LNVGF - Lenovo Group: Cheap But Too Many Headwinds

2023-06-07 13:53:01 ET

Summary

- Lenovo endures another torrid quarter, led by weakness in the PC business.

- The server side has also been disappointing, with continued top-line growth outweighed by margin headwinds.

- Valuations may already have priced in a fundamental improvement following the YTD re-rating; I would be cautious here.

The bear case on Lenovo ( OTCPK:LNVGY ), a leading global personal computer (PC) vendor with a presence in servers, continued to play out in its latest quarter, which saw more earnings weakness amid PC headwinds and subpar server profitability. While management feels the PC cycle has bottomed out, particularly on the commercial side, heading into H2, this may be attributable more to a favorable YoY comparison than a cyclical upswing in PC demand. Hence, I would remain conservative on the demand outlook, particularly with economic data beginning to deteriorate globally. The artificial intelligence tailwind hasn't quite propelled the server side either, as Chinese cloud service providers continue to favor ODMs (i.e., 'Original Device Manufacturers' like Foxconn ( OTCPK:FXCOF )) over Lenovo's OEM (i.e., 'Original Equipment Manufacturer') offerings. The key upside, in my view, is Inspur's expected market share losses post-sanctions, with Lenovo one of the potential supply chain diversification beneficiaries given its customer overlap. Also appealing is the ~8x fwd P/E and attractive mid-single-digit yield, though the stock is already up ~18% YTD. This is still (mostly) a business in secular decline, however; thus, I would remain cautious pending signs of a sustained fundamental improvement.

Q4 2023 Falters Again; Cyclical Trough Not Here Yet

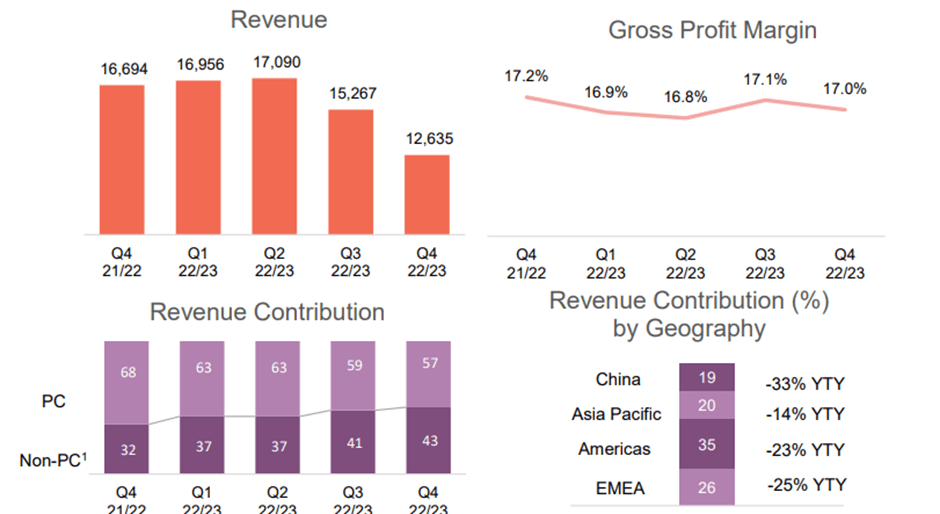

Lenovo reported disappointing March quarter results – while the group-level sales decline was largely anticipated by consensus, the 2.3% operating margin fell well short due to a continued decline in the PC business. At the group level, PC is still the main revenue contributor at 61% for the full year, though the main concern is profitability – the current 7.3% operating margin remains far above the ~5% pre-COVID margin and is, thus, vulnerable to downside. Yet, management offered reasons for optimism from here, citing positive signs of a PC market stabilization amid normalizing inventory levels by H2 2023. In line with this view, Lenovo's guidance is for a return to YoY growth in the PC business in the back half of this year, followed by a subsequent acceleration in 2024. Yet, it's hard to look past the elevated PC margin post-COVID; without a significant increase in PC demand, the segment margin is likely at risk of reverting towards pre-COVID levels in the next quarters (implying >2% margin downside).

{kind=link}

Lenovo

On the other hand, 2024 demand will benefit from the Windows 11 refresh cycle – historical cycles indicate PC demand tends to spike as the previous Windows version (Windows 10 in this case) reaches its end of life ( 2025 for Windows 10 ). Given Windows 10 currently has an outsized >70% market share vs. other Windows operating system versions, the coming refresh cycle presents a major tailwind, particularly for commercial models. That said, stocks are valued based on underlying cash flows into perpetuity. Net against the structural PC headwinds, one year of elevated shipments likely won't be enough to offset near-term margin headwinds or a long-term revenue decline.

