LZ - LegalZoom: Q2 2023 Results Showcased The Strength Of LZ Freemium Model

2023-08-21 21:11:19 ET

Summary

- LegalZoom's 2Q23 earnings beat expectations, with increased revenue guidance for FY23.

- The introduction of LZ Books is a strategic move that aligns with LZ's position in the SMB company lifecycle.

- Profitability is expected to increase as LZ continues to grow and experiences operating leverage.

Summary

This post is to provide an update on my thoughts on LegalZoom.com ( LZ ) business and stock after the 2Q23 earnings. I recommend a buy rating for LZ as I expect growth to accelerate in FY24 when the US economy recovers and LZ to see continuous profit margin expansion as it benefits from operating leverage.

Investment thesis

LZ's $169 million in sales beat both consensus forecast ($167 million) and the company's own guidance ($166-168 million). Management increased their revenue guidance for FY23 by $7 million to $642 - $652 million on the heels of this beat, which would put 2H23 revenue at $311.2 million (a 3% increase from 2H22 revenue). Since LZ has been growing at a rate of >3% over the past few quarters, even though it was a very tough period (FY22), I believe it will easily meet this guidance with the ongoing strength of its business model and new product launch. The metrics behind LZ's freemium business model show that it is still successful. Growth in both business formation units (42% y/y) and transaction units (26% y/y) accelerated significantly from 1Q23 (32% and 15% respectively). LZ has also recently announced the release of LZ Books, an affordable accounting solution for microbusinesses without employees.

In my opinion, introducing this product is a brilliantly complementary strategic move. To begin, roughly two-thirds of all U.S. small businesses are run by sole proprietors, making up roughly 23 million total businesses. At $9.99, the annual dollar TAM is close to $2.8 billion. Also, this fits perfectly with the benefits LZ offers to small and medium-sized businesses. Due to their advantageous position at the outset of a company's life cycle (during incorporation), LZ is frequently the first business advisor a startup engages. This puts it in a prime position to upsell complementary products that streamline operations for SMBs. As LZ scales, I expect it to roll out more relevant products that they can further upsell.

Profitability ought to increase in tandem with growth. EBITDA for 2Q23 was $30 million for LZ, which is above both the consensus estimate ($28 million) and LZ's own guidance range ($27–29 million). The most notable change is the 620 basis point increase in non-GAAP EBIT margin from 2Q22's 10.4%. This reinforces my earlier argument that the LZ freemium model is profitable because increased efficiency in S&M spending is the primary factor in margin expansion. Since the margin expansion seen this quarter is based on revenue growth of 3%, I think LZ will continue to see margin expansion, probably at a faster pace. As the US exits this economic turmoil, which should drive more SMB creations, LZ should see faster growth, thereby driving more operating leverage.

On the bearish end, I am pessimistic about the near future because management has stated that the LZ Tax and changes to the partnership channel will create more headwinds to subscription revenue growth in the latter part of 2H23. In addition, sales mix is expected to maintain its downward pressure on top-line sales results. While the quarter on quarter increase in transaction units was encouraging, the decrease in transaction AOV of over 27% resulted in a decline in transaction sales of 9%. Despite my expectation that transaction revenue will become less relevant as subscription products gain popularity, I do think some investors will focus solely on total revenue. Until subscription revenue constitutes a larger share of the company's income (roughly 60% in 2Q23), total revenue growth will remain constrained from a headline basis.

