LEN - Lennar: Too Risky To Commit Capital In This Sector

2023-11-25 01:01:46 ET

Summary

- The company's financial position is strong, with a high cash balance and low debt, but uncertainties in the economy warrant a hold rating.

- The company's current ratio is high due to inventory levels, but a focus on selling complete homes will improve cash flow.

- The company has exhibited decent growth and improved margins, but future profitability and efficiency may be affected by economic conditions and declining home sales.

Investment Thesis

Lennar Corporation (LEN) is about to report FY23 results in a couple of weeks. I wanted to look at the company's financial position and give some comments on the outlook. The company seems very efficient and will weather the uncertainties of the economy quite well in my opinion, however, because of these uncertainties I will be staying on the sidelines for now and I am assigning a hold rating until we get some more clarity.

Financials

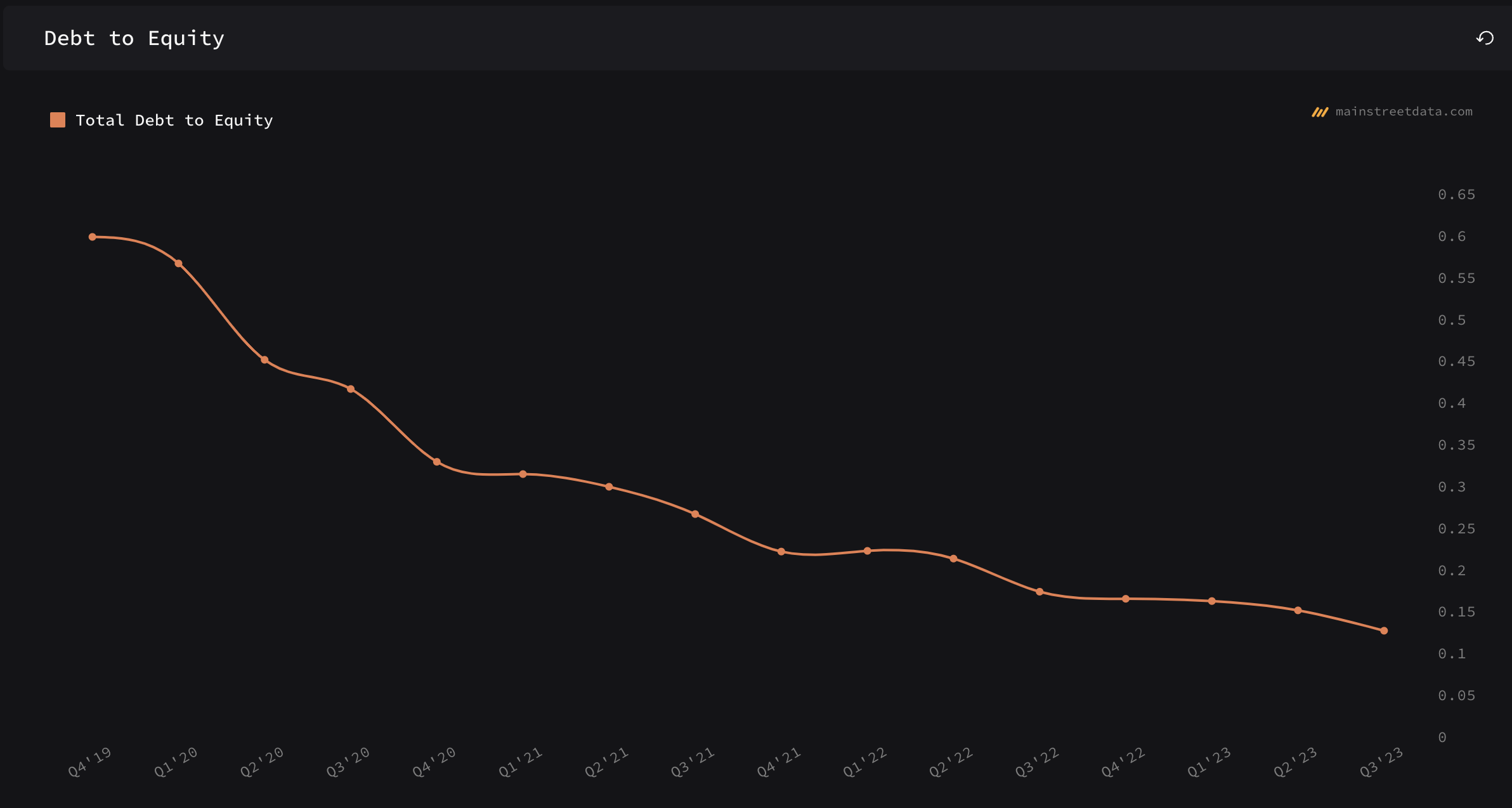

As of Q3 '23, the company had around $4B in cash and equivalents, against $3B in long-term debt. The interesting part is, that the company isn't paying any interest expense on it, or at least it is not reflected in its income statement. Lennar has been paying down its outstanding debt steadily over the years, which is good management, and given that it seems like the company's not paying any interest on it, the company is at no risk of insolvency at this point. Its debt/equity ratio has also been steadily due to repayments, and it looks like the company is not heavily leveraged anymore.

Debt to Equity (MainStreetData)

