LMAT - LeMaitre: Remaining Constructive On Long-Term Valuations

Summary

- Reasonable growth vertically throughout P&L and cash flows, exhibiting strength in major markets.

- Growth in rep headcount converting at the top line looks to further growth in reps in FY23.

- Valuations support with company reinvesting heavily in future growth and distributing cash back to shareholders.

- Net-net, reiterate buy.

Investment Summary

Following my bullish last publication on LeMaitre Vascular, Inc. ( LMAT ) the stock has ticked ~7% into the green and now trades back near previous highs. Now the company has come through with a robust Q4 earnings print demonstrating continued strengths in regional, divisional growth, coupled with profitability that is generating future value for LMAT shareholders. Net-net, I reiterate that LMAT is a long-term buy on a long-term valuation of $85, and here I'll run through the reasons why, linking back to its recent earnings future growth estimates. In the meantime, check out my previous extensive analyses on this name:

- Balance sheet ready to unlock sick capital

- Reiterate Buy Thesis Following Strong Q2 Numbers

- 16% Return Objective From Idiosyncratic Risk Premia

- Balance Sheet Expansion Adds ~$2 Per Share Value To Date

- Widened Capital Structure, Acquisitions Drive Top-Line Growth

LMAT Q4, FY22 analytics: Growth, profitability the standout

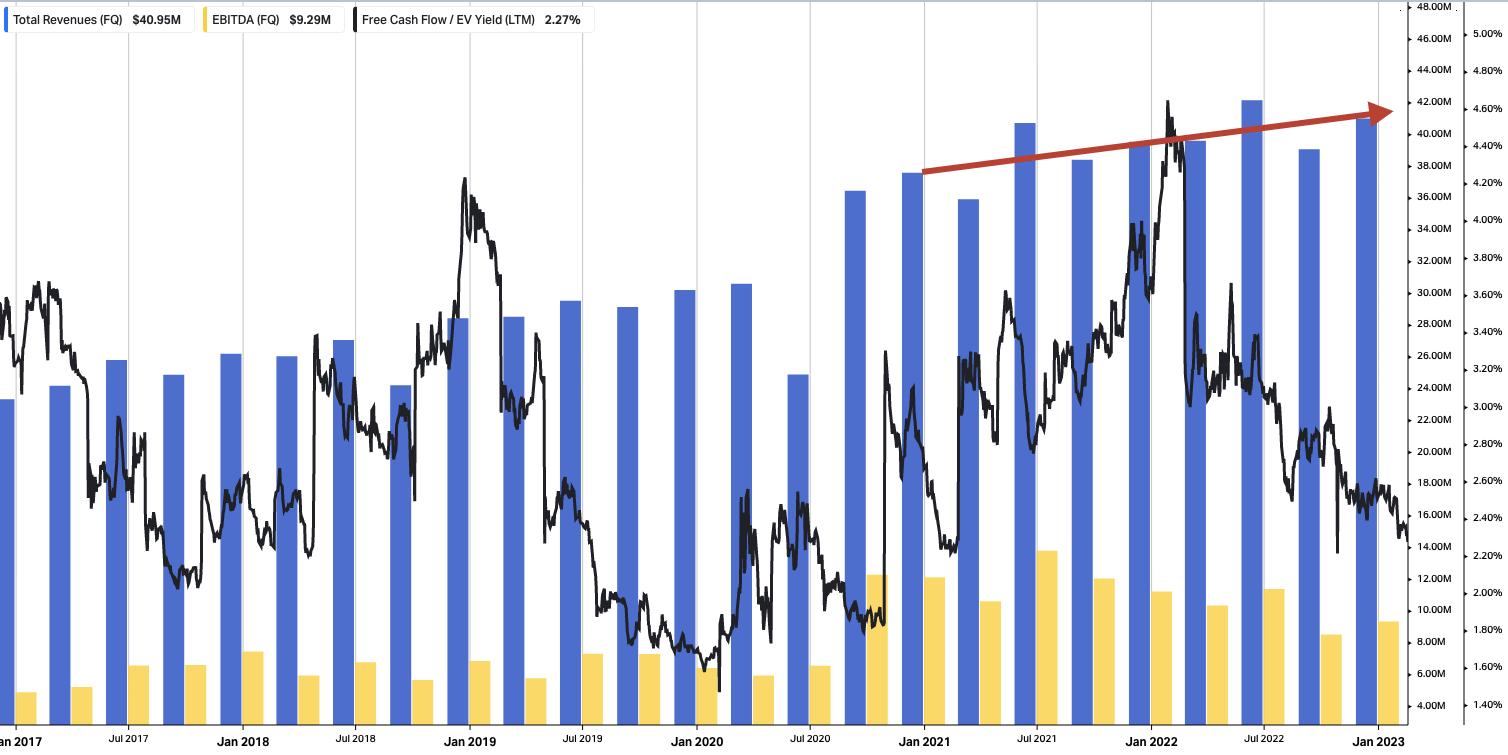

Looking straight at the numbers, I'd allude investors to the fact that LMAT continues stretching top-line sales growth in tandem with long-term averages, with FCF yields cyclical as the company makes ongoing strategic investments for future growth [Figure 1]. Turning to the quarter, Q4 top-line revenue growth pulled in to 400bps on $41mm in turnover. A 410bps FX headwind is baked into this result, subsequently in constant currency terms YoY core business growth was 8% for the period. Looking at its FY22 growth it saw 500bps reported revenue growth to ~$162mm, up 9% when backing out the FX headwind. Further, it saw ~210bps of gross margin compression to 63.6%, yet 150bps came from currency effects. Further impacting the company's cost of revenues, it increased its direct labour manufacturing team by half in FY22', combined with a greater manufacturing footprint in general. I'd say this is a net positive, because, as competitors faced numerous challenges in retaining and growing their workforce, LMAT seemed to have no troubles in this domain. A tick of approval in my estimation.

Fig. (1) LMAT Long-Term Sales, Core EBITDA, FCF Yield

{kind=link}

With respect to the company's regional and divisional growth, highlights for investors are as follows:

