LEN - Lennar Corporation: Rating Upgrade As Orders Momentum Was A Positive Surprise

2023-09-21 09:04:05 ET

Summary

- Lennar Corporation's 3Q23 results show strong order growth, leading to a revision of the rating from hold to buy.

- The company's performance exceeded expectations, with operating EPS of $3.91 and robust order increases in multiple regions.

- Management's proactive approach to reducing cycle times and improving efficiency, along with a solid balance sheet, support positive near-term outlook and continued growth.

Summary

Following my coverage of Lennar Corporation (LEN)( LEN.B ), I recommended a hold rating due to my expectation that FY23 and FY24 will be difficult years for the business. This post is to provide an update on my thoughts on the business and stock after the 3Q23 results. I am revising my rating from hold to buy as I am now much more positive on the near-term outlook after seeing the order growth strength in 3Q23.

Investment thesis

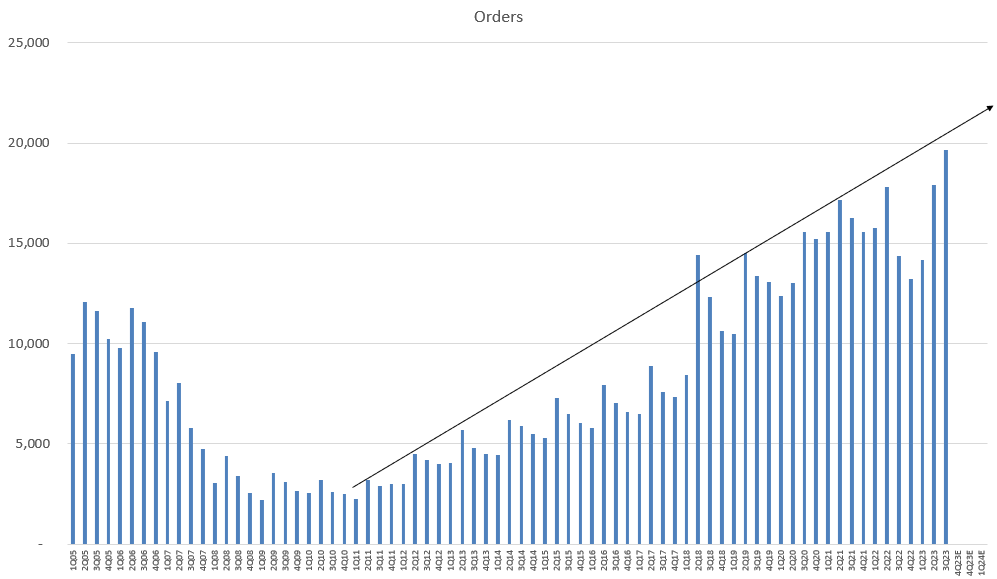

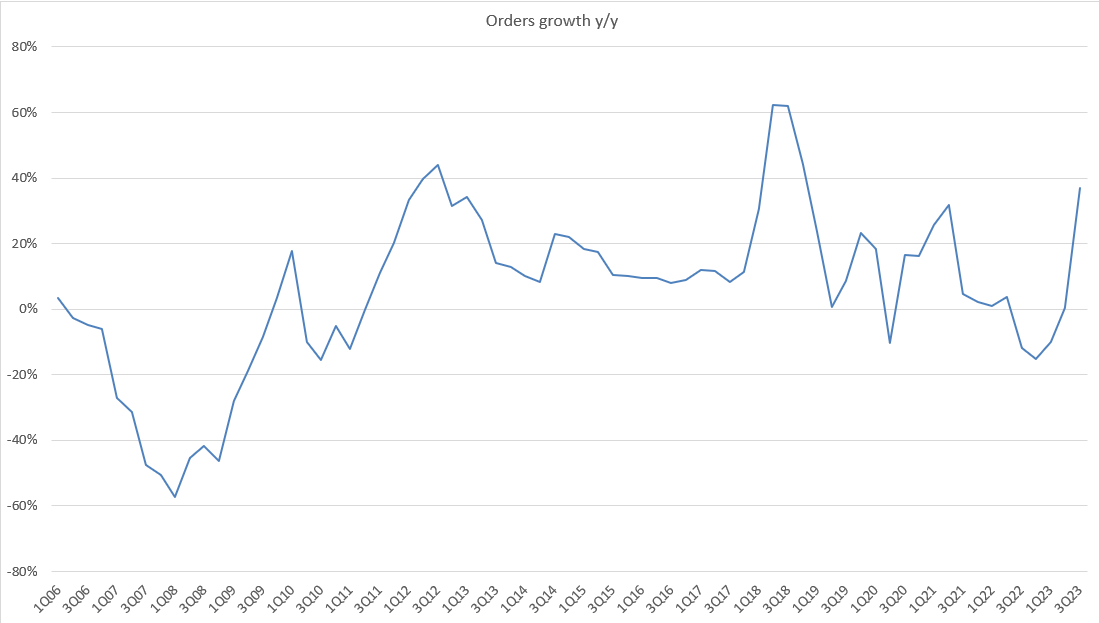

LEN's 3Q23 operating EPS came in at $3.91, well above the $3.51 expected by consensus, on revenue of $8.7 billion. Texas and the West saw the largest increases in unit orders, at 84% and 67%, respectively, while the East saw the smallest increase, at 2%. When factoring in the annual increase of 5% in the number of communities, the resulting increase in monthly sales pace to 5.2 homes per community is 30%. In my opinion, the results were fine, and management forward-looking commentaries were very encouraging as well, albeit the market did not react positively (stock was down 6% at one point before recovering).

To begin, orders in 3Q excluding JV was extremely strong, which is not something I would anticipate in a weak macro environment. The 37% increase in 3Q orders was significantly higher than the 25-32% increase forecasted by management (2Q23 was only 1%). Absorption increased by 31%, while the average number of communities increased by only 4%. The Central region saw a 32% increase in orders, the East region a 2% increase, and Texas and the West saw an 84% increase in orders. The company highlighted areas of relative strength, such as Florida and the Carolinas, as well as areas where more incentives were needed, such as Austin and Boise, as well as regions of California. As a result of the significant improvement in cycle times in 3Q and the very strong growth in both orders and closings, management upgraded their forecast for closings in FY23 from 68-70k to 70.6-71.6k (which implies an upgrade of 300bps at the mid-point from 4.5% to 7.5%). Even more positively, management anticipates that cycle times will continue to decrease through the end of the year and into FY24. In its initial FY24 forecast, LEN projected a 10% increase in volume.