{kind=link}

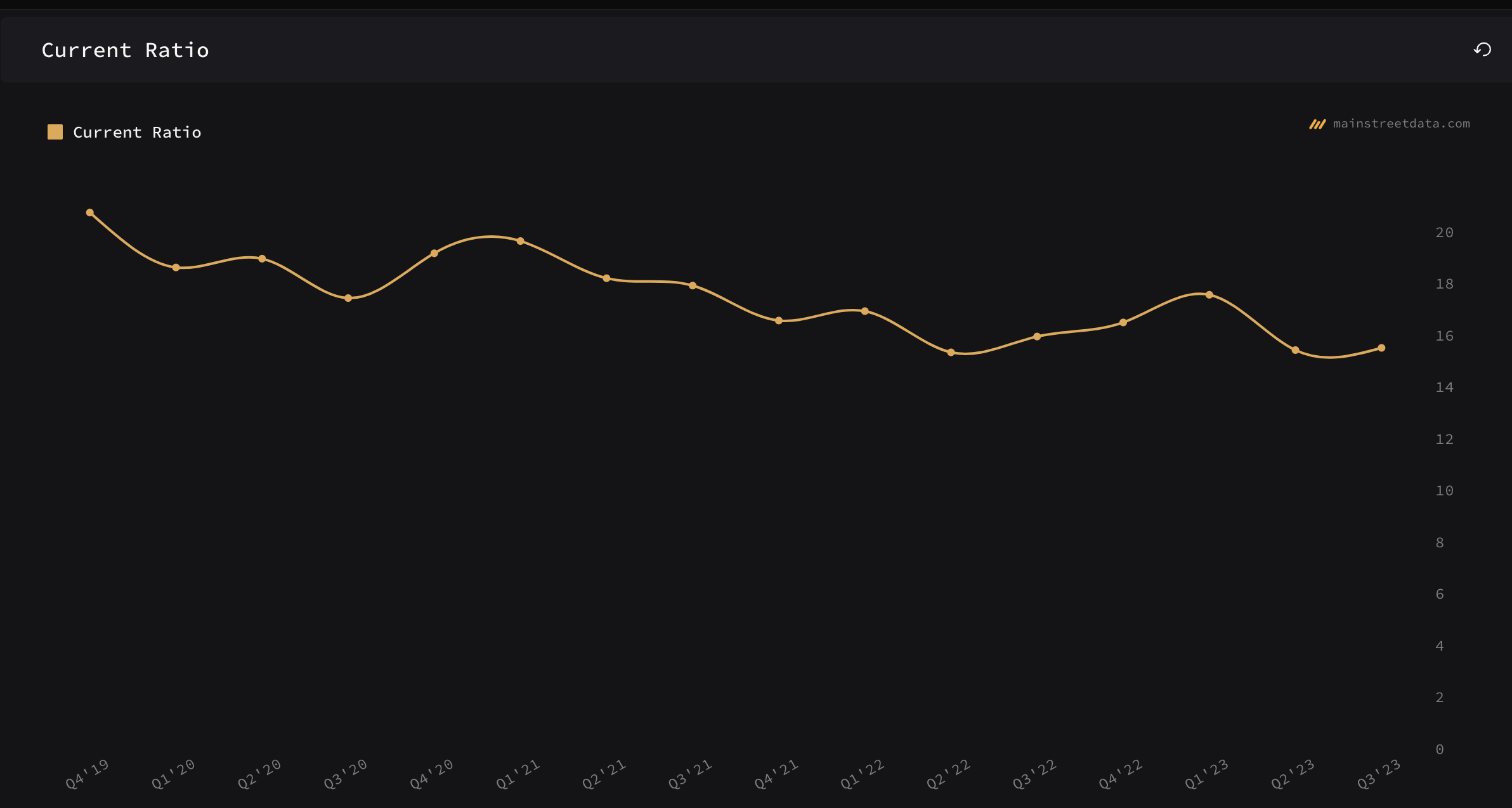

The company's current ratio is very high due to inventory levels. It is not particularly bad; however, I feel it is inefficient use of assets in my opinion. The company is going to start focusing on selling homes that are complete and closable, rather than on homes that will be sold much further out in the future. I like this initiative as it will bring an increase in inventory turnover in the future, which will improve the company's cash flow.

Current Ratio (MainStreetData)