- Upsides at the top-line were underscored by 22% growth in APAC, 9% expansion in its EMEA footprint and another 6% throughout the Americas.

- Looking at divisional growth, the company's carotid shunts led the way with 24% YoY growth schedule, whereas the company's biologics and bovine grafts businesses recognized 11% expansion. I would point out however the company has a large back order in its omniflow segment, which saw sales clip down by 55%, however this could also prove to be a meaningful tailwind as we progress through the year. I'll be watching this carefully in the upcoming quarter, as management see it sorted by Q2.

- The company also booked its first sales in Korea, its newest and 25th direct market and forecasts $1.2mm in revenues from this in FY23.

Looking at the productivity numbers in greater detail, LMAT noted it now has 131 within its sale rep headcount after an aggressive 27% growth in rep numbers over the year. The biggest growth of 40% was observed in its APAC region, reflecting the top-line growth there. A few points must be recognized from this data:

- The larger rep headcount means each individual rep has less of an area to cover, which means more penetration of individual markets and better contact with providers [vascular surgeons, hospitals].

- Revenue per rep came in to $312,980 for the quarter and this is a robust number. However, I'd point out that I called for LMAT to hit $330,500 in revenue/rep to meet its guidance back in Q3 FY22 - but this was a projected 125 rep count. If we adjust the calculations for the 125 number, the company hit ~$330,000 in revenue/rep and this is a positive factor.

- Management also project 135-140 sales reps in its headcount by the end of FY23. Subsequently, it projects Q1 sales growth at 13% organically and this would be a record to $43.8mm. Hence, the investment in human capital looks to be paying dividends at this point in time. At 135 in the headcount, each rep would hypothetically need to generate $324,440 in revenue to hit the $43.8mm mark - hence illustrating the benefit of increasing the headcount in the first place, as each member needs to generate less revenue in order to hit the target.

Understandably, therefore, the company's operating margins were impacted from the increased headcount, at 17% by the end of Q4 after an 8% YoY increase. But one thing I'd point out is that management expect the investments in human capital listed above to come through in FY23', backing in a reduction in OpEx by 11% [from a 15% growth in FY22], and therefore looks for a 19% expansion in operating income for this year. Added to that, it expects 625 staff in total on its books by year's end, another 30 or so from last year.

