LEN - Lennar: Strong Earnings And A Resilient Housing Market Make It A Buy

2023-09-14 20:04:46 ET

Summary

- Lennar's shares have risen 60% in the past year, despite high mortgage rates, due to structural factors supporting the housing industry.

- Lennar's earnings report showed solid performance, with deliveries rising 8% and a backlog of 21,321 homes worth $9.9 billion.

- The company's strong balance sheet, low debt levels, and ability to reduce share count support its earnings growth and provide financial flexibility.

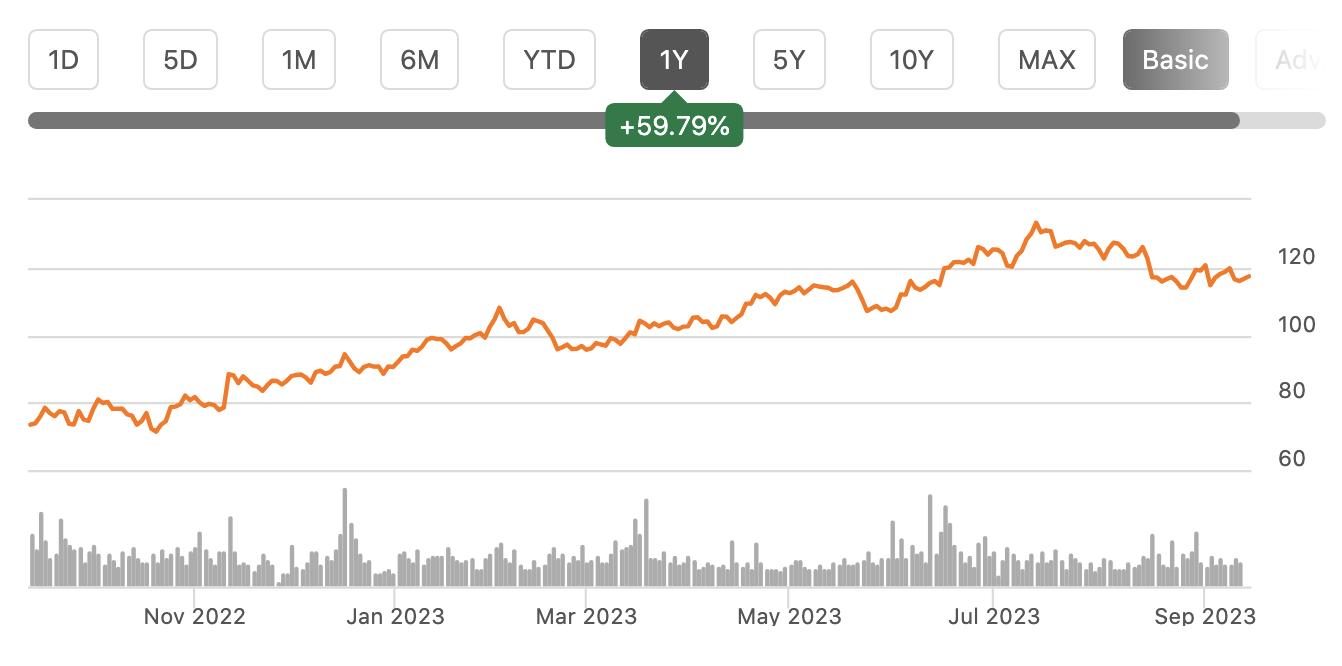

Shares of Lennar (LEN) have been a tremendous performer over the past year, rising about 60%. Given mortgage applications have been steadily falling with rates over 7%, the strong performance from the homebuilders may be surprising. However, there are structural factors supporting the industry, and as we saw Thursday afternoon with its earnings release, the company is performing well. Even after the strong run, there is likely further upside, and the company’s earnings reaffirmed my bullishness.