{kind=link}

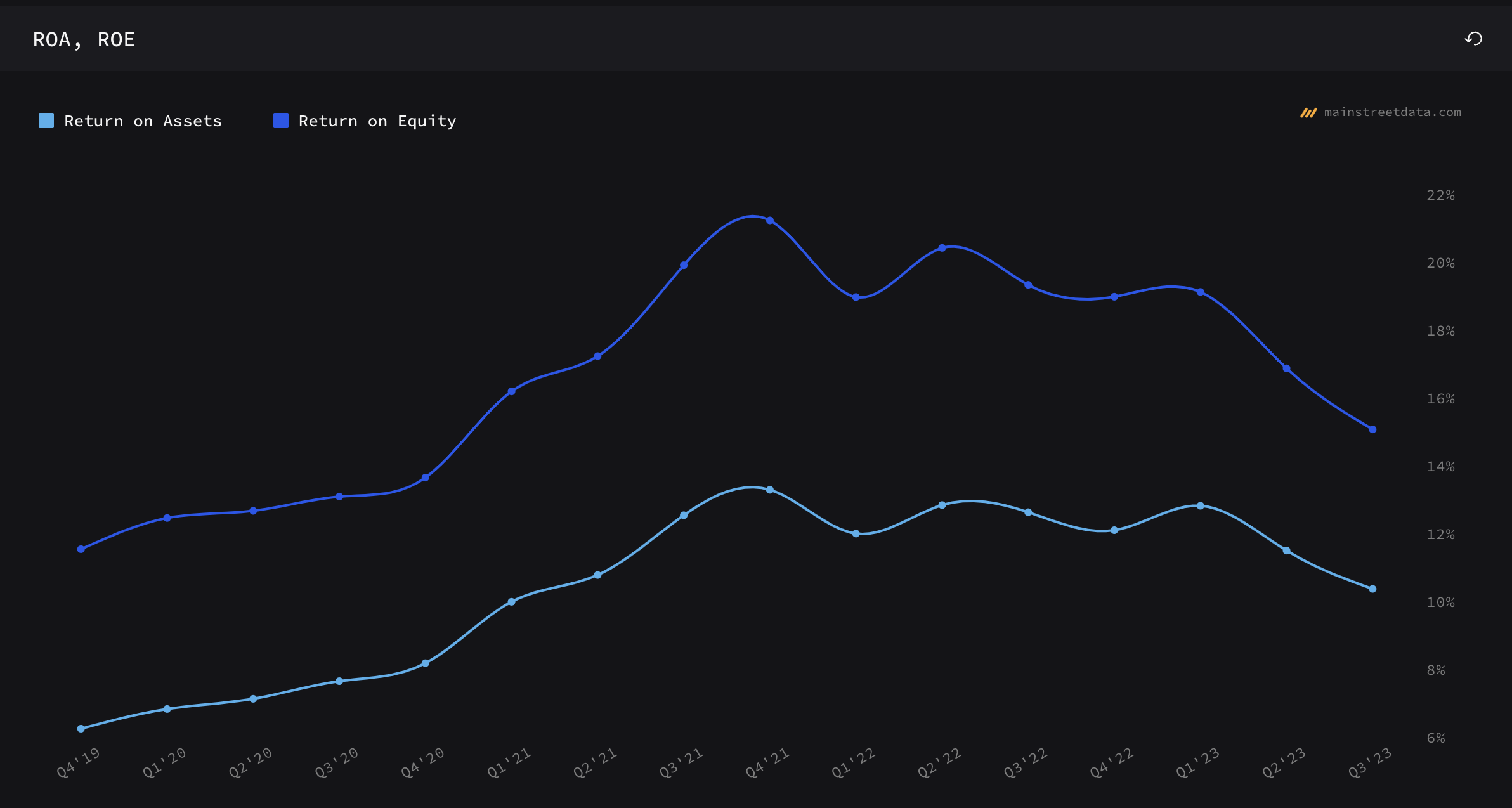

In terms of efficiency and profitability, the company's ROA and ROE have seen a slight decline in recent quarters; however, these are still quite healthy. The slight decrease in these metrics can be attributed to an increase in total assets coupled with lower net income levels over the last few quarters compared to the prior year, mostly because of an increase in inventory. Nevertheless, the company seems to be quite efficient in using its assets and shareholder capital.

{kind=link}

The company's historical return on invested capital has been in an uptrend for the last 5 years and it looks great if we just look at the company by itself. If we add on the competition, we can see that LEN has the lowest return compared to the competition selected by Seeking Alpha by default. So, do with this information what you will but to me, it seems like the company is not as appealing as some of the competition below.

ROTC vs Competition (Seeking Alpha)

{kind=link}

In terms of revenues, the company grew quite nicely over the last decade, exhibiting around 21% CAGR with a massive jump in sales from FY17 to FY18, which can be attributed to a 55% increase in home deliveries and a 10% increase in prices, according to the FY18 10-K report. According to analysts , the company will see quite low revenue growth for the next 5 years. I would take these with a grain of salt since it is impossible to predict what is going to happen 2 years from now. It is easier to know what is going to happen at the end of the year as the company usually gives guidance. Macro conditions may change, and performance may be affected considerably. Will the company see similar growth going forward, so far it looks like it'll be quite low, so I will take a conservative outlook when I value the company in the later section.