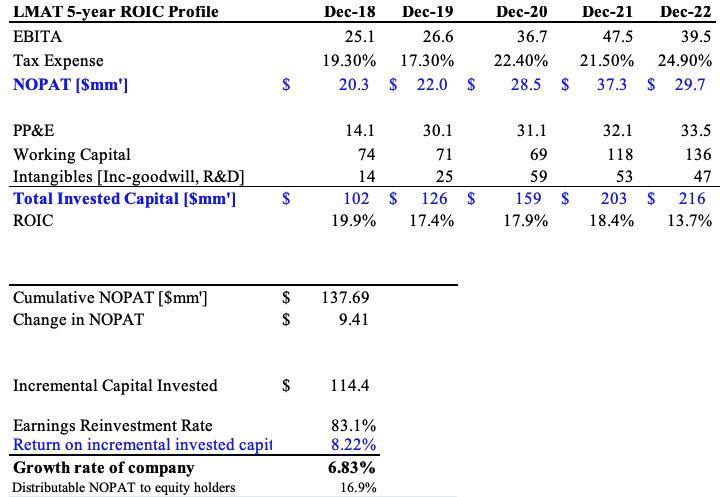

Extending from the points on investment into future growth from above, I'd suggest it is important to note that profitability is a standout in the investment debate for LMAT. It is rated an 'A' for profitability in the quant grading system and is positioned well above the sector at an 8% trailing ROE [~10% using non-GAAP earnings] and 13.7% trailing ROIC. This number has crept down from FY18 yet the company has also allocated additional $114mm in capital investment over this time, generating $137mm in post-tax earnings on an additional growth of ~$9.4mm in NOPAT over that time. Subsequently, the incremental ROIC on the long-term investment is 8.22%. In that vein, the company has reinvested ~83% of its post-tax earnings into future growth and realized a reasonable rate of return. As a footnote, the company's growth rate over this time has been ~6.8%, not too far off the CAGR of its stock price of 7.25% since FY18.

Fig. (2)

Data: Author, using data from LMAT SEC Filings

{kind=link}

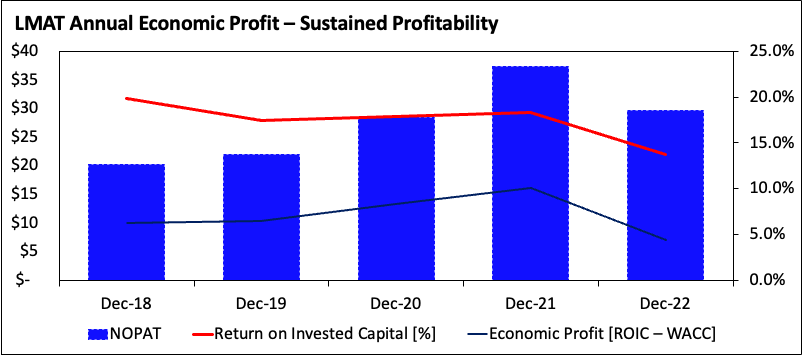

Added to this, the ROIC spread above LMAT's hurdle rate has been equally as positive, generating consistent economic profit along the way. Economic profit is defined as the ROIC less the cost of capital, and is essential to observe in a firm generating value for shareholders as it suggests the company is able to generate a return on its investments above what it cost to make the investment in the first place, per Mauboussin (2022) . For those observing Figure 3, you'll note the economic profit for FY22 was 4.4%. Notwithstanding the fat it generated an additional $12.7mm in CFFO in Q4 and increased its dividend payout to $2.7mm. In that vein, all of the growth accrued by LMAT across FY22 was accretive to shareholder value. This discussion on profitability is critical in making inferences on the company's propensity to deliver ongoing profitability and bottom-line growth looking ahead.

Fig. (3)

Data: Author, using data from LMAT SEC Filings

{kind=link}

FY23 guidance points to further growth momentum

Another highlight in the current LMAT investment debate is that it expects 9% core revenue growth in FY23, calling for $178mm at the upper bound. It looks to pull this down to $30-33mm in operating income, a 19% growth at the midpoint, and an increase of 24% of earnings to $1.20 per share at the upper end of range. The question then turns to what will get LMAT there. In my estimation, based on the company's recent trajectory, I'd suggest it comes down to 3 main implications:

- Management implemented a price hike across its portfolio of ~500-600bps from January 1st this year. I'm not sure of the exact regions it made these, presumably in its main markets and on the remainder of its volumes for the year. Hence, we'd need to see volumes at least remain sticky for the entire year to drive the upside here.

