LEGH - Lennar Q3 Earnings Preview: A Pivotal Moment

Summary

- Lennar Corporation is due to report financial results covering the third quarter of its 2022 fiscal year.

- This will prove to be an important moment for investors given what is going on in this space and it could go a long way to determining the firm's trajectory.

- LEN stock looks cheap enough, even if financial performance weakens, to offer some long-term upside for investors.

Right now, the housing market is in a really interesting spot. Although it's true that the US continues to suffer from a housing shortage, it's also true that rising interest rates, higher inflation, and general concerns about potential economic malaise, have all coalesced to create some real near-term risks for the market. One company that could very well be impacted by this rather soon is Lennar Corporation ( LEN ), which focuses on the building and selling of homes. Fundamentally, the company has done extraordinarily well as of late. Revenue and profits have been through the roof and shares of the company are trading at incredibly low levels at this time. This creates a rather difficult situation for value-oriented investors.

On the one hand, fundamentals likely will deteriorate moving forward. But eventually, the market should post some recovery. My argument is that, in the near term, shares might experience further downside. But ultimately in the long run, even if financial performance reverts back to what it was a couple of years ago, shares would still be trading on the cheap. When management reports financial results covering the third quarter of the company's 2022 fiscal year after the market closes on September 21st, investors will have the first look in three months into how the fundamental strength of the company is currently holding up. Analysts expect positive results, but where the company heads in the near term will likely be determined by new orders, deliveries, and management outlook for the foreseeable future. While I do acknowledge that the near-term outlook for the company is anything but great, I do think that, for long-term investors, now might be a great time to consider initiating a position in the firm or adding on to a position that might already exist.

Lennar - Building up to the big moment

The last time I wrote an article about Lennar was back in late November of 2021. In that article, I talked about how the company had seen a rise in activity over the prior few years, driven by a surge in demand for housing. I called the company's fundamental condition impressive and said that shares looked cheap on an absolute basis even though they looked more or less fairly valued compared to similar firms. At the end of the day, I called the company a cheap play on the housing market and assigned it a 'buy' rating, reflecting my belief that it would likely outperform the broader market for the foreseeable future. Since then, things have not played out exactly as I anticipated. While the S&P 500 has dropped by 16.2%, shares of Lennar have generated a loss for investors of 25.8%.