{kind=link}

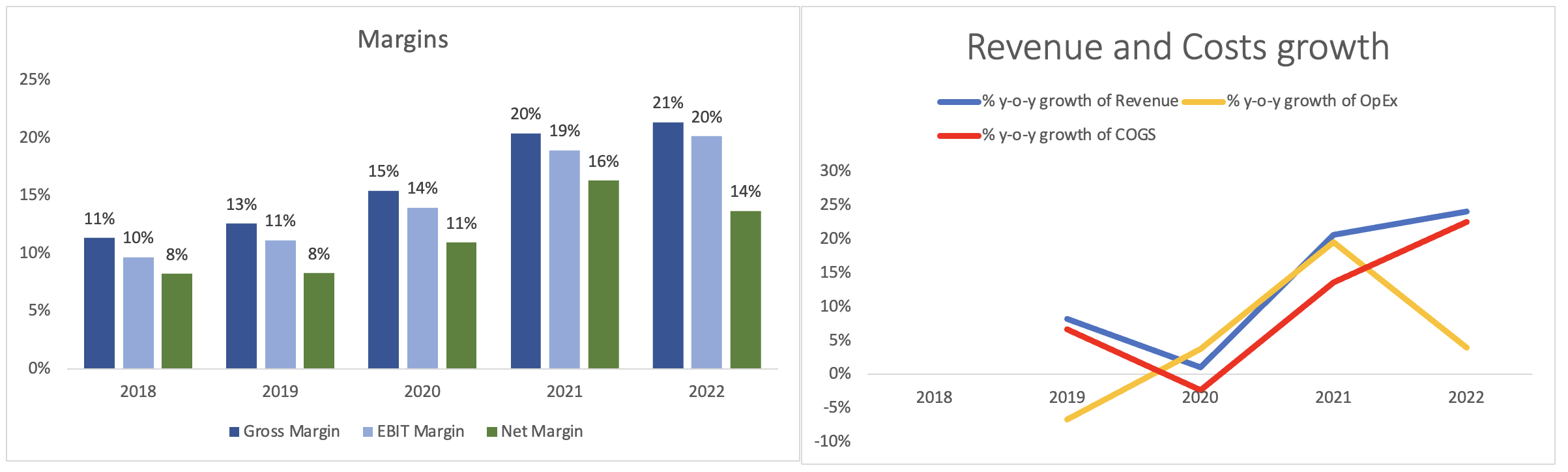

In terms of margins, these have improved considerably over the years, which can be attributed to the company's efforts to control costs. Costs in some years did not increase as much as sales did, which helped the company become more profitable recently.

Margins and Growth of Costs and Revenue (Author)

{kind=link}

Overall, it looks like the company has been doing decently over the years, however, I would expect something to give very soon, and I do expect some further dips in profitability and efficiency when the company announces its FY23 results in December.

Comments on the Outlook

In terms of economic conditions, it is not looking good in general. High-interest rates are not particularly good for people. It costs a lot more to take out a mortgage than it did just a year ago, which will put a damper on home sales as more and more people will be delaying their home purchases in hopes of interest rate cuts sometime in '24-'25. It is not out of the realm of possibility for sure. The rates will stay elevated for longer; however, we don't know how long. The average mortgage payment rose 85% from January '22 to September '23. This has affected many people's purchasing power and many people started delaying their mortgage applications. In the same article, it said that

" Mortgage applications for home purchases in mid-October fell to their lowest levels since 1995 and were 21% lower than application activity at the same point a year ago.

Existing home sales have dropped in six of the last seven months, including a 2% decline in September 2023. Over the previous year, existing home sales activity declined 15.4%."

Because of these declines, average home prices also fell, which negatively affected and will affect in the future if they continue to fall, the company's sales and margins.

