LGGNF - Legal & General: 10% Dividend Yield In 2024

2023-08-30 07:11:32 ET

Summary

- L&G reached a 230% solvency ratio, exceeding expectations and confirming a solid balance sheet in a challenging environment. In addition, the company managed to reduce its rate sensitivity.

- Strong operating profit driven by LGRI division. This was supported by Pension Risk Transfer, and we project higher returns thanks to Contractual Service Margin performance evolution.

- Higher DPS with a 10% yield projection in 2024 makes Legal & General a buy.

Last week, Legal & General Group Plc (LGGNF)(LGGNY) released its half-year results. The company is one of the United Kingdom's leading financial services institutions selling pensions, life insurance, and investment products across various geographies. L&G's strategy mainly focuses on traditional life insurance, with leading positions in the P&C and annuities segments supported by a solid asset management division called LGIM. Aside from the progressive stands-out results, the company's business model is organized to be cash-generative and coupled with a progressive DPS strategy. Looking back, L&G annuities and the Pension Risk Transfer division ((PRT)) become the largest source of Legal & General cash and are now the key to the company's earnings and dividend sustainability. Looking back (Fig 1), we provided a comps analysis with Aviva called " Attractive ROE Will Lead To Appreciation Over Time ," and our buy case was supported by 1) positive results track record, 2) EPS growth higher than dividend growth (with an upside in potential higher shareholder remuneration), and 3) a superior ROE thanks to expected synergies and the Asset Management diversification. Since our initiation of coverage, the company's total return has been negative by approximately 6.5%; however, last September, following the ex-UK Prime Minister Liz Truss's words and the Bank of England's intervention to avoid a collapse of the British pension funds , we decided to reiterate the L&G buy target (Fig 2). At that time, we considered L&G an opportunistic investment, and it was a solid call: L&G investment return is up by 25.35%, outperforming the S&P 500 change. Here at the Lab, we continue to cover Aviva ( here is our latest publication ).

