to highlight the performance of the primary sectors in which we feel we have an advantage and in which we invest. There is no reason to present this other than for transparency reasons. Owning a highly concentrated portfolio will prevent our results from looking like anything we compare them to in most years, but knowing the performance of energy broadly, midstream energy specifically, and North American airlines will add some context for those partners who wish to do some higher-level analysis. Please see the accompanying disclaimer & footnotes at the end of the letter for a broader description of each of these indices.

Results for 1H 2022

The gross return for the fund in the first half of 2022 was .9%. Through May the fund was up 19%, then the Federal Reserve raised interest rates 75bps instead of the initially expected 50bps and the bottom fell out. The drumbeat of recession was too much to bear and year-to-date outperformers as well as economically sensitive names (generally one in the same up to that point) were eviscerated. Admittedly, we didn’t think anything of it. Expected, unexpected; +75bps, +50bps; recession, no recession, frankly we don’t really care.

We’ve worked at an investment firm that insisted on focusing on such things, and even making investment decisions based on such things, and not once can we remember that approach being additive to long-term performance. There are simply too many variables to guess correctly. So, we abstain, albeit suffer the short-term consequences at times.

Getting back to basics

In 1943 psychologist Abraham Maslow first published his hierarchy of human needs. The hierarchy consisted of five levels, with the apex being “Self-actualization”, which includes morality, creativity, spontaneity, lack of prejudice, etc. The hierarchy then descends to “Esteem” and then “Belonging”. All three of the top needs require an inward focus on one’s own identity and how that’s portrayed to the outside world. However, the last two needs are existential. First is “Safety” of body, health, assets and employment.

Then lastly “Physiological” needs, i.e., food, water, sleep. Maslow suggested humans can only fulfill their needs one level at a time—going from bottom to top—and must meet the needs at a given level before ascending to the next.

This theory elegantly explains evolving human priorities. How can I think about making a better tomorrow if I have no food, shelter or physical security, in which case there might not be a tomorrow? Is it any coincidence Maslow developed his theory during the atrocities of World War II and on the heels of the Roaring Twenties? Perhaps he felt a need to explain society’s rapid descent from elation to despair. Regardless, since the end of that war Western society gradually moved up the hierarchy, while most of the rest of the world arguably struggled near the bottom.

But now we are all once again in rapid descent, trying to preserve our health, physical safety, and affordable access to food. Needs that can only be highlighted by a pandemic or a war. It’s a stark reminder that while we should always strive for self-actualization, we can only successfully pursue it by ensuring our basic needs are also met.

And while investing probably belongs in one of the higher levels of human needs, as a subset, it too seems to follow a hierarchy. The bottom tier might be labeled “Get some of my money back”, followed by “All of my money back”, “Return on my money”, “Reasonable return on my money” and finally “Moonshot”. Here too investors find themselves rapidly descending the hierarchical order as ape NFTs, joke digital coins, and cash incinerating tech stocks bring investors back to fundamentals. The FOMO mantra seems to have petered out for the time being.

Legacy Ridge Capital never found itself in the “Moonshot” camp. I’m not sure if that’s because Nate and I are naturally pragmatic, or because we satiate our gambling desires on weekend football parlays, but ensuring we get your money back while trying to get a reasonable return on that money fulfills our investing needs just fine.

Energy as a weapon

While we were structurally positive on energy fundamentals prior to February 24 th , Russia’s invasion of Ukraine dramatically ups the ante. Two salient facts have reemerged following this tragedy: energy security is of primary importance to Western nations and not all of us have it, and, as a result, there is clearly terminal value in oil and gas securities beyond 2030.

How Europe and its allies marshal their resources to prevent further Russian aggression while simultaneously assuring consumers have the energy they need is left to be resolved. But the current situation is not sustainable. Europe cannot be reliant on Russian energy and the world cannot continue to fund Russian imperialism.