{kind=link}

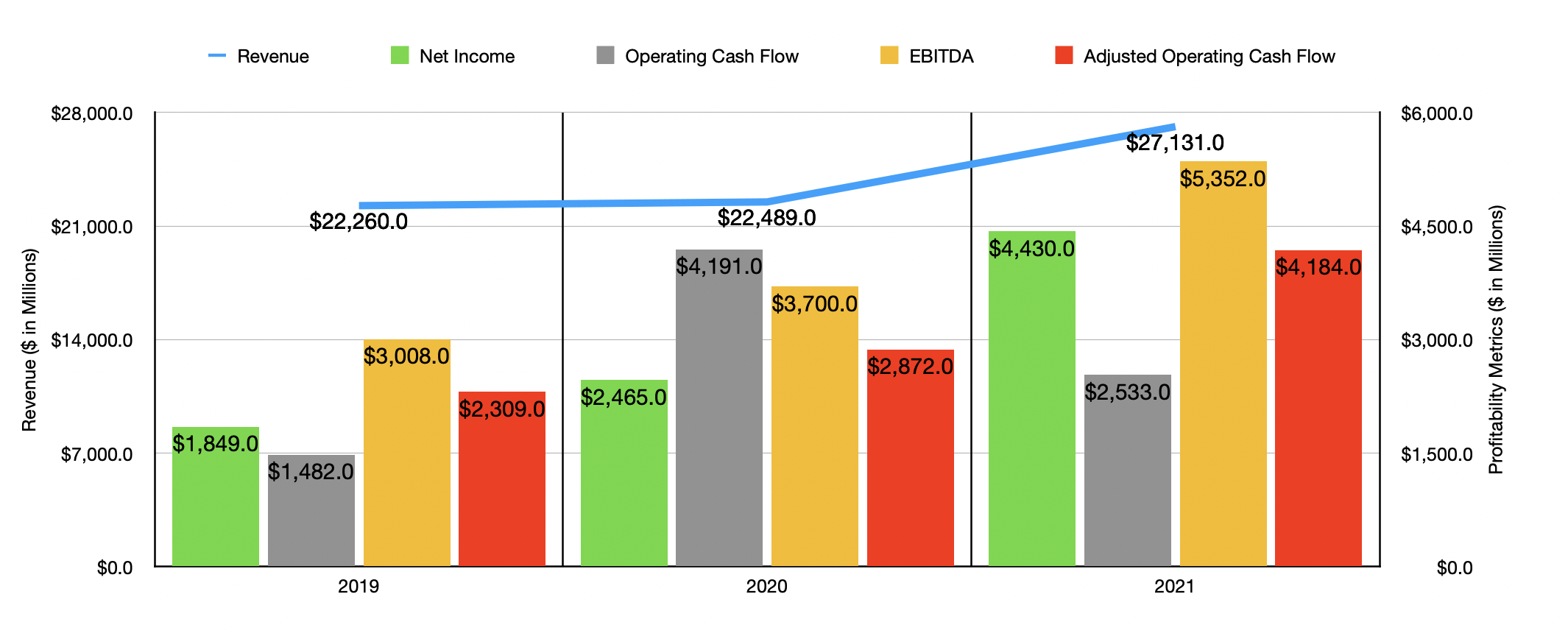

At first glance, this might make it seem as though the company's fundamental condition had deteriorated. But that couldn't be further from the truth. Let's consider, for instance, how the company ended its 2021 fiscal year . Revenue for that year came in at $27.13 billion. That represents an increase of 20.6% over the $22.49 billion the firm generated the same time one year earlier. This increase was driven by a couple of key factors. One of them was a rise in the average price that it received for houses that it produced. On homes delivered, the company generated revenue of about $424,000 apiece. Average revenue in 2020, meanwhile, was $394,000. To put this in perspective, this disparity would have added additional revenue of $1.59 billion just based on the number of homes delivered in 2020. But that wasn't the only increase we saw. We also saw deliveries rise to the tune of 13%, climbing from 52,925 to 59,825.

This rise in revenue brought with it a nice increase in profits. Net income for the company rose from $2.47 billion to $4.43 billion. Operating cash flow actually dropped from $4.19 billion to $2.53 billion. But if we were to adjust for changes in working capital, it would have increased from $2.87 billion to $4.18 billion. We also saw a nice increase in EBITDA, with the metric rising from $3.70 billion in 2020 to $5.35 billion last year.

