ENB:CC - Leggett's 8% Yield Is Great But These 8% Yielding Aristocrats Are Much Better Buys

2023-12-07 07:30:00 ET

Summary

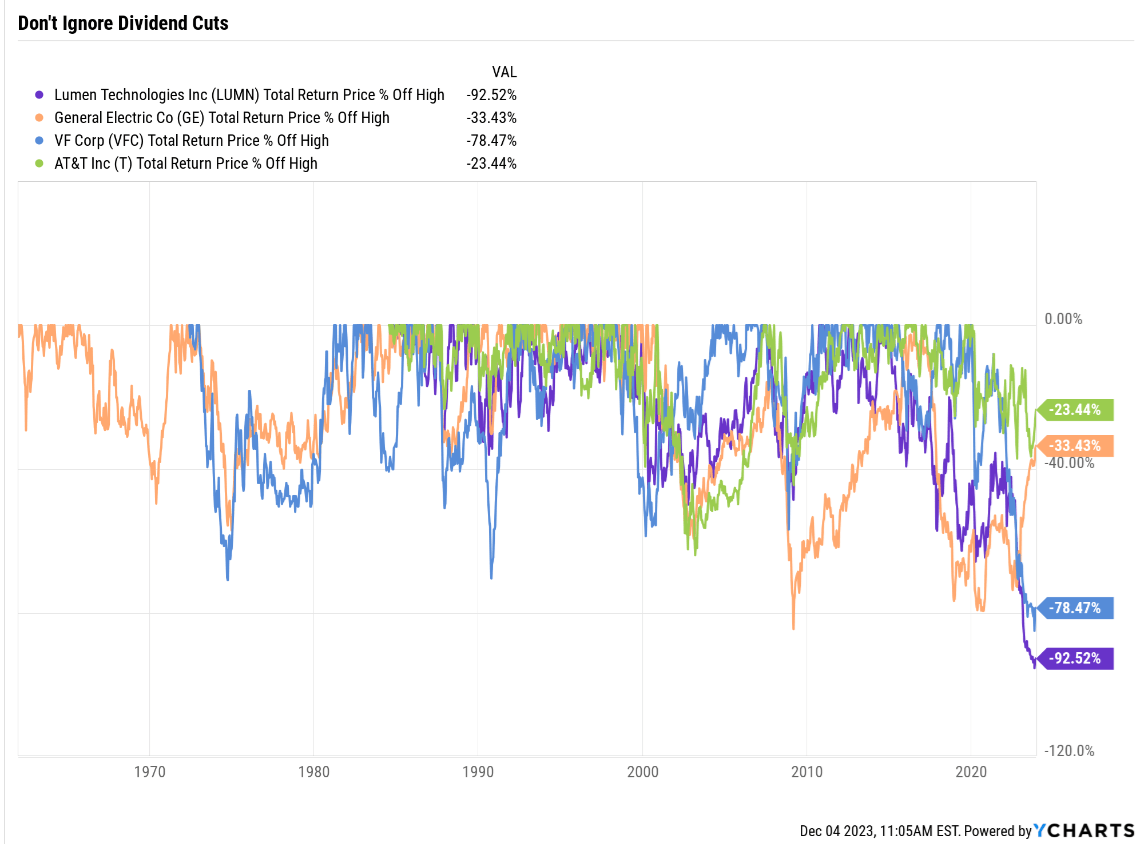

- Dividend aristocrats can fail over time, as seen with the bankruptcies of Winn-Dixie, K Mart, and terrible long-term returns from GE, AT&T, CenturyLink, and VF Corp.

- I love recommending safe, high-yield aristocrat bargains to buy now and warn about rising dividend cut risk at deteriorating dividend aristocrats like Leggett & Platt.

- Leggett's pandemic supply chain disruption and inflation impacts have left it in a weakened state, likely going into a 2024 recession.

- S&P has downgraded its credit rating and the negative outlook is a warning sign that LEG's dividend cut risk has risen to 6% for next year.

- These 8% yielding aristocrat alternatives yield more than LEG with 6X lower dividend cut risk, with similar long-term return potential and Buffett-like return potential over the next two years.

The dividend aristocrats are legendary for their dividend dependability. After all, a company doesn't achieve a 25-year dividend growth streak without being a mature, well-managed business with strong leadership, an income-friendly corporate culture, and a conservative balance sheet.

However, even the mighty aristocrats can and do fail over time. Winn-Dixie and K Mart were once aristocrats and went bankrupt. K Mart went bankrupt and then was acquired by Sears, which then went bankrupt. So, it holds the ignominious distinction of being the only aristocrat to go bankrupt twice.

GE (GE) hasn't failed as a business, though it cut its dividend five times over a 14-year period and is down 65% adjusted for inflation from its 2000 record high.