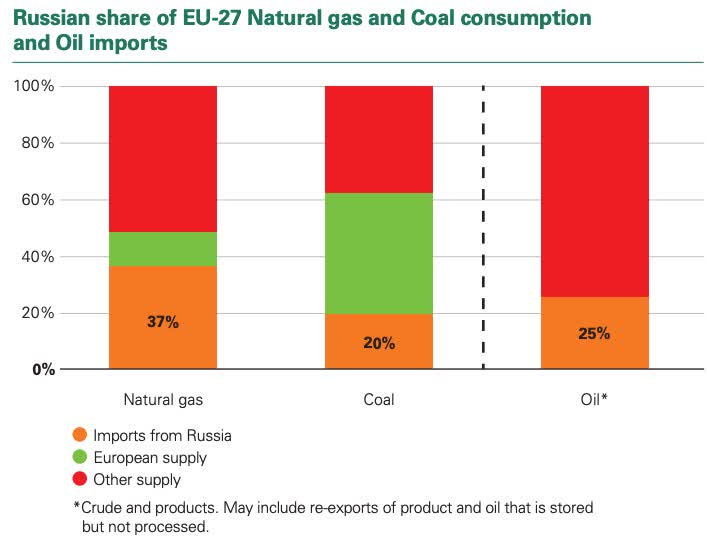

Untangling the global energy trade that developed over the past 30+ years will be hard. Russia produces 12% of global crude oil, behind only the United States and Saudi Arabia, but is the second largest crude oil exporter at 4.6 mb/d (they export more oil than Europe produces). Russia also produces 17% of global natural gas, behind only the United States. They are an energy powerhouse and they’ve made Europe their primary customer.

European energy consumption by fuel type is: 34% oil, 25% natural gas, 12% coal, 12% renewables, 10% nuclear, and 7% hydroelectricity. Hydrocarbons satisfy 71% of Europe’s primary energy needs and the chart below illustrates how critical Russia is in meeting those needs.

{kind=link}

The energy source of biggest concern is natural gas. Gas isn’t transported as easily as coal and oil, so over the years Europe developed a pipeline network connecting itself to Russia’s vast reserves. Hypothetically this is the lowest cost and most secure delivery mechanism available, but the customer must trust the counterparty since supply can be turned on or off with the turn of a few valves.

By 2021, Russia supplied 80% of the EU’s 233 billion cubic meters ( bcm ) of natural gas pipeline imports and 16% of the EU’s LNG imports. And now Russia is playing games.

The situation thus far is akin to the proverbial frog in boiling water: things progress slowly then quickly become critical. Europeans feel some of the pain, but the season (It’s warm) and the construction of retail energy markets (price is lagged up to a year) prevent them from feeling the full brunt just yet. However, the situation will become critical in the next 6-12 months as scarcity during winter becomes likely, gas gets rationed and heating bills explode.

Germany, as Europe’s largest and most vulnerable economy, is taking this seriously. German economy minister Robert Habeck (who is a leader in the environmentalist Green Party) said “It is obviously Putin’s strategy to rattle us, drive up prices and divide us. We won’t allow that. We will defend ourselves resolutely, precisely and thoughtful”. In response, Munich is now lowering the water temperature of public swimming pools, Cologne is dimming streetlights and Hamburg is planning on limiting hot water usage to certain times of the day.

Officials readily admit the current situation could cause the economy to collapse, industries to be shut down or bailed out, and citizens to freeze to death in the upcoming winter. The Bavarian Industry Association estimates the German economy could contract 12.7% in the back half of this year if gas flows through Nord Stream are completely halted. The ceramic, chemical, food processing, and steel industries could shrink more than 30% in such a scenario. German utility Uniper ( UNPRF ) has already sought a government bailout and warned customers to expect “an enormous increase” in their electricity bills starting next year.

The solution is to apply a tourniquet to stop the bleeding, then redesign a strategy that’s been years in the making. Economic minister Habeck again, “It took decades to build up the dependency of Russian gas, and we are trying to change this now in months”. The Netherland’s, Austria and Germany have done an about-face on coal fired power generation and restarted idle facilities while more than 20 European LNG projects have been approved or fast-tracked since March. At full capacity these projects could displace 80% of gas imported from Russia.

The lending arm of the EU, the European Investment Bank, is revisiting its adverse stance on LNG facilities. Bank president Werner Hoyer said the bank “has always been very reluctant to finance LNG terminals, but we are aware we can no longer afford to take this strict stance.” Idealism is giving way to pragmatism across Europe.

But the energy crisis will not be contained within the borders of the European Union and we doubt it ends soon. As countries substitute natural gas with crude oil, heating oil, coal, wood (anything that burns and is available), the entire energy complex will be stressed. And as critical industries completely shut down or curb production, existing global supply chain shortages will persist if not intensify. The world has very little margin for error as surpluses disappear, and as capital starvation persists for the most crucial resources.

It is very possible tightening monetary conditions do not resolve the current situation, and only lead to global stagflation. The biggest proxy for global energy, crude oil, best highlights what may lie ahead for supply and demand: prices are $95 a barrel in a scenario where the US is releasing 1mb/d of oil from the Strategic Petroleum Reserve (this ends in October), China attempts to exit COVID lockdowns for tens of millions of citizens, and industries slowly return to 2019 capacity levels. One could argue today’s oil price is as good as it’s going to get for consumers for the next several years.

In our opinion, the onus is on the United States to displace Russian gas and help some of our greatest allies not only deal with an energy crisis, but also attain energy security. The US produced 934 bcm of natural gas in 2021, representing 23% of global supply, and LNG exports have grown from 4 bcm in 2016 to 95 bcm in 2021—30 bcm of which went to Europe. Two more export facilities reached Final Investment Decision since May, but more are needed! We have the resource, we have the technical capability, we just need to take the initiative. Nate and I are betting the US delivers.