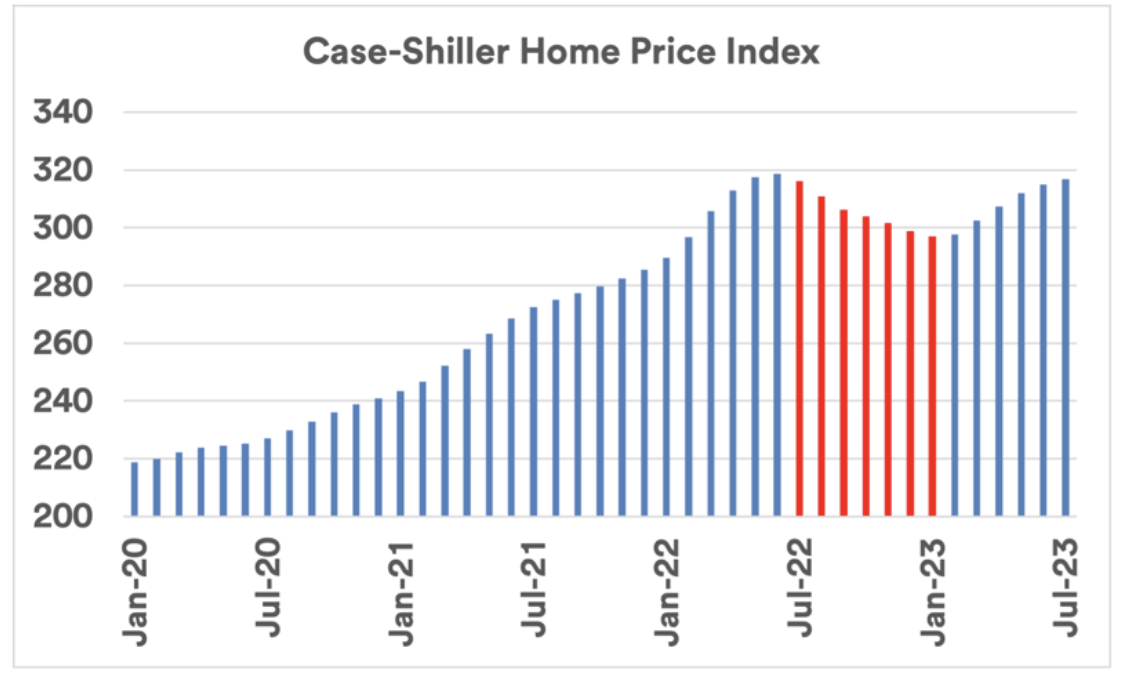

There is a light at the end of the tunnel, however. Home prices began to pick up throughout the year, which is good for LEN. It looks like people are starting to get used to the idea of higher interest rates and some of them stopped delaying the purchase of a house as they see it as a good investment and may refinance their mortgage in the later years once the rates start to come down significantly (if they will).

Price index (S&P Dow Jones Indices)

{kind=link}

I don't think this is the end of the panic. The economy is still very strong with very low unemployment numbers. Inflation may rear its ugly head again. I don't like the fact that house prices are rising again after not-so-big of a drop in a couple of months in '22. Once the unemployment rate starts to tick meaningfully up, I wouldn't be surprised to see some defaults on mortgages due to payments being too high in this environment and house prices may come back down again.

It is all a speculation on my part, but I think the outlook is not on the positive spectrum and I would be very cautious in starting a position in such a risky sector right now.

Valuation

Let's look at some assumptions. These will of course be my assumptions and yours may differ. For revenue growth, I like to be on the conservative end for an extra margin of safety. I don't think LEN will be able to achieve 21% CAGR over the next decade given the very little growth guided for FY23 and beyond (as per Seeking Alpha) and the uncertain economic outlook, which has me a little worried. Below are my assumptions for three cases, the base, conservative, and optimistic, and their respective CAGRs.

{kind=link}

Is this too conservative? Maybe, but I rather be safe than sorry.