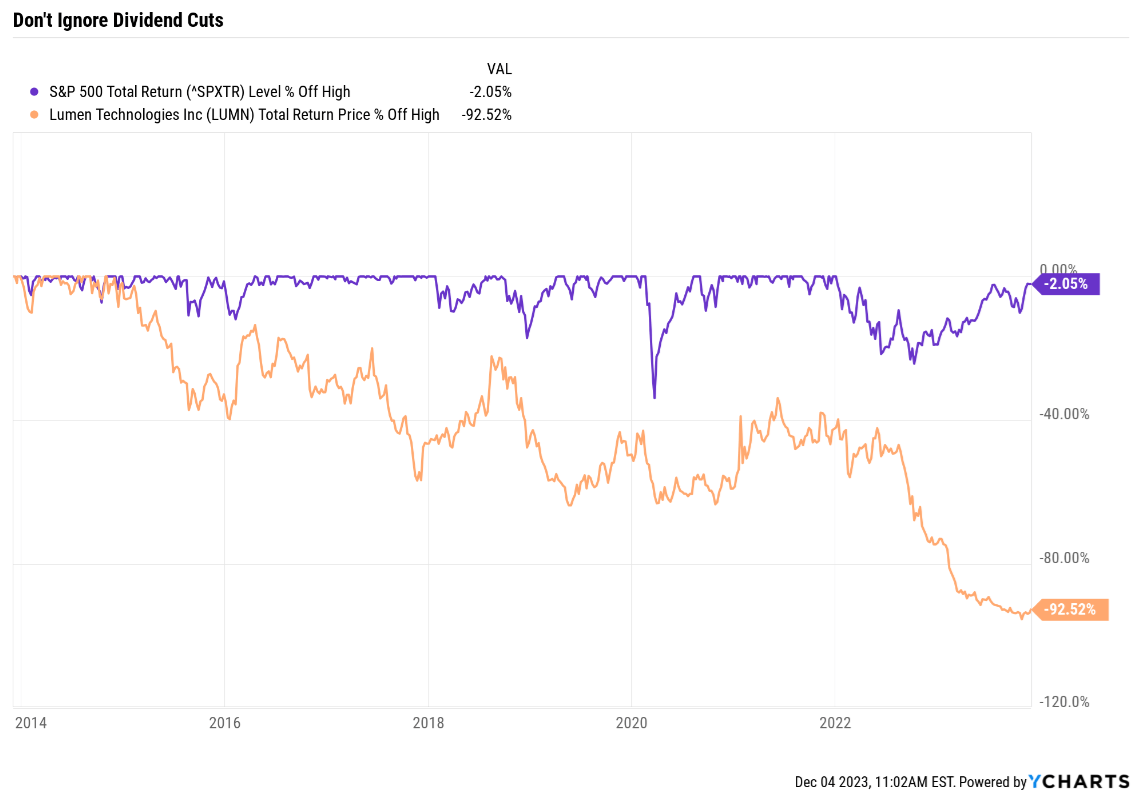

AT&T (T) and VF Corp. are two recent failed aristocrats, and if you want to see a house of horrors, consider the cautionary tale of CenturyLink, now Lumen Technologies.

{kind=link}

CenturyLink cut its dividend three times before suspending it entirely. Each time, it had a good reason for the cut. And each time, bulls said, "Even with the cut, the yield is still good."

Well, as far as I know, dividend cuts from former aristocrats have never turned out well.

{kind=link}

And this doesn't take inflation into account.

{kind=link}

The historical data is clear, that if a dividend is cut, it's usually best to sell, move on and never look back.

I've recently warned about rising dividend cut risk at Walgreens ( WBA ) and 3M ( MMM ).

- Sell Walgreens And Buy These Amazing 9% Yielding Alternatives

- 3M Could Get Cut In Half, So Buy These 8%-Yielding SWANs Instead

Today, I'm providing an update about the recent deterioration at Leggett & Platt ( LEG ), which has increased the risk of a dividend cut in 2024 to 6%. That's not a base-case "cut is coming, so sell now," but it's significantly higher than the 1% pre-Pandemic.

Let me share the best available facts about this 8% yielding dividend king. Then, I'll share the best 8% yielding dividend aristocrat alternatives for those uncomfortable with LEG's weakening fundamentals.

Leggett & Platt: An Industry Leader You've Never Heard Of

You've probably not heard of Leggett & Platt, but it's an industry legend.

Founded in 1883 in Missouri, Leggett manufactures and distributes furniture, engineered components, and products among homes, offices, automobiles, and commercial aircraft.

Basically, it is furniture components for industrial customers.

Leggett faces a problem that many companies faced during the pandemic: supply chain disruption.

{kind=link}

During the Pandemic stimulus boom, consumers were flush with cash and willing to pay any price for a limited supply.

The home market was booming, and auto-makers were similarly eager to maximize their supply.

How things changed, as inflation took off and interest rates soared at the fastest rate in 42 years.

Now, the housing market is frozen, and consumers have little taste for more bedding and furniture.

The Promise And Peril Of Leggett

At the moment, management is working hard to cut costs and hunker down through this challenging period, one it's seen dozens of times in the past 135 years.

Management has been moving money around on the balance sheet via inventory adjustments to maximize cash flow and keep the dividend covered.

The trouble is that if we get a recession next year, things will get worse for LEG's core markets, not better, then management will run out of time.

Not to save the business, the bond market is estimating a 7.5% risk of LEG failing completely, but of preserving the dividend.