{kind=link}

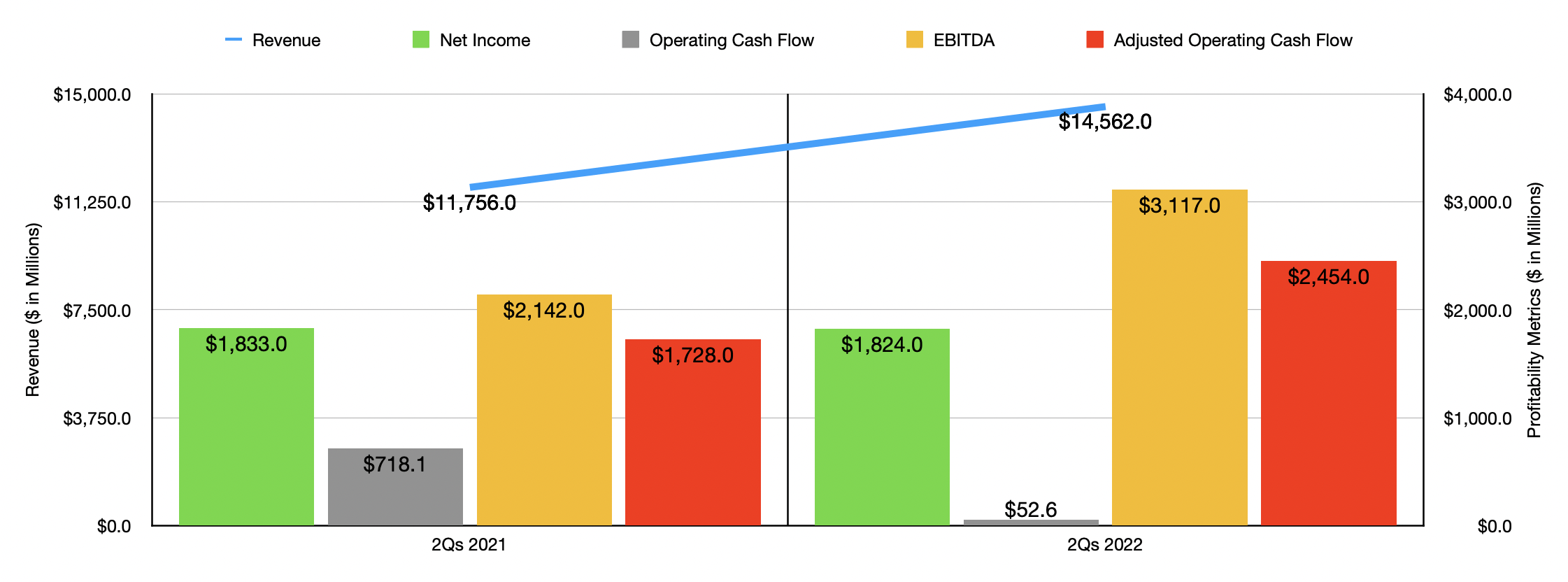

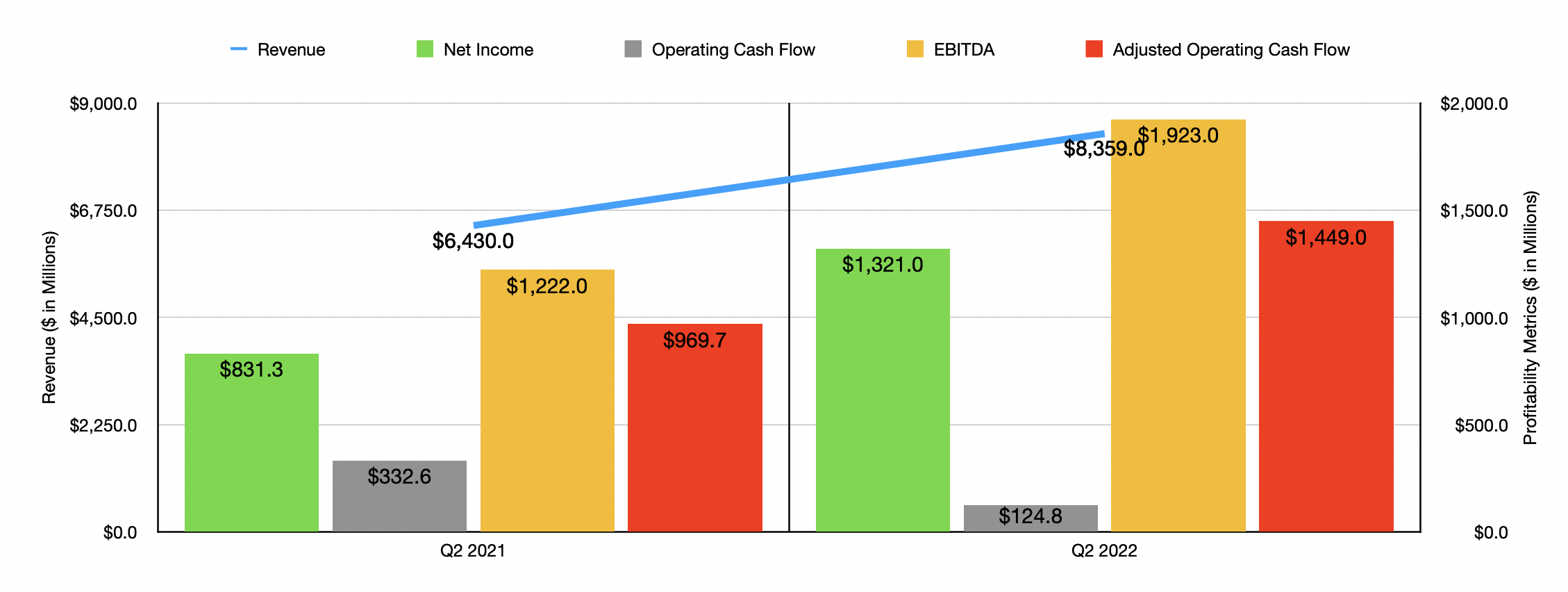

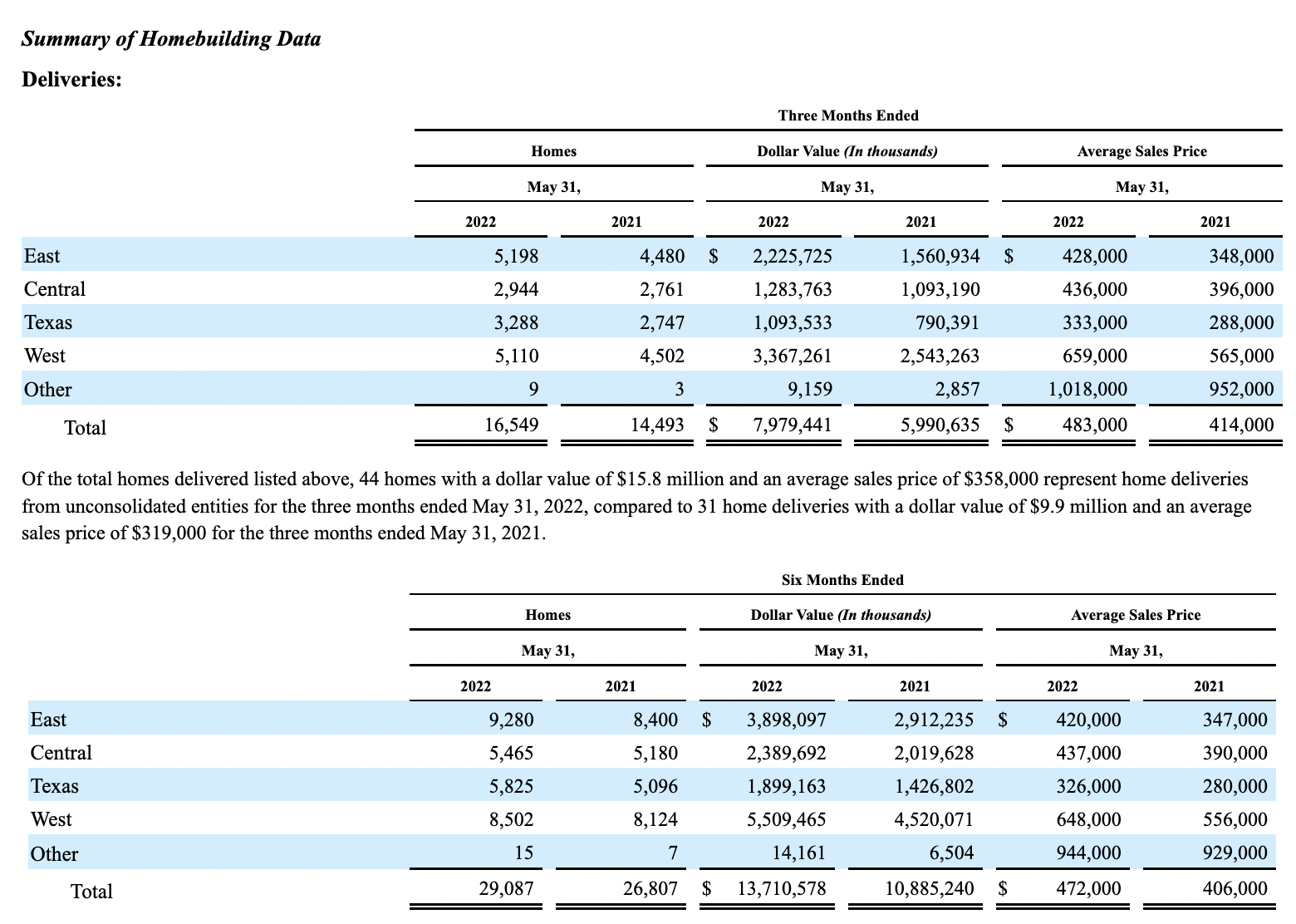

So far, the 2022 fiscal year has proven to be remarkably robust for the firm. Revenue in the first half of the year totaled $14.56 billion. That's 23.9% above the $11.76 billion reported one year earlier. This rise was driven again by a sizable increase in the pricing of deliveries from $406,000 in the first half of the 2021 fiscal year to $472,000 the same time this year. In addition to this, the number of deliveries rose from 26,807 to 29,087. As you can see in the data provided in my charts, this strength continued into the second quarter alone as well. Revenue of $8.36 billion beat out the $6.43billion experienced one year earlier. This was thanks to deliveries rising from 14,493 to 16,549. And it was also due in part to prices of homes delivered climbing from $414,000 to $483,000.