{kind=link}

In the company’s fiscal third quarter , Lennar earned $3.91 in adjusted EPS on revenue of $8.7 billion. This handily bested consensus by $0.38 cents and $200 million, respectively as deliveries were solid and margins held in relatively well. Now, earnings were lower than the $5.18 reported a year ago while revenue was down 2%. Last summer was just when the Federal Reserve was accelerating its interest rate tightening and represented a peak in the housing market, so some deterioration vs those levels was to be expected (however as discussed below, we are seeing signs the worst of the weakness in the housing market has passed).

Lennar reported that deliveries rose 8% to 18,559 as construction times have fallen by 32 days as supply chain issues fade. The average sales price fell by about 8.5% to $448,000 vs $491,000 last year. Some of this is due to weaker market conditions, but also a mix shift to lower priced homes, amidst higher mortgage rates, played a role. Given the decline in sales prices, gross margins were solid at 24.4%, down 480bp as material costs have fallen, helping to offset prices.

For perspective, Lennar earned more in this one quarter that it did in all of 2017 —if this is a housing market downturn, the company is weathering it extremely well. Additionally, there are signs that activity is picking up. New orders rose an impressive 37% to 19,666 with the value up 30% to $8.6 billion. Buyers are coming back into the market, after adjusting to higher interest rates. Notably, orders were about 1,000 units above deliveries, meaning Lennar expanded its backlog.

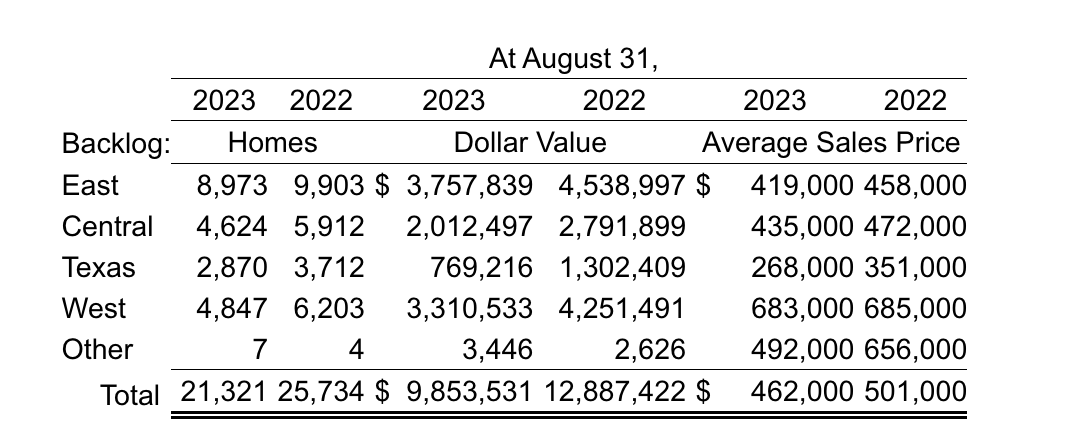

Indeed, that backlog is now 21,321 homes, worth $9.9 billion. As you can see below, the average sales price in its backlog is $462k—above last quarter’s price, which is consistent with macro data showing improving pricing in the housing market (more below).

{kind=link}

This backlog helps to insulate the company from periods of weak sales as it can deliver and work down the backlog first. Indeed, it has done that to an extent over the past year, bringing down its backlog by 4,400. This enables Lennar to keep production rates steadier than the fluctuations in sales. Notably, it could run down the backlog at this pace for another 5 years before exhausting it. That provides a substantial cushion against weakness in the market.

In Q4, per management guidance, deliveries should rise to about 22,000 and gross margins should be flat to up 20bp sequentially. This should drive EPS of at least $4,50-$4.75, and full year earnings past $13.50.

Critically, the company has also taken advantage of the boom in housing the past three years to build a fortress balance sheet. It is carrying $3.9 billion in cash and equivalents, and homebuilding debt to capital is just 11.5%, an historic low. It repurchased $366 million of stock and $475 million of debt in the quarter. This continues the strategy of reducing both debt and the share count, which it has steadily done at much lower prices than where the stock is today. Since the end of 2019 , the number of shares outstanding is down over 10%.