The ongoing restrictions in the resale market have also contributed to LEN.B consistent demand. Management has highlighted that higher interest rates are having less of an impact on demand and that consumers have adjusted to the new normal. In my opinion, buyers are being driven toward new construction due to a lack of available, reasonably priced homes in the secondary market. Leading indicators mentioned by management were also encouraging, in that cancellations have returned to typical levels and there has been a sequential increase in home absorptions in most markets. This trend has been spearheaded by the Carolinas, Florida, and even some areas of Texas.

Viewed together, there seems to be a constraint on supply, which coupled with management strong execution on driving order growth and the past few weak quarters (indicating demand being pushed back), I now believe order growth can continue at this rate for the near term. If we assume the same growth trend, the next 3 quarters should continue to be in the range of ~20k, implying high y/y growth.

{kind=link}

{kind=link}

Despite its robust growth prospects, the management has remained committed to its cash-oriented strategy. After reviewing the third-quarter results, I am even more confident in the company's ability to capitalize on the housing undersupply while prioritizing cash generation. The company has maintained a healthy cash position of approximately $4 billion, and its debt has significantly decreased, further enhancing the quality of its financial position. Importantly, the company intends to continue its share repurchase program as a consistent part of its capital allocation strategy.

As the normalization of supply chains proceeds, I expect an uptick in inventory turnover rates and a closer match between construction starts and actual sales, both of which will have a beneficial effect on cash flow. It's worth noting that the company's land supply has decreased from 1.7 years in 2Q23 to 1.5 years in 3Q23, with 73% of available lots already optioned. Moreover, the majority (85%) of the company's most recent acquisitions were finished parcels, which should drive improvements in inventory turnover, which has increased from 1.1 to 1.3 since the same time last year. These actions should help steer the company towards its long-term objective of achieving 100% FCF conversion.