{kind=link}

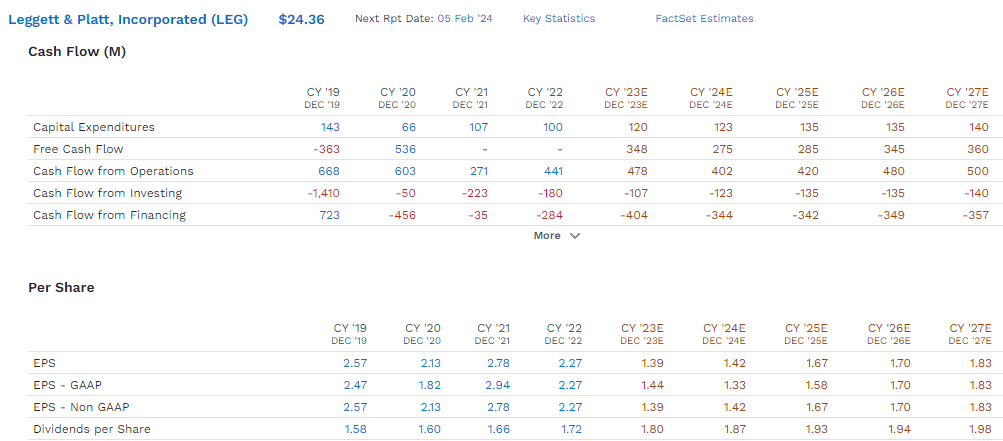

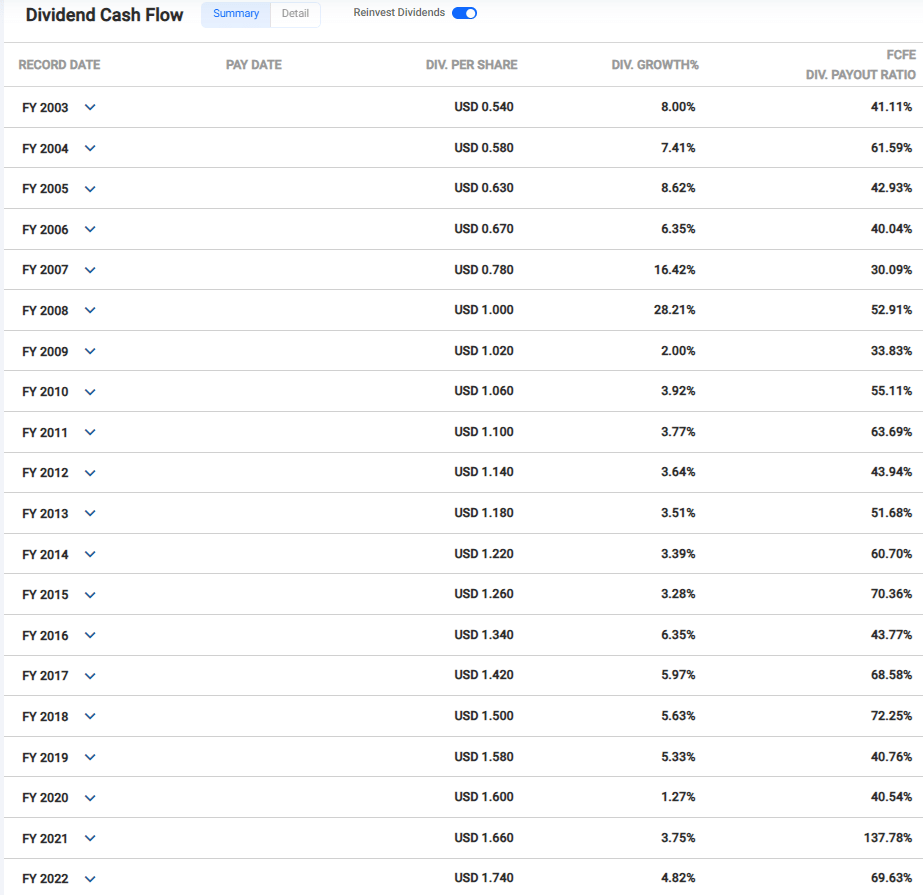

The good news is that LEG's dividend costs $250 million annually, and its free cash flow is expected to fall to no more than $275 million.

The bad news? Rating agencies want to see 60% or lower FCF payout ratios for most companies, and analysts expect a 90% FCF payout ratio next year.

{kind=link}

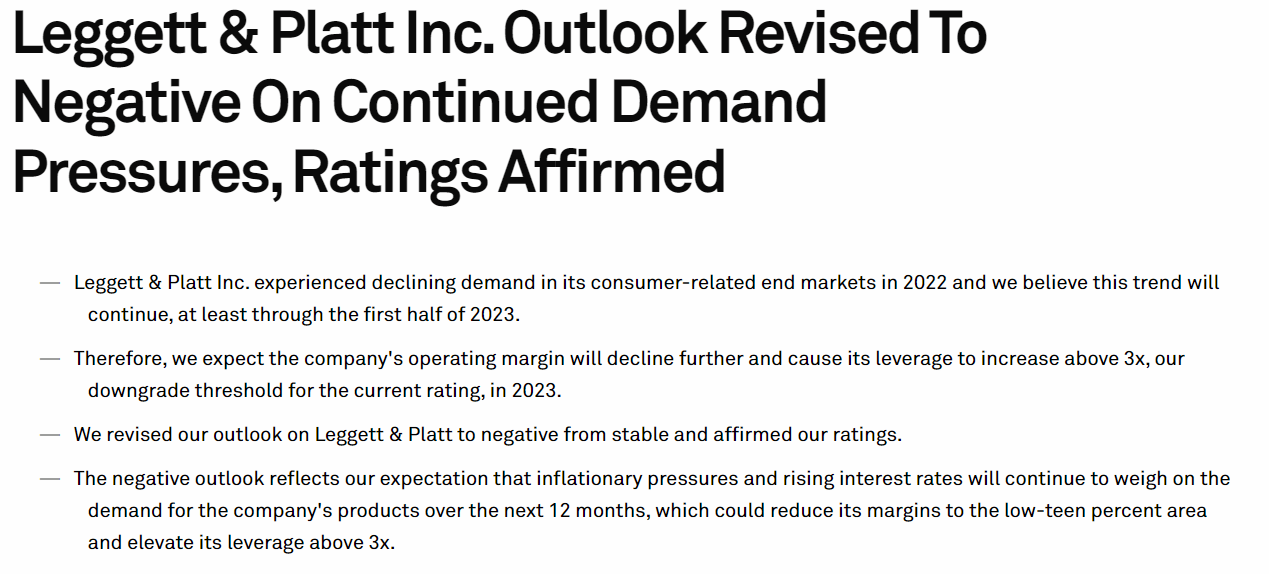

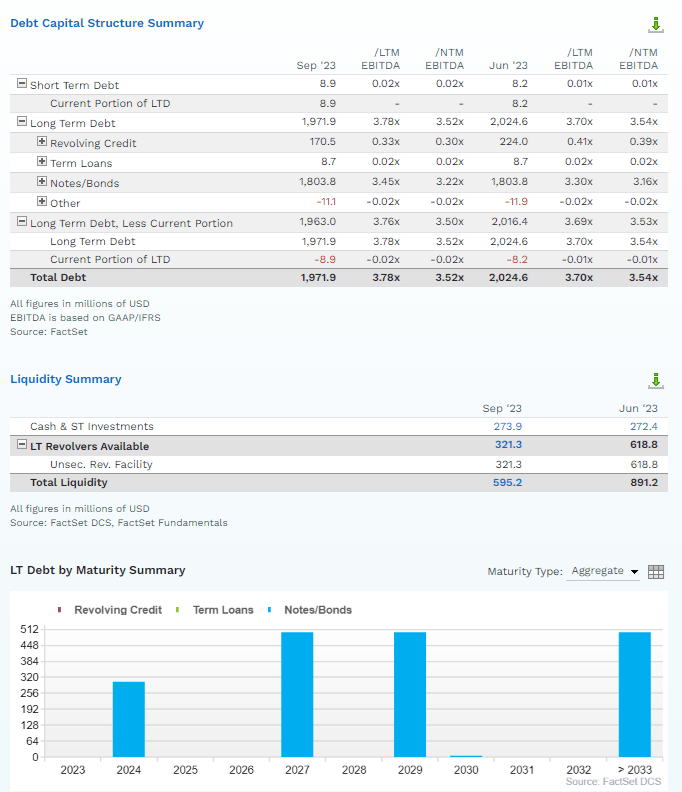

S&P is already nervous about the company's debt/EBITDA ratio rising above 3X, the safety limit for most companies to be considered investment grade.