{kind=link}

As can be expected, this increase in revenue so far this year has been instrumental in pushing some of the company's profitability metrics up. But not every profitability metric showed signs of improvement. In fact, net income reported by the company dropped modestly from $1.83 billion to $1.82 billion. Operating cash flow also declined, dropping from $718.1 million to $52.6 million. If, however, we were to adjust for changes in working capital, it would have risen from $1.73 billion to $2.45 billion. Meanwhile, EBITDA for the company also increased, climbing from $2.1 billion in the first half of 2021 to $3.1 billion the same time this year.

{kind=link}

{kind=link}

{kind=link}

After the market closes on September 21st, the management team at Lennar is due to report financial performance covering the third quarter of the company's 2022 fiscal year. This would be an important quarter since it will help us gauge not only how the company has dealt with a difficult housing market in recent months, but also with what management guidance is moving forward. Generally speaking, we do know that things have not been going perfectly when it comes to the housing market. Homebuilder confidence dropped in the month of August, representing the ninth straight month of declines. And the most recent housing starts data was rather disappointing. That number was 1.466 million in August of this year. Not only was that down compared to the 1.554 million reported one year earlier, it also missed analysts' expectations of 1.540 million.

{kind=link}

Despite this trend of weakness, analysts have high expectations for the company from a revenue and earnings perspective. The current expectation is for the company to generate revenue of $9.09 billion. That compares to the $6.94 billion reported one year earlier. Earnings per share should be $4.82, or $4.87 on an adjusted basis. This translates to net income of $1.40 billion or $1.41 billion on an adjusted basis. To put this in perspective, earnings per share last year totaled $4.52. That translated to nearly $1.41 billion in profits. All of this is important to keep an eye on, as will be the cash flow of the company. But perhaps the most important thing would be the leading indicators of the company. In its second quarter earnings release, management said that new orders would be between 16,000 and 18,000 homes. They also said that they expect deliveries to be between 17,000 and 18,500, with average sales prices slightly above with the company reported for the second quarter. Any weakness in terms of new orders, deliveries, or sales prices, could be a sign of additional pain in the near term.