Valuation

{kind=link}

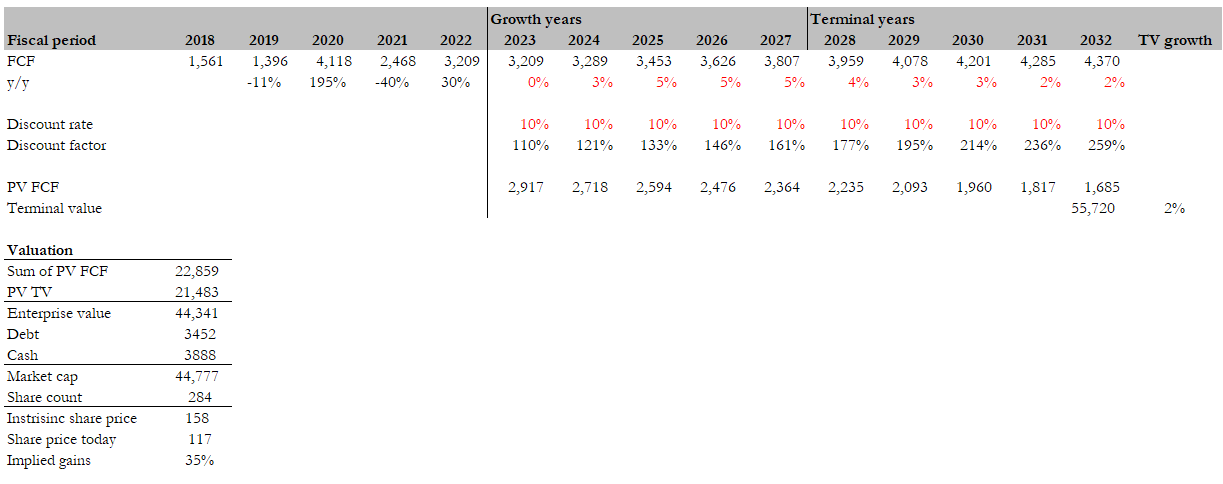

With the drop in share price and improved outlook over the near term, I believe the LEN.B. share price is attractive today. Reusing my previous model with updates in FY23 and FY24 to reflect my improved outlook, I believe the fair value for LEN.B is $158. My model assumptions are that LEN will continue to see order momentum sustain through FY23 and gradual improvement in FY24. Post FY24, my assumptions are the same as my previous stance, where I expect LEN to grow at the same rate in the mid-single digits, mirroring the GDP growth rate with a slight premium as it catches up on growth. In the terminal years, I expect growth to slowly normalize to 2% (inflation levels). I note again that this growth is lower than global real estate growth , which is fair as the US is much more developed. In addition, LEN.B. now has a better balance sheet (reflected in the lower net debt position), which has a positive impact on my target price.

From a valuation perspective, the stock has traded down to 8x forward PE, 2x downward revision vs. my last post. I expect multiples to rerate back to 10x as the market becomes convinced that the growth momentum continues for the next few quarters.

Risk

Restating my previous thoughts on risk here: the key short-term risk is higher interest rates, which will hinder affordability for customers. Other risks also include a mis-execution in LEN's current strategy to lean, which might impact its ability to capture a recovery in demand as it lacks manpower.

Conclusion

I upgrade my rating from hold to buy, primarily due to the impressive order growth witnessed in 3Q23. The company's strong performance, with operating EPS surpassing expectations and robust order increases in several regions, instills confidence in its near-term outlook. Furthermore, management's proactive approach to reduce cycle times and enhance efficiency bodes well for cash flow generation, supported by a solid balance sheet with reduced debt and a strong cash position. As supply chains normalize, I anticipate improved inventory turnover and a more synchronized relationship between construction starts and sales. This, along with the company's strategic focus on finished parcels and a constrained housing supply, positions LEN.B for continued growth.

For further details see:

Lennar Corporation: Rating Upgrade As Orders Momentum Was A Positive Surprise