There is a 33% chance of LEG getting downgraded to BBB- the lowest level of investment grade.

S&P

A downgrade to BBB- would represent a 1 in 9 chance of LEG defaulting on its bonds, resulting in bankruptcy.

After the most recent earnings, management reduced guidance, citing a lack of housing recovery that had previously been expected.

Well, the good news is that interest rates have fallen recently, but the bad news is that the economic outlook has darkened significantly.

{kind=link}

Ironically, in the strongest economy in 83 years, LEG has seen falling sales, earnings, and cash flow.

After management reduced guidance in the earnings release, here is how LEG's 2023 and 2024 consensus estimates reacted.

- 2023 EPS fell from $1.53 to $1.38 (-10%)

- 2024 EPS fell from $1.63 to $1.42 (-13%)

Remember that in 2023, LEG's FCF payout ratio is now expected to hit 90%, meaning that almost all the free cash flow it generates goes to the dividend.

{kind=link}

LEG's highest payout ratio was 138% during the Pandemic but usually doesn't exceed the safety guideline of 60%.

So you can see why I'm a bit nervous about what might happen if we get a recession in 2024 and things potentially get even worse for LEG.

Leggett significantly expanded its operating cash flow year over year in 2022 and we think it will improve modestly in 2023. The company's working capital, excluding cash and current debt, rose to 15.3% of its annualized sales in the fourth quarter of 2022, compared with 13.4% a year ago. Therefore, we believe Leggett & Platt could modestly improve its working capital and increase its free cash flow, even amid a difficult year. That said, we forecast the company will pay $240 million in dividends, which limits its capacity to rapidly reduce its debt, even if it suspends its share repurchases and acquisitions." - S&P

When S&P mentions the dividend in its rating downgrades, that's a red flag.

S&P says that if debt/EBITDA remains above three or margins remain this depressed, it would consider a downgrade to BBB- negative outlook.

{kind=link}

LEG's leverage ratio is expected to come down just a little in 2024. And that's with management still not guiding for a recession.

It has a $300 million bond maturing in 2024, which it initially sold at a 3.8% yield and today yields 6.4%.

- LEG either has to pay off the bond using up all its cash and retained cash flow or refinance at a 2.6% higher interest rate

- Resulting in $7.8 million in higher interest costs

But wait a second? Won't interest rates crash in a recession? And won't that mean that LEG will be able to refinance its debt at a similar interest rate as the initial bond?

Keep in mind, that the recession is likely to be mild, and possibly the Fed will not be cutting rates at all. If inflation stays stuck at 3.6%, as it currently is, then the Fed might actually have to start hiking rates again, long-term rates could take off to new cycle highs of 5.5% (per BlackRock) and 30-year mortgage rates of 8.5% could make the housing market even worse.

If rates do fall, they are highly unlikely to return to zero, where they were when LEG borrowed this current bond.

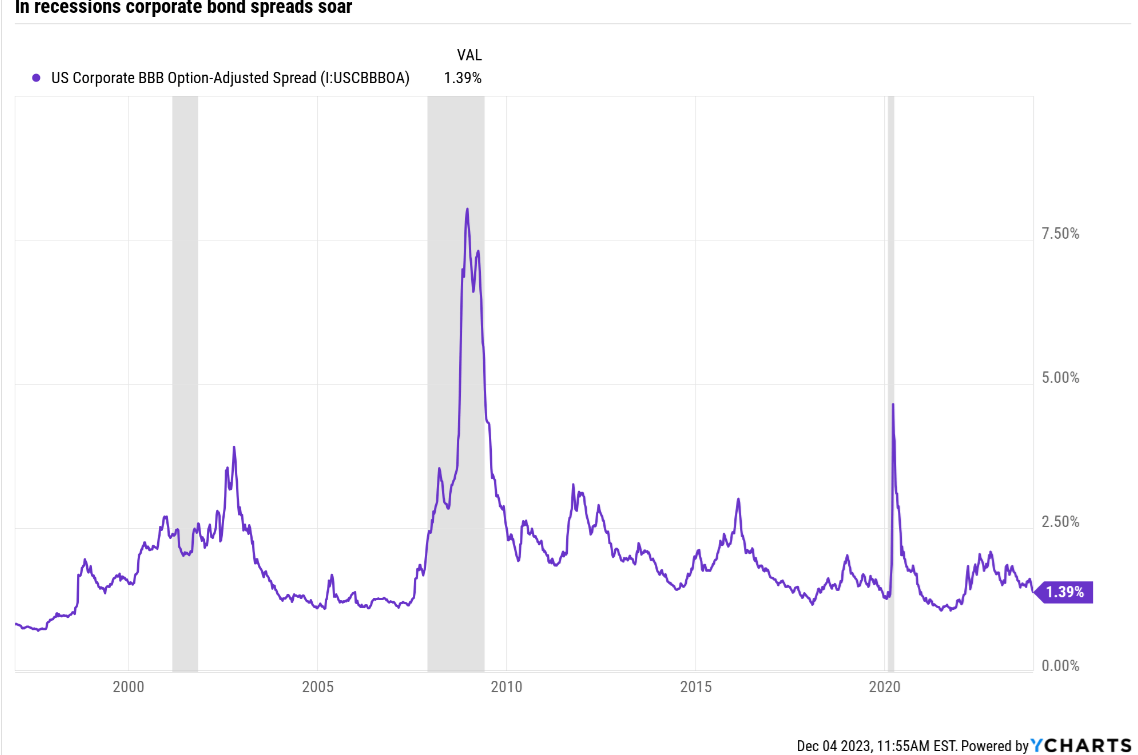

Keep in mind, in recession, risk premiums tend to blow out.