{kind=link}

Fig 1

{kind=link}

Mare Past Analysis

Fig 2

Q2 results

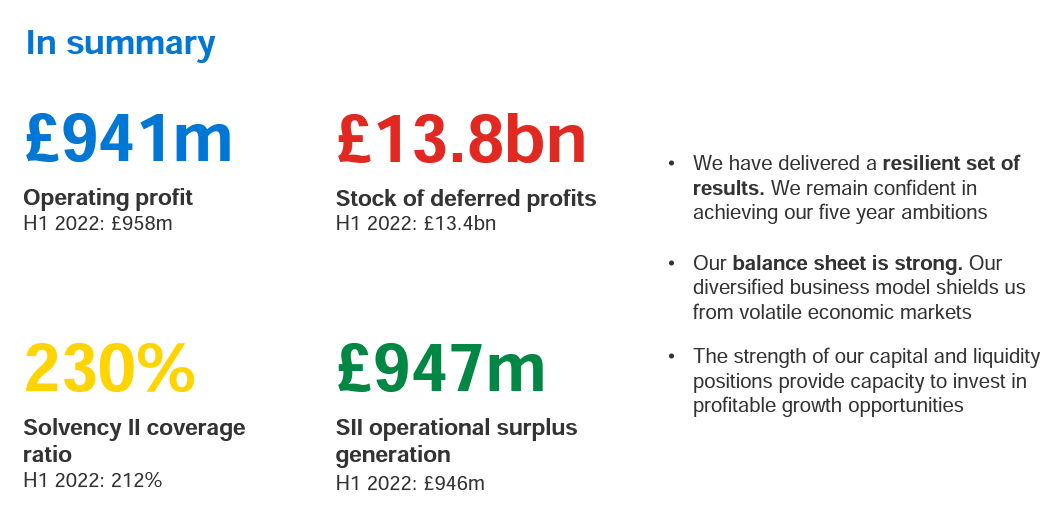

Before moving on with our supportive upside, it is essential to recap L&G's H1 financial performance. Cross-checking the company's results vs. expectations, the Solvency II ratio exceeded consensus by 50 basis points and reached 230%. The company's operating profit stood at £941 million with a plus 13% vs. Wall Street estimates ahead. The Retail, LGRI, and LGC divisions mainly drove this positive performance. The beats were predominantly higher thanks to investment return and asset optimization action. Looking at the divisional basis, the LGIM segment reported lower sales vs. the Visible Alpha consensus. This outcome is related to a net outflow that reached £19.3 billion. In summary, Legal & General delivered a resilient H1 in a challenging macroeconomic environment. They recorded a profit after tax of £316m versus the £575 million recorded last year in the same period. This was mainly due to a write-off of minus £163 million from Modular homes closure in Onto and lower investment performance due to the mark-to-market impact of rising interest rates.

{kind=link}

L&G H1 Financials in a Snap

Source: L&G H1 results presentation

Why are we still over-weighing L&G?

Following our annual results comment and after reviewing the company's H1 financial release, we added more color to our long-standing buy. As a reminder, L&G is a British company with no reporting in Q1. Here we present the three key takeaways that continue to support our target price target:

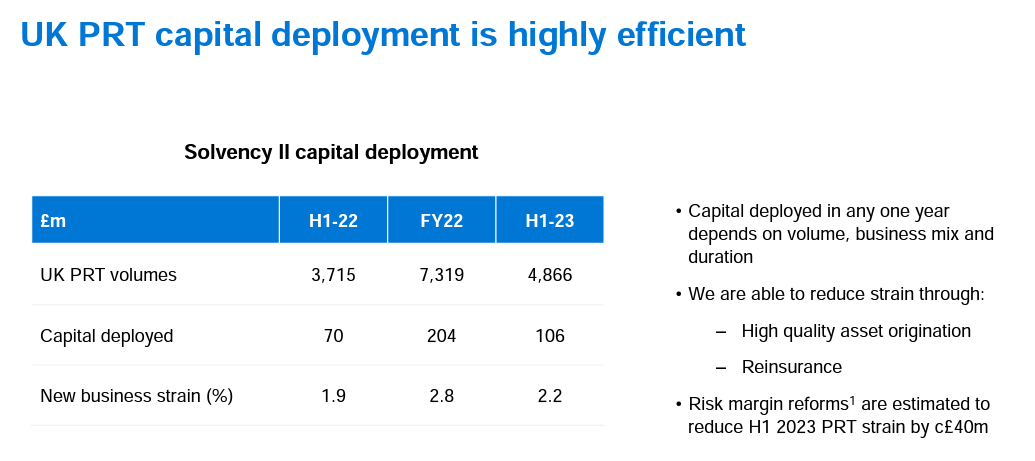

- " Interest rate increases coupled with credit spread widening are generating further growth in the PRT division." L&G's new PRT business was significantly up in H1, with a plus 31% versus H1 2022 (Fig 4). £10 billion of new Pension Risk Transfer will likely create a £1.5 billion higher capital buffer on the Solvency II ratio. This fully confirms our thesis on a positive earnings growth trajectory coupled with a stronger balance sheet evolution. Today, there is £11 billion of UK PRT, and it remains very well self-sustainable with low capital requirements;

- " Related to the higher interest rate, L&G's solvency requirement will benefit from this environment. " Supported by point 1), earnings diversification (Fig 1), and resilience performance in volatile markets, the solvency ratio was higher than the regulatory capital requirements ( 230% vs. 180%);

- "We are confident that L&G's excess capital will be used for higher dividend growth." Once again, the company confirmed a plus 5% interim DPS increase from 5.44p to 5.71p. In addition, the company established a 5% DPS increase for 2024, and the L&G dividend will reach 21.35p with an expected dividend yield of 10% (Fig 1). This tasty yield is a buy signal that cannot be unnoticed.