Company Highlight: Vistra Corp ( VST )

We had a hard time deciding which company we should discuss in this letter. By just about every metric, all our holdings are cheap from both a relative and absolute perspective – especially compared to the performance of commodity prices and the recent pullback in the overall complex of energy stocks. For the first six months of 2022, oil was up 41%, natural gas up 45%, natural gas liquids up 34%, and the futures curve for electricity (in the two biggest deregulated power markets) is up ~30%, but our holdings were only up a measly ~1% by mid-year! The point is all our positions are investment stories worth telling.

However, Vistra Corp stands out among the names we own. First, the market environment has improved materially over a multi-year basis, which will enhance VST’s ability to mint cash and at the same time underscores the longevity of VST’s asset base. Second, VST’s market value has remained flat, despite shrinking the share count by nearly 15% since adopting a transformational capital allocation strategy. The combination of those two factors results in ~50% more value in a VST share today than just six months ago.

The bottom line is that the discount to intrinsic value of VST’s equity has become more attractive than ever. To better understand the two broader points, as well as our heightened conviction, it’s worth providing a brief history of the IPPs and summarizing the original VST investment thesis.

History has a way of tainting sentiment

VST is one of three publicly traded electricity companies known as integrated power providers ( IPPs ), a not so helpful name for an extremely small subgroup of utilities. The IPPs primarily operate two symbiotic business segments: producing wholesale electricity ( Generation ) and selling that electricity to retail customers ( Retail ). The IPPs do not own transmission and distribution lines like the larger universe of regulated, investor-owned power companies ( Utilities ) do. And as such, the IPPs do not earn a regulated rate of return.

It’s a gross oversimplification, but investment returns for IPPs were historically almost wholly driven by commodity prices. That’s because IPPs were almost exclusively generation companies without significant retail operations.

At the time, investing in an IPP was considered a relatively safe bet – akin to owning a regulated utility with a lot more commodity upside. You would have been hard pressed to find anyone who thought natural gas prices (the marginal fuel source for power) would go down. Simultaneously, there was a significant buildout of natural gas-fired generation capacity.

Ultimately, however, the IPPs were not a safe bet and investors got burned – management teams were directionally incorrect on the price of natural gas (due to the fracking revolution) and leverage used to build new generation became untenable. The result was a slew of IPP bankruptcies during the 2000s.

The period between 2010-2020 was monumental for the US electricity market. Natural gas prices averaged $3.30/mcf compared to $5.80/mcf in the prior decade. Equally important, the US experienced massive growth in zero marginal cost renewables. Those two factors put enormous pressure on profit margins for conventional, dispatchable power plants.

More often than not, coal and nuclear plants were cash flow negative. As a result, the deregulated market participants rationalized operations and assets through consolidation and plant closures. For the IPPs that have since survived, focus increasingly shifted from wholesale power to retail sales (cash flow stability), reducing leverage, and, to a lesser extent, growing their own renewable energy portfolios.

Why sentiment remains stubbornly low

Despite all the progress the IPPs have made over the past decade, investor sentiment for the space never recovered. To attract investor dollars, IPP management teams have pursued various capital allocation strategies, highlighted ESG efforts, committed to carbon free capacity growth, and pledged to achieve investment grade debt ratings.

All the while, investors and regulators have become increasingly hostile to any business activity directly responsible for carbon emissions. The market has adopted the view that fossil fueled power generation is obsolete, and that green energy is the only ‘investable’ form of energy.

As a long-time observer of deregulated power markets, the aversion to invest in this sector is understandable. Not only is it difficult to gauge the direction of commodity prices, but it’s absolutely impossible to forecast the constantly changing regulatory environment and market rules that determine the profitability and ultimately the useful lives of power plants. Investor concerns surrounding asset duration are seemingly paramount – why else would the market allow a company like VST to trade at an enterprise value ~5x next year’s EBITDA and a roughly 25% free cash flow yield?

We think we’re being pragmatic in our view that VST’s portfolio of assets have a terminal value far more than what the market thinks is justified, and the electricity crises in Europe, California, and Texas are proving us right. That gets us to the original investment thesis.

The argument for owning VST shares

The basis for our interest in VST is the company’s ability to generate significant free cash flow, repurchase shares, thereby compounding free cash flow per share over time. With a free cash flow yield of close to 25%, VST could theoretically buy back every outstanding share in four years! But management has been postponing a massive buyback program for years. That changed in late-2020 when the board approved a new capital allocation framework whereby VST intends to repurchase $2B of equity through 2022 and $1B each year from 2023-2025, all while paying $315M in annual dividends.