{kind=link}

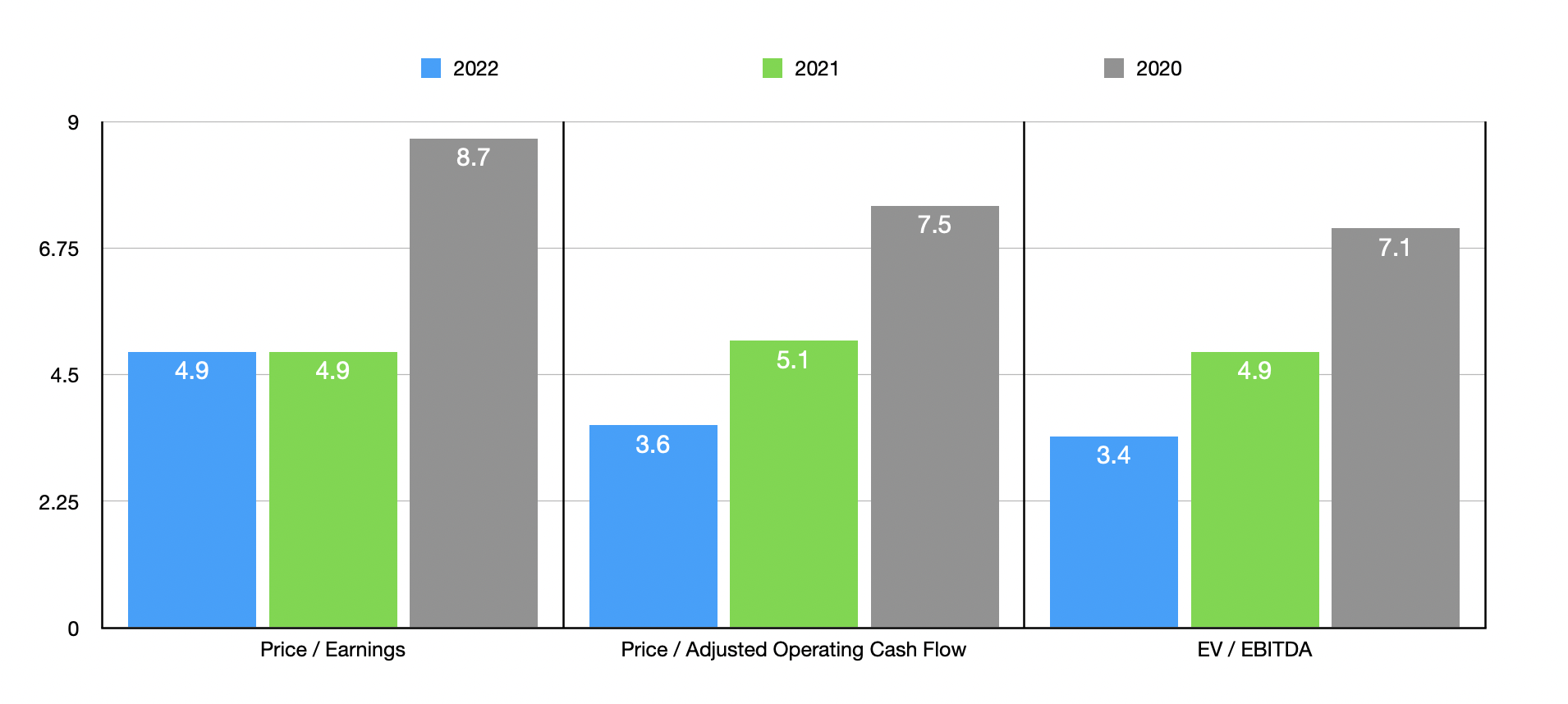

Even if the company does experience some downside in the future, shares are likely going to look cheap in retrospect. If we were to annualize results experienced so far for the first half of the year, we should anticipate net income for 2022 of $4.41 billion, adjusted operating cash flow of $5.94 billion, and EBITDA of $7.79 billion. These would translate to forward multiples that are quite low. For instance, the price to earnings multiple would come in at 4.9, while the price to adjusted operating cash flow multiple would be even lower at 3.6. But the lowest would be the EV to EBITDA multiple of 3.4. As you can see in the chart above, shares would still be cheap even if financial performance reverts back to what it was in the 2020 fiscal year. Also as part of my analysis, I compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 3.2 to a high of 7.5. And when it comes to the EV to EBITDA approach, the range was between 3 and 6. Compared to the pricing of Lennar using data from 2021, we can see that four of the five companies are cheaper than it. When it comes to the price to operating cash flow approach, the opposite is true, with the multiples ranging between a low of 7 and a high of 4,289, with our prospect being the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Lennar Corporation |

| 4.9 |

| 5.1 |

| 4.9 |

| PulteGroup ( PHM ) |

| 4.5 |

| 15.0 |

| 3.6 |

| Meritage Homes Corporation ( MTH ) |

| 3.2 |

| 25.6 |

| 3.0 |

| Legacy Housing Corporation ( LEGH ) |

| 7.5 |

| 7.0 |

| 6.0 |

| Tri Pointe Homes ( TPH ) |

| 3.6 |

| 11.5 |

| 3.9 |

| D.R. Horton ( DHI ) |

| 4.7 |

| 4,289.0 |

| 4.0 |

Takeaway

Right now, the fundamental data for Lennar looks really impressive. Although the company might be pricier than many of its peers, it is still cheap on an absolute basis. Investors are right to worry about current market conditions and the impact that might have on housing. It is also true that, as a result, the company could suffer for a few quarters or even a couple of years. But even seeing financial performance pull back some, shares would still likely warrant some upside. And once the market does recover, the upside for investors from here could be quite significant. Due to this, I've decided to keep my 'buy' rating on the company for now.

For further details see:

Lennar Q3 Earnings Preview: A Pivotal Moment