Moving forward with others' upside, we should include the following:

- Thanks to UK PRT's new volumes, the company is expanding into new markets, and according to the company, there will be $1 billion in annuities from the US. Here at the Lab, it is not the first time we have mentioned cross-selling opportunities in new geographies. This is an evident first sign of L&G's optimization strategy. For this reason, H1 net capital generation reached £752 million and was better than average consensus estimates of £550 million;

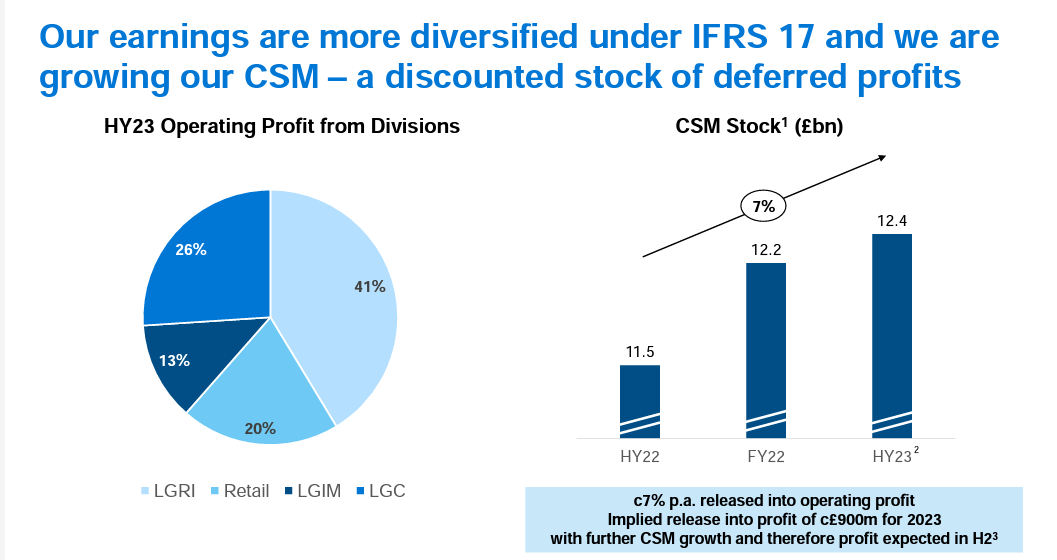

- Key to note is the Contractual Service Margin performance. As a reminder, this ratio represents future unrealized profits from the existing business. According to L&G, this ratio will grow by 7% in 2023 (Fig 3); in our estimates, following the Assicurazioni Generali update, we are estimating a 5% growth until 2025 due to higher income generation from investment, better yield, and organic capital generation for new businesses;

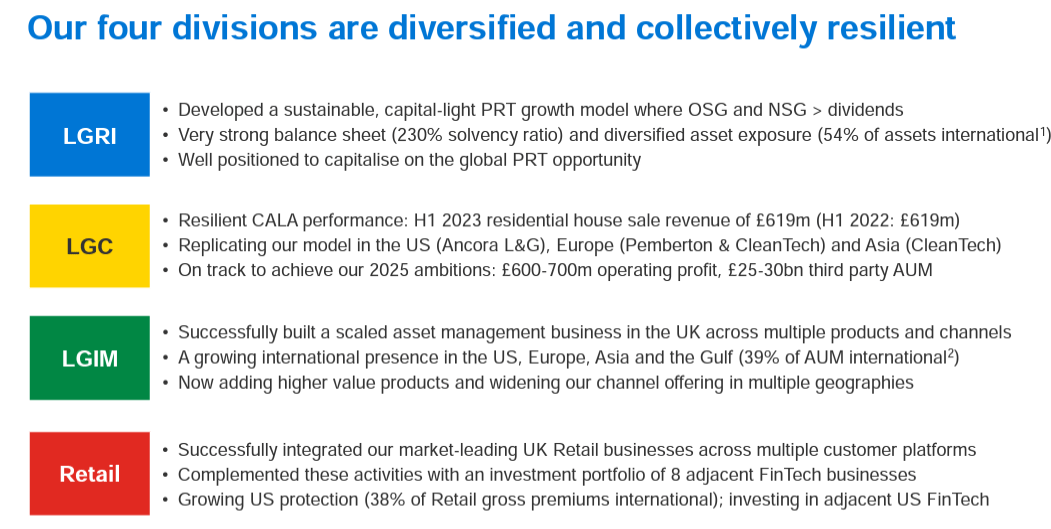

- Also, still related to point 2), LGRI results were driven by asset optimization and higher return on surplus assets (Fig 2). Here at the Lab, we noticed that there is no performance split between the various outputs;