In terms of margins and EPS, it seems that the management is doing a very good job at controlling costs, so I decided to not lower efficiency and profitability too much, however, to keep it more conservative, and to add a little extra margin of safety, below are the margins and EPS compared to FY22 numbers.

Margins and EPS assumptions (Author)

{kind=link}

For the DCF valuation, I went with the company's WACC of 10.3% as my discount and 2.5% terminal growth rate. On top of these assumptions/estimates, I decided to add a 40% margin of safety because I think the next year or so seems very choppy and the more cushion I have, the better I will sleep at night. With that said Lennar's intrinsic value and what I would be willing to pay for it to take on those risks is around $120 a share, which means the company is trading at a slight premium.

{kind=link}

Closing Comments

Your valuation may be different and that is okay. I feel this value would reflect my risk/reward appetite quite well. I am curious to see what kind of outlook the management sees for the next year when the company reports FY23 numbers in December. I don't think we have seen the end of volatility and the next half a year or so may present an even better buying opportunity. There are just too many unknowns for me right now in terms of macroeconomic conditions. Is the FED done raising rates? They seemed to be quite dovish these days, but I don't think they have ruled out future hikes if necessary. I don't think we will see cuts any time soon. House prices may continue to rise, which will eventually lead to many people not being able to afford their homes and we will start to see defaults and price drops once again.

I would like to get more clarity before committing my capital to such an uncertain sector for now. Unless the price gets very attractive, I don't mind waiting out the chaos, knowing that I got a good deal on the company for the long run.

For further details see:

Lennar: Too Risky To Commit Capital In This Sector