Valuation

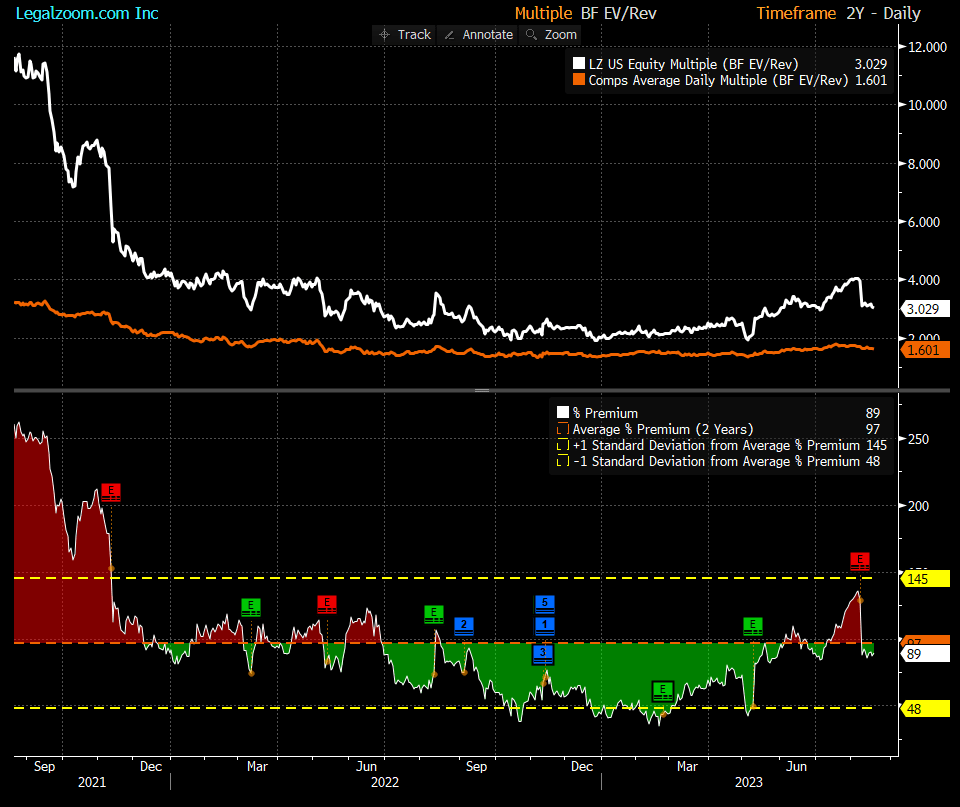

I believe the fair value for LZ based on my model is $13.50. My model assumptions are that growth will be slow in 2023 as it laps the launch of new products last year and also because of the weak macro environment. That said, revenue should meet the higher end of FY23 guidance. Looking past FY23, I expect growth to accelerate above FY22 growth levels. For FY24 and FY25 figures, I used consensus estimates as a yardstick for market expectations. With a better growth profile and stronger balance sheet (net cash position), I expect LZ to continue trading at a premium vs. peers. Assuming LZ trades at 3x forward revenue in FY24, I believe the upside is 12% from here. Further upside from here should be driven by multiples rerating higher than I expected when growth shows acceleration in FY24.

Peers include: CBIZ ( CBZ ), Huron Consulting ( HURN ), ZipRecruiter ( ZIP ), Kforce ( KFRC ), ASGN ( ASGN ), First Advantage ( FA ), ManpowerGroup ( MAN ), and Korn Ferry ( KFY ). The median forward revenue multiple peers are trading at is 1.43x, the expected 1Y growth rate is flattish, and the median net debt to equity ratio is 53%.

Own calculation

{kind=link}

Risk

LZ growth is basically tied to the health of SMBs in the US, which is strongly correlated with the economic cycle. Currently, the US economy is on the brink of a steep recession. Suppose it happens, it could really hurt LZ's growth profile in the near term, dampening the stock price.

Conclusion

In conclusion, LZ 2Q23 results affirm the strength of its freemium model, marked by robust sales, margin expansion, and successful product diversification. The acceleration in growth of business formation and transaction units underscores the model's effectiveness. The introduction of LZ Books aligns strategically with LZ's position as a startup's initial advisor, enhancing its potential upsell opportunities. Despite potential headwinds from changes in the partnership channel and the LZ Tax and revenue mix, I believe the company's long-term trajectory remains promising.

For further details see:

LegalZoom: Q2 2023 Results Showcased The Strength Of LZ Freemium Model