- To notice is also the fact that L&G reduced its interest rate sensitivity. It now is three basis points lower with a change of +/-100bps rates compared to the FY 2022 annual results.

{kind=link}

L&G in line with targets / DPS evolution

Fig 1

{kind=link}

L&G revenue & income diversification

Fig 2

{kind=link}

L&G CSM performance

Fig 3

{kind=link}

L&G PRT performance

Fig 4

Conclusion, Valuation, and Risk Statement

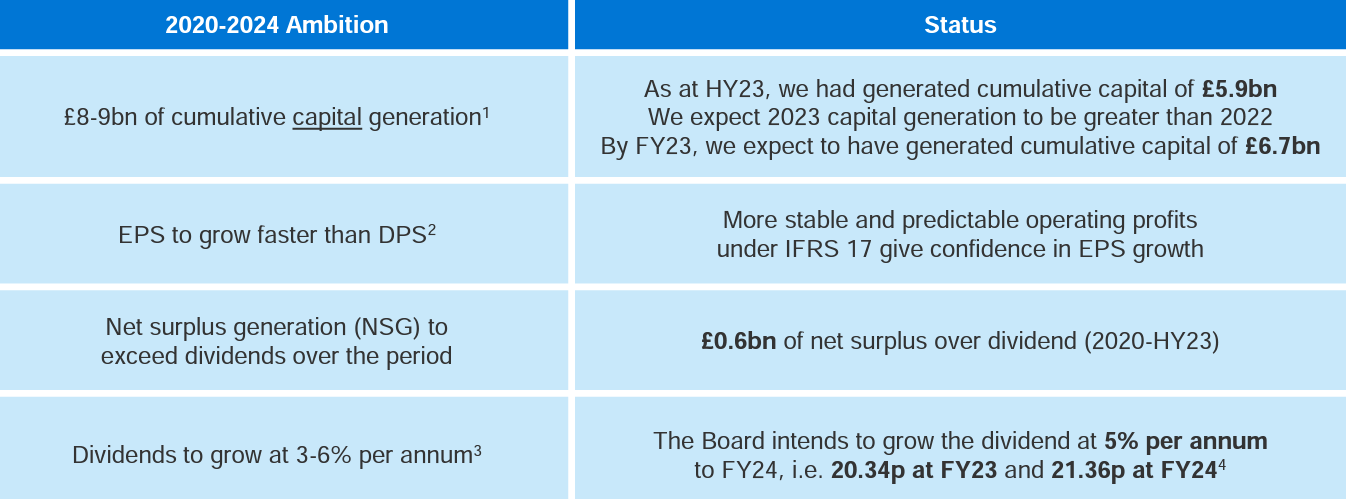

Given the solid results, we might expect a stock price positive reaction in the following weeks. A stable solvency ratio, lower interest rate sensitivities, and low strain offset AuM outflow and negative investment performances. Given the L&G results quality at the Lab, we might expect a share buyback announcement. After the dividend payment (paid in July), we forecast a Solvency ratio of 224% in Q3. L&G increased its cash generation projection from £5.1 billion to £5.9 billion with a net surplus over dividend payment of £0.6 billion. L&G is entirely on track to deliver on its promises: earnings diversification and higher shareholder value.