- As mentioned earlier, the company expects to have anywhere between 135-140 reps under its wings by the year of the end. Subsequently, it depends on a) how well these reps convert; b) the absence of underperforming reps i.e. their quality/efficiency; c) low turnover within the established headcount; d) the total revenue per rep. If any of these factors slip, this could impact the guidance number.

- I'd also suggest the performance of the company's expanded footprint in APAC and Korea will be key performance drivers for the year. Management hinted in strong growth in Japan throughout this 1st quarter, a good point to note given its efforts in applying for a carotid indication in that market. Hence, there's a few moving parts with its geographical footprint that could either accelerate or decelerate growth early in the year.

Combined, my estimate is that growth assumptions looking ahead would hinge largely on an outperformance in these domains.

Valuation and conclusion

The company trades at a premium to the industry at 43x forward P/E and 23.7x forward EBITDA. On face value this may seem expensive. However, here I'm going to attempt to demonstrate investors why I believe this is still undervalued, considering the company's profitability and sustainable growth rate to justify a higher multiple.

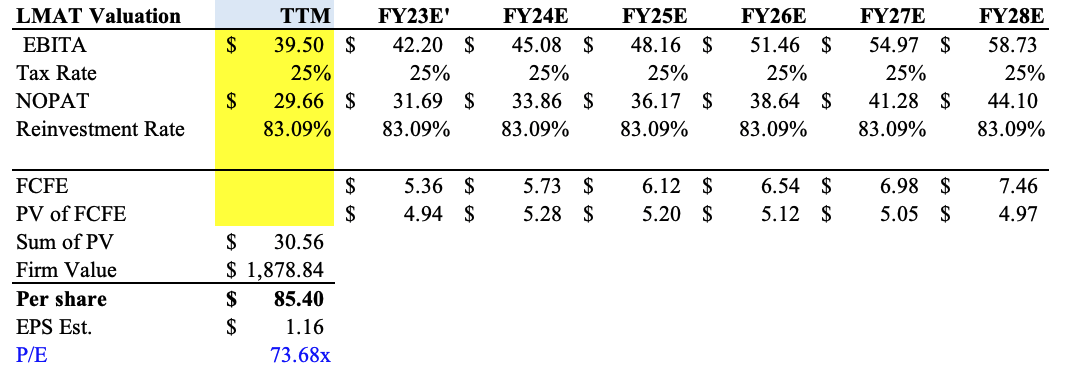

To value LMAT I've taken a discounted cash flow that factors in the 4 main drivers of future growth and value creation for shareholders, per Mauboussin ( 2014 ; 2014 ; 2022 ) and Morgan Stanley ( 2020 ; 2021 ). Specifically, the calculus estimates fair value with the combination of 1) reinvestment of post-tax earnings for growth; 2) the incremental return on this reinvestment; 3) the corresponding growth rate in post-tax earnings; 4) the residual cash flows distributable to equity holders. Here I've taken a 5-year investment horizon [in-line with my own horizon] to gauge the cash flows one would receive over this time. I've assumed that LMAT will continue reinvesting >80% of its post-tax earnings over this time, a 25% tax rate and a geometric company growth rate of ~6.8%. Discounting the estimated FCF's at an ~8.5% discount rate [current S&P 500 earnings yield + UST 10yr yield]. Next is to apply the Gordon Growth Model with each of these parameters to estimate the corporate value, per Epoch Investment Partners (2019) and McKinsey (2020) . On these basic assumptions, net-net, I value the company at a market cap of $1.88Bn, otherwise $85.40 per share. On its FY23 EPS estimates, this justifies a 73.7x P/E. Note, the calculations don't include the company's dividend growth and with this included I see the stock potentially even higher.

Fig. (4)

{kind=link}

Net-net, I reiterate LMAT at a buy on long-term value. The company continues putting its balance sheet to effective use, investing in strategic areas to fund future growth. Looking at its profitability and ability to fund its future growth initiatives, whilst maintaining a constant dividend payment and distribute a reasonable amount of FCF's to equity holders, the stock commands a high multiple and could be resilient in the face on an economic downturn as well. Subsequently, I rate LMAT a buy on a long-term valuation of $85.40.

For further details see:

LeMaitre: Remaining Constructive On Long-Term Valuations