Assuming no growth in earnings (which is what consensus suggests) or any change to valuation, the cash returned to shareholders will average 20% per year through 2025. More importantly, free cash flow per share would compound at more than 16% per year resulting in nearly $8.00 per share by the end of 2025 (VST currently trades at only $22.80!). That’s a shareholder return story that we salivate over and reason enough to make it a large position within the fund.

Even so, a fairly long list of recent events (both market-based and geopolitical) has given us greater conviction in the market environment, profitability, and longevity of VST’s business. Those events include market reforms in Texas post Winter Storm Uri, the astonishing increase in commodity prices since the invasion of Ukraine, growing power demand, and scarcity of supply in key areas of VST’s operations. The resulting improvement in power market fundamentals has compelled us to make VST the top position in the fund.

The improvement in power market fundamentals was highlighted in the most recent VST earnings call by outgoing-CEO Curt Morgan: “Frankly, in my 40 years, I have not seen a confluence of events quite like this. Certainly, Vistra is in the right position to capitalize on the strong forward curves…It is a rare opportunity presented to us and it is our job to create the most value out of it while managing the risk” . And that improvement is reflected in recent multi-year guidance from VST – something the IPPs never provide due to the illiquid nature of the electric power price curve.

It’s worth expanding on this point. First, for more than a decade, the power price forward curve has almost always been in steep contango with a low starting price (power prices in outer years decline). Over the past six months, the entire curve has moved up substantially – for 2022 and 2023, ERCOT forwards are up 55% and up 58% in PJM, the two key markets for VST. Moreover, forward prices are up another 10% since VST provided their multi-year guidance.

For that reason, VST has increased its commodity-linked facility from $1B to $3B over the past several months to secure hedged positions that lock in future cash flows in the face of one the highest power price curves the company has ever witnessed and farther into the future than the company has ever hedged. To put things in perspective, VST is now ~50% hedged for the 2023-2025 period. This is notable because VST is typically only ~50% hedged over the ensuing 12-month period (compared to 36 months today).

Concurrently, VST’s retail electricity business has been performing well and appears better positioned to grow both the number of customers as well as volumes. Residential customer count grew organically in Q1 2022, something that hasn’t happened since 2008, as the retail business begins experiencing tailwinds from the fallout from winter storm Uri (i.e., customers fleeing financially distressed Texas retail providers who were caught massively short generation during the storm).

Retail volumes are also experiencing tailwinds from the influx of people, economic growth, and crypto miners moving to Texas (not to mention increased demand from extreme weather). Indeed, already this year, ERCOT has witnessed more than a handful of record-breaking demand days for June and July. During some of those record-breaking days wind energy, a significant portion of the state’s capacity, failed to deliver (only about 8% of peak capacity on 7/11 and 12% on 7/13).

The dearth of capacity has pushed prices into the thousands on several occasions and the state has already hit the scarcity price ceiling of $5,000/MWh for several hours in the second week of July (that’s more than 225x the average price of power in 2020!).

This gets us to the second reason why we have even more conviction in owning VST shares – despite all the positive trends and market improvements, VST’s equity value has gone nowhere. Not only has VST’s capital allocation framework already reduced outstanding shares by ~18% and provided investors with dividend growth of 18%, but it has set the foundation for even more capital allocation flexibility. In short, a cheap stock keeps getting cheaper, and over the next several years management will have even more dry powder to return cash to shareholders.

To highlight the potential value in a VST share and what we view as a compelling capital allocation strategy, as a mental exercise, just extend the buyback program through the end of the decade. Adopt the longstanding Wall Street assumption that VST is a no-growth business. And finally, assume the share price stays flat. From 2022-2030, VST should generate a total of $21B in free cash flow. By the end of 2030, shares outstanding would decline by 90%, giving VST a market capitalization of $0.9B, and net debt would decline from $9.6B to $1.3B.

This would result in an enterprise to EBITDA multiple of roughly 1.0x. Free cash flow per share would compound at 33%, growing to roughly ~$58 per share (a 250% free cash flow yield!). Even more important for a long-term shareholder, the equity interest in a single outstanding share held over that period would increase by over 900%!

What isn’t convincing about the above hypothetical is that share prices rarely remain constant, and we have no illusions about the volatility in VST’s share price. Kris wrote in his 2019 year-end letter that “we would actually prefer it if [VST’s share price] went nowhere for as long as possible… [and] management dramatically shrinks their share count, making eventual value realization that more meaningful to long-term investors like us.” At the time, the shares were priced at ~$17 and management were allocating all excess cash to debt reduction.

Now the priority is shrinking the share count. Whether the share price moves up meaningfully or the share count is reduced drastically, we think both scenarios work in our favor.

Have a great rest of the summer,

Kris & Nate

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Legacy Ridge Capital Partners Equity Fund I 2022 Mid-Year Letter