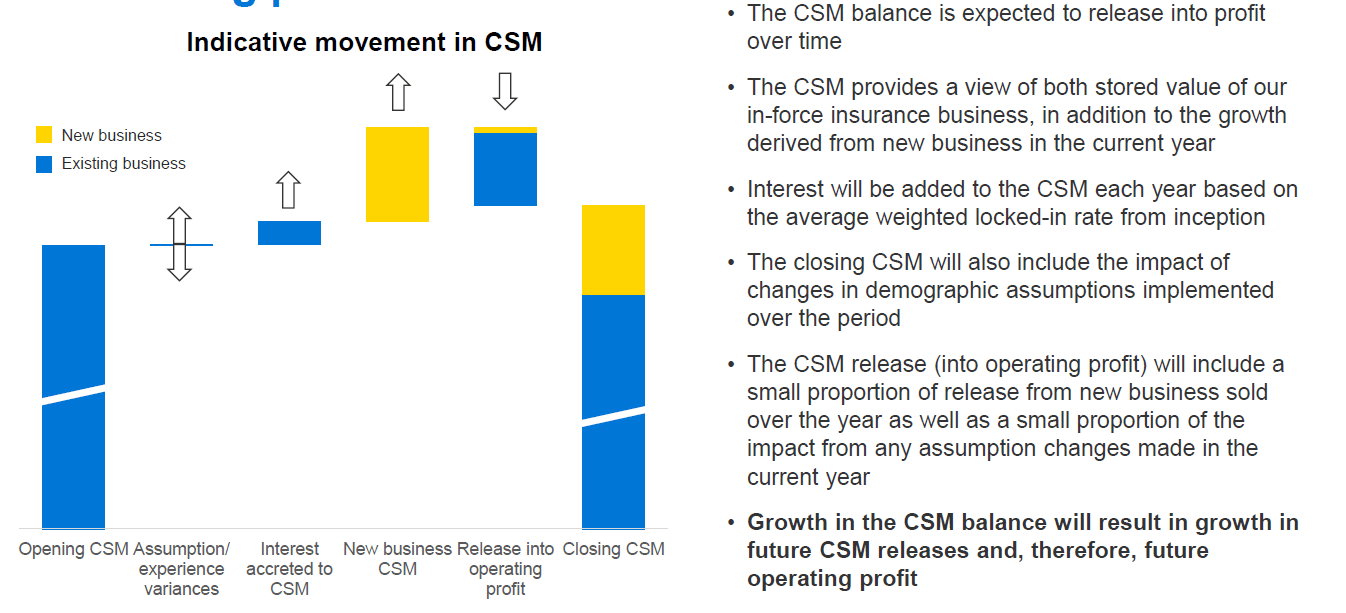

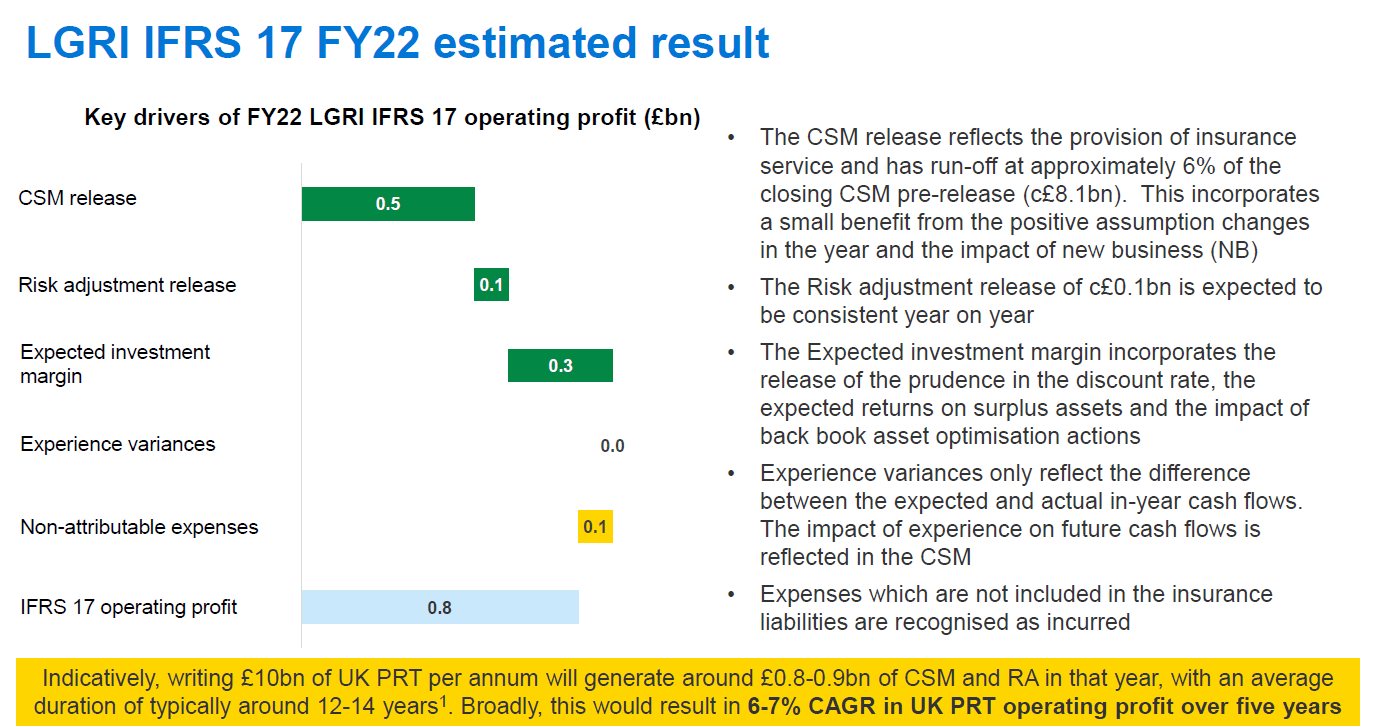

Regarding the valuation, L&G is trading at an 8x P/E, which we believe does not give any credit to the company's past track record. In the last decade, L&G achieved a CAGR in operating profit, EPS, DPS, and book value per share of 9%, 11%, 11%, and 7% respectively. Here at the Lab, given our upside, we are above the Wall Street estimates at the EPS level, projecting a 2024 EPS of 29 cents. Despite a volatile macro environment, L&G earnings stability is enhanced by client retention. Indeed, according to management, L&G clients usually span at least 40 years (this is due to the pension average retirement). For this reason, L&G has solid earnings projections over time. Part of the EPS upside is derived from the CSM opportunity (Fig 5) that represents an internal engine in the insurance business profit ( IFRS 17 Might Provide An Upside ). In our estimates, we projected a growth rate of 5%; however, the company's operating profit CAGR is at around 6/7% in the next five years (Fig 6).

{kind=link}

CSM upside

Fig 5

{kind=link}

IFRS 17 Might Provide An Upside

Fig 6

As already happened in our investment ( Enel , for instance), we should be patient and not change our valuation methodology. Valuing the company as Prudential plc at 12x P/E (UK-based and the closest competitor in GEO revenue diversification), with a projected dividend yield of 10% in 2024, we confirm our £3.5 target price ($21.3 in ADR). L&G and Prudential engage in the same activities, selling insurance products and providing asset manager services.

Concerning the downside scenario, we should include regulatory changes, higher volatility, and credit risk. In addition, related to L&G's asset management division, any government and corporate bond deterioration might impact the company's investment performance and hit performance fees and net AuM flows. L&G has an extensive investment portfolio, and we positively report its latest changes to lower the investment volatility. In addition, the company has asset class exposure to real assets, which might impact L&G's operating profit, as happened in Q2 with a real estate write-off. Operationally, the company divisions are exposed to natural catastrophe threats. L&G complied with the Solvency II requirements to mitigate this pessimistic scenario, so we consistently reported the ratio as a key metric in our quarterly comments.

For further details see:

Legal & General: 10% Dividend Yield In 2024