The spread between risk-free US treasuries and corporate bonds can increase and the riskier a company's credit rating the higher the spread can rise.

{kind=link}

Right now, LEG is facing very modest bond spreads.

In a recession, it could be facing refinancing rates of 3% to 4% above 10-year treasury yields, which might bottom at 3% to 4%, according to leading economists.

That would be a 7% to 8% potential refinancing rate for LEG in a 2024 recession.

That would suck up $10 million in remaining interest and push LEG's 2024 FCF payout ratio to 100%.

And that assumes no decline in sales, which would likely occur in a 2024 recession.

While I estimate LEG's dividend cut risk at 6%, it has a negative outlook, just like S&P's rating, and if fundamentals continue to deteriorate, I'll be adjusting the DK safety and quality scores accordingly.

How to Find The Best 8% Yielding Leggett Alternatives Video (Click This Link To Watch)

Here is how I have used our DK Zen Research Terminal to find the best 6% yielding dividend king alternatives to Hormel (HRL).

From 505 stocks in our Master List to the best high-yield Ultra-SWAN quality dividend kings with superior long-term return potential.

All in one minute, thanks to the DK Zen Research Terminal. This is how I find all my investment ideas.

| Screening Criteria |

| Companies Remaining |

| % Of Master List |

| 1 |

| Dividend Champions List (any stock with a 50+ year dividend growth streak) |

| 134 |

| 26.80% |

| 2 |

| BHS Rating "reasonable buy, good buy, strong buy, very strong buy, ultra value buy" |

| 96 |

| 19.20% |

| 3 |

| Non-Speculative (No Turnaround Stocks, investment grade) |

| 79 |

| 15.80% |

| 4 |

| Yield 6+% |

| 3 |

| 0.60% |

| Total Time |

| 1 minute |

Short, simple, and super effective. It's always and forever a market of stocks, not a stock market.

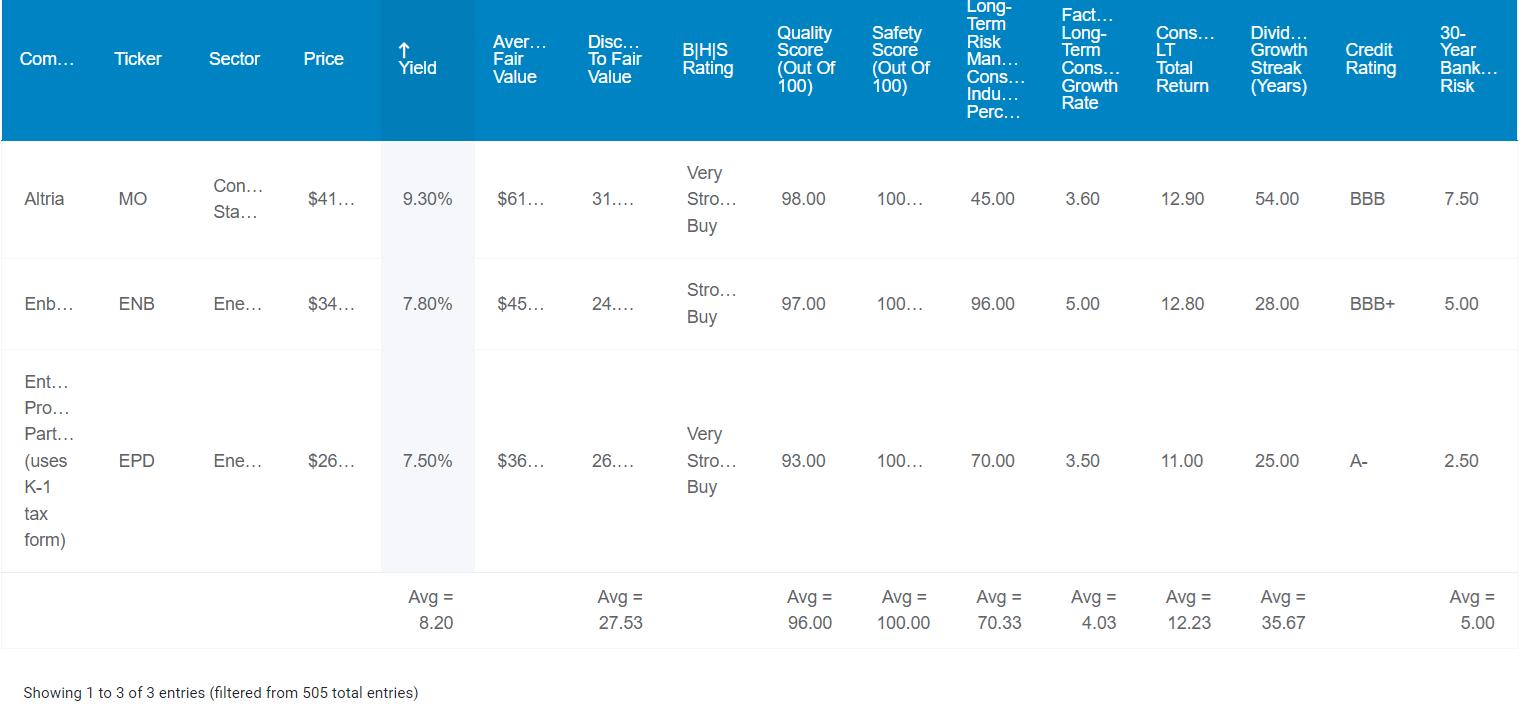

8% Yielding Dividend Aristocrats Alternatives To Leggett

Bottom line up front, here are the fundamentals for these incredibly safe 8% yielding Ultra SWAN dividend aristocrat Leggett Alternatives.