Promising Mid to Long-Term Server Prospects; Profitability Remains Below Par

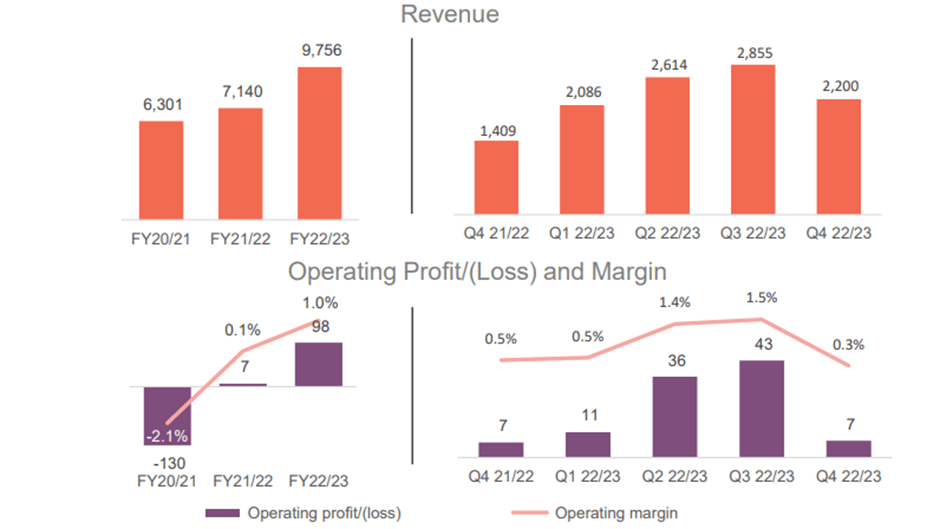

While the server business growth was strong at +37% YoY, operating margins were a letdown at 0.3% (below the 1.5% last quarter). While $249mn of one-off restructuring fees impacted the segment P&L, a deteriorating IT spending backdrop also weighed on results, along with higher R&D investments. Management also noted progress on the AI side via offerings like 'Premier Support Plus' for customer service and 'Digital Workplace Solutions' for remote working, though any near-term impact is likely minimal. Key to monitor will be Lenovo's progress in penetrating Chinese cloud service provider demand – given they tend to opt for ODMs (vs. Lenovo's OEM offering) to fulfill their AI-related server needs, Lenovo doesn't benefit from a meaningful AI tailwind. This leaves the company exposed to both a macro-driven slowdown and reprioritization of tech budgets toward AI, so unless the company makes meaningful headway in China (albeit at lower margins given the more competitive Chinese market), the segment top-line could come under pressure.

{kind=link}

Lenovo

Building market share in China is important because of the sanctions placed on market leader Inspur earlier this year (added to the US Department of Commerce's Entity List). In effect, Inspur will need to be licensed by the US government (reviewed under a 'presumption of denial') to acquire US-origin items, putting it on the back foot in the server race. Given Inspur's outsized >30% share in the Chinese server market (vs. high-single-digits for Lenovo) and its overlapping customer base with Lenovo (including blue-chip Chinese internet names like Alibaba ( BABA ) and Tencent ( OTCPK:TCEHY )), the company is well-positioned to benefit. Capturing share won't be straightforward, though, given players like H3C and Foxconn) offer similar, if not better, continuity. Plus, uncertainties remain about any second-order impacts – similar restrictions on other Chinese server producers, possibly even Lenovo, could be a possibility down the line, along with a shift away from US server players like Dell should a tit-for-tat ensue.

Cheap, but Too Many Headwinds

Lenovo's latest quarter did little to invalidate the secular bear thesis, as earnings continued to be pressured across the PC and server businesses. While management could be right about a cycle bottom for PCs in H2, the sustainability of a fundamental PC recovery (vs. favorable YoY comps) post-Windows 10 refresh cycle remains a concern. Server demand is another concern heading into a global slowdown, though supply chain diversification benefits following Inspur's sanctions earlier this year could provide some offsetting benefit to Lenovo. It may not be sufficient to offset the PC end-demand softness and continued inventory digestion, though, particularly with management moving the H2 bar higher post-quarter. Having also re-rated this year despite its core PC revenue base headed for secular decline, I would remain cautious at these levels.

For further details see:

Lenovo Group: Cheap But Too Many Headwinds