This steady share count reduction enables faster EPS growth than underlying earnings growth. Its extremely low debt level protects the company from a downturn. Equally importantly, it gives the company tremendous financial flexibility. It can take advantage of stock market downturns to increase the pace of buybacks, or it can use that flexibility to buy land options or even consider M&A during times of stress. With its balance sheet, Lennar can be patient and is positioned to be a buyer when others are forced to sell.

In my view, we can expect the company to continue to report run-rate results in line with Q3 (which is what the Q4 guidance suggests), as home prices have broadly stabilized, and buyers’ demand has been more resilient than many expected. Improved construction times and costs also help to protect margins and provide some offset from weaker demand. Its lower share count and interest expense also help to support EPS, and accordingly, I expect 12-month forward results to be in the $13-$13.50 range that the company is set to earn in fiscal 2023.

Now, housing is a very macro-driven sector, and so even with these strong results, you may be concerned that the outlook for the market is too negative to invest in Lennar. Let me address those concerns and explain why I am structurally bullish on US housing.

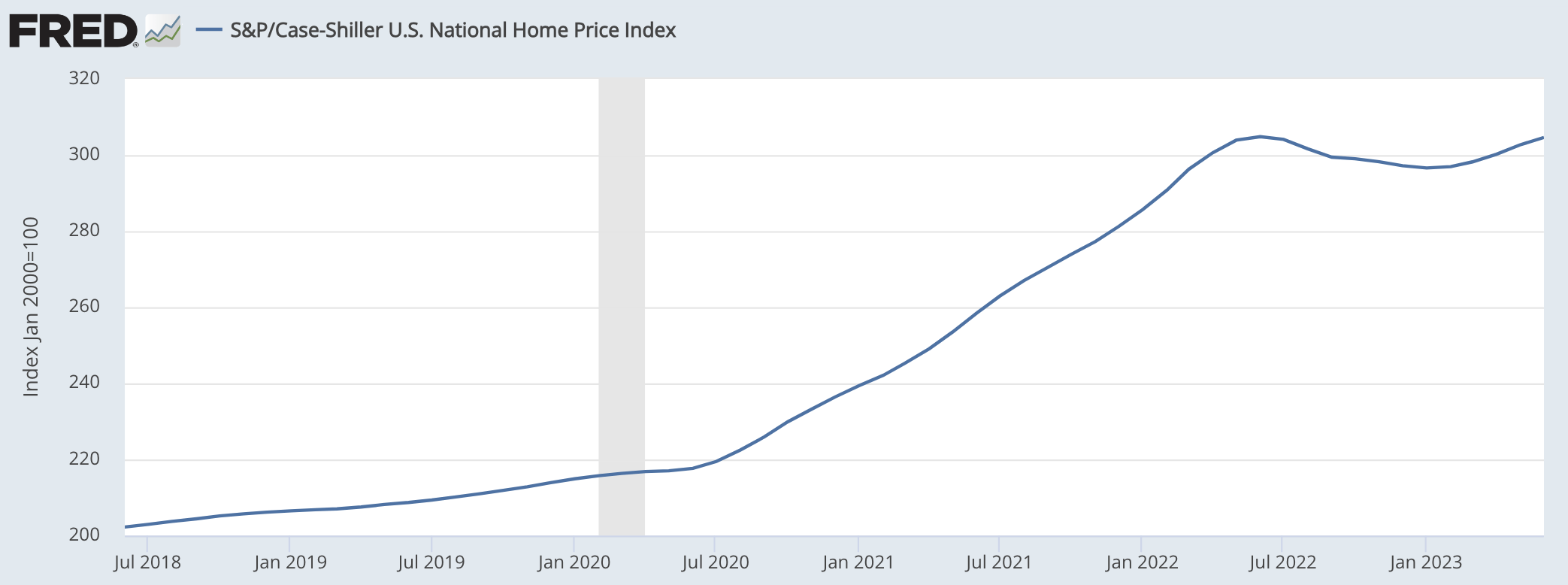

Last summer when the Fed began aggressively raising rates to combat inflation, we saw home prices began to fall, after an extraordinary run since COVID. This interest rate shock essentially caused buyers to take a step back from the market. However, after this initial reaction, buyers re-emerged, perhaps having to reset expectations for what they could afford, and we have seen prices start to tick back up in recent months