Fundamentals Summary

- Yield: 8.2% (5X S&P 500 and 2.5X more than SCHD or VYM)

- Dividend safety: 100% safe (1% dividend cut risk)

- Overall quality: 96% low-risk Ultra SWAN dividend aristocrats

- Credit rating: BBB+ stable outlook (5% 30-year bankruptcy risk)

- Dividend Growth Streak: 36 years

- S&P LT Risk management global percentile: 70th = low risk (good risk management)

- Long-term growth consensus: 4.0% vs 5.2% LEG

- Long-term total return potential: 12.2% vs 13.2% LEG

- Discount to fair value: 28% discount (potential very strong buy) vs 13% overvaluation on S&P

- 10-year valuation boost: 3.3% annually

- 10-year consensus total return potential: 8.2% yield + 4% growth + 3.3% valuation boost = 15.5 % vs 9% S&P

- 10-year consensus total return potential: = 322 % vs 134% S&P 500

Leggett theoretically offers slightly better long-term return potential if the thesis doesn't break, but the risk of that increases significantly in a 2024 recession.

In contrast, these 3 Ultra SWAN aristocrats offer an 8.2% yield that is not just very safe, but their growth outlook is much less risky.

Dividend Kings Zen Research Terminal

{kind=link}

I've linked articles about each for further research and sorted by yield.

Consensus Total Return Potential Through 2025

- if and only if each company grows as analysts expect

- and returns to historical market-determined fair value

- this is what you will make.

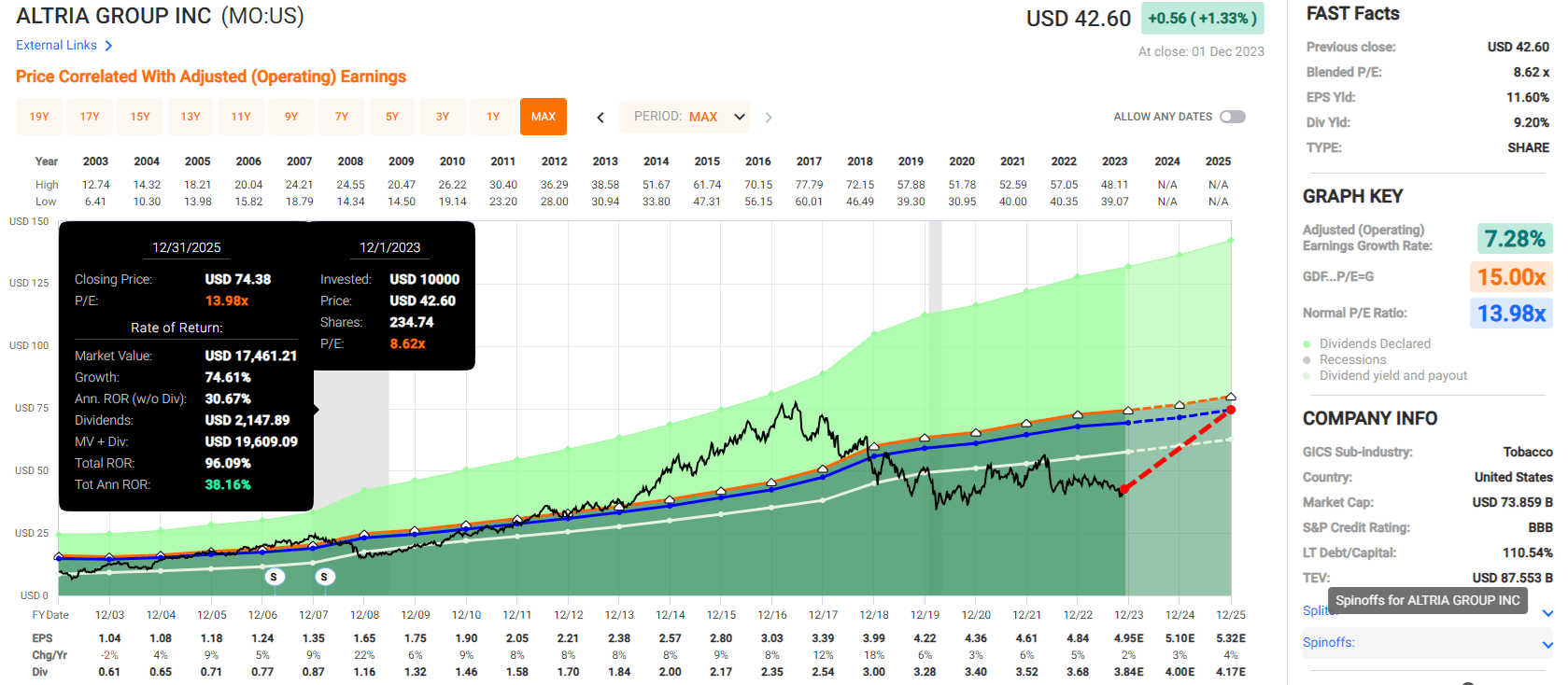

Altria

{kind=link}

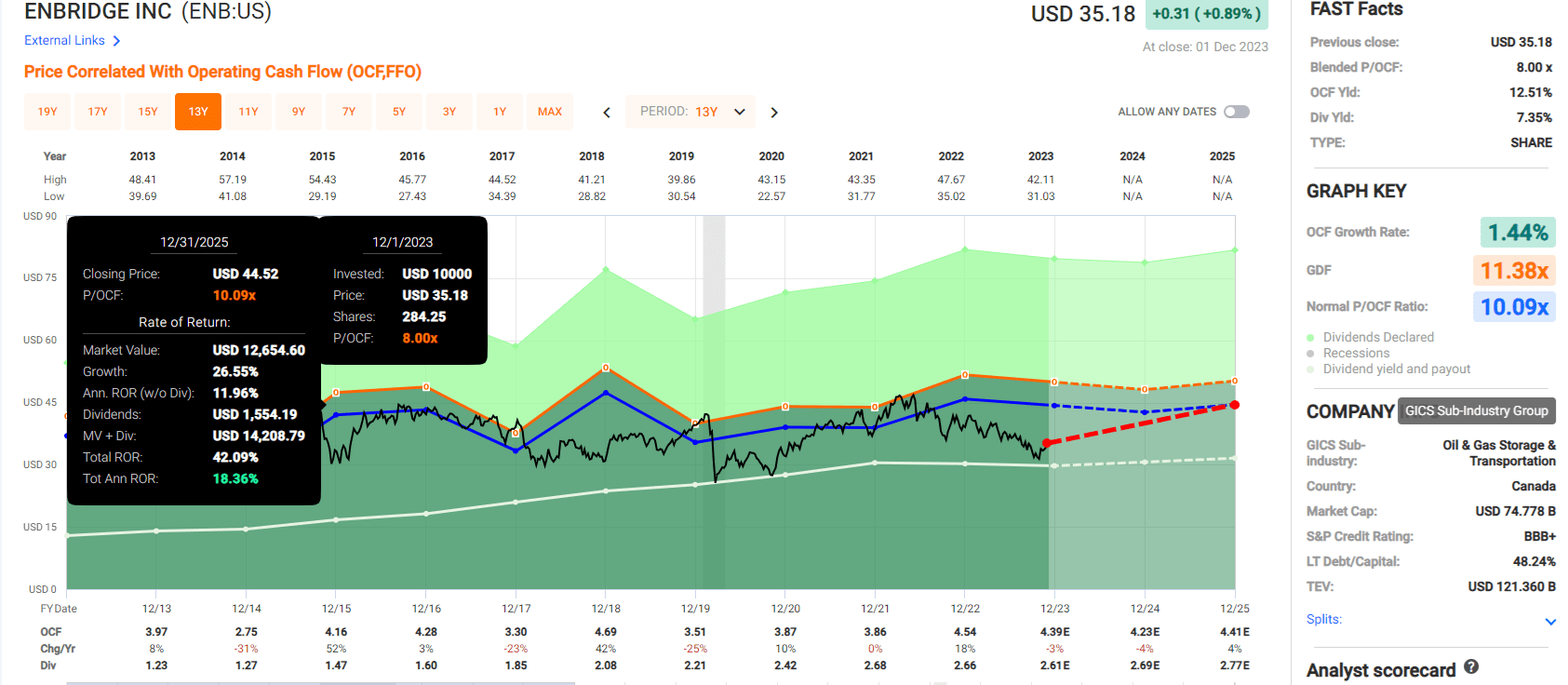

Enbridge

{kind=link}

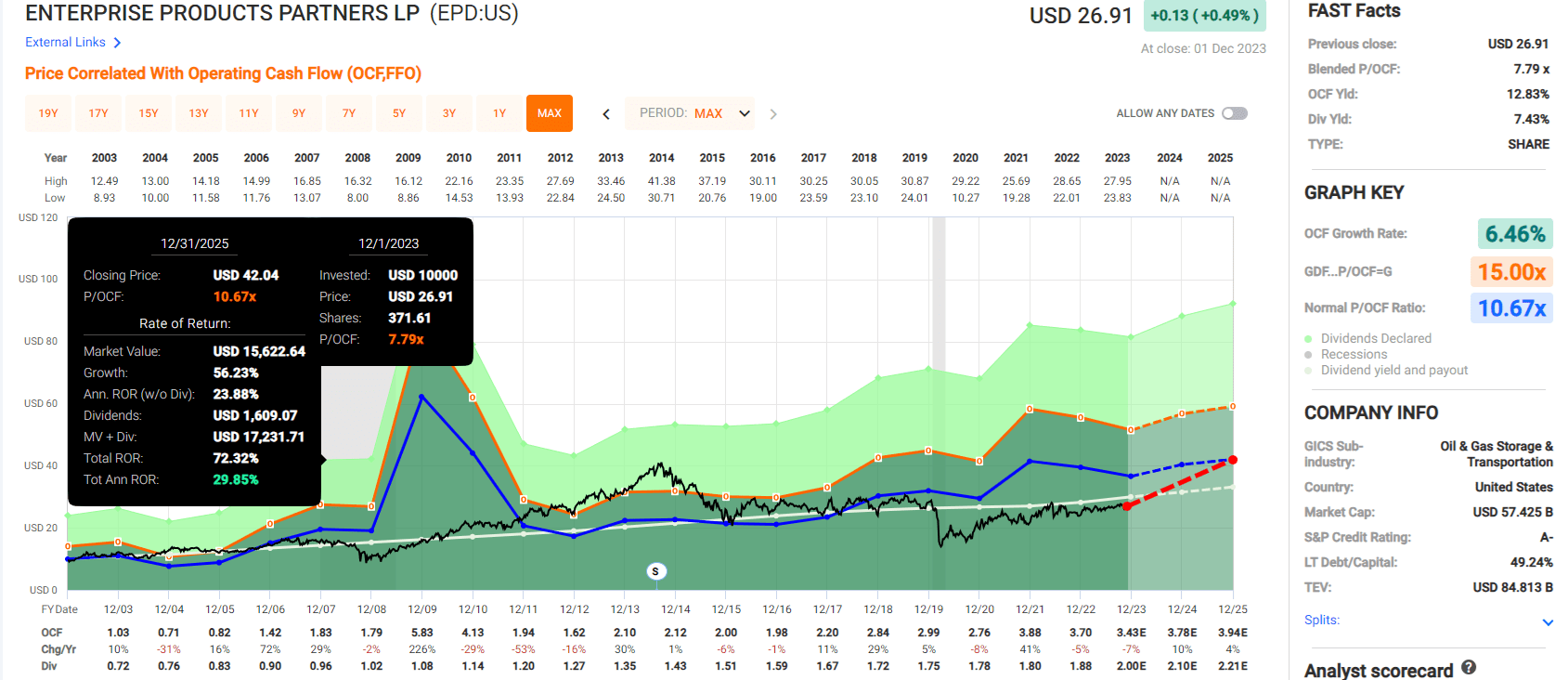

Enterprise Products Partners

{kind=link}

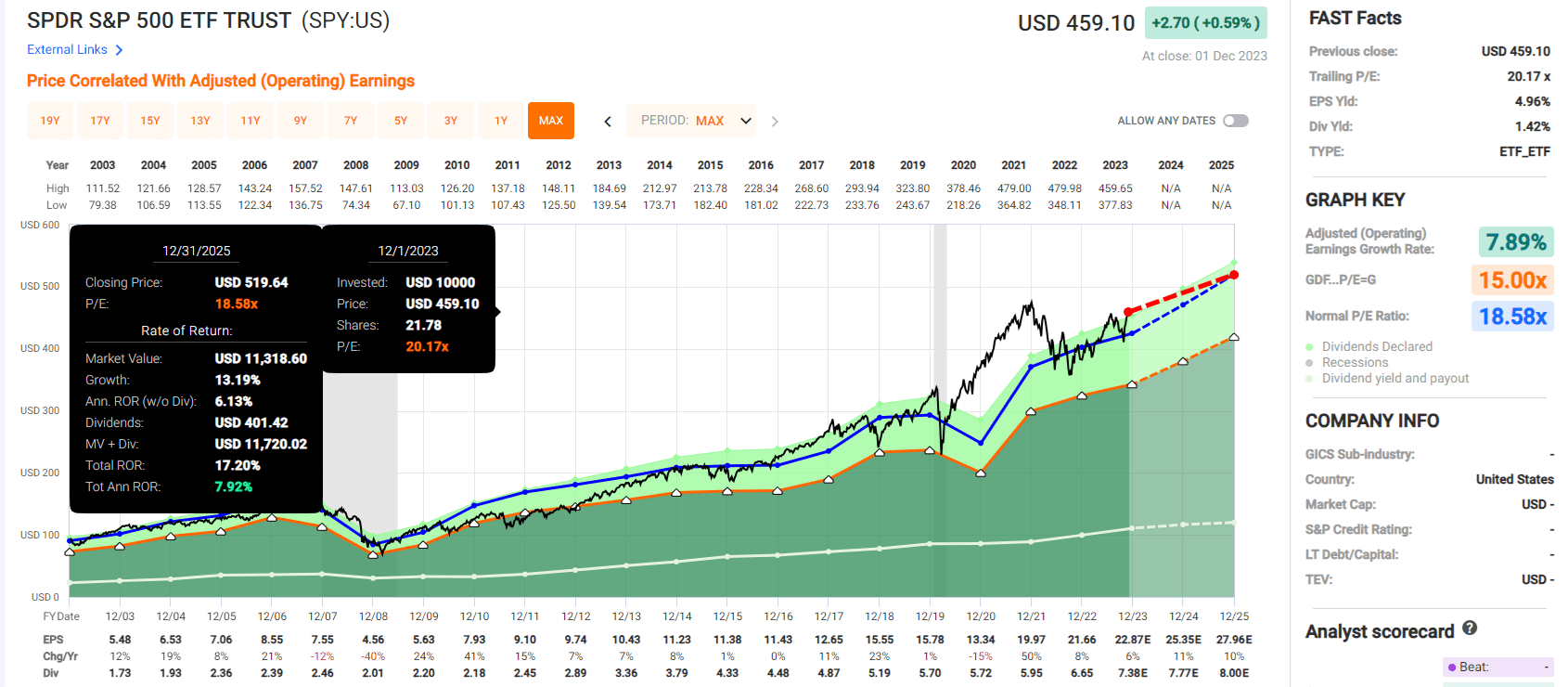

S&P 500

{kind=link}

Bottom Line: Leggett's 8% Yield Is Speculative, And There Are Much Safer Alternatives

Wall Street never runs on certainties but on probabilities.

Dividend aristocrats become aristocrats due to solid, mature, and stable businesses, strong management cultures, good balance sheets, and conservative risk management.

However, even the mightiest aristocrats can fall on hard times, as GE showed so spectacularly and we saw with VF Corp. in 2023.

Leggett and Platt is a solid company, an industry leader in a highly fragmented industry.

Its turnaround plan is sensible, with S&P 66% confident it will work.

However, LEG has been struggling in the best economy in 83 years, and now the economy is weakening. A recession could potentially force management to choose between preserving the investment-grade credit rating and the dividend.

- 6% risk of a dividend cut right now

For some people, a 6% dividend cut risk on an 8% yield with a 5.2% long-term growth outlook is a very attractive proposition.

For those seeking SWAN quality or better, MO, EPD, and ENB offer a superior yield, much better fundamental safety, and similar growth prospects, but with far higher growth visibility.

MO, EPD, and ENB Fundamentals Summary

- Yield: 8.2% (5X S&P 500 and 2.5X more than SCHD or VYM)

- Dividend safety: 100% safe (1% dividend cut risk)

- Overall quality: 96% low-risk Ultra SWAN dividend aristocrats

- Credit rating: BBB+ stable outlook (5% 30-year bankruptcy risk)

- Dividend Growth Streak: 36 years

- S&P LT Risk management global percentile: 70th = low risk (good risk management)

- Long-term growth consensus: 4.0% vs 5.2% LEG

- Long-term total return potential: 12.2% vs 13.2% LEG

- Discount to fair value: 28% discount (potential very strong buy) vs 13% overvaluation on S&P

- 10-year valuation boost: 3.3% annually

- 10-year consensus total return potential: 8.2% yield + 4% growth + 3.3% valuation boost = 15.5 % vs 9% S&P

- 10-year consensus total return potential: = 322 % vs 134% S&P 500

LEG theoretically offers a 20% annual return potential over the next ten years. That's a spectacular opportunity...if everything goes right.

However, remember that LEG's 2023 and 2024 estimates have been sliding by the week and continue to deteriorate.

So keep in mind the speculative nature of LEG's 8% yield when considering whether to buy it or choose safer alternatives like MO, EPD, and ENB.

For further details see:

Leggett's 8% Yield Is Great, But These 8% Yielding Aristocrats Are Much Better Buys