{kind=link}

There are a few reasons for this. First, while there was so much focus on how much higher rates impact buyers, they also impact sellers. Many households bought or refinanced their mortgage to a rate below 4% from 2020-2022. If you sell your house to buy another, you will be paying back a low-rate mortgage to take out a loan of over 7%. This strongly encourages people to stay in their current home, unless they absolutely have to move. On a $300,000 30-year mortgage at 3%, the monthly payment is about $1,265. At 7%, it is $1,995. That is nearly $9,000 per year in higher payments. That is a strong incentive to stay put.

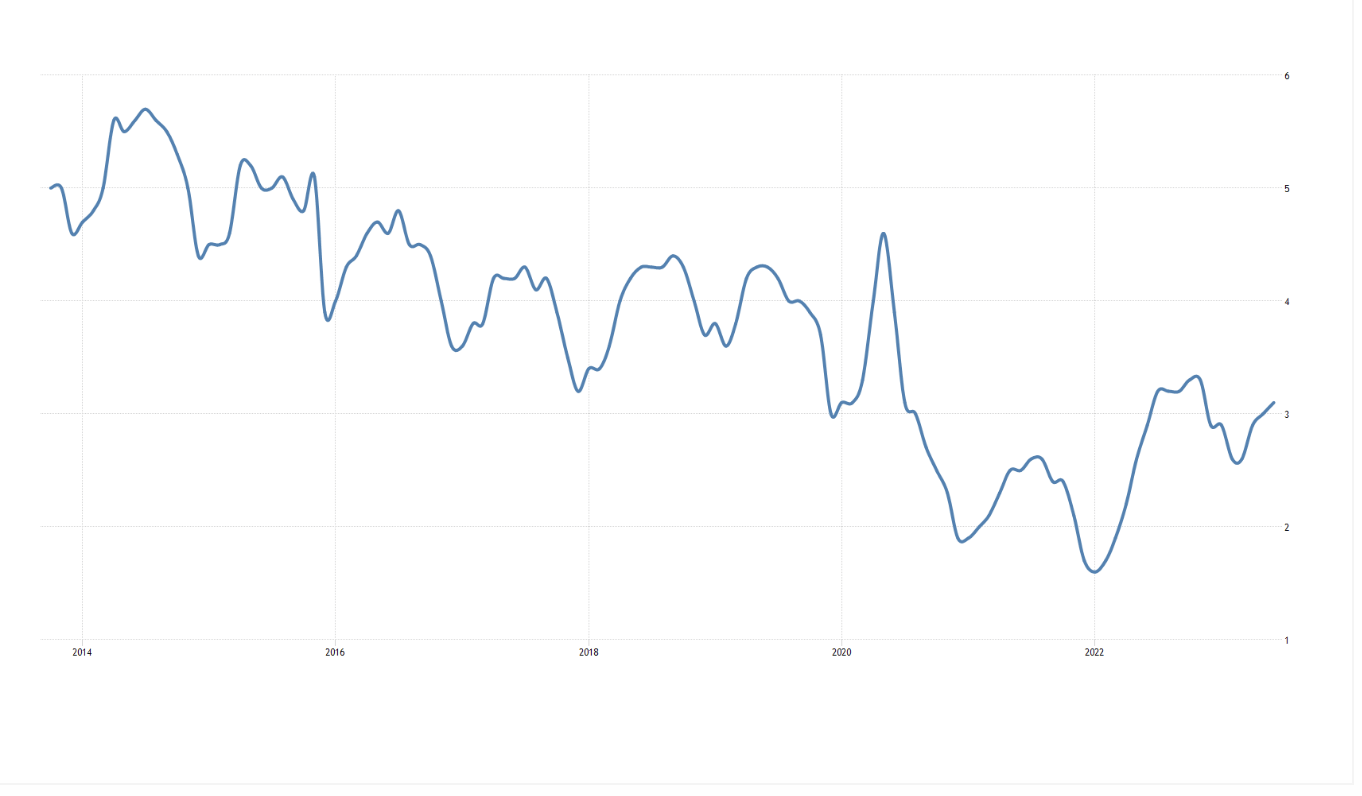

The sharp rise in rates has left many homeowners with “golden handcuffs’—extremely attractive mortgages that essentially lock them into their current home. This has kept inventory very tight, and tight inventories generally support prices. As you can see below, the monthly supply of existing home inventory remains well below its pre-COVID norm, even with the rise since 2022.

{kind=link}

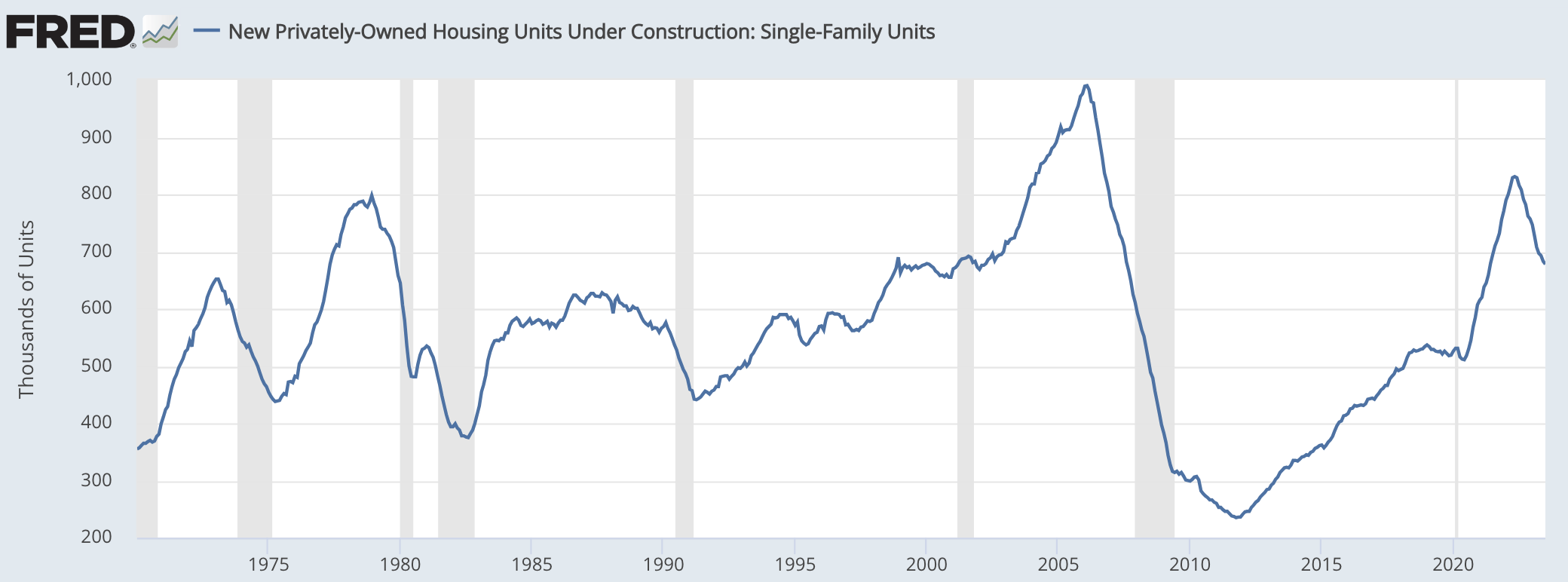

Aside from limiting existing home inventory, higher rates have reduced new home inventory Homebuilders were deeply scarred by the 2008 crash of the housing bubble and were likely worried higher rates could cause a sharper downturn in the housing market than materialized. Accordingly, as you can see below, we saw a large pullback in houses under construction starting last year. This reduction in new home supply after the surge in home construction after 2020 helped to keep inventories tight and support prices.

{kind=link}

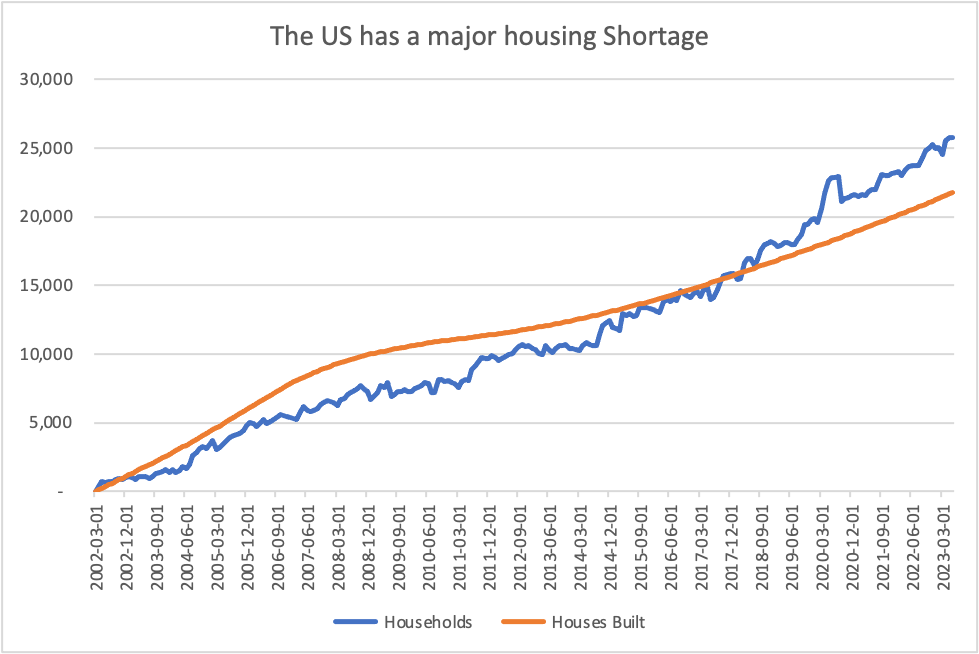

Importantly, this comes against the backdrop of a market that is structurally tight—America simply has too few houses. As you can see below, over the past twenty years, we have created 4 million more households than houses. In the boom of the 2000s, we were building more houses, but with the sharp drop in construction after 2008, households caught up and eventually surpassed the number of houses built.

Census Bureau, My Own Calculation

{kind=link}

Particularly with millennials entering their 30s, a prime time to become a homeowner, there is significant structural demand in the housing market, and the supply side has not kept up. This is a reason, in my view, why the market has proven so durable despite the worries about higher rates. Fundamentally, it is good to operate in a market that is operating in a supply shortage—that keeps prices strong and profit margins wider. Given the magnitude of the shortage, this imbalance is likely to last several years in my view.

This is exactly the environment Lennar faces. It is why I believe the company can keep posting solid results well beyond this quarter. At less than 9x earnings, shares are discounting a meaningful decline in profits that I do not view as likely. With its strong cash flow, the company can keep reducing its share count aggressively, further supporting EPS. Just as shares performed well this past year, as earnings held up better than feared, I expect the same to occur over the next 12 months. Given the structural support for housing leading to resilient earnings, I can see shares trading to 12x earnings of about $13 or about $156, representing 33% upside, as the market realizes Lennar and its stellar balance sheet are not as cyclically exposed as some fear. This assumes no shift in Fed policy—if rates were to come back down, we could see even more buying demand and higher EPS. Even after their rally, Lennar shares have more room to run, and I would be a buyer here.

For further details see:

Lennar: Strong Earnings And A Resilient Housing